Author: David, Deep Tide TechFlow

On Reddit's stock subreddit communities, stocks with skyrocketing discussion volume aren't necessarily worth buying, but they are definitely getting attention because there's usually a catalyst behind the discussions.

Our monitoring tools scan daily changes in discussion volume and sentiment distribution across several major stock communities on Reddit, fishing out abnormal signals for further analysis.

Last week's hot discussion signals were concentrated in the space sector:

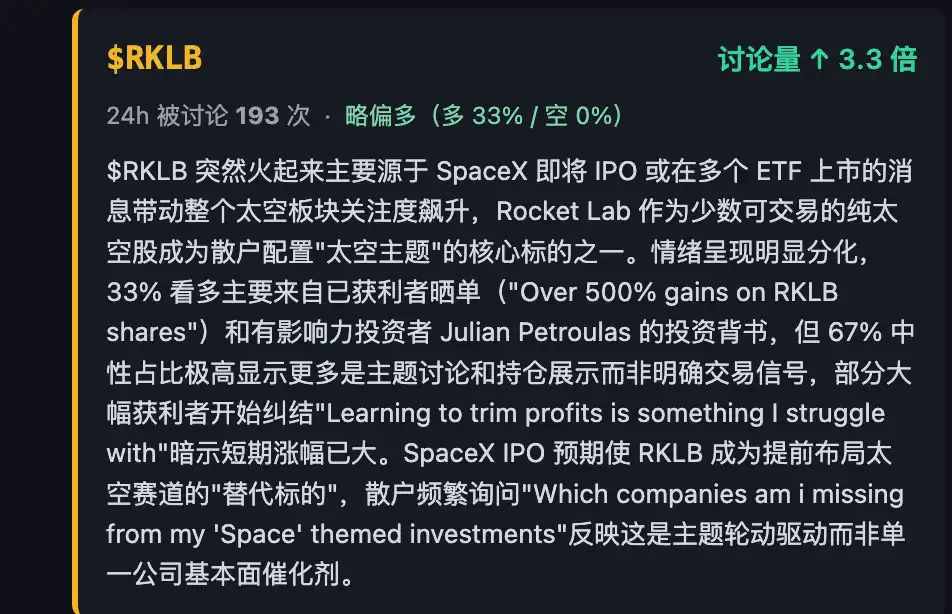

SPCE (Virgin Galactic) topped the hot list with 2,828 discussion threads in 24 hours; meanwhile, RKLB (Rocket Lab) discussion volume surged 3.3 times, and LUNR (Intuitive Machines) and ASTS (AST SpaceMobile) also appeared frequently in the hot discussion zone.

These four stocks are often bundled together on Reddit because they are among the few pure-play space stocks accessible to retail investors. In the years before SpaceX goes public, these are the substitutes for retail investors to allocate to a 'space theme'.

Currently, common discussions in Reddit's US stock communities include "Which companies am I missing from my space themed investments?", which to some extent reflects the spillover effect of SpaceX sentiment and the expectation among foreign retail investors that it will ignite the space concept, prompting them to position themselves early.

