Автор: @SoskaKyle

Перевод: AididiaoJP, Foresight News

Оригинальное название: Какие предупреждения «отток капитала» Ethena несет для крипторынка?

Криптовалютный рынок уже несколько месяцев находится в «режиме избегания рисков». Все это время я постоянно анализировал различные рыночные данные, пытаясь найти признаки улучшения. В этой статье я начну с рыночной структуры перпетуальных контрактов, затем, объединив данные из прозрачной панели Ethena, расскажу, каковы на самом деле аппетиты к риску на рынке.

Проще говоря, объем средств Ethena, находящихся «в обороте», упал до многолетнего минимума, составляя лишь 71% от минимума 2025 года. Это не значит, что с самой Ethena что-то не так, но это отражает реальное состояние всего рынка. Сейчас количество активных медведей и активных быков на рынке почти сравнялось, что является очень редкой ситуацией в криптосфере, и, судя по истории, такой баланс трудно поддерживать долго.

Криптовалютный рынок всегда славился высокой волатильностью цен и активным использованием плеча. Я уже писал исследовательскую статью о BitMEX, где подробно анализировал их стократные перпетуальные контракты того времени.

С эпохи BitMEX и до сегодняшнего дня криптовалютные фьючерсы стали продуктом с наибольшим объемом торгов в индустрии, обычно в 5-20 раз превышая объем торгов на спотовом рынке. Поскольку перпетуальные контракты являются основным местом для маржинальной торговли розничных инвесторов, чтобы понять аппетиты к риску в криптовалютах, нужно внимательно следить именно за ними.

Компания Ethena, в частности, предоставляет нам уникальный взгляд на рынок деривативов. Как показано на рисунке ниже, Ethena занимается «керри-трейдом» в криптовалютах. Стратегия проста: когда трейдеры хотят открыть длинные позиции, Ethena выступает их контрагентом — открывает короткие позиции. Затем Ethena покупает точно такое же количество базового актива, которое она продала без покрытия. Можно понять это так: Ethena предоставляет «леверидж» как услугу. Трейдеры хотят использовать леверидж, чтобы сыграть на рост, но им не хватает средств; у Ethena есть средства, но она не хочет нести направленные риски. Таким образом, трейдеры через перпетуальные контракты, оплачивая определенный базис и финансирование, «занимают» средства у Ethena для использования левериджа.

(Источник изображения: docs.ethena.fi / 4pillars)

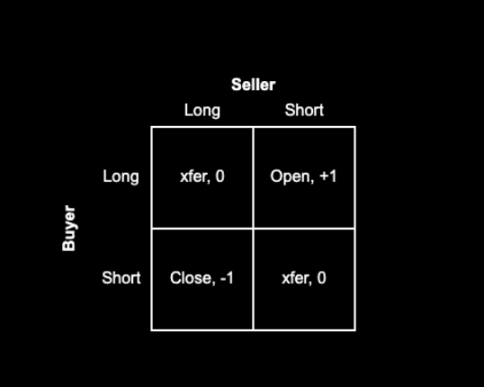

Механизм перпетуальных контрактов определяет, что каждому длинной позиции обязательно соответствует короткая, их количество всегда 1:1. Каждый контракт на рынке представляет собой соглашение о платежах между бычьей и медвежьей сторонами. Роль биржи заключается в том, чтобы выступать посредником, обеспечивая наличие достаточного маржинального обеспечения с обеих сторон — и длинной, и короткой — для каждого контракта. Приведенная ниже матрица показывает четыре возможных результата сопоставления сделок биржей.

Матрица логики сопоставления перпетуальных контрактов

У каждой сделки есть покупатель и продавец. Если и покупатель, и продавец изначально были длинными или оба были короткими, бирже просто нужно передать контракт от одной стороны другой, это не увеличит и не уменьшит общее количество контрактов на рынке. Если покупатель хочет открыть длинную позицию, а продавец — короткую, то биржа должна создать новый контракт, где покупатель будет длинной стороной, а продавец — короткой, таким образом общее количество контрактов на рынке увеличится на 1. И наоборот, если продавец хочет закрыть свою длинную позицию, а покупатель — свою короткую, биржа может «разъединить» этих двух участников из их старых контрактов и аннулировать эти два контракта, общее количество контрактов на рынке уменьшится на 1.

Так в чьих же руках находятся эти контракты на нормальном рынке? Я думаю, что в основном их можно разделить на следующие четыре типа участников:

-

【Быки】 Активные быки. Это те, кто хочет открыть длинные позиции, делая ставку на рост цены. Они склонны к риску, их готовность входить на рынок полностью зависит от уверенности в рынке.

-

【Медведи】 Активные медведи / хеджеры.

-

a. Те, кто напрямую открывает короткие позиции по активу.

