Автор: Artemis

Компиляция: Shenchao TechFlow

Введение Shenchao: Уолл-стрит рассматривает Coinbase как брокера, следующий за взлётами и падениями биткойна, и даёт ей вдвое меньшую оценку, чем Circle. Однако данные показывают, что 92.8% платежей, совершаемых ИИ-агентами, происходят на Base, а 99.8% расчётов ведутся в USDC. Coinbase уже стала базовой инфраструктурой для нативных финансовых операций с ИИ, а не просто биржей. Если прогноз McKinsey о том, что объём торговли через ИИ-агентов к 2030 году достигнет $5 трлн, сбудется хотя бы наполовину, логика оценки Coinbase будет переписана.

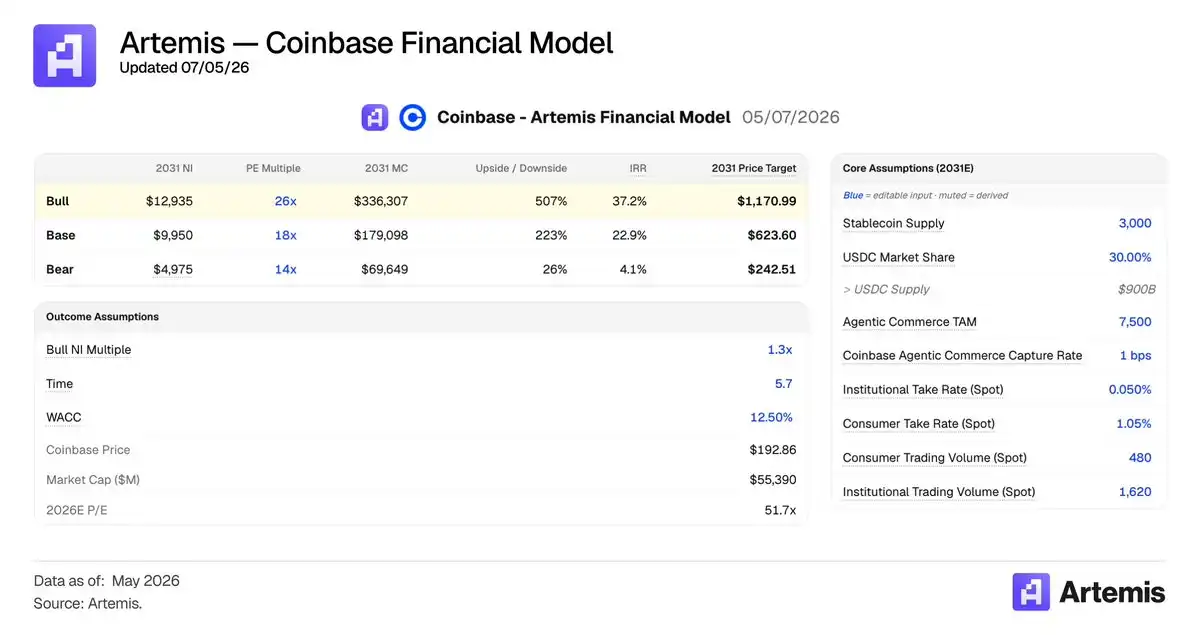

Бычий сценарий: Coinbase станет компанией с капитализацией $300 млрд к 2031 году

Ключевой тезис: Большинство рассматривает Coinbase как криптоброкера, чья активность зависит от биткойна и объёмов криптотрейдинга. Этот узкий взгляд упускает долгосрочный потенциал роста Coinbase. В мире, где предложение стейблкоинов к 2031 году достигнет $3 трлн, а объём торговли через ИИ-агентов — $5 трлн, Coinbase как со-создатель USDC (по льготному соглашению о распределении с Circle) и создатель x402 и Base (где в основном происходит эта торговля), получит огромную ценность.

Введение

Artemis — исследовательская компания в области цифровых финансов, специализирующаяся на данных из блокчейна. Мы помогали McKinsey оценивать реальные объёмы платежей стейблкоинами, много писали о торговле через ИИ-агентов и цифровых финансах в 2030 году. По мере слияния криптоиндустрии и ИИ, Coinbase перестанет быть просто криптобиржей и станет расчётным, дистрибьюторским и коммерческим слоем для нативных финансовых операций с ИИ.

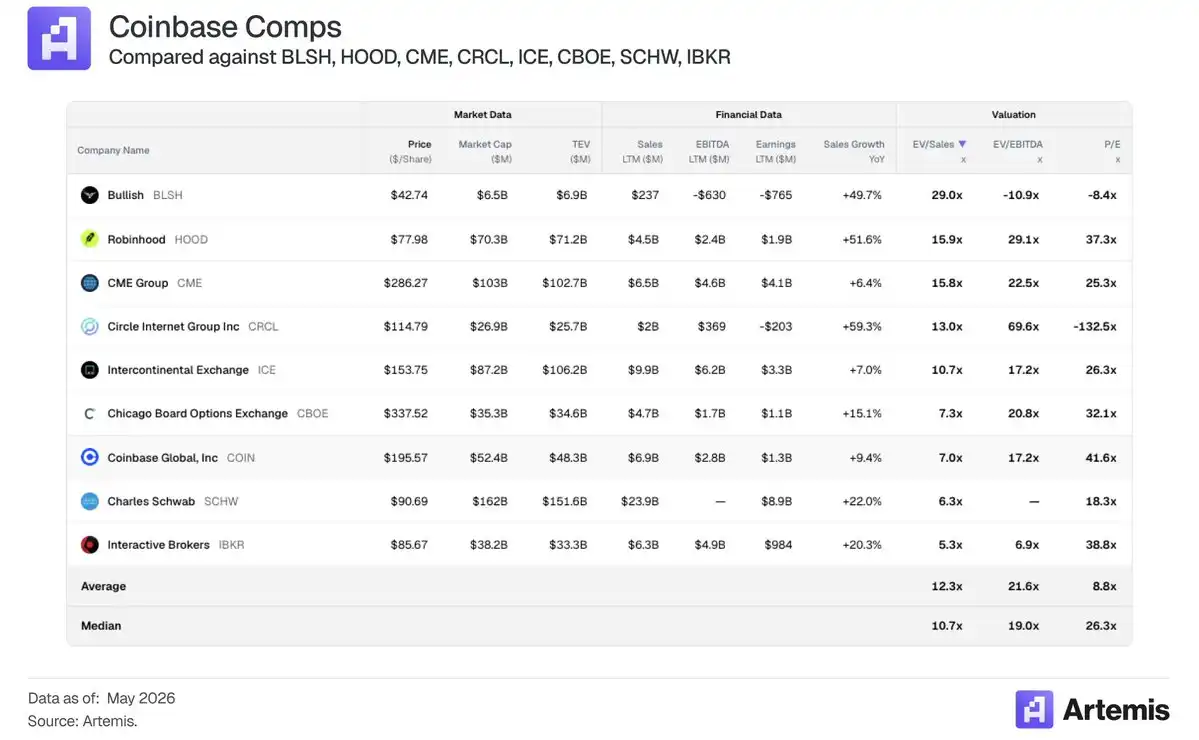

Большинство рассматривает Coinbase как циклического криптоброкера, зависящего от объёмов криптотрейдинга.