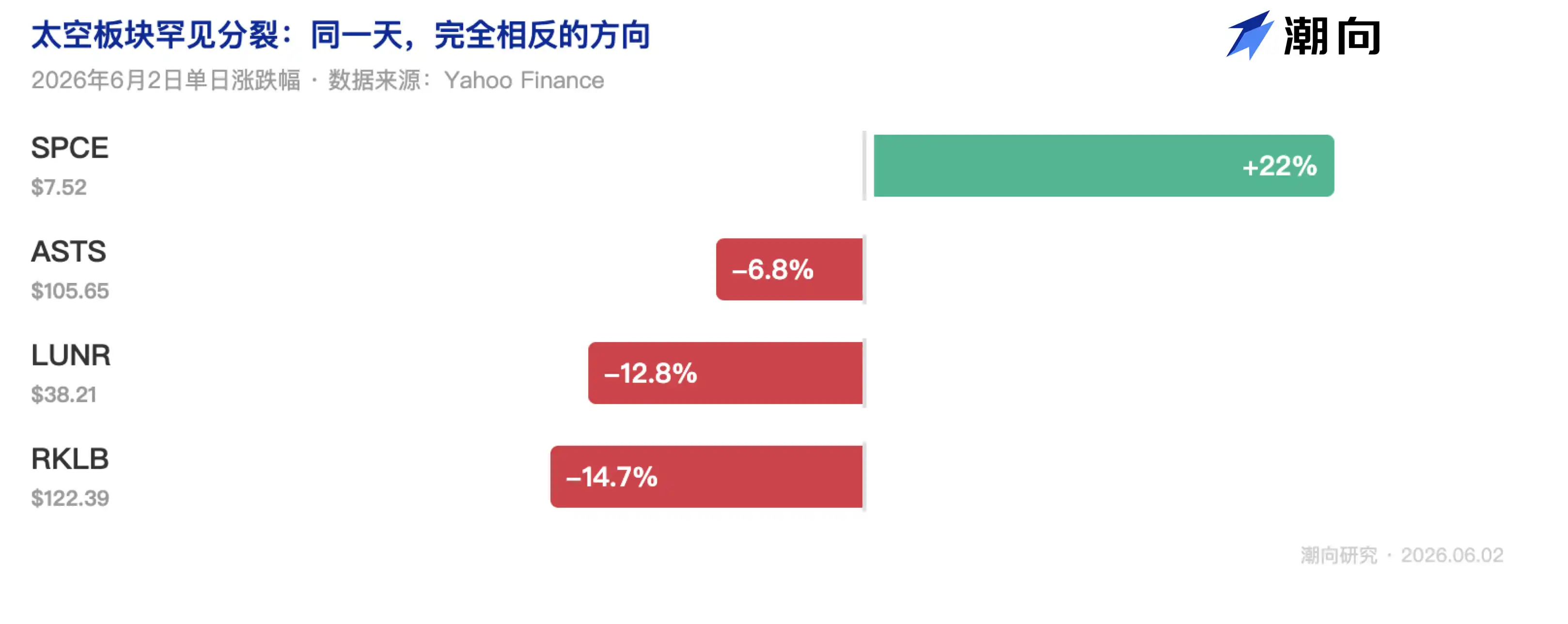

Looking at the current trends of these stocks, they have moved in completely opposite directions within the same sector: SPCE soared 22% in a single day, while RKLB fell 15%, LUNR fell 13%, and ASTS fell 7%.

Therefore, in the current hot discussions, SPCE attracted new attention due to its profit-making effect, while RKLB/LUNR/ASTS generated discussions from existing holders due to price declines or loss anxiety.

If you are also watching the space sector or have corresponding holdings, the following analysis of the recent developments of these 4 US stocks might provide some assistance for decision-making.

Most Space Stocks Fell, Impacted by Overlapping Negative Events

Except for $SPCE, this wave of decline in space stocks involved at least 3 negative events that happened to coincide in the same week.

Blue Origin Rocket Explosion.

Blue Origin is the space company founded by Amazon's Jeff Bezos. Its New Glenn heavy-lift rocket competes in the same market as SpaceX's Falcon Heavy and Rocket Lab's Neutron, which is under development. On May 29, during a static fire test at Cape Canaveral, the New Glenn rocket exploded, prompting the FAA (Federal Aviation Administration, which must approve all commercial launches) to immediately ground it.

This event had the biggest impact on $ASTS:

The company plans to launch 45-60 satellites into orbit before the end of the year, and Blue Origin is one of its primary launch suppliers. The grounding directly eliminates one launch pathway.

$RKLB itself doesn't use New Glenn for launches, but its own Neutron under development is a competitor. The explosion reminded investors that building rockets really can lead to explosions. Another space stock, $LUNR, was affected more by sector-wide sentiment spillover.

However, $SPCE actually benefited. Virgin Galactic operates suborbital space tourism, directly competing with Blue Origin's New Shepard business. After the New Glenn explosion, market funds flowed out of Blue Origin-related stocks, with some moving into SPCE. Additionally, SPCE has a relatively smaller market cap, making its price more prone to volatile swings.

SpaceX IPO Pricing Could Happen as Early as June 11.