-

b. Те, кто хеджируется с помощью структурированных продуктов. Например, некоторые VC или сотрудники, получающие вознаграждение в токенах компании, могут захотеть зафиксировать текущую цену, чтобы хеджировать риск падения при будущем разблокировании токенов. А также маркет-мейкеры или торговые компании, такие как Cumberland, Wintermute, которые могут помогать хеджировать риски малоликвидных проектов (например, Monad), открывая короткие позиции по крупным монетам с высокой корреляцией, таким как Bitcoin, Ethereum, чтобы косвенно хеджировать риски по своим малым монетам. Такие проекты, как Neutrl, специализируются на подобных сделках.

-

【Арбитражные медведи】 Трейдеры базиса (включая Ethena и другие подобные учреждения). Они являются оппортунистами, не заинтересованными в ставках на направление. Когда на рынке слишком много желающих открыть длинные позиции и недостаточно желающих открыть короткие, они приходят и выступают в роли контрагента, зарабатывая на базис и финансировании. Их объем капитала может гибко调整调整 (адаптироваться).

-

【Смешанный арбитраж】 Арбитражеры между перпетуальными контрактами. Они одновременно держат длинные и короткие позиции по перпетуальным контрактам, ища небольшие ценовые разницы для арбитража между разными биржами или разными перпетуальными контрактами на разные монеты. В любой момент их длинные и короткие позиции полностью совпадают, они не делают ставку на направление.

Поскольку длинные и короткие позиции по перпетуальным контрактам должны соответствовать 1:1, мы можем вывести формулу:

Активные быки + Длинные позиции арбитражеров = Активные медведи + Короткие позиции трейдеров базиса + Короткие позиции арбитражеров

В то же время, особенность арбитражеров такова, что:

Длинные позиции арбитражеров = Короткие позиции арбитражеров

Подставляя второе выражение в первое и сокращая позиции арбитражеров с обеих сторон, получаем:

Активные быки = Активные медведи + Короткие позиции трейдеров базиса

Бизнес Ethena как раз может служить хорошим представителем «коротких позиций трейдеров базиса». Наблюдая за ее данными, мы можем大致大致 (в общих чертах) увидеть разрыв в силе между активными быками и активными медведями.

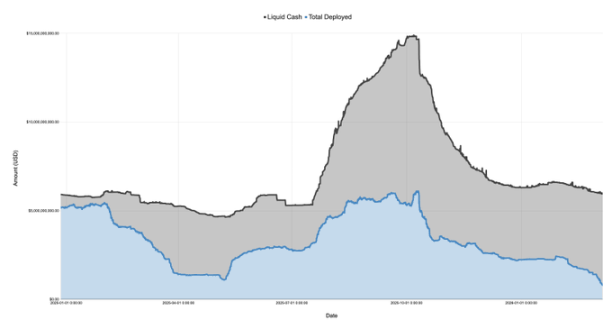

На следующем рисунке показаны части «Денежные средства» и «Размещенный капитал» в опубликованном самим Ethena балансе, с 27 декабря 2024 года по 7 марта 2026 года:

В январе 2025 года, с запуском монеты Трампа TRUMP, рыночные настроения резко ухудшились, и рынок перешел в режим «избегания рисков». Затем последовали обсуждения тарифов, и вплоть до «Дня освобождения» в апреле рынок продолжал снижаться. За этот период средства Ethena, находящиеся «в обороте», резко упали с более чем 5 миллиардов долларов до всего лишь 1.1 миллиарда, снизившись более чем на 75%!

Помните, что размещенный капитал Ethena можно рассматривать как индикатор «избыточного спроса на длинные позиции» на рынке. Хотя Ethena — не единственная, кто этим занимается, их объемы велики (иногда они могут составлять до 25% от общего открытого интереса на Binance и Bybit), и пока у них есть свободные деньги, теоретически они будут удовлетворять неудовлетворенный спрос на длинные позиции на рынке. Таким образом, эти данные говорят нам, что к апрелю 2025 года, хотя общий потенциальный спрос на длинные позиции, возможно, и не упал на 75%, та часть «чистого спроса на длинные позиции», которая осталась после заполнения «активными медведями», действительно резко обвалилась.

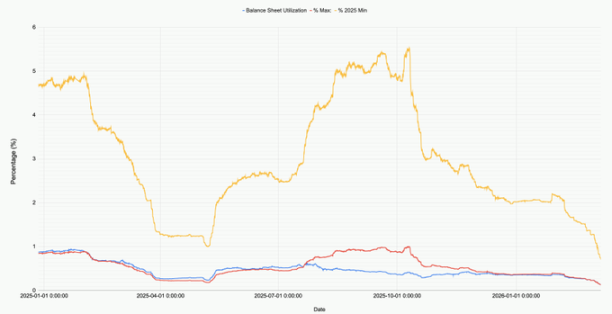

На следующем графике показаны изменения доли размещенных средств в балансе Ethena, а также минимумы и максимумы 2025 года.

