Рынок государственных облигаций Японии переживает беспрецедентные за последние десятилетия потрясения, заставляя глобальных управляющих активами вновь оценить давно игнорировавшийся риск: могут ли японские инвесторы, владеющие казначейскими обязательствами США на сумму около $1 трлн, вернуть свои деньги на родину?

Согласно последнему отчету британской Financial Times, ряд инвестиционных компаний уже начали готовиться к возможному масштабному оттоку японского капитала обратно на внутренний рынок, делая ставку на то, что японские инвесторы начнут постепенно продавать казначейские облигации США и покупать доходность по японским государственным облигациям (JGB), которая продолжает расти.

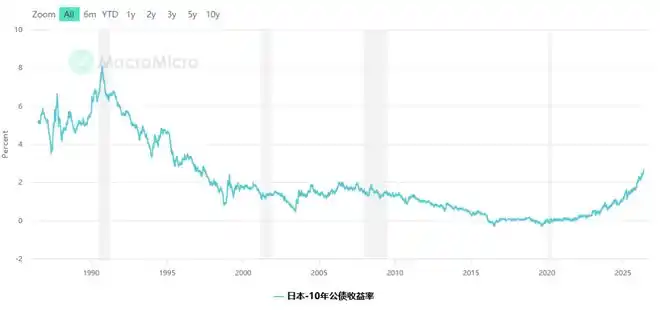

Доходность японских облигаций взлетела до многолетних максимумов

В пятницу доходность 10-летних эталонных японских гособлигаций в ходе торгов достигла 2,73%, что является самым высоким уровнем с мая 1997 года.

Доходность 30-летних японских облигаций впервые превысила 4% — уровень, которого бумаги этого срока не достигали с момента их первого выпуска в 1999 году. На этой неделе доходность 5-летних и 20-летних облигаций также обновила исторические рекорды.

Министр финансов Японии Сацуки Катаяма в пятницу заявила журналистам, что доходность государственных облигаций на основных мировых рынках растет: «Эти динамические процессы взаимно влияют друг на друга, создавая кумулятивный эффект».

Аналитики ожидают дальнейшего роста доходности японских облигаций. В декабре прошлого года Банк Японии повысил ключевую процентную ставку до 0,75%, что стало самым высоким уровнем за 30 лет, и рынки в целом ожидают нового повышения на 25 базисных пунктов до 1% в июне этого года.

Логика триллионного «возвращения на родину»

Чтобы понять эту ставку, необходимо понять, почему японские инвесторы держат за рубежом такие огромные активы.

На протяжении последних десятилетий в Японии сохранялись сверхнизкие процентные ставки, а внутренние облигации практически не приносили доход. В погоне за доходностью японские институциональные инвесторы, такие как страховые компании, пенсионные фонды и банки, в массовом порядке выходили на зарубежные рынки, покупая казначейские обязательства США, европейские облигации и другие глобальные активы.

В настоящее время японские инвесторы владеют казначейскими обязательствами США на сумму около $1 трлн, что делает их крупнейшими иностранными держателями американского госдолга, значительно опережая другие страны.

Теперь, по мере резкого роста доходности японских облигаций, эта логика меняется на противоположную. Главный инвестиционный директор британской компании по управлению активами BlueBay Марк Доудинг прямо указал на этот сдвиг. BlueBay только в марте этого года запустила свой первый фонд японских облигаций.

Доудинг заявил: «Новые средства больше не будут размещаться за рубежом. Они не пойдут ни в корпоративные облигации США, ни в казначейские обязательства США, а будут размещены обратно внутри Японии».

Капитал уже начал возвращаться «тонкой струйкой»

Данные рынка показывают, что признаки возвращения капитала уже появились, хотя масштабы пока невелики.

Согласно данным исследовательской компании EPFR, в марте этого года инвесторы вложили в фонды японских суверенных облигаций чистые $7 млрд, что стало самым большим месячным притоком с момента начала ведения записей по этой категории. В апреле чистый приток составил $86 млн, вернувшись к недавнему нормальному уровню.

Менеджер фонда Ruffer Мэтт Смит дает более прямой прогноз. Он заявил: «Давление нарастает — доходность на длинном конце внутреннего рынка продолжает расти, и институциональные сигналы тоже говорят: "Пожалуйста, верните деньги в Японию". Мы считаем, что укрепление иены сначала будет происходить медленно, а затем внезапно ускорится».

Смит также отметил, что Ruffer в настоящее время держит длинные позиции по иене в качестве основного хеджирующего инструмента. «Как только на рынках возникнет нестабильность, особенно с центром на американском кредитном рынке, и японские инвесторы начнут возвращать капитал на родину, иена укрепится».

Массовый отток еще не начался, и у самих японских облигаций есть скрытые риски

Однако аналитики предупреждают, что японские институциональные инвесторы на самом деле все еще являются чистыми покупателями иностранных облигаций.

Аббас Кешвани, макростратег по Азии в RBC Capital Markets, указывает, что, хотя доходность японских облигаций уже «формально предлагает инвесторам лучшую компенсацию», за последние 12 месяцев японские инвесторы все еще были чистыми покупателями иностранных облигаций на сумму около $50 млрд.

Причина заключается в неопределенности на самом рынке японских облигаций. Премьер-министр Японии Санаэ Такаити выиграла выборы в феврале этого года, и ее предвыборные обещания включали увеличение государственных расходов и субсидии для смягчения инфляционного давления. Аналитики все чаще предупреждают, что правительству позже в этом году придется составлять дополнительный бюджет, что еще больше снизит цены на японские облигации и повысит их доходность.

Кешвани заявил: «И динамика спроса и предложения указывают на дальнейший рост доходности. Как инвестору, если вы знаете, что доходность будет продолжать расти, сейчас трудно найти желание покупать».

Ранее Банк Японии, будучи крупнейшим покупателем на рынке, активно скупал японские облигации посредством количественного смягчения и политики контроля кривой доходности. По мере того как Банк Японии постепенно сворачивает эти меры, и рынок возвращается к традиционной логике спроса и предложения, волатильность цен на японские облигации заметно усилилась.

Что это означает для рынка казначейских обязательств США

Потенциальный масштаб возможного возвращения японского капитала заставляет рынок казначейских обязательств США серьезно отнестись к этому риску.

Япония является крупнейшим иностранным держателем казначейских обязательств США с объемом владения около $1 трлн. Если японские институциональные инвесторы начнут систематически сокращать свои позиции, воздействие на баланс спроса и предложения на рынке американских гособлигаций будет существенным.

В настоящее время ставки Уолл-стрит больше носят упреждающий характер и не являются реакцией на уже свершившийся факт. Но по мере того, как доходность японских облигаций продолжает расти — аналитики рассматривают достижение доходности 10-летних японских облигаций на уровне 3% позже в этом году как реалистичную цель — логика этой ставки будет становиться все более очевидной.