Неудивительно, что динамика Coinbase совпадает с динамикой других брокеров, таких как IBKR, Robinhood, Schwab.

В то время как Circle, как чистая ставка на рост стейблкоинов, получает гораздо более высокие мультипликаторы оценки (103.9x NTM P/E).

Coinbase может стать компанией с капитализацией $300 млрд к 2031 году (рост в 6 раз от сегодняшнего уровня, CAGR 35%), став главным бенефициаром стейблкоинов и платежей через ИИ-агентов — а не просто криптобиржей. Полная модель доступна здесь.

Наши ключевые предположения:

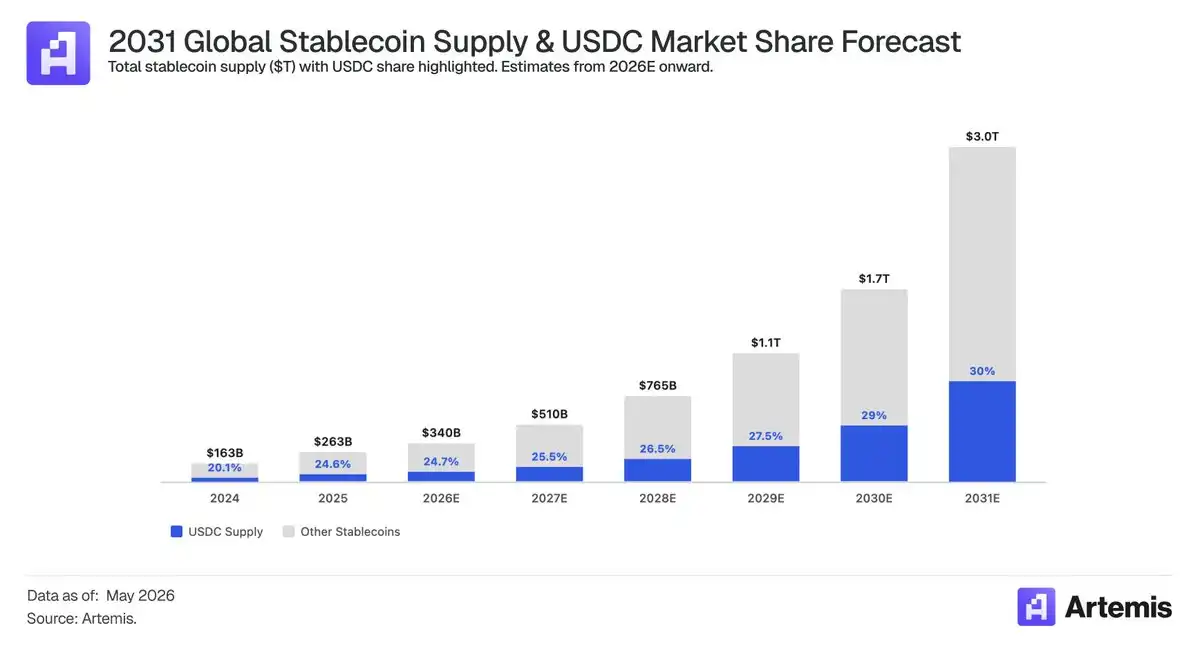

- Предложение стейблкоинов достигнет $3 трлн к 2031 году.

- Объём торговли через ИИ-агентов достигнет $7.5 трлн к 2031 году.

- Наши предположения по основному биржевому бизнесу совпадают с рыночными — доход от транзакций около $6 млрд в 2028 году.

Рынок упускает из виду факт, что Coinbase выигрывает и извлекает пользу из двух эпохальных попутных ветров:

1. Восход стейблкоинов и глобальный спрос на цифровой доллар. Министр финансов США Скотт Бессент прогнозирует, что предложение стейблкоинов достигнет $3 трлн к 2030 году (рост в 10 раз от сегодняшнего уровня). Bain & Company считает, что предложение вырастет в 12 раз к 2030 году, до $3.8 трлн.

