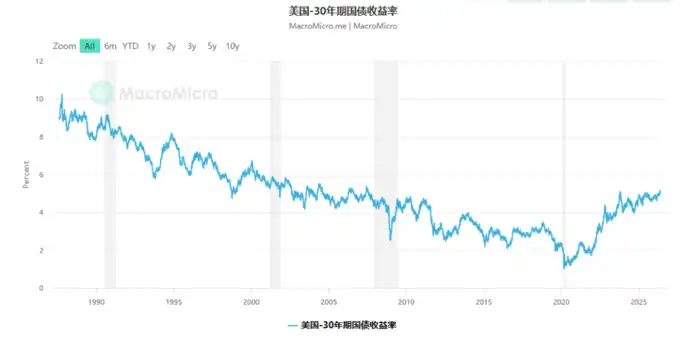

The yield on the 30-year Treasury bond has once again broken through 5%. This time, the market's reaction is markedly different from that in 2023—investors are beginning to truly accept the reality that high interest rates will persist for a long time.

Analysis points out that behind this lies a deeper structural shift: the three pillars supporting low inflation and low interest rates in the U.S. over the past 50 years—cheap capital, cheap labor, and cheap energy—are simultaneously eroding. And the direction of AI will be the biggest unknown determining future inflation trends.

The yield on the 30-year U.S. Treasury bond recently broke through 5% again. Writing in the Financial Times, columnist Rana Foroohar points out that, unlike the brief breach of 5% in 2023 followed by a rapid decline, this time the market's reaction is distinctly different—investors finally seem to be truly accepting the reality that the U.S. is bidding farewell to the era of low interest rates and entering a new phase with more persistent and diverse inflationary pressures.

The article cites a recent report to clients by Apollo chief economist Torsten Sløk, which states, "Investors should position their portfolios for a persistent high interest rate environment in the short, medium, and long term."

Behind this lies a larger structural story: the three cheap factors that drove U.S. economic growth over the past 50 years—cheap capital, cheap labor, and cheap energy—are simultaneously reversing.

How Did Half a Century of "Cheap Dividends" Come About?

The nearly half-century-long downward trend in the 30-year Treasury yield, falling from around double-digit percentages in the early 1980s to about 1% during the pandemic, was not an accident.

It was underpinned by a complete macro logic:

Cheap Capital: Decades of globalization and manufacturing technology advancements kept goods prices low; oil-exporting countries recycling massive petrodollars into the U.S. provided ample cheap funding; pension privatization reforms spurred enormous demand for various financial products; global investors vied to buy U.S. Treasuries, as no country was safer than America.

Cheap Labor: Outsourcing of industries, weakening of unions, automation waves, and the "shareholder primacy" corporate culture (emphasizing financial engineering over employee investment) collectively suppressed wages, especially for non-college-educated workers, persistently supporting corporate profit margins.

Cheap Energy: The petrodollar system helped curb inflation to some extent, and the global energy trade being settled in dollars also reinforced the dollar's global dominance.

These three pillars jointly supported half a century of low-inflation, low-interest-rate prosperity in the U.S.

The Three Pillars Are Simultaneously Loosening

In her article, Rana Foroohar notes that each of these supporting factors is now changing.

On the Capital Front: With each U.S. Treasury auction, international buyers are decreasing, not increasing. Deglobalization and supply chain reshoring will push up goods and services prices in the short term. Meanwhile, the foundation of the petrodollar system is being eroded.

On the Energy Front: Continued tensions in the Middle East directly impact Asian energy-importing countries. But in the longer term, this may accelerate the deployment of clean energy in major Asian nations—while the U.S. is retreating from climate commitments. This means long-term capital flows may shift from the U.S. to major Asian countries.

On the Labor Front: In recent years, labor shortages, large-scale strikes (including successful union action in the auto industry), tighter immigration restrictions, and growth in union membership in some sectors (especially white-collar industries) have all pushed wages higher. However, this trend is being partly offset by two factors: one is rising corporate healthcare insurance costs, leading companies to hedge by suppressing wages; the other is the impact of artificial intelligence.

And Then There Are the Slow Variables: Debt, Geopolitics, and Populism

In addition to the explicit factors above, there are several "slow variables": rising government debt, intensifying geopolitical friction, and the spread of populism.

The combined effect of these risks is that lenders demand a higher risk premium to lend money out—especially for terms of several years.

This directly pushes up long-term interest rates, i.e., the yield on the 30-year Treasury bond.

AI: Savior or New Source of Inflation?

Of all the variables, the direction of artificial intelligence is the most difficult to judge, yet its impact could be the most far-reaching.

Rana Foroohar outlines two starkly different scenarios:

The Optimistic Scenario: The productivity benefits of AI diffuse widely across industries and individuals, creating new jobs and income sources. Models from Yale's Budget Lab show that in this scenario, U.S. national debt would fall significantly, and inflation would also recede.

The Pessimistic Scenario: AI serves merely as a tool for corporate layoffs, cost compression, and profit expansion, while the infrastructure construction of AI itself (consuming vast amounts of chips, land, water, and electricity) creates new inflationary pressures. The net effect is to raise, not lower, costs. Governments would also be forced to bail out displaced workers, increasing debt instead.

Currently, AI giants are voraciously consuming real estate, chips, water resources, and electricity, already pushing up the prices of these resources in the overall economy. The final outcome will likely take years to become clear.

The Real Challenge Facing Investors

The article's conclusion is direct and sobering: Most market participants have spent their entire careers in the "cheap era." Their intuition, models, and expectations were calibrated in a low-interest-rate environment.

And now, that environment is changing.

"Expectational inertia" is a powerful force—when the 30-year yield broke 5% in 2023, many thought it was just a brief anomaly that would soon recede. But this time, the market's reaction is already different.

Adjusting means abandoning old expectations. For investors accustomed to low interest rates, that is no easy task.