The market's fear of downside risk has nearly vanished, and a core pricing mechanism in the options market is failing.

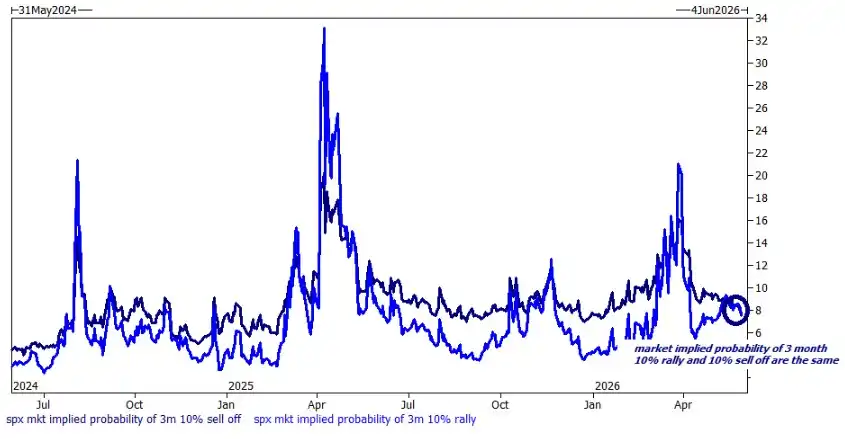

In a latest weekend report, Goldman Sachs derivatives strategist Brian Garrett pointed out that the volatility skew of S&P 500 options has fallen to an 18-month low. The market is pricing a roughly 8% probability for both a 10% decline and a 10% rise—a phenomenon directly characterized by Goldman's volatility team as 'Skew Failure.'

At the same time, the Goldman Sachs Panic Index closed in single digits, hitting a two-year low, indicating that market demand for hedging against tail risks has fallen to extremely low levels.

This signal appears against the backdrop of the U.S. stock market's continued surge. The S&P 500 has been hitting record highs on average every five trading days this year, and Micron's stock price surpassed $1,000 for the first time after hours on Sunday.

Garrett admitted that internal team discussions have evolved from 'Make it stop' in March to 'This is still going up?' in May. However, his own stance is shifting from cautious optimism to increasing pessimism, and he clearly listed several bearish reasons.

Three Bearish Signals Emerge, Cracks Appear Between Market Sentiment and Fundamentals

Garrett listed three major concerns in the current market.

First, market leadership is extremely narrow. The top ten weighted stocks in the S&P 500 now account for 40% of the index's weight, and the last four record highs occurred when overall market breadth was negative—a phenomenon that has never occurred before.

Second, thematic concentration is extremely high. Year-to-date, the S&P 500 excluding AI-related stocks has lagged the overall index by 700 basis points.

Third, price action is highly similar to history. Garrett noted that the 2026 price pattern closely resembles that of late 1998 to 1999.

Although bearish voices are flooding media headlines and social media, Garrett emphasized that this concern is not reflected in the pricing of the options market—at least, the fear of downside risk is almost nowhere to be seen.

Skew Failure: Downside Hedging Costs Fall to Historic Lows

Goldman's volatility team provided three key observations from the options market.

First, the S&P 500 volatility skew has fallen to an 18-month low. This move is driven by two forces: the put wing is unusually cheap, while the call wing is relatively expensive.

Second, the Goldman Sachs Panic Index closed in single digits last Friday, hitting a two-year low. This index synthesizes the two-year percentile rankings of VVIX, VIX, Skew, and at-the-money volatility.

Third, and most crucially: the market prices the probability of a 10% decline and a 10% rise as exactly the same, both around 8%. This means the options market no longer assigns extra premium to downside risk; the protective function of Skew has effectively failed.

Garrett pointed out that the direct implication of the above phenomena is: for investors looking to hedge correlation risk, the current hedging cost is extremely low.

Low-Cost Hedging Paired with Right-Tail Positioning

Based on the above assessment, Garrett provided several specific trade recommendations.

For investors bullish on market style rotation, expecting the rally to shift from concentration to dispersion, Goldman recommends buying RSP (Invesco S&P 500 Equal Weight ETF) outperformance options relative to SPX, with a 1-month 100% outperformance option costing about 145 basis points. It also recommends buying VIX call options as a hedging tool, noting that the term structure for August and beyond is extremely flat, with VVIX at 86.

For investors seeking simple downside protection, Garrett suggests directly buying S&P 500 put options—given the extremely low put skew, the payout structure is quite attractive.

Additionally, Goldman recommends going long Bitcoin ETF volatility with delta-neutral hedging. Garrett noted that Bitcoin has historically performed like a 'leveraged Nasdaq,' but its current pricing is at a two-year low and about 10 volatility points lower than SMH.

Fund Flows: Hedge Funds Net Buyers for Two Consecutive Weeks, Single-Stock ETF Assets Double

According to Goldman's latest Prime Brokerage data, hedge funds have been net buyers for two consecutive weeks, at the fastest pace this year, mainly reflected in long additions and macro short covering.

Significant sector rotation is evident: Financials (down 6% YTD) saw net buying, while Industrials (up 11.5% YTD) saw net selling.

On the futures side, end-user positioning has rebounded to near 2024 highs. Goldman's team specifically noted that levered ETFs are mechanically expanding their balance sheet size; CTA strategies are currently positioned near neutral, but systematic strategies show clear asymmetry towards the left tail—buying about $12 billion in a flat 1-month scenario versus selling about $100 billion in a down 1-month scenario.

Notably, global leveraged and inverse single-stock ETF assets under management have surpassed $60 billion, doubling in two months. The size of this niche market can no longer be ignored.