Author: Smac, Partner at Compound VC

Translation: Saoirse, Foresight News

Editor's Note: Market hotspots are emerging one after another, with the AI frenzy sweeping across the board, while some question whether it will repeat the bubble of the metaverse. Amidst the clamor, people are often swept up by current trends, unable to see the long-term picture. To make rational judgments, one must learn to elevate their perspective. Smac, a partner at Compound, uses a meteorological analogy to dissect the market logic behind the rotating bubbles.

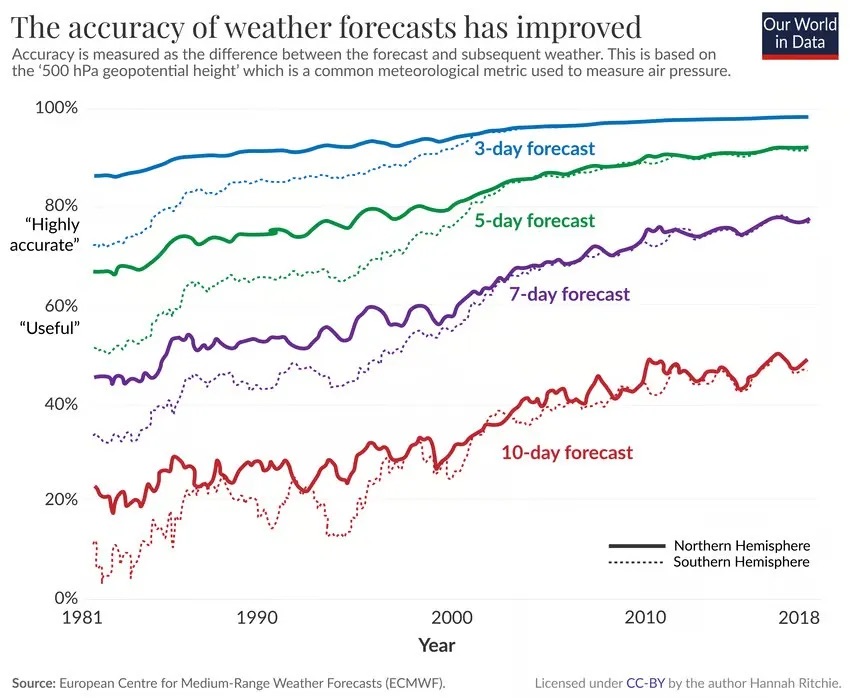

Meteorology is a fascinating field. Over the past fifty years, various forecasting tools have evolved, increasing the accuracy of weather predictions. Today's five-day forecast is as reliable as the single-day forecast from thirty years ago.

To most people, weather is a coherent, moving system: clouds roll in, rain falls, it stops, and it clears. Imagine a winter front arriving; the image that likely comes to mind is a vast, grey cloud cover stretching hundreds of miles, dumping heavy snow. Meteorologists call this stratiform weather, essentially like a layered cake, where the same weather experience unfolds across the covered area.

But weather isn't limited to this single form. If you've seen a summer thunderstorm in the plains, you'll notice it operates differently. First, an individual convective cell forms: warm, moist air near the ground rises, meets cold air aloft, condenses, and forms a towering, localized cumulonimbus cloud. Within an hour, hail, lightning, and torrential rain follow, visibility dropping to under a hundred meters.

Once the cell reaches its peak and releases its energy, it gradually dissipates. The storm's downdraft of cold air spreads outward at speeds up to 40 miles per hour. When this cold air collides with surrounding warm, moist air that hasn't yet formed a storm, it acts like a wedge, pushing the warm air upward again.

As long as sufficient atmospheric instability exists, this "cold air wedge" can trigger a new convective cell ten or more miles away from the original storm.

The new cell couldn't have formed on its own; the energy was already present in the atmosphere, lacking only a trigger, which the dying storm provided. Then, the new cell repeats the evolution of the previous storm.

When multiple convective cells form in sequence, they constitute a Mesoscale Convective System. From the ground, one only encounters each storm individually; each one feels like the entire weather system. On one side, all is calm, with people unaware of the coming storm; on the other side, the rain has already passed. But from a satellite's eye view, you see a series of separate cells linked in a line, each at a different stage of development, moving forward until it exhausts the warm, moist air along its path.