SpaceX confidentially submitted its S-1 filing in April, targeting a valuation of $1.8 trillion and raising up to $75 billion, potentially the largest IPO in Wall Street history. Over the past few years, RKLB, LUNR, and ASTS were popular partly because SpaceX wasn't public, making them the only entry points for retail investors into space. Now that the main player is arriving, some capital will naturally move out of these substitutes to make room for SpaceX.

Insiders Themselves Are Selling.

Public data shows RKLB's CEO Peter Beck sold approximately 2.51 million shares over the past 6 months, cashing out about $142 million. The President, COO, and General Counsel also recently reduced their holdings, totaling about $18 million.

Some of this was part of pre-arranged 10b5-1 plans (a preset trading arrangement for compliant CEO selling), but the timing was chosen near historical highs. Over the past year, RKLB rose 412%, ASTS rose 437%, and LUNR rose 267%, so profit-taking pressure was already relatively loose.

The Four 'Space Companies' Are Not Doing the Same Thing

Retail investors tend to treat SPCE, RKLB, LUNR, and ASTS as one sector and trade them together, but these four companies have completely different businesses, revenue stages, and risk profiles.

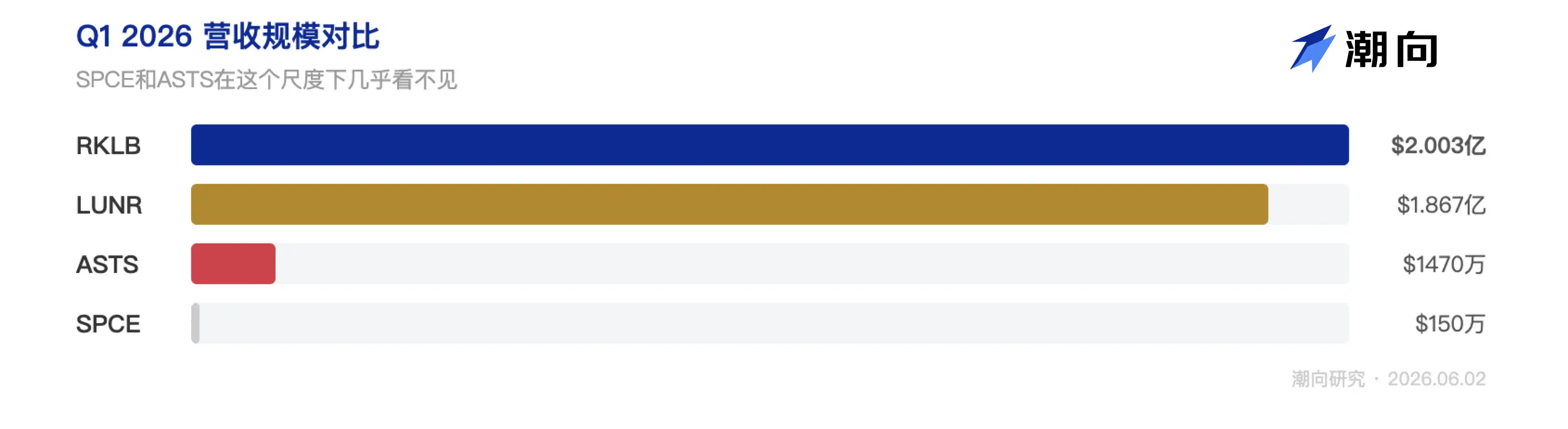

From the table above, RKLB is the only one among the four with substantial and accelerating revenue.

Looking at this year's Q1 revenue for these companies, RKLB's revenue was earned deal by deal, increasing 63.5% year-over-year, beating analyst expectations. LUNR's number is similar in size, but a large portion comes from consolidating the revenue of Lanteris, a company it acquired for $800 million this year. Excluding that part, its organic growth is less dramatic, and its final revenue still missed analyst expectations by 9%.

ASTS and SPCE's revenue bars are almost invisible in this chart; their revenue scale is negligible compared to the first two.

