Автор | Odaily星球日报(@OdailyChina)

Автор | Дин Дан(@XiaMiPP)

В индустрии стейблкоинов Circle и Stripe раньше были партнерами с четким разделением обязанностей.

Circle отвечала за отображение долларов из реального мира в блокчейне, создание стейблкоина USDC; Stripe же через свою глобальную платежную сеть позволяла этим цифровым долларам циркулировать в реальных коммерческих сценариях. Одна производила деньги, другая обеспечивала их движение. Эти союзники в прошлые годы были почти идеальным дополнением друг другу.

Однако два недавних события, если рассматривать их вместе, вызывают微妙ное ощущение: эти две компании, кажется, понемногу движутся в одном направлении.

11 февраля Stripe объявила о запуске функции оплаты x402 на Base. Эта функция позволяет разработчикам напрямую взимать плату с AI-агентов с помощью USDC. Стейблкоин больше не просто инструмент оценки на биржах; в волне AI Agent он станет платежным средством для транзакций между машинами.

В ту же неделю дочерняя компания Stripe, занимающаяся инфраструктурой стейблкоинов, Bridge, получила предварительное одобрение на получение банковской лицензии траста (OCC). Это означает, что Bridge потенциально может начать продвигать бизнес по выпуску стейблкоинов, хранению и управлению резервами в качестве регулируемого финансового учреждения.

С одной стороны, Stripe создает новые платежные сценарии с использованием USDC; с другой — она строит собственную финансовую инфраструктуру для стейблкоинов.

Индустрия стейблкоинов старой эпохи

Если разобрать мир стейблкоинов, индустрия не так уж сложна.

Самый нижний уровень — это уровень эмиссии. Такие организации, как Circle, отвечают за отображение долларовых резервов реального мира в блокчейне, создавая стейблкоины, например USDC. Выше находится расчетный уровень, где роль учета и клиринга средств выполняет блокчейн-сеть. Далее идет платежный уровень. Такая интернет-платежная инфраструктура, как Stripe, внедряет стейблкоины в реальные коммерческие транзакции, позволяя средствам из блокчейна попадать в такие сценарии, как электронная коммерция, SaaS или международная торговля. На самом верху находится уровень приложений. Здесь происходят различные конкретные финансовые активности, от DeFi до платежей для AI Agent.

Когда стейблкоины были лишь инструментом крипторынка, участники этой индустрии всегда четко выполняли свои роли: эмитенты отвечали за «чеканку монет», платежные платформы — за «прием денег», блокчейн — за расчеты, а разработчики фокусировались на сценариях применения.

Еще в 2014 году Stripe стала одной из первых основных платежных систем, поддержавших оплату Bitcoin. Однако из-за высокой волатильности цены биткоина, длительного времени подтверждения транзакций и непредсказуемости комиссий эта бизнес-попытка в конечном итоге была свернута в 2018 году. Биткоин был больше похож на спекулятивный актив, а не на валюту, подходящую для интернет-платежей.

Появление стейблкоинов как раз заполнило эту нишу. Ценовая стабильность, программируемость и возможность расчетов в блокчейне USDC сделали его ближе к идеалу Stripe — «нативной для интернета валюте». В 2022 году Stripe снова вошла в криптосферу, выбрав поддержку платежей USDC. Этот шаг не только вернул стейблкоины в основную платежную систему, но и объективно способствовал быстрому росту объема обращения USDC, чья рыночная капитализация в обращении一度 превысила 550 миллиардов долларов.

В рамках такого синергетического отношения Circle предоставляла стабильный цифровой доллар, а Stripe — глобальную платежную сеть, вместе продвигая USDC от инструмента криптотрейдинга до рынка объемом почти 700 миллиардов долларов.

Данные в блокчейне также подтверждают эффект масштаба, вызванный такой协同作用. Согласно данным Artemis, в январе объем транзакций USDC в блокчейне превысил 8,4 триллиона, в то время как общий объем транзакций стейблкоинов на рынке составил 10 триллионов. Другими словами, с точки зрения количества транзакций USDC занимает 84% общей доли рынка.