Supercell storm cloud near Amistad, New Mexico, at sunset

This sequential storm system requires vastly different atmospheric conditions than a single frontal system:

- Warm, moist air near the surface acts as the storm's "fuel."

- Dry, cold air aloft encourages the warm air to rise, creating atmospheric instability.

- Winds varying with altitude cause the storm to rotate and move laterally, known as wind shear.

When these three conditions align, a parade of storms unfolds.

After all this meteorology, back to the point: the financial markets today operate almost exactly like this meteorological phenomenon.

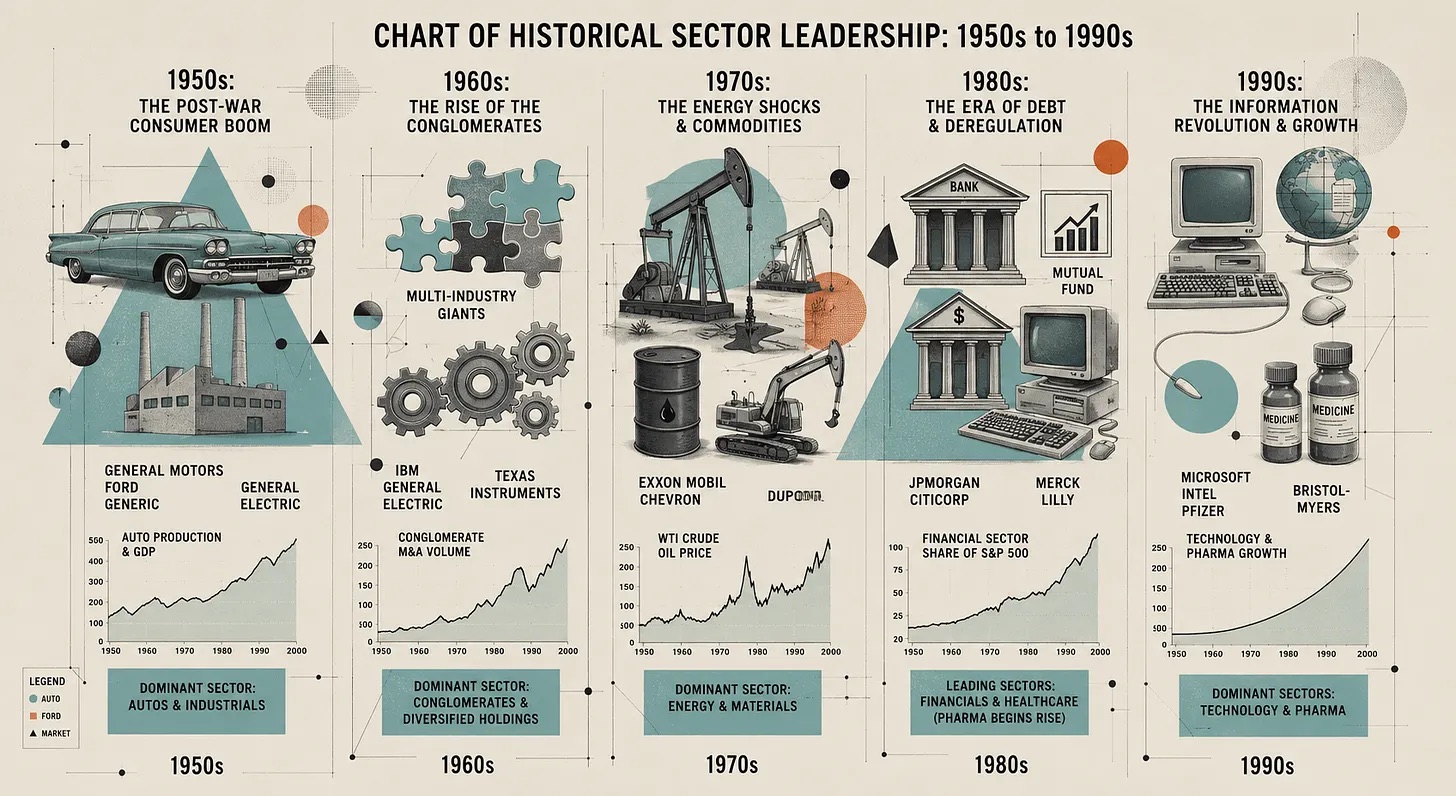

The markets of the past were like stratiform weather systems: a multi-year bull market, followed by a multi-year bear market, with slow rotations of sector leadership. The 1982-2000 long bull market, followed by the internet bubble, then the 2003-2007 real estate and credit cycle. These cycles were long and clear. Even if investors' timing was off by years, understanding the major trend still led to profits.