Посмотрите на текущую ситуацию (9 марта 2026 года): общий объем средств, размещенных Ethena на всех рынках (BTC, ETH, SOL, BNB, XRP, HYPE), составляет всего около 791 миллиона долларов. Эта цифра составляет 71% от минимума 2025 года и всего 12.9% от максимума, достигнутого до 10 октября 2025 года. Еще раз подчеркиваю, это ни в коем случае не означает, что сама Ethena плоха, это отражение реального рыночного спроса: желание открывать длинные позиции сейчас действительно находится на исторически низком уровне.

Особенно值得注意的是, что совсем недавно (8 февраля 2026 года), когда Bitcoin упал до 60 тысяч долларов, размещенные средства Ethena тогда еще составляли более 2 миллиардов. Всего за месяц эта цифра резко сократилась на 60%!

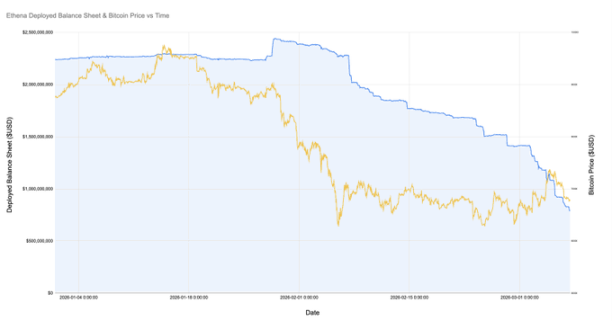

На следующем графике показана связь между размещенными средствами Ethena и ценой Bitcoin с января этого года в увеличенном масштабе.

После падения Bitcoin до 60 тысяч, базисные позиции Ethena сократились с более чем 2 миллиардов до менее чем 800 миллионов, упав более чем на 60%. Интересно, что сама цена монеты за этот период особо не двигалась. Почему так произошло? Может быть несколько причин:

-

Те базисные позиции, которые были открыты во время обвала в феврале, хотя, возможно, все еще были прибыльными, но по мере того, как базис становился неблагоприятным (даже отрицательным), а финансирование также стало отрицательным, такие сделки стали неустойчивыми, и их постепенно закрыли.

-

Увеличилось количество активных медведей и хеджеров, и эти участники менее чувствительны к цене (например, им необходимо продавать, чтобы зафиксировать прибыль), вытесняя таких оппортунистических трейдеров базиса, как Ethena.

-

Действительно стало меньше людей, желающих использовать леверидж для открытия длинных позиций.

Лично я думаю, что в основном это первые две причины, влияние третьей невелико. Посмотрите на график выше: в период, когда Ethena закрывала позиции, общий открытый интерес по Bitcoin (и другим основным монетам) на самом деле оставался довольно стабильным. В то же время, ставки финансирования в течение длительного времени были отрицательными, например, накопленная ставка финансирования по SOL на некоторых биржах даже была отрицательной. Это указывает на то, что на рынке действительно стало больше людей, желающих открыть короткие позиции или хеджироваться.

Если бы пришлось угадывать основную причину, я думаю, что, возможно, средним и малым криптокомпаниям и VC сейчас приходится нелегко. Подумайте о тех проектах с малой капитализацией, таких как Eigen, Grass, Monad и так далее — их сотни и тысячи. За каждым проектом стоит несколько десятков VC, у самих проектов есть казначейства и сотрудники, которых нужно содержать. VC необходимо контролировать убытки, фиксировать прибыль для отчетности перед LP, проектам необходимо сохранять денежный поток и не увольнять сотрудников. В такой ситуации все пытаются выжать воду из камня. Естественным способом является использование некоторых структурированных продуктов для открытия коротких позиций по корзине основных монет с высокой корреляцией, чтобы хеджировать риски по своим малым монетам. Сейчас эта стратегия, возможно, стала переполненной.

Мы также можем видеть некоторые признаки, например, иногда ETH внезапно сильно растет, и в результате заставляет резко подняться一大片一大片 (целую плеяду) монет средней и малой капитализации, это может быть вызвано закрытием этих хеджевых позиций, приводящим к «короткому сжатию» (squeeze). А то, что такие трейдеры базиса, как Ethena, вытесняются, само по себе является свидетельством переполненности этой стратегии.

Независимо от конкретной причины, одно можно сказать наверняка: в криптосфере силы активных быков и активных медведей сейчас почти сравнялись, возможно, впервые. Конечно, никто не утверждает, что это не может стать новой нормой, но, судя по историческому опыту других финансовых рынков, такой тонкий баланс обычно трудно поддерживать в течение длительного времени.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения比推 TG:https://t.me/BitPushCommunity

Подписка比推 TG: https://t.me/bitpush