By Ma He, Foresight News

On the evening of June 10th, Beijing time, the U.S. Bureau of Labor Statistics officially released the Consumer Price Index (CPI) data for May 2026. The report showed that driven by a significant surge in energy prices triggered by geopolitical conflicts, U.S. inflationary pressures rebounded noticeably, further dampening market expectations for the Federal Reserve's interest rate cut path within the year. According to data from the U.S. Bureau of Labor Statistics, the CPI rose 0.5% month-over-month (seasonally adjusted) in May, slightly slower than April's 0.6% increase, but rose 4.2% year-over-year (unadjusted), accelerating significantly from 4.2% in April and reaching the highest level since April 2023. Core CPI (excluding food and energy) rose 0.2% month-over-month, below market expectations of 0.3% and April's 0.4%; it rose 2.9% year-over-year, slightly up from the previous reading of 2.8%, in line with market expectations.

Energy prices were the core driver of this month's inflation rebound. The energy index rose 3.9% month-over-month and surged 23.5% year-over-year. Among them, gasoline prices rose 7.0% month-over-month, soaring 40.5% year-over-year; fuel oil rose 58.9% year-over-year. The U.S. Bureau of Labor Statistics explicitly stated that the energy index contributed to over 60% of the month-over-month increase in the overall CPI for May. Geopolitical conflicts involving Iran and related tensions have continued to push up international oil prices since February, with WTI crude once breaking above $100 per barrel, directly transmitting to U.S. domestic gasoline and energy service costs.

Following the data release, by the close on June 11th, the S&P 500 index fell approximately 1.62%, and the Nasdaq index declined 1.98%. The U.S. dollar index strengthened, and the U.S. Treasury yield curve shifted upward overall.

As a typical risk asset, the crypto market also faced clear pressure—Bitcoin price fluctuated between $61,000 and $62,000 around the data release, with market concerns that hot data could further squeeze liquidity expectations.

No Fed Rate Cuts This Year?

More crucial was the repricing in the interest rate derivatives market. According to the CME FedWatch Tool, the probability of the FOMC meeting on June 16-17 maintaining the federal funds rate unchanged in the current 3.50%-3.75% target range exceeds 96%. The probability of rate cuts for the entire year has significantly decreased, with some traders even starting to price in the possibility of the first rate hike at the end of 2026 or in 2027. The market had previously anticipated 1-2 rate cuts of 25 basis points in 2026, but this path has now been substantially delayed or canceled.

Most institutions believe that this CPI reinforces the expectation of 'higher-for-longer' interest rates, but there is still some distance from truly restarting a rate hike cycle.

Olu Sonola, Chief U.S. Economist at the international credit rating agency Fitch, said: "Headline inflation is indeed hot and heating up, but this isn't yet a story of panic-style rate hikes." He believes that core inflation remains relatively contained, providing the Fed with room to continue holding steady. What will truly determine the policy direction moving forward will be the upcoming months' core inflation and inflation expectation data.

Seema Shah, Chief Global Strategist at Principal Asset Management, stated that while headline inflation above 4% remains unsettling, energy is the primary driving force, and housing inflation is moderating, with no broad "second-round inflation effects" seen yet. Therefore, the Fed still has reason to remain patient.

She also pointed out that the market's current pricing for further rate hikes may be on the high side.

J.P. Morgan Asset Management believes this data may be close to a cyclical peak in this round of inflation. David Kelly, the firm's Chief Global Strategist, said that although inflation levels remain above the target range, "the most likely decision for the Fed at the upcoming policy meeting is to keep rates unchanged" and continue observing subsequent data changes.

The latest data from Kalshi shows the market's bet on the Fed holding rates steady this year has surged to 72%, while the probability of a single 25-basis-point cut has dropped to 18%.

This stands in stark contrast to market expectations at the beginning of the year. In early 2026, the market generally believed the Fed would start a rate-cutting cycle against the backdrop of persistently declining inflation. April's CPI year-over-year had already risen to 3.8%, and the May data further confirmed the inflation rebound trend, making the high-interest-rate policy environment a mainstream narrative once again. While the external shock from energy prices has some temporary nature, if it transmits to core service prices, it will force the Fed to reassess the neutral interest rate level.

For the new Chair Wash, the June meeting is an important debut. Wash was formally sworn in as Fed Chair in late May 2026, succeeding Jerome Powell whose term ended. The June meeting will release a new Summary of Economic Projections and dot plot, and the market will closely watch officials' latest assessments of the inflation path, labor market, and policy rates.

Analyzing at a deeper level, the slowdown in core CPI month-over-month to 0.2% in May provided some relief signals, indicating underlying inflation pressures are not spiraling out of control broadly. However, the Fed historically places more emphasis on the "trend" of core indicators rather than single-month fluctuations, especially against a backdrop of volatile energy prices. The persistent stickiness of housing costs, potential second-round effects (energy costs pushing up other goods and services prices), and geopolitical uncertainties all add complexity to policy formulation.