But today's market is nothing like that. We are in a convective storm chain market: one hot sector after another hits like sequential storms. To those inside, each surge feels unstoppable and all-encompassing.

Capital flows out of fading narratives and ignites new frenzies in adjacent areas. The pace of leadership rotation has dramatically accelerated—AI infrastructure, GLP-1s (a class of diabetes drugs popular for weight loss, now a hot investment theme), stablecoins, quantum technology, nuclear energy, decentralized autonomous tech, robotics, space... Each undergoes a complete hype cycle, with its own cohort of true believers, a full narrative arc, and inevitably, a correction. The "cold air" from the dying bubble spreads out, igniting the next hotspot in a new area.

Refusing to acknowledge this fundamental market shift is self-delusion. People love to mock the phrase "this time is different," but ignoring permanent changes in the financial environment is either intellectual laziness or stubborn nostalgia for a market that no longer exists.

A Market Landscape Transformed

For a long time after WWII, financial markets moved at the pace of slow-moving weather systems. A bull market could last ten, fifteen, even twenty years, with rotations still anchored to long-term secular trends.

Approximate timeline of thematic sectors and leading market segments

Back then, sector rotations occurred within a unified macro backdrop. Only at major inflection points—the breakdown of Bretton Woods, Volcker's anti-inflation push, the peak of the dot-com bubble, the Global Financial Crisis—did the grand market regime truly shift.

This structure arose from many factors: high transaction costs, minimal retail participation forcing a long-term holding mindset, pension funds as the primary retirement vehicle. The S&P 500 was dominated by manufacturing, energy, banking, and retail—companies whose earnings grew roughly in line with the economy, stable and predictable. Information also moved slowly; an annual report might take weeks to be digested by most investors.

Volatility was also more symmetrical. Deep corrections followed bull markets, with leverage unwinding slowly over long periods. Rallies in bear markets were similarly gradual. The market lingered in different emotional states for long stretches, with regime changes measured in quarters or years.

In the weather analogy, the old market had: moderate fuel, high atmospheric stability, weak wind shear. Long, smooth waves. Investors could plan accordingly. Today, all environmental conditions have changed, some reversed, leading to a structural transformation.

Where Did the Change Come From?

Numerous shifts intertwine and amplify each other, each alone powerful enough to reshape markets. In summary, there are eight core transformations:

- The Democratization of Speculation

- The Formation of Perpetual Buyers

- Passive Investing Creates Inelastic Counterparties

- The Rise of Multi-Strategy & HFT, The Disappearance of the Middle

- Volatility Suppression

- A Complete Shift in Index Composition

- The End of Information Latency

- Fiscal & Monetary Regime Change

1. The Democratization of Speculation

The participant base has visibly changed. In the 1990s, retail trading accounted for only ~10% of US equity volume. High commissions meant retail mostly bought and held stocks, with little active speculation.

Robinhood pioneered zero-commission trades and payment for order flow. In Fall 2019, Schwab eliminated commissions, followed by Fidelity, TD Ameritrade, E*Trade—rewriting the rulebook.

Covid accelerated this: stimulus checks, idle time at home, gamified mobile trading apps. Retail's share of volume surged to ~25% in 2020-2021. Many thought it was temporary, but elevated retail participation persists. On April 29, 2025, amid market gyrations from tariff news, JPMorgan data showed retail order flow hitting a record 48% of volume. On normal days, it's over double pre-Covid levels; during big moves, it can reach 35%.

The deeper change is in *what* retail trades. Single-stock options dominate, with zero-day-to-expiration options exploding. The new cohort is younger, highly concentrated, trades narratives. Critically, they often use leverage not captured in margin data, and trade more on price action than fundamentals, heavily influenced by social signals.

In weather terms: the market's "warm, moist air" near the surface is more abundant than ever, with immense latent energy potential.

2. The Formation of Perpetual Buyers

I've written about this before. In short, the US retirement system shifted from Defined Benefit pensions to Defined Contribution plans. Individuals now must manage their own retirement savings. This translates to a massive, price-insensitive, passive flow of capital into equities every pay period—an automated, perpetual bid.