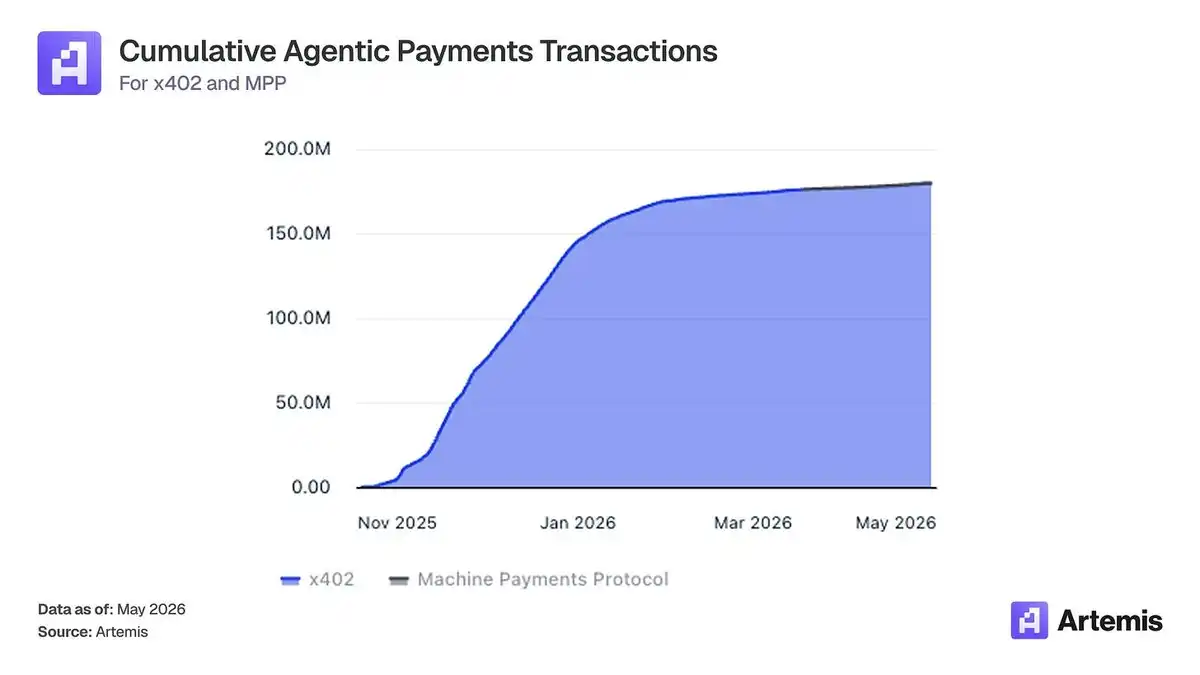

2. Восход торговли через ИИ-агентов. McKinsey прогнозирует, что глобальный объём торговли через ИИ-агентов составит $3-5 трлн к 2030 году. Мы прогнозируем, что примерно 1/3 этого объёма будет рассчитываться в блокчейне с использованием таких протоколов платежей для ИИ-агентов, как x402 и MPP. Сейчас мы наблюдаем быстрый рост платежей ИИ-агентов в блокчейне:

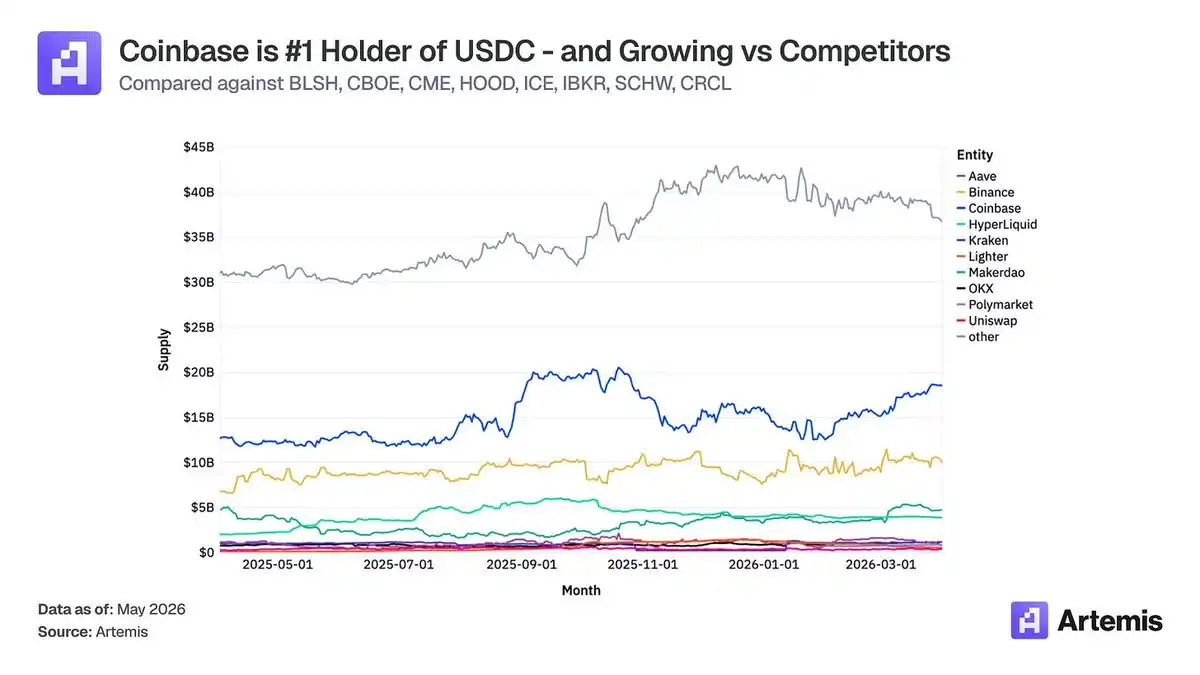

Coinbase явно выигрывает от этих двух тенденций как крупнейший и наиболее регулируемый дистрибьютор USDC, а также обладатель ведущей сети для платежей ИИ-агентов.

Даже если институциональные инвесторы скептически относятся к DeFi и считают крипто "мёртвым", Coinbase всё равно победит — не благодаря крипто и объёмам торговли, а благодаря тому, что станет самым надёжным и доминирующим платформой для стейблкоинов и инфраструктуры для платежей ИИ-агентов.

