Мемы: почему они режут только тебя? Статья, которая объясняет их настоящий механизм роста

Автор Danny в статье «Почему купленные вами мемы только падают?» предлагает новый взгляд на механику роста мем-токенов через призму «финансовой физики». Вместо хаотичного азарта, он описывает мемы как трёхмерную модель роста, где стоимость определяется не спекуляциями, а математической логикой.

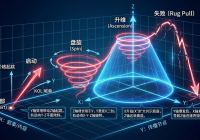

Ключевая идея: капитализация мема не просто «растёт» — её «удерживает» расширяющаяся база консенсуса. Модель строится на трёх осях:

- X: Плотность нарратива — сила идеи, культурный код, меметичность.

- Y: Сеть распространения — узлы влияния от крупных лидеров до обычных пользователей.

- Z: Движение капитала — ликвидность, объёмы торгов, рыночная капитализация.

Успешные мемы проходят этапы: запуск (Y-всплеск), раскрутка (рост Z и X), восхождение (расширение базы и рост капитализации). Провальные мемы рушатся, когда за всплеском активности (Y) не следует развитие нарратива (X), и цена (Z) обваливается.

Статья подчёркивает: устойчивый рост возможен только при одновременном усилении всех трёх осей, создавая «конус богатства» с широкой основой консенсуса.

比推01/21 07:41