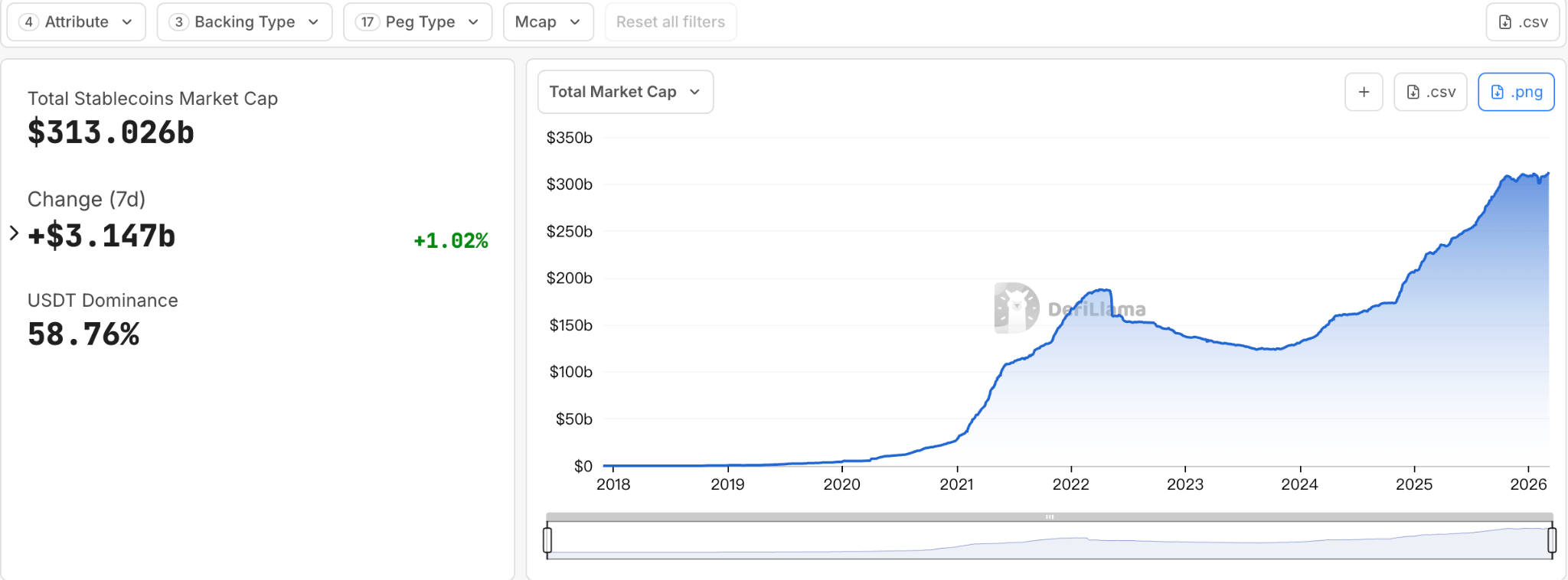

В то же время внешняя регуляторная среда также претерпела значительные изменения. С официальным принятием «Закона GENIUS» стейблкоины, этот финансовый эксперимент, который когда-то находился в серой зоне регулирования, постепенно включаются в правовое поле финансовой системы. Сегодня рынок стейблкоинов превышает 3000 миллиардов долларов. В будущем объемы, которые будет нести этот рынок, могут достичь уровня финансовой сети в триллионы долларов.

Стейблкоины больше не являются просто внутренним инструментом крипторынка, а начинают рассматриваться как часть финансовой инфраструктуры следующего поколения. Когда рынок из крипто-инструмента вырастает в финансовую инфраструктуру, логика индустрии часто меняется вместе с ним.

Когда стейблкоин становится инфраструктурой

В любой финансовой системе реальная стабильная прибыль обычно исходит не от отдельного звена, а от контроля над ключевыми узлами. Тот, кто может контролировать пути движения денег, может определять правила.

Если стейблкоин — это просто базовый актив, а платежные шлюзы, инструменты для разработчиков и бизнес-сценарии полностью контролируются другими платформами, то фактическая прибыль, которую может получить эмитент, весьма ограничена. Напротив, если контролировать платежную сеть или расчетную систему, то можно постоянно получать выгоду на каждом этапе движения денег.

Следовательно, когда стейблкоины начинают эволюционировать из криптоактива в финансовую инфраструктуру, начинает проявляться почти неизбежная тенденция: изначально распределенные по разным уровням отраслевые роли начинают пытаться расшириться вверх и вниз по цепочке, включая больше звеньев в свою систему.

В финансовой истории этот процесс не нов. От банковской системы до сетей кредитных карт и интернет-платежных платформ зрелые финансовые системы в конечном итоге часто проходят аналогичные этапы — от распределения ролей к структурной интеграции.

Теперь этот ветер отраслевой консолидации也开始 подуть в мире стейблкоинов.

Если рассматривать индустрию стейблкоинов как вертикальную структуру, то за последние несколько лет Circle и Stripe находились на двух концах этой цепи.而现在,它们都在向中间移动。

Circle: Не хочет быть просто «печатным станком»

В экосистеме на блокчейне эффективность обращения и частота использования USDC уже давно不容忽视. В последнем отчете о потоках стейблкоинов скорость обращения USDC почти в 5 раз выше, чем у USDT.

Однако полагаться только на выпуск стейблкоинов — не самая многообещающая бизнес-модель.