Почему Coinbase выигрывает от стейблкоинов

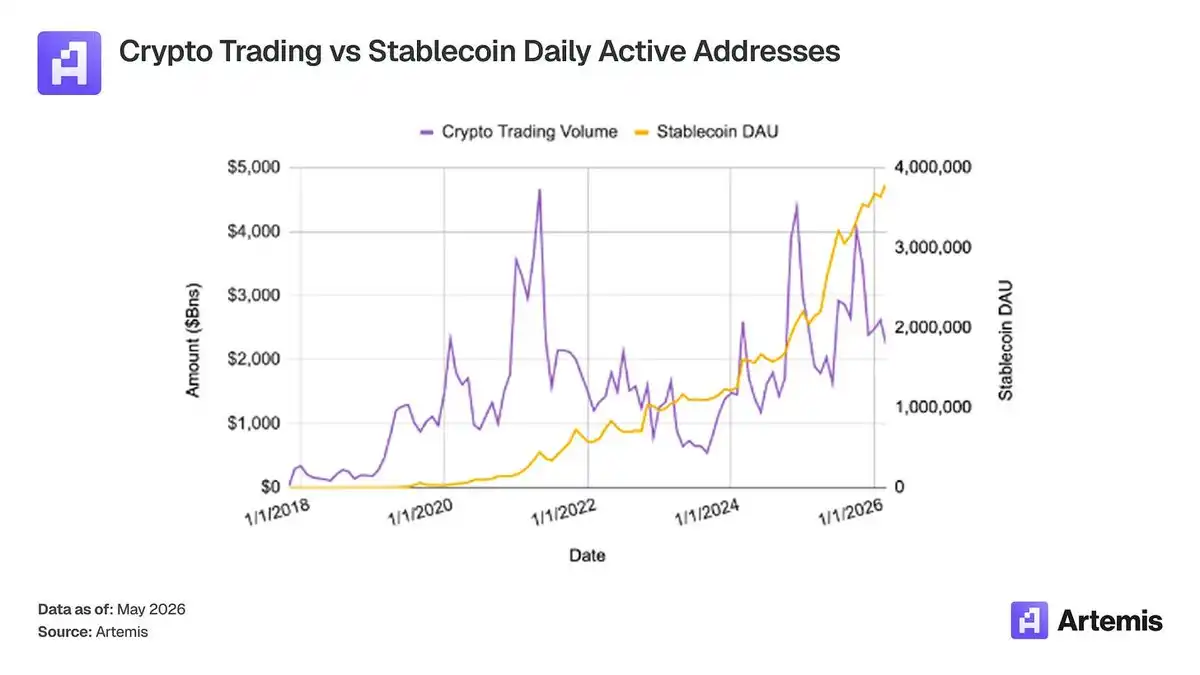

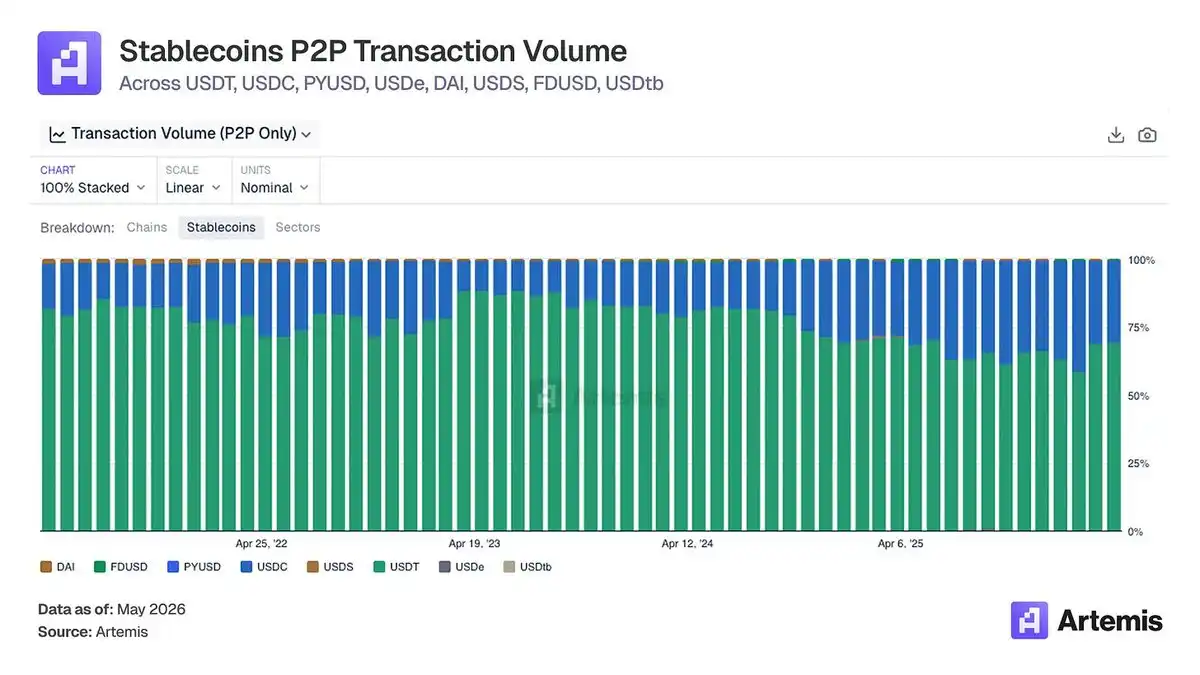

Рынок не понимает, что Coinbase — явный победитель от роста стейблкоинов. Даже при падении объёмов криптотрейдинга, использование стейблкоинов исторически показывает устойчивый восходящий тренд.

Соглашение о распределении USDC — это актив Coinbase, а не Circle. Доля дохода, которую Circle выплачивает Coinbase, выросла с 32% в 2022 году до примерно 50% за последние два года. Структурная причина проста: Coinbase зарабатывает около 100% доходности на USDC, хранящихся в её продуктах, и получает значительную долю от балансов вне платформы в рамках механизма Payment Base waterfall. По мере роста объёмов дистрибуции Coinbase (в среднем $17.8 млрд USDC в продуктах Coinbase в Q4 2025 года, рекордный показатель), растёт и её доля в водопаде.

С точки зрения инвестора, это соглашение больше похоже на то, что Coinbase передаёт на аутсорсинг регуляторные функции и управление резервами Circle, а не на то, что Circle платит Coinbase за дистрибуцию. Соглашение о сотрудничестве заключается на 3 года с автоматическим продлением при выполнении трёх пороговых условий (продукт, компания, дистрибьютор). Публичные документы показывают, что при выполнении этих условий "протокол Circle не может быть прекращён". Механизм продления — не обрыв для переговоров, а продолжение фиксации. Для Circle уход означает потерю крупнейшего единого канала дистрибуции USDC. Для Coinbase, в восходящем сценарии (чёткое регулирование, способствующее масштабированию платежей стейблкоинами, значительное расширение капитализации USDC) выгода будет напрямую поступать через ту же долю в контракте. Структура контракта устроена так, что позиция Coinbase постоянно укрепляется, независимо от того, кто управляет Circle.