Crypto and U.S. Stocks

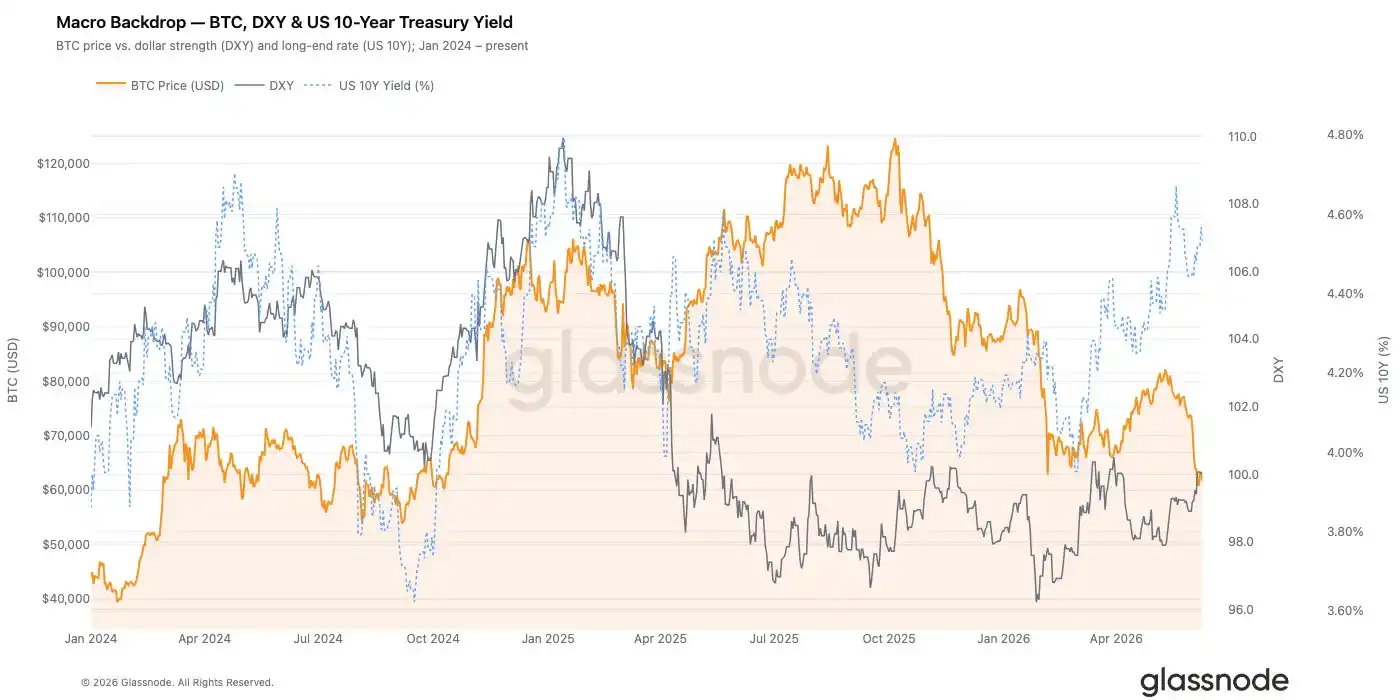

The Fed's policy path is the core anchor for the global liquidity environment. A high-interest-rate or delayed-rate-cut environment is typically accompanied by a stronger dollar, rising U.S. Treasury yields, and pressure on valuations of risk assets. The correlation between crypto assets like Bitcoin and growth-oriented assets like Nasdaq has significantly increased over the past few years. Marginal changes in liquidity expectations are often first reflected in BTC prices and ETF fund flows.

Data from SoSoValue shows that since May this year, Bitcoin spot ETFs have seen significant and continuous net outflows, putting pressure on Bitcoin's price. BTC once fell below the $60,000 mark, later fluctuating around $62,000, with the risk of breaking down again at any time.

Although the current crypto ecosystem is much more mature than during the 2022-2023 bear market, in the short term, CPI data could still trigger a pullback in risk appetite, leverage unwinding, and amplification of short-term volatility.

The latest weekly report data from Glassnode shows that Bitcoin continues to exhibit characteristics of a later-stage correction, with recent buyers suffering significant losses, realized losses remaining high, and several major sources of demand substantially weakened. Bitcoin's price drop to around $60,000 triggered a significant deleveraging event, clearing a large number of speculative positions in the market. While this helps reset leverage levels, spot demand has not yet shown substantive recovery. The options market remains in a defensive posture, implied volatility stays elevated, demand for downside protection is strong, and dealer positioning is concentrated around current spot levels. Combined with declining institutional participation and slowing corporate treasury accumulation, these data points indicate that risk appetite remains low.

Overall, the market appears to be progressing further into a capitulation phase. Although leverage has largely been reset and valuation metrics have reached historically low levels, the demand response typically associated with long-term market lows has not yet materialized.

Historical experience shows that when inflation is mainly driven by supply-side factors like energy and core data remains relatively controlled, markets often gradually repair expectations for a "soft landing" after digesting the initial shock.

As for U.S. stocks, major investment banks maintain optimistic expectations. J.P. Morgan Asset Management believes this data may be close to a cyclical peak in this round of inflation. David Kelly, the firm's Chief Global Strategist, said that although inflation levels remain above the target range, "the most likely decision for the Fed at the upcoming policy meeting is to keep rates unchanged" and continue observing subsequent data changes.

J.P. Morgan indicates that "one-off shocks" like energy shocks may become the new normal. The AI investment cycle continues, but it also warns that inflation is higher than pre-pandemic, the correlation between stocks and bonds may structurally increase, and the 60/40 portfolio faces greater pressure.

Goldman Sachs recently raised its year-end target for the S&P 500 to 8,000 points (previously 7,600), expecting 24% EPS growth in 2026. It believes earnings growth remains the main driver of the stock market, though it noted in recent comments that the probability of Fed rate cuts this year has significantly decreased.