Traditional pensions operated differently: DB plans had to manage duration risk against liabilities. Managers made active judgments on valuation; if stocks were expensive, they could tilt towards bonds. Even if slow-moving, this was far more active than today's purely passive perpetual bid.

This is crucial: the marginal trading dollar today has far more price impact than before.

3. Passive Investing Creates Inelastic Counterparties

Passive index investing, by definition, buys and sells irrespective of price, purely based on index weight. The higher a stock's market cap, the more passive money flows in, and vice versa. This inherently embeds momentum into the market's plumbing. The Magnificent Seven's dominance is partly fueled by this.

Countless articles have detailed index concentration. Yes, these companies are exceptionally profitable and growing. But the core issue: there is no natural "sell" switch for passive flows.

4. The Rise of Multi-Strategy & HFT, The Disappearance of the Middle

While perpetual passive buyers formed, the active trading landscape also transformed. The hallmark is the rise of multi-strategy pod shops: Citadel, Millennium, Point72, Balyasny—housing hundreds of independent PMs running specific strategies under strict risk controls. AUM for these firms exploded, concentration mirroring index concentration.

Simultaneously, High-Frequency Trading now accounts for 50-60% of US equity volume, ~75% in futures. This combination creates a fragile market microstructure: funds trade against each other, weakening price discovery. Much of the volume is just capital churning within the system.

In normal times, bid-ask spreads are razor-thin—a good thing. But when a narrative breaks, positioning becomes extreme, or multiple firms' risk limits are breached, the microstructure fails. PMs' risk exposures are highly correlated, stop-loss rules similar. One firm's forced selling triggers others'. Think Feb 2018, Aug 2019, Mar 2020, Aug 2024. The structure enabling these events is now entrenched and will repeat.

Traditional fundamental long/short hedge funds are being squeezed out. These funds ran 20-40 stock books based on deep research, with investment horizons of quarters. Now, they're absorbed into larger platforms, move to private markets, family offices, or single-strategy funds. I believe there's still significant alpha in understanding narrative rotation and patience amidst short-term flows.

5. Volatility Suppression

Combining the above four points, today's volatility regime makes sense. Since 1990, the VIX has closed below 20 on about two-thirds of trading days. Volatility exhibits ~85% day-to-day correlation, meaning today's vol level heavily depends on yesterday's.

But regime shifts are extreme and asymmetrical. Numerous studies show suppressed volatility eventually breaks out violently over a few days, but decays back slowly over weeks.

The reasons are structural: a massive "short vol" industry exists. The rise of 0DTE options means market makers' hedging further suppresses intraday vol. Markets simmer at low volatility, risk builds, and when tail risks emerge, everyone rushes for the exits simultaneously.

Simply put, volatility distribution is now more pathological: long periods of compression lead to more violent decompressions.

6. A Complete Shift in Index Composition

The sixth change is the composition of the indices themselves. In 1980, the S&P 500 was dominated by manufacturers: Industrials, Materials, Energy, Financials, Staples. Their earnings grew roughly with GDP, stable, with valuation multiples mean-reverting. Forecasting P&G's earnings five years out wasn't wildly off.

Today is different. Information Technology, Communication Services, plus tech-heavy names in Consumer Discretionary like Amazon and Tesla, comprise over 40% of the S&P 500. These companies' earnings aren't linear. Software has near-zero marginal distribution costs. AI is profoundly uncertain—will AI labs become the core infrastructure for the next half-century, or money-losing science projects? Opinions diverge wildly.

For such companies, forecasting near-term earnings is hard; long-term value is highly speculative, leading to massive valuation swings. Valuation relies less on financial statements, more on narrative. For investors who can anticipate technological frontiers, competitive moats, and nascent markets, this creates massive alpha opportunities.

Traditional manufacturers expand capacity gradually, DCF models are stable, multiples mean-revert. Now, valuation often hinges on the market's belief in a story. This isn't to say traditional valuation is dead; it's the reality for these new asset types.

Today's major indices are packed with these long-duration, narrative-driven assets. The steeper the temperature gradient in the atmosphere, the more potential energy. Similarly, more of these assets mean more potential market energy, leading to more violent moves when triggered.

7. The End of Information Latency

Everyone feels this intuitively, but its impact is underrated. For most of financial history, market-relevant information traveled with the speed of its distribution medium. Now, information is virtually latency-free.