Будущий рост USDC

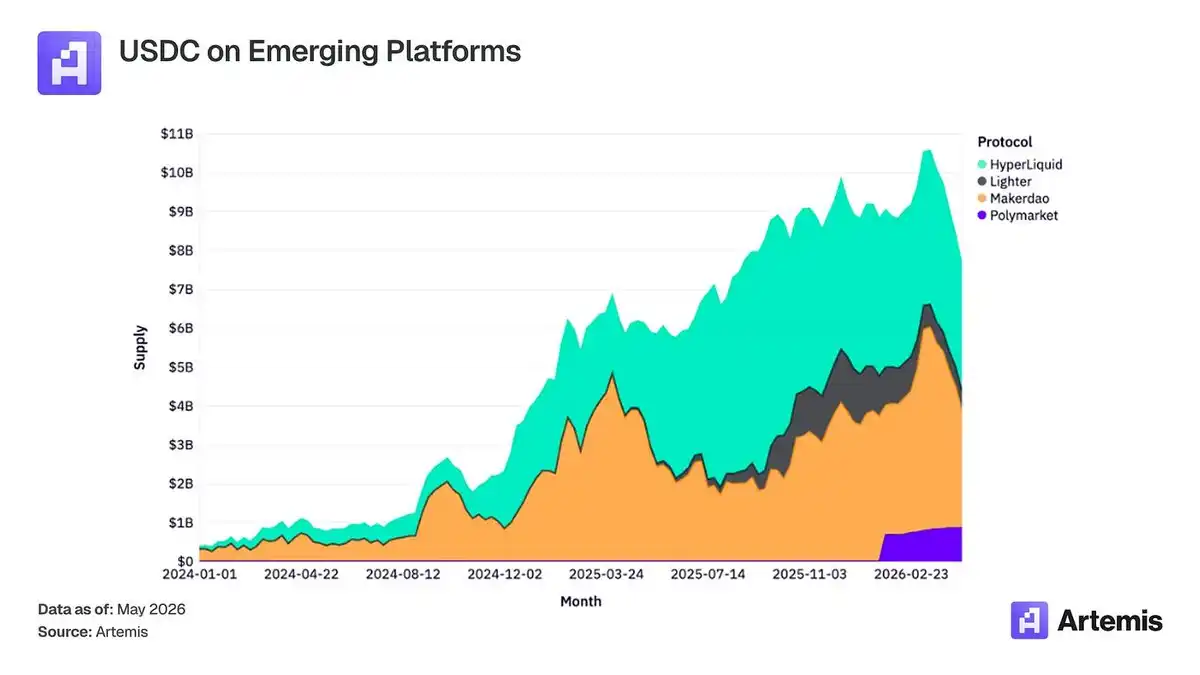

Помимо Coinbase, мы видим множество интересных случаев использования USDC, особенно в новых протоколах. Мы наблюдаем значительный рост предложения USDC в протоколах Polymarket, Hyperliquid, MakerDAO за последние два года. По мере появления новых финансовых применений на блокчейн-платформах, мы видим, что USDC продолжает использоваться в этих протоколах.

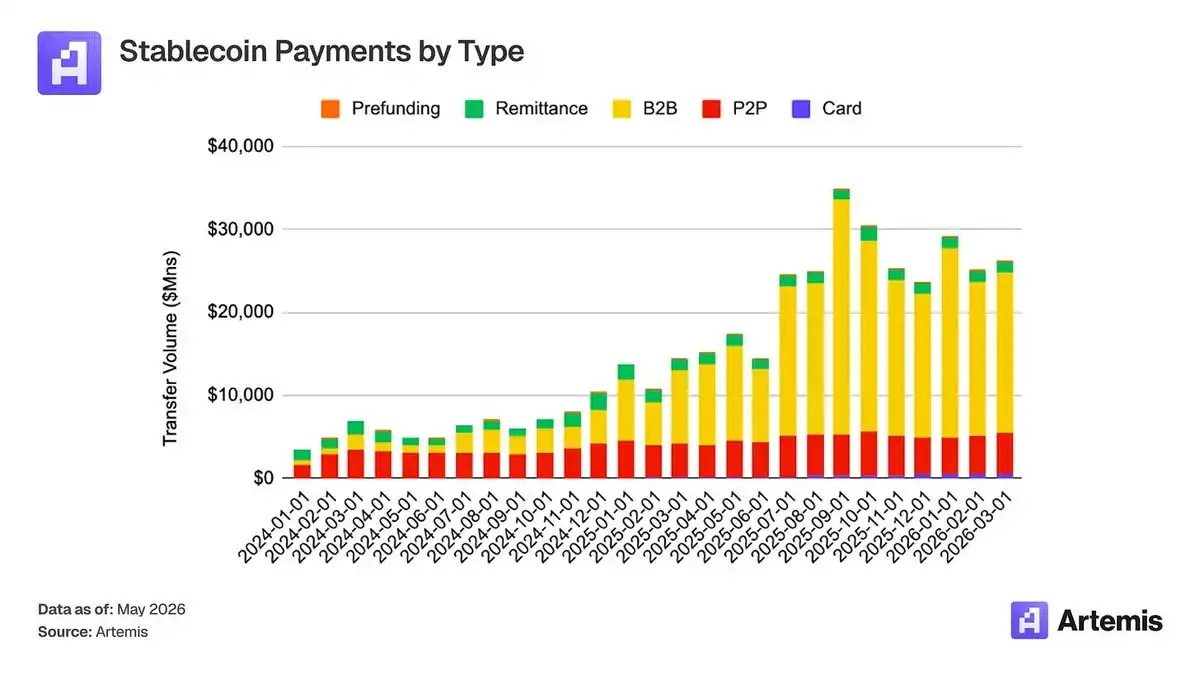

Coinbase находится в выгодном положении, чтобы захватить следующую волну использования стейблкоинов — платежи. Типы платежей (B2B, B2C) через карточные экосистемы значительно выросли за последний год, и USDC постоянно увеличивает свою долю в этих транзакциях.

Наблюдая за переводом USDC от адреса к адресу (косвенный показатель транзакций), можно увидеть, что USDC набирает долю относительно USDT.

Рынок неправильно трактует закон CLARITY?

Закон "О чёткости регулирования рынка цифровых активов 2025 года" (H.R. 3633), обычно называемый "законом CLARITY", был принят Палатой представителей США 17 июля 2025 года при двухпартийном голосовании 294-134. Этот закон создаст всеобъемлющую нормативную базу для цифровых активов, за исключением платёжных стейблкоинов. Для Coinbase закон CLARITY представляет собой важнейший ожидающий принятия законодательный акт в регулирующей среде компании, который установит в основном полную федеральную нормативную архитектуру для экосистемы цифровых активов, в которой работает Coinbase.

Закон CLARITY также имеет большее значение для экономики стейблкоинов Coinbase, чем принято считать. Потоки доходов от соглашения Coinbase с Circle о распределении и доле резервов, при текущих предположениях о процентных ставках, сопоставимы с экономической выгодой самого Circle на уровне эмитента, в то время как программа вознаграждений USDC от Coinbase вносит другой вклад, окончательный масштаб которого зависит от окончательной формулировки компромисса Тилллиса-Олсбрукса. Рынок недооценивает масштаб и устойчивость этих доходных линий, связанных со стейблкоинами, рассматривая их как придаток биржевого бизнеса, а не как самостоятельную экономику базовой инфраструктуры. Принятие закона CLARITY усиливает этот аргумент, формализуя более широкую регуляторную архитектуру для клиринга, расчётов и обращения стейблкоинов — и чётко определяя зарегистрированных посредников, через которых проходят институциональные потоки стейблкоинов. Это переопределяет бизнес Coinbase по стейблкоинам как уровень приложения регулируемой и быстро институционализирующейся системы, а не как независимую линейку потребительских продуктов, стоимость которой колеблется в зависимости от розничного объёма торговли токенами.

