撰文:Tiger Research

编译:AididiaoJP,Foresight News

摘要

-

尽管私募股权市场提供了高额回报,但其仍然主要面向机构投资者和高净值个人,普通投资者难以参与。

-

代币化可以解决传统金融体系在流动性、准入性和便利性方面的局限性,但仍面临重大的法律和技术障碍。

-

Ventuals、Jarsy 和 PreStocks 等项目正在探索代币化私募股权的不同方法。尽管这些尝试仍处于早期阶段,但它们已经显示出降低市场结构性壁垒的潜力。

私募股权极具吸引力,但普通投资者无法参与

普通人如何投资 SpaceX 或 OpenAI?作为非上市公司,它们对大多数投资者来说遥不可及。普通投资者的参与机会几乎为零,因为投资机会通常只在公司上市后才会出现。

问题的核心在于普通投资者被排除在私募市场创造的高额回报之外。过去 25 年私募市场创造的价值约为公开市场的三倍。

这种结构性壁垒源于两个核心因素。首先私募公司的融资过程高度敏感,无论投资者的资质如何,交易通常只会开放给知名的机构投资者。其次私募资本市场的增长为企业提供了更多融资选择,许多公司现在无需上市即可筹集数十亿美元资金。

OpenAI 是这两种动态的典型例子。2024 年 10 月,它从 Thrive Capital、微软、英伟达和软银等主要投资者处筹集了 66 亿美元。到 2025 年 3 月,它又通过软银领投、微软、Coatue 和 Altimeter 参与的融资轮筹集了 400 亿美元,成为历史上规模最大的私募融资。

这一现象揭示了一个现实:只有少数机构投资者能够参与私募市场,而成熟的私募资本基础设施为这些公司提供了上市之外的融资选择。

因此当今的投资环境正变得越来越封闭,加剧了高增长机会分配的不平等。

平等准入,代币化能否解决结构性壁垒?

代币化能否真正解决私募股权市场的结构性不平等?

从表面上看这一模式颇具吸引力:现实世界的资产被转换为数字代币,实现碎片化所有权,并支持全球市场的全天候交易。但本质上代币化只是将 Pre-IPO 股权等现有资产重新包装为一种新形式。传统金融中已经存在改善准入性的解决方案。

来源:ustockplus

例如,韩国的 Dunamu's Ustockplus、美国的 Forge 和 EquityZen 等平台允许普通投资者在现有监管框架内交易私募股票。

那么,代币化的独特之处在哪里?

关键在于市场结构。传统平台采用点对点(P2P)撮合模式,买家必须等待卖家挂单。如果没有对手方,交易就无法完成。这种模式存在流动性低、价格发现有限和执行时间不可预测等问题。

代币化有望解决这些结构性限制。如果代币化资产在中心化交易所(CEX)或去中心化交易所(DEX)上市,流动性池或做市商可以提供持续的对手方,从而提高执行效率和定价准确性。除了减少摩擦,这种方法还能重新定义市场架构。

此外,代币化还能实现传统金融体系无法支持的功能。智能合约可以自动分配股息、执行条件交易或实现可编程的治理权。这些功能为新型金融工具的诞生提供了可能,这些工具在设计上兼具灵活性和透明度。