Especially positioning information travels faster than ever. Investors see real-time reactions of known figures. More people publicize their positions. A torrent of real-time info fuels FOMO. Gain screenshots abound, stories of turning $1k into millions go viral. The fear of missing out is perpetual.

8. Fiscal & Monetary Regime Change

This needs little elaboration. The summary:

- Persistently accommodative US monetary policy, low real rates.

- Quantitative Easing expanding the Fed's balance sheet.

- Low discount rates elevating prices of all long-duration assets.

- Activist fiscal policy—stimulus checks, industrial policy bills.

- Full employment alongside wartime-sized deficits.

- A K-shaped economy, decoupling financial markets from Main Street.

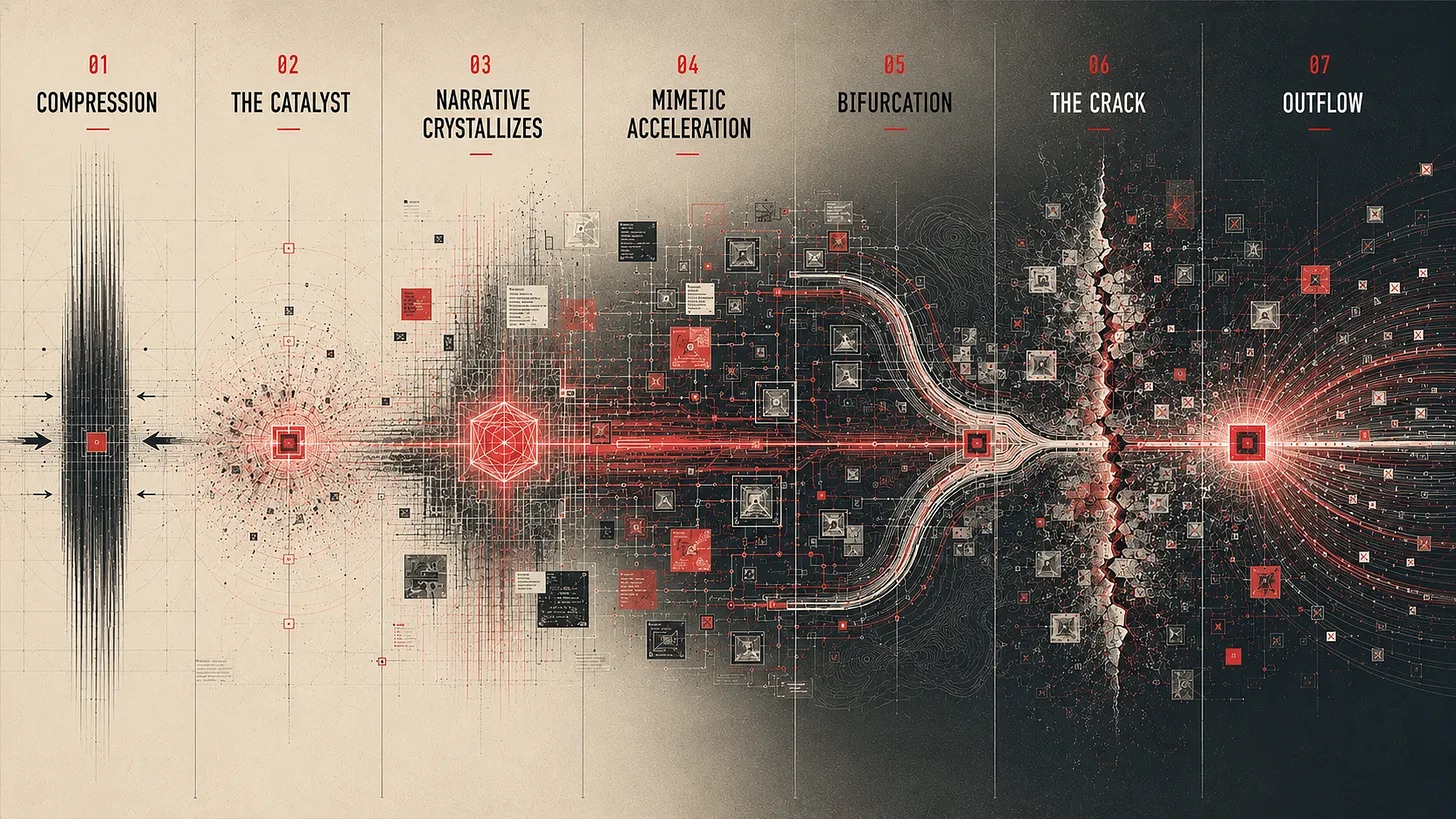

How the Storms Form

Combine all the above, and rotating market bubbles become an inevitable outcome.