Почему Coinbase выигрывает в платежах ИИ-агентов

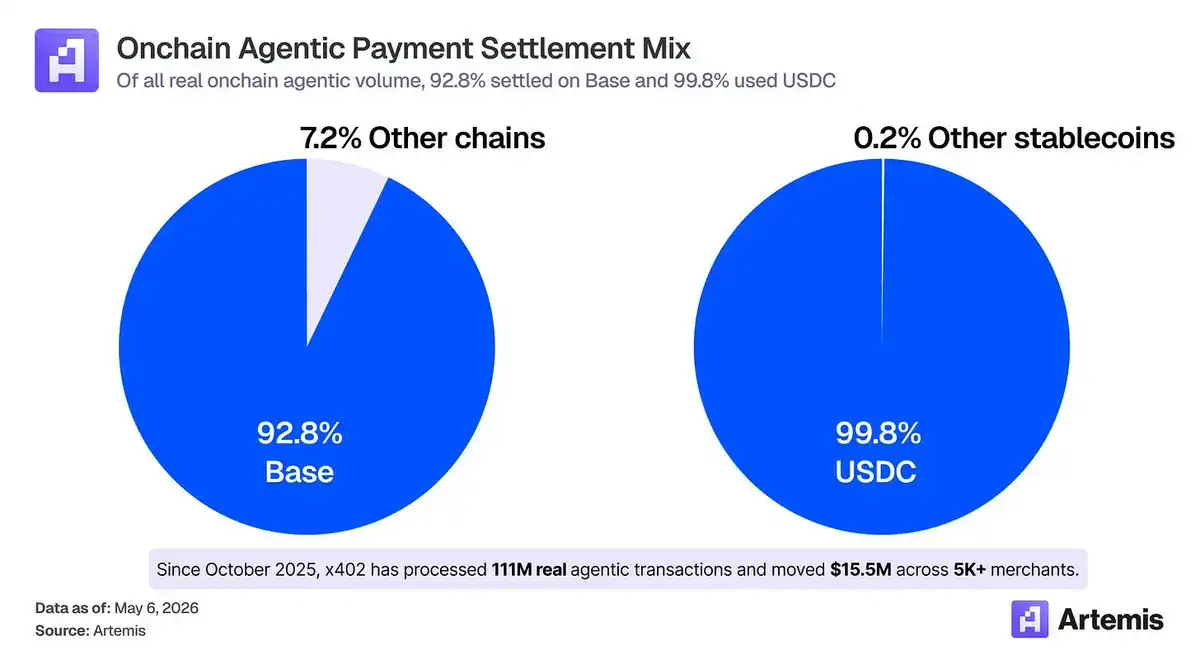

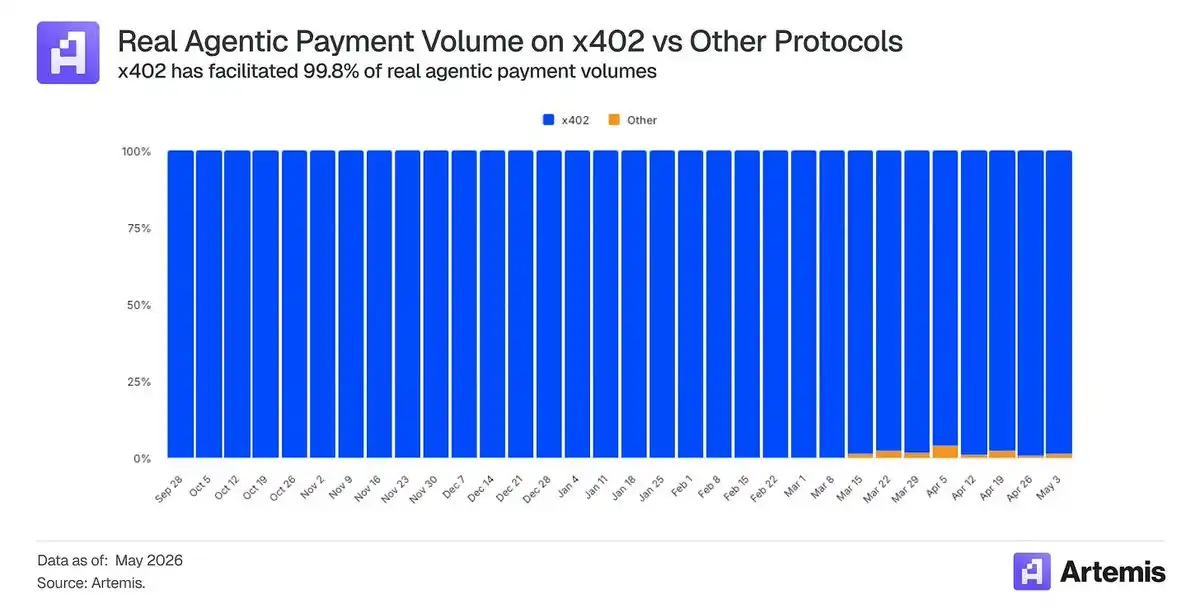

Большинство инвесторов считают, что Stripe (оценка $159 млрд по состоянию на февраль 2026 года) и Tempo являются явными победителями в торговле через ИИ-агентов, но данные из блокчейна говорят об обратном: 92.8% реальных платёжных объёмов ИИ-агентов происходят на Base, а 99.8% рассчитываются в USDC.

Из всех объёмов платежей ИИ-агентов более 99.8% происходит через x402 — это открытый платёжный протокол, впервые представленный Coinbase.

ИИ-агенты превращаются из помощников, отвечающих на вопросы, в системы, совершающие транзакции от имени пользователей, покупая API, конечные точки данных, вычислительные мощности, логические выводы и услуги с суб-пенсовой экономикой и машинной скоростью.

Существующие карточные экосистемы не предназначены для этого. Типичная карточная транзакция имеет фиксированные затраты около $0.03-0.04 до комиссии за обмен, что делает вызов API стоимостью $0.003 экономически нецелесообразным — разница на два порядка. Стейблкоины, рассчитываемые в высокопроизводительных L2, проводят клиринг за секунды при стоимости в доли цента и не требуют вмешательства человека для установления биллинговых отношений.

McKinsey прогнозирует, что глобальный объём продаж через ИИ-агентов составит $3-5 трлн к 2030 году. Gartner оценивает, что к 2028 году ИИ-агенты будут посредниками в более чем $15 трлн B2B-закупок. Обе цифры носят ориентировочный характер и должны рассматриваться как таковые; однако бесспорно то, что если какая-либо из них реализуется, это структурно предпочтёт стейблкоиновые экосистемы, а USDC уже является выбором по умолчанию, от чего напрямую выигрывает Coinbase.