Основные источники дохода эмитента стейблкоинов大致分为 две части:一是 процентный доход, генерируемый резервными активами,二是 комиссии, связанные с выпуском и погашением стейблкоинов.但随着稳定币规模不断扩大,这部分收益往往还需要与生态伙伴进行分成。例如,作为 USDC 最重要的分发渠道之一,Coinbase 每年就会从 USDC 体系中获得接近 10 亿美元的利润分成。这意味着,即便发行方承担着稳定币体系中最核心的“铸币”角色,其实际可支配的收益空间仍然受到生态结构的制约。

Это также объясняет, почему за последние два года стратегия Circle явно сместилась в сторону уровня приложений: она больше не удовлетворяется просто выпуском стейблкоинов, а пытается построить完整的 стейблкоин支付网络.

Судя по公开тной информации,布局 Circle на уровне приложений大致分为三步。

Первый шаг — блокчейн Arc уровня L1, разработанный для предприятий. На уровне приложений он играет роль «координационного слоя», помогая разработчикам создавать приложения для платежей, расчетов и т.д. Arc был запущен в тестовой сети в октябре 2025 года, привлек более 100 компаний, обработал более 166 миллионов транзакций, запуск основной сети запланирован на 2026 год.

Второй шаг — с USDC в качестве ядра, через протокол кросс-чейн передачи (CCTP) и инструменты шлюзов решить проблему фрагментации ликвидности. На уровне приложений помочь предприятиям объединить USDC из мультичейна в Arc и CPN, обеспечивая беспрепятственное распространение и создание приложений.

Третий шаг, а также ключевой продукт Circle на уровне приложений — CPN (Circle Payments Network). Был запущен в мае 2025 года, представляет собой сеть координации платежей «открытого стандарта», разработанную для программируемых, соответствующих требованиям и аудируемых платежей. На сегодняшний день зарегистрировались 55 финансовых учреждений, еще 74 проходят проверку на соответствие требованиям.

Эта布局 показывает, что Circle постепенно превращается из простого эмитента стейблкоинов в полноценную прикладную инфраструктуру, способную обеспечивать движение资金.

Stripe: «Касса» тоже хочет контролировать пути

Stripe же находится на другом конце системы стейблкоинов. Являясь одной из最重要的 мировых интернет-платежных инфраструктур, Stripe контролирует огромное количество торговых точек. В 2025 году общий объем обработанных платежей на платформе Stripe достиг 1,9 триллиона долларов, что на 34% больше, чем годом ранее, и составляет около 1,6% мирового ВВП. От Shopify до Amazon, платежные системы множества интернет-магазинов построены на инфраструктуре Stripe. В некотором смысле, Stripe не производит валюту, но она контролирует входные точки для движения денег.

Однако если в будущем эмитенты стейблкоинов и блокчейн-сети совместно будут контролировать расчетный уровень, то платежные платформы могут быть сжаты до роли простых поставщиков技术服务.

Вот почему Stripe в последние годы начала систематически расширяться вверх и вниз по цепочке создания стоимости.

В феврале 2025 года Stripe завершила приобретение платформы инфраструктуры стейблкоинов Bridge за 1,1 миллиарда долларов. Наконец, 12 февраля этого года Bridge получила условное одобрение OCC, что является ключевым элементом инфраструктурных устремлений Stripe.

В то же время Stripe совместно с Paradigm инкубирует публичный блокчейн L1 Tempo, надеясь построить расчетную цепь,专门 ориентированную на интернет-финансы. Публичная тестовая сеть была запущена в декабре 2025 года, запуск основной сети запланирован на 2026 год.

Кроме того, в 2025 году Stripe приобрела компанию по инфраструктуре кошельков Privy, чтобы предоставлять пользователям встроенные кошельки и системы идентификации, снижая thus барьер для входа пользователей в финансовую систему на блокчейне.

Если рассматривать эти действия вместе, становится очевидной очень четкая тенденция: Stripe движется от платежных шлюзов вниз, пытаясь контролировать底层轨道 работы стейблкоинов.

Две компании встречаются в середине индустриальной цепочки

Circle расширяется от уровня эмиссии к уровню приложений, а Stripe движется от платежного уровня вниз к инфраструктуре. Когда оба пути движутся к центру индустриальной цепочки, изначально четкие границы неизбежно начинают пересекаться.

На фоне переформатирования структуры индустрии стейблкоинов это更像 напоминание: конкуренция в сфере стейблкоинов больше не сводится к тому, «кто выпустит больше токенов». В будущем真正 важным вопросом, возможно, станет — кто контролирует пути движения стейблкоинов.

Когда выпуск, расчеты, платежи и приложения постепенно重新 интегрируются, конкуренция в мире стейблкоинов также сместится с «объема активов» на «финансовые сети». И на этой новой трассе старые союзники Circle и Stripe уже начали встречаться в середине индустриальной цепочки.

История стейблкоинов также превращается из эксперимента криптоиндустрии в重建 финансовых сетей.

Рекомендуемая литература

《Последний отчет по стейблкоинам: реальное распределение и потоки гораздо важнее объема предложения》

《За сильным отскоком акций Circle: ИИ, рынки предсказаний и институциональное принятие》