The lifecycle is multi-stage and logical:

- Dormancy: Sectors fall out of favor, ignored. But work continues in obscurity.

- Catalyst: A genuine breakthrough—technical, regulatory, earnings—noticed first by deep sector specialists.

- Narrative Formation: A cohesive market narrative emerges, dramatically lowering the cognitive barrier to entry. Purists may hate the simplification, but simple stories enable mass participation.

- Divergence of Opinion: Clear polarization occurs. Beyond true believers, the pool of potential marginal buyers shrinks. The gap between bulls' and bears' valuation estimates widens.

- Break: In hindsight, the peak is always clear. Today's participants are eager to call tops, a natural outcome of the attention economy. Once the narrative cracks, concerted selling begins. Capital seeks a new home.

- New Hotspot Emerges: The outflowing capital—the "cold air wedge"—triggers the next bubble in a new area.

Looking Ahead

The implications of this new regime are profound. We can predict the *shape* of the storm chain, but not the exact *location* of each cell.

Post-Covid, many believed market aberrations were temporary or unique to ZIRP. Some of that was true, but it's now clear the structural shift is permanent. None of the eight drivers are reversing:

- Commissions aren't coming back.

- Passive AUM isn't shrinking.

- Traditional DB pensions are gone for good.

- Social media and information speed will only increase.

- Multi-strategy shops may evolve but, given their scale/profitability, aren't disappearing soon.

- Information latency isn't getting longer.

This environment is the new "climate." Expecting a return to the slow, stratified markets of the 80s/90s is refusing to face reality.

Some argue the duration of each bubble will compress indefinitely. That's hard to say, as it becomes a game of anticipating others' anticipation. But one thing is certain: each cycle educates participants, potentially accelerating the next. Crypto traders now play by traditional market rules. However, narrative-driven cycles have a natural minimum duration; they can't accelerate infinitely.

This rotating bubble market primarily benefits two types of investors. First, **deep sector specialists** who understand the underlying tech, regulation, supply chains, unit economics, and can judge if the narrative can become reality. AI tools will make many think they belong here—a dangerous trap. Second, **regime observers**. Most investors fall here, tasked with identifying what the dominant sophisticated cohort is doing.

And the pipeline of future narratives is rich: AI infrastructure & apps, robotics, embodied AI, precision medicine, crypto, materials science, fusion & advanced fission, grid storage, space, brain-computer interfaces, quantum. Even within a megatrend, different segments (upstream/downstream, layers of the tech stack) will bubble sequentially.

Retail has innate advantages in this market: time flexibility, no investment committee meetings, no quarterly redemption pressures. The effective "buy the dip" strategy of recent years provided a baseline. With proper risk management, retail can thrive here.

Rising Above the Storm

Explaining the structure might sound like I'm making a value judgment. I have my opinions. In venture, we can choose not to fund projects with negative social externalities. But in public markets, the most common error is predicting the market you *wish* existed, not the one that does.

It's a human emotional bug; even Newton fell victim to it.

Emotion is the enemy of returns. Constantly, you see asset managers on TV calling for a crash, a recession. They are perma-bears, rarely right.

The market isn't going back. Is this storm-chain regime more pathological than the old one? I can't say. Objectively, many changes enabling it are positive: lower investment barriers, automated retirement savings, accessible passive vehicles, real-time information—democratizing finance.

On the ground, each storm feels all-encompassing, vision limited to the immediate squall. That's the experience inside each sector bubble: a gravitational pull absorbing all market attention. To see the full chain—one bubble dying, the next igniting—you must actively elevate your perspective. Participants in each cycle are lost in their own mania or despair.

Markets are fascinating because they constantly evolve, yet price discovery remains a human endeavor. Humans are emotional and repeat mistakes. This tension creates what we see: seeming chaos up close, but from a higher vantage, just a rolling sequence of bubbles.

The core intent here is to encourage stepping out of the immediate storm, observing from a higher plane, seeing where the chain is headed, and avoiding being swept away by the emotions of any single bubble.

Simple in theory, demanding immense discipline in practice. Easier said than done.