Счёт данных

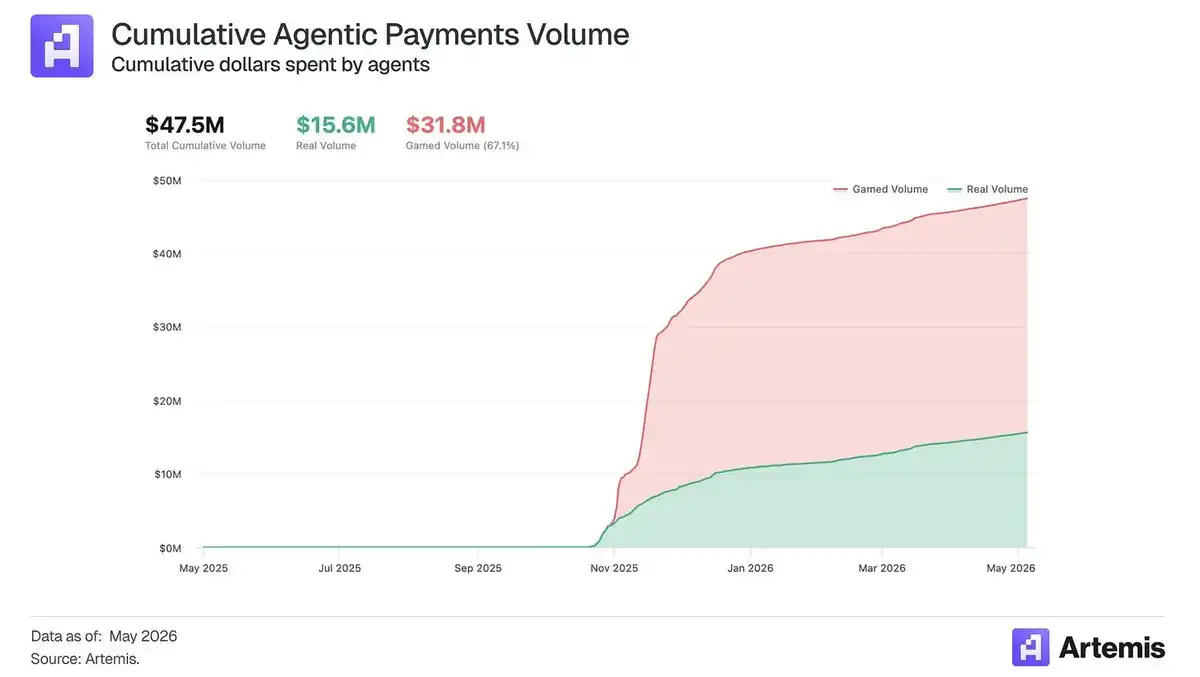

Стандарт x402 — это нативный для HTTP протокол микроплатежей, совместно разработанный Coinbase (ныне управляемый Linux Foundation), который стал ведущим открытым протоколом для инициации платежей ИИ-агентами. С октября 2025 года x402 обработал более 180 миллионов платежей ИИ-агентов, переместив $47.5 млн расходов ИИ-агентов среди более чем 5000 торговцев, продающих ИИ-агентам.

Когда торговцы делают свои услуги доступными для потребления ИИ-агентами, L2 Coinbase и USDC уже являются платёжной экосистемой по умолчанию. Кроме того, Agentic.Market даёт Coinbase возможность владеть обнаружением ресурсов. Если ИИ-агенты будут использовать его для поиска, оценки и маршрутизации к сервисам x402, ценность будет получена не только через расчёты на Base и объёмы USDC, но и через положение Coinbase как рынка, координирующего транзакции между ИИ-агентами и сервисами.

Как Coinbase монетизирует

Coinbase захватывает экономику платежей ИИ-агентов через четыре составные линии, вращающиеся вокруг опоры стейблкоинов: плавающие средства USDC, расчёты на Base, монетизация CDP/AgentKit и дистрибуция Agentic.Market.

Доходность резервов USDC. Линия дохода с наибольшим потенциалом роста для Coinbase — не комиссия за транзакции, а плавающие средства. Кошельки ИИ-агентов требуют предварительного пополнения баланса для авторизации автономных расходов, оплаты API, покрытия сервисов по мере использования и проведения расчётов в реальном времени для машинной торговли. По мере того как ИИ-агенты становятся экономическими субъектами, балансы USDC, хранящиеся в контролируемых Coinbase кошельках, становятся регулярными, приносящими доход депозитами. Каждый доллар USDC, удерживаемый ИИ-агентом, генерирует доход от резервов, независимо от скорости оборота этого доллара.

Экономика секвенсора Base. Каждая транзакция x402 или MPP, рассчитываемая на Base, становится упорядоченной транзакцией, которая может генерировать приоритетные комиссии. Эта линия масштабируется с количеством транзакций, а не только с объёмом платежей, что важно, потому что торговля через ИИ-агентов может быть более частой и с меньшими чеками, чем человеческая торговля. То есть комиссии секвенсора, вероятно, являются наименьшей частью потенциала роста, поскольку стоимость транзакций со временем снижается.

Монетизация CDP, AgentKit и фасилитаторов. Coinbase может монетизировать уровень для разработчиков, позволяющий ИИ-агентам иметь кошельки, управлять разрешениями, спонсировать газ, рассчитывать платежи x402 и взаимодействовать с платными сервисами. Это включает в себя комиссии фасилитатора за транзакции x402, инфраструктуру кошельков, транзакции без газа, управление ключами, стратегический контроль и инструменты для разработчиков корпоративного уровня. Если CDP станет инфраструктурным стеком по умолчанию для платежей ИИ-агентов, Coinbase сможет получать доход от платформы, даже если конечная стоимость платежа низка.

Потенциал масштабирования

Мы предполагаем, что к 2030 году объём торговли через ИИ-агентов достигнет $5 трлн в год. Большая часть этого всё ещё будет направляться через карточные экосистемы, ACH, банковские платежи и экосистемы счёта-на-счёт, особенно для крупных потребительских и корпоративных закупок. Но машинно-ориентированная, высокочастотная, трансграничная, API-ориентированная торговля будет непропорционально использовать стейблкоины и платёжные стандарты, такие как x402 и MPP.