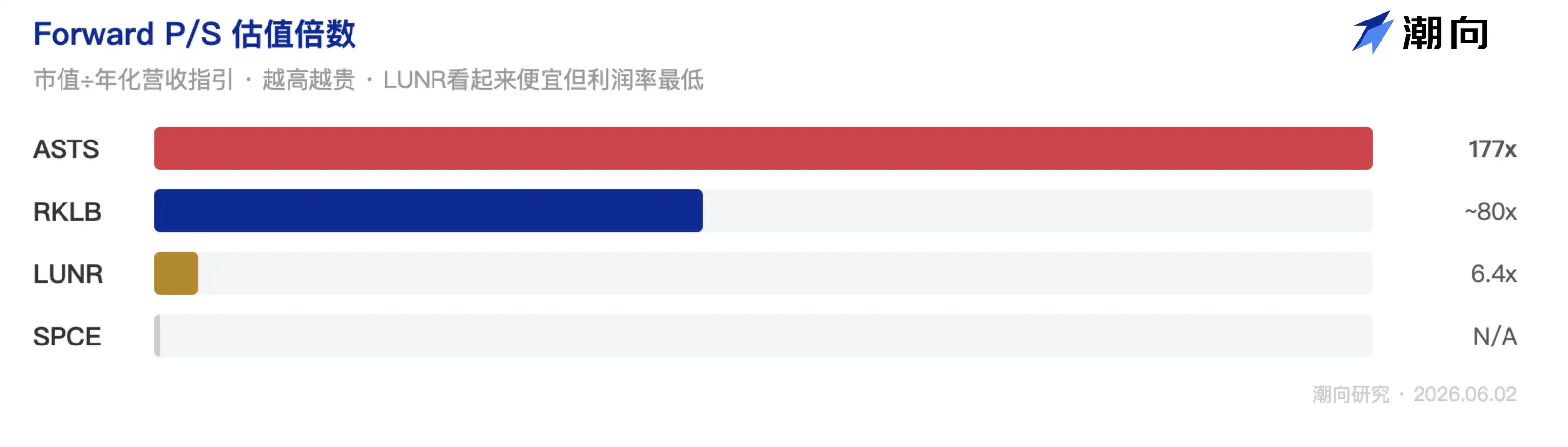

RKLB: The Only One with Accelerating Fundamentals, But $122 Is No Longer Cheap

Rocket Lab is the second-largest US rocket company. Its self-developed Electron small rocket has completed over 50 launches, while also building satellite platforms and space components sold to NASA, the Department of Defense, and commercial customers. Government and commercial revenues are roughly split, making its customer base much more diversified than the other three.

The company's biggest variable is the Neutron medium-lift launch vehicle currently under development. Neutron is positioned as a direct competitor to SpaceX's Falcon 9. If its maiden flight succeeds, RKLB would upgrade from a 'small launch service provider' to 'the only listed company besides SpaceX capable of launching medium payloads.' The target for the first flight is Q4 2026, but it has been delayed twice before (due to a first-stage tank test failure causing schedule adjustments). This also means valuations differ vastly between success and failure scenarios.

Regarding this company's Q1 financial figures, they are visible in the charts later. Here are three things the table doesn't show:

First, within its $2.2 billion backlog, there's an $816 million SDA (Space Development Agency) satellite contract, the largest single order in Rocket Lab's history, indicating the company is transitioning from a launch service provider to a 'full-stack space supplier.'

Second, Q1 saw the signing of 5 exclusive Neutron launch contracts, meaning customers booked flights before the rocket even flew, showing increasing market confidence in Neutron.

Third, CEO Peter Beck cashed out $142 million over the past six months. Although part of a 10b5-1 plan, this level of selling is not insignificant within the aerospace industry.

In terms of valuation, the company's Forward P/S is around 80x. This multiple embeds three assumptions: Neutron's success, continued growth in defense contracts, and further gross margin expansion. Any failure to meet these could challenge sustaining this valuation.

Overall, the current price of $122 has already priced in good news relatively fully. A return to the $96~$102 range (near the 50-day moving average) would offer a much better risk-reward ratio.

Tide Direction Judgment: Leaning bullish, but waiting for a better price is advisable. Core catalysts are Q4 Neutron maiden flight progress and the Q2 earnings report on August 6.