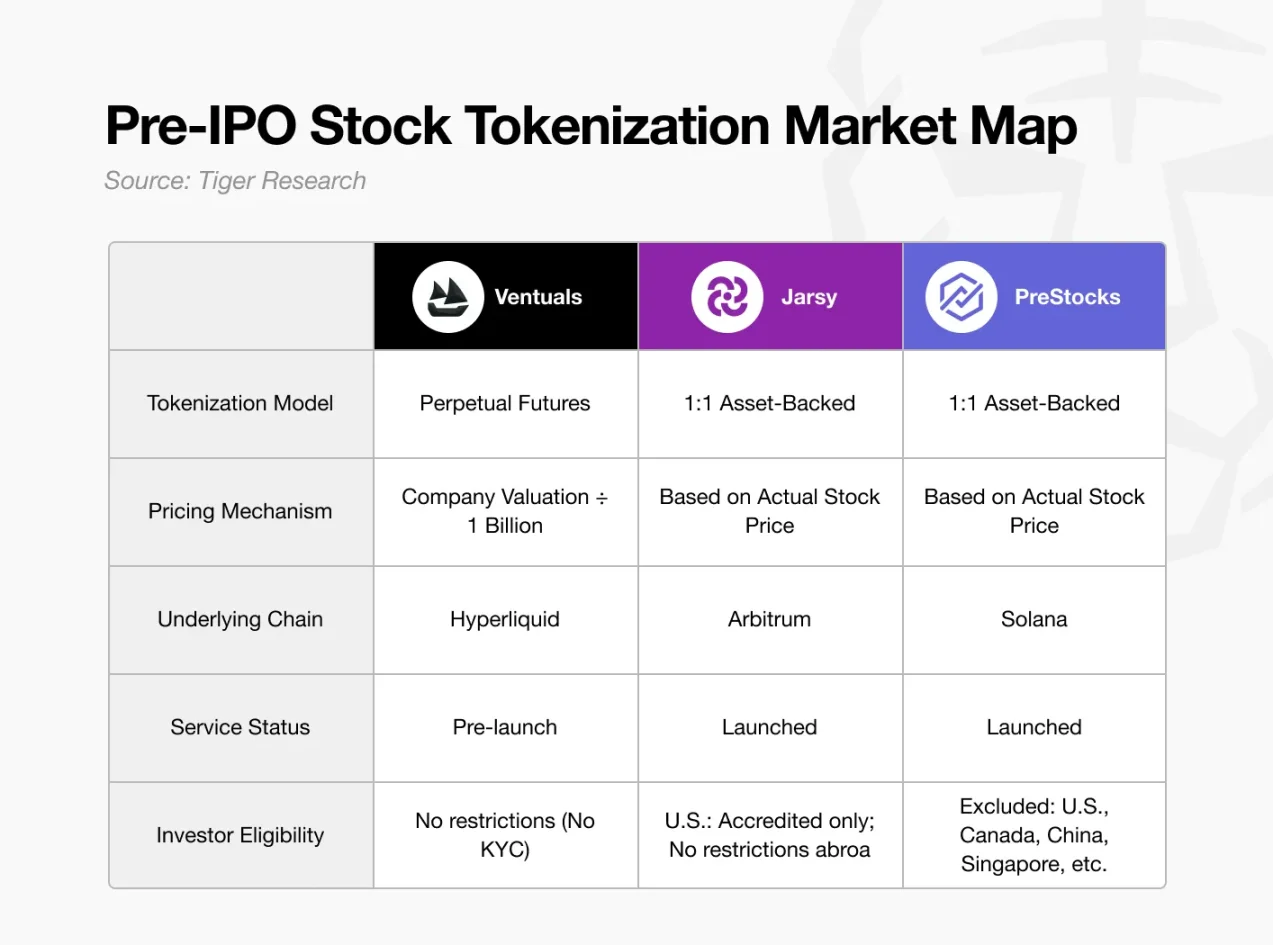

尝试代币化 Pre-IPO 股权的项目

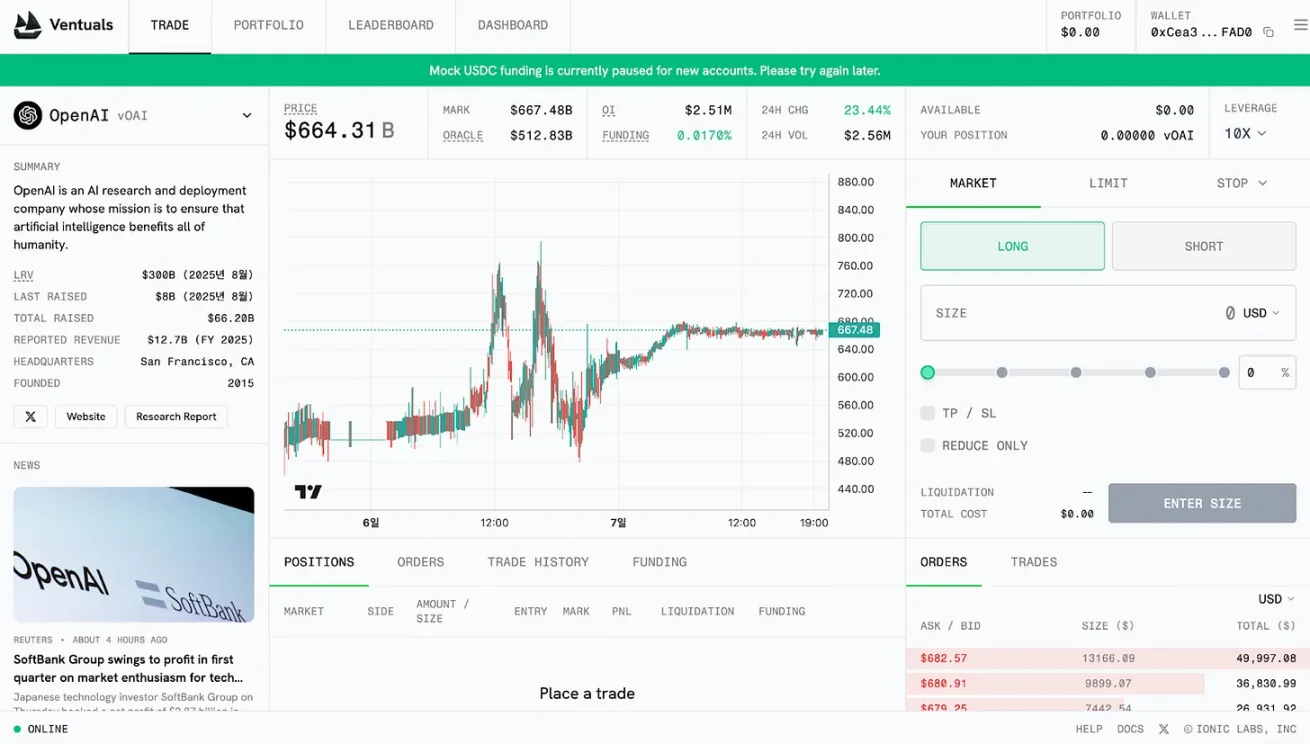

Ventuals

来源:Ventuals

Ventuals 构建的是一种永续合约结构。其核心优势在于无需持有标的资产即可进行衍生品交易。这使得平台能够快速上线大量 Pre-IPO 股票,同时规避身份验证或合格投资者认证等常规监管要求。

永续合约通过 Hyperliquid 的 HIP-3 标准实现。然而该标准目前仅在测试网上运行,Ventuals 仍处于预发布阶段。

其定价模型也非常规,代币价格并非基于股价或实际市场交易,而是通过公司总估值除以 10 亿计算得出。例如如果 OpenAI 的估值为 350 亿美元,那么 1 枚 vOAI 代币的价格为 350 美元。