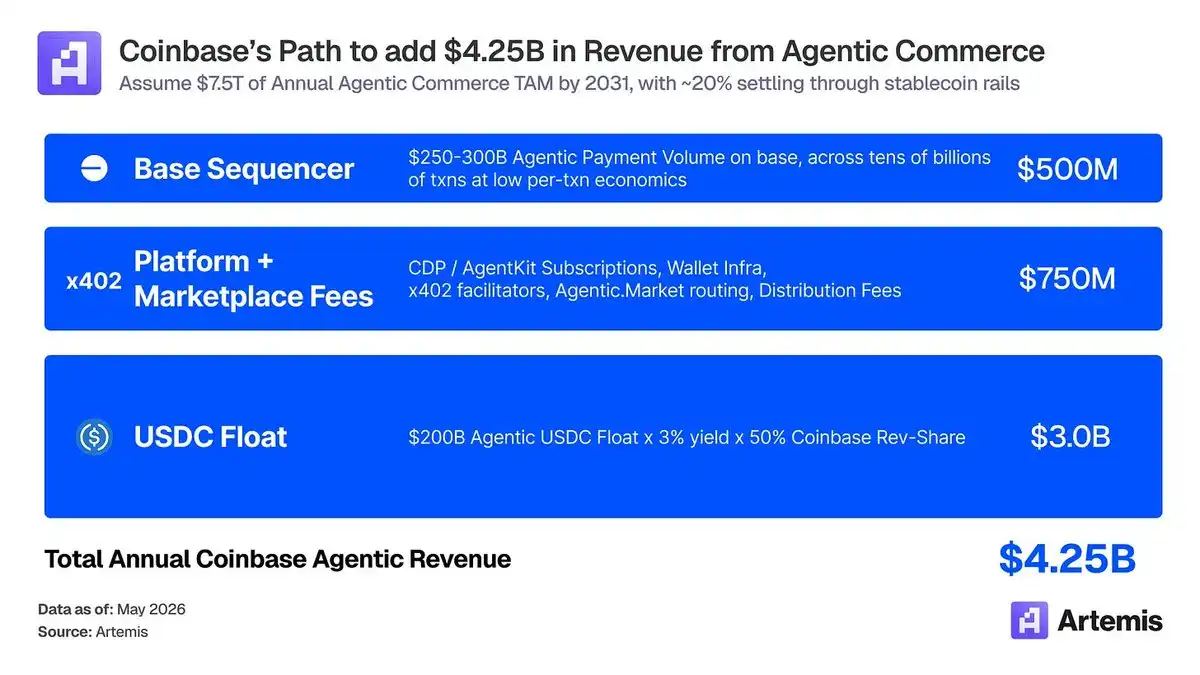

В бычьем сценарии примерно 20% торговли через ИИ-агентов будет рассчитываться через стейблкоиновые экосистемы, что означает $1.0-1.5 трлн ежегодных платежей ИИ-агентов на основе стейблкоинов. Иллюстративный расчёт дохода для бычьего сценария выглядит следующим образом:

- Плавающие средства USDC: $200 млрд среднего баланса USDC ИИ-агентов × 4% доходность резервов × 50% приписываемая экономика Coinbase = $4 млрд

- CDP/AgentKit/Фасилитаторы/Agentic.Market: Подписки разработчиков, инфраструктура кошельков, фасилитация x402, маршрутизация рынка, аналитика провайдеров и дистрибьюторские сборы = $750 млн

- Секвенсор Base: $250-300 млрд объёмов платежей ИИ-агентов на Base, десятки миллиардов транзакций, с низкой экономикой на одну транзакцию = $250 млн

Это указывает на примерно $4.25 млрд годового приписываемого Coinbase дохода от ИИ-агентов. Важный вывод заключается в том, что если Coinbase станет операционным счётом, платформой для разработчиков, уровнем обнаружения и расчётной экосистемой для автономной торговли, будет накоплена реальная ценность, и они уже добились огромного прогресса в этом направлении за последние месяцы.

Почему побеждают Coinbase и USDC

Преимущество Coinbase заключается в том, что она контролирует четыре взаимно усиливающихся уровня стека платежей ИИ-агентов: плавающие средства USDC, расчёты на Base, инфраструктура CDP/AgentKit и обнаружение Agentic.Market.

USDC уже является активом для расчётов по умолчанию, что означает, что разработчики интегрируют его в первую очередь из-за самых глубоких инструментов, ликвидности и поддержки разработчиков. Затем Base выигрывает как естественная расчётная цепочка для нативных платежей ИИ-агентов в USDC, с низким трением для разработчиков и растущим покрытием фасилитаторов. CDP и AgentKit находятся на более высоком уровне, предоставляя разработчикам кошельки, управление ключами, спонсорство газа и платежную инфраструктуру, необходимые для того, чтобы ИИ-агенты стали экономически активными. Наконец, Agentic.Market может стать уровнем обнаружения и маршрутизации, где ИИ-агенты находят, сравнивают и потребляют сервисы с поддержкой x402. Конкуренты, входящие на этот рынок, должны одновременно воспроизвести ликвидность, расчёты, инфраструктуру для разработчиков и дистрибуцию — и каждый новый ИИ-агент, торговец и сервис делают существующий стек Coinbase всё труднее заменить.

Заключение

Рынок рассматривает Coinbase как криптобиржу, упуская из виду, что они строят платформу для нативных финансовых операций с ИИ. Глобальные лидеры прогнозируют $3 трлн предложения стейблкоинов и $5 трлн торговли через ИИ-агентов к 2030 году, а стейблкоины уже отвязались от цен на криптовалюты. Coinbase позиционировала себя как победитель в этом мире и демонстрирует раннее лидерство. x402, USDC и Base уже стали фактическим стандартным стеком для торговли через ИИ-агентов, причём каждая доля на каждом уровне превышает 90% у конкурентов. Coinbase находится в уникальном положении, разработав Base, инкубировав x402 и получив льготную долю в экономике USDC. Неправильная оценка имеет три опоры. Структура протокола с Circle — это продолжающаяся фиксация, а не возобновляемый контракт, что означает, что линии дохода от стейблкоинов являются устойчивыми, а не рискованными. Закон CLARITY формализует регулируемый инфраструктурный уровень, на котором уже работает Coinbase, переоценивая бизнес с потребительского продукта на базовый рыночный канал. А четырёхуровневый стек ИИ-агентов (USDC, Base, CDP, Agentic.Market) рефлексивно комплементарен, каждый новый ИИ-агент и торговец делают ров защиты труднее атаковать. Coinbase должна торговаться ближе к группе инфраструктурных аналогов, а не к группе брокеров. Мы считаем, что Coinbase станет компанией с капитализацией $300 млрд благодаря этим эпохальным попутным ветрам, причём большая часть дохода будет поступать от таких линий, как стейблкоины и торговля через ИИ-агентов, в форме подписок и сервисов.

Раскрытие информации: Этот материал предназначен только для информационных целей и не является инвестиционной, финансовой, торговой рекомендацией или советом любого другого рода. Высказанные мнения являются мнениями автора и не должны рассматриваться как рекомендация покупать, продавать или удерживать какие-либо активы. Автор или связанные с ним стороны могут иметь позиции по обсуждаемым активам. Вы должны провести собственное исследование и проконсультироваться с соответствующими финансовыми специалистами перед принятием любых инвестиционных решений.