The Other Three: Need to Wait for More Catalysts, Beware of Squeeze Rallies

We can pull the core financial metrics of these 4 hot space stocks together for a more intuitive view:

LUNR: $187M Revenue Tripled, But Mainly from Acquisitions

Intuitive Machines delivers NASA equipment to the lunar surface and is a core contractor for NASA's CLPS (Commercial Lunar Payload Services) program. The Q1 revenue tripling looks impressive, but the $800 million acquisition of Lanteris and its consolidation was the primary contributor; organic growth is far from the stated 199%.

On the other hand, revenue missed expectations by 9%, and EPS missed by four times.

The IM-3 lunar landing mission in the second half of the year is the decisive milestone. The previous IM-1 lander tipped over, and IM-2 landed but had limited communication. If IM-3 can achieve a soft landing at the lunar South Pole, follow-on NASA contracts are likely; failure would significantly discount the whole story.

A Forward P/S of 6.4x appears the cheapest, but gross margin is only 19%, so a low P/S doesn't equal undervaluation. The analyst target price is $40.78, and the current $38.21 is already close.

Tide Direction Judgment: Neutral to slightly bearish. Wait for IM-3 results.

ASTS: The Biggest Story, But Blue Origin Grounding Directly Disrupts the Script

AST SpaceMobile is building a space-based cellular network, allowing standard phones to connect directly to satellites for internet without modification. The 4 billion people worldwide without signal are the potential market. AT&T and Verizon have signed cooperation agreements, and the FCC has issued licenses.

The story framework is not the problem; the issue may lie in the execution timeline. To achieve meaningful coverage, it needs to launch 45-60 BlueBird satellites into orbit before year-end, but Blue Origin's grounding directly eliminated one launch pathway.

Satellite analyst Tim Farrar warned that realistically only 3-5 Falcon 9 launches might be available this year. Deutsche Bank has already downgraded its rating to Hold. The average analyst target price is $82.24, 22% lower than the current price.

The company holds $3.5 billion in cash, so it's not short on funds in the near term. However, a Forward P/S of 177x prices in all satellites launching on time.

Tide Direction Judgment: High risk. Wait for Blue Origin's return-to-flight schedule to become clear before considering.

SPCE: The Most Discussed on Reddit, Beware of Short Squeeze

Virgin Galactic operates suborbital space tourism, with tickets costing $750,000. After pausing commercial flights in 2024 to focus on developing the Delta spacecraft, Q3 plans include glide tests and Q4 power tests. Q1 revenue was $1.5 million (not billion), with a market cap of $760 million.

The driving forces behind this surge are: Blue Origin competitor's incident + short interest of 23.2% triggering a short squeeze + retail FOMO. Trading volume reached 12 times the daily average, triggering a volatility halt intraday.

The RSI has reached 90 (this indicator fluctuates between 0 and 100; exceeding 70 is considered overbought, and 90 is an extreme state...).

Tide Direction Judgment: Avoid. No revenue support, no profitability timeline. Highest Reddit discussion volume does not equal the highest investment value.

Has It Fallen into a Golden Pit? Still Too Early to Say

Answering the article's title question: We believe it's not a golden pit yet, but if the decline continues, RKLB might be approaching a reasonable entry range.

The Blue Origin explosion is a material negative (directly impacting ASTS's launch plans). The SpaceX IPO is a short-term capital flow shock (sector attention might actually rise post-listing). High-level profit-taking itself is healthy.

The long-term logic for the sector isn't broken, but short-term pricing has indeed run ahead of fundamentals.

If we must rank these four. RKLB is the only one worth seriously tracking. With its $2.2 billion backlog, 43% gross margin, and continuous beats, its scarcity as the 'only listed full-stack space company' might actually become more pronounced after SpaceX goes public.

But the current $122 is probably still expensive; $96~$102 looks more like a reasonable range.

-----

This article is based on public information and independent analysis, for reference only, and does not constitute investment advice. Investing involves risks, caution is advised when entering the market.

Data Sources: Yahoo Finance · SEC Filing · TradingView · Reddit/ApeWisdom · Stocktwits · CNBC · TipRanks · Simply Wall St

Tide Research · TideResearch · June 2, 2026