这种低门槛模式也带来了结构性挑战,其中最突出的是预言机依赖问题。私募公司的估值数据本身不透明且更新频率低。基于此类不完整信息的衍生品可能加剧市场的信息不对称。

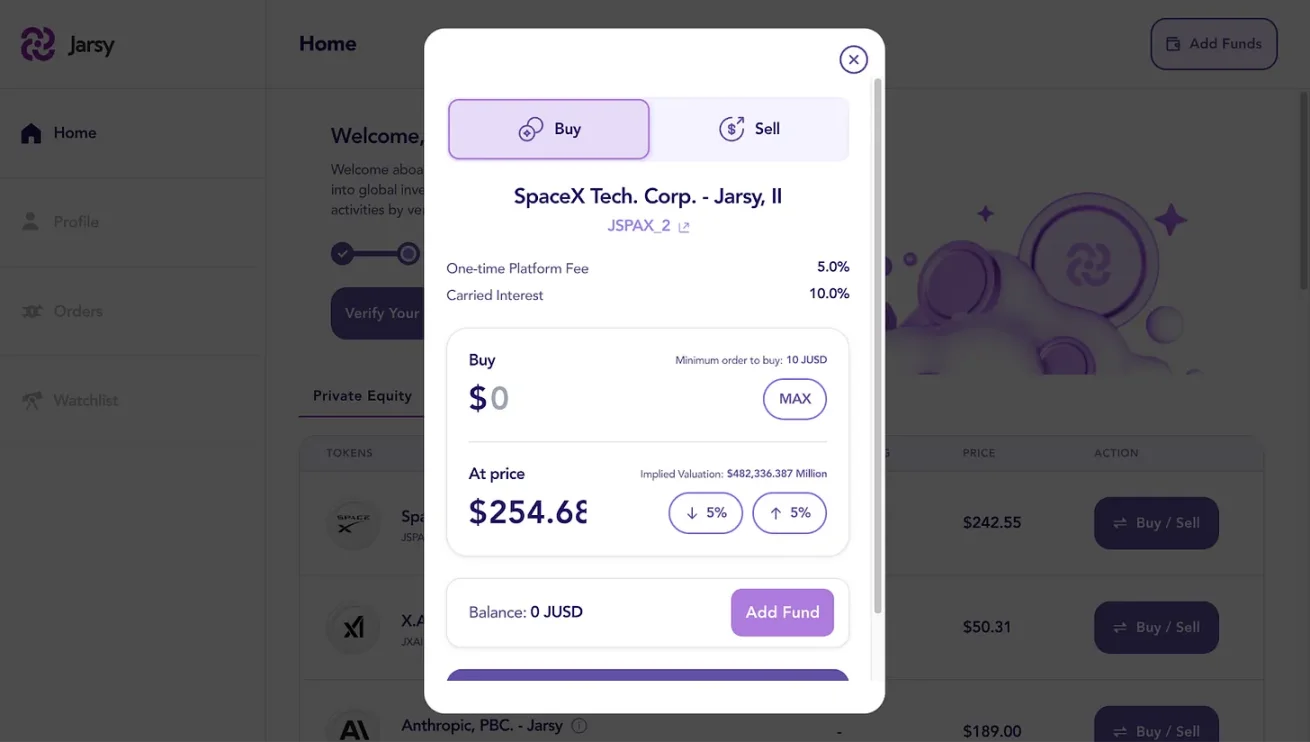

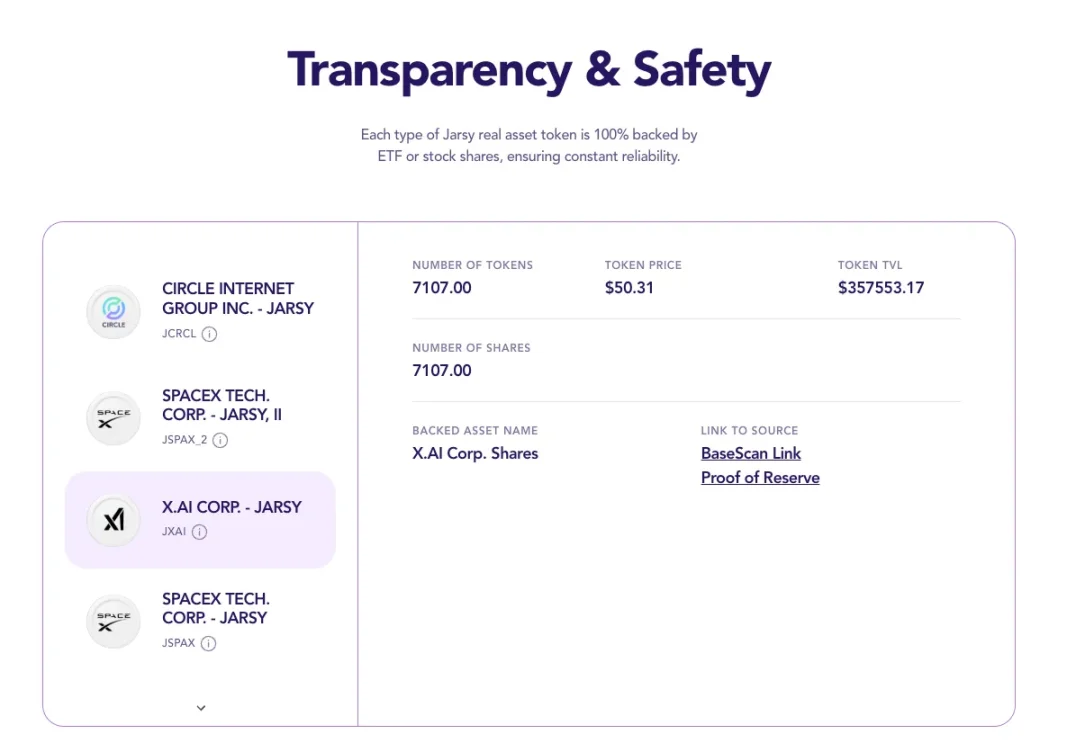

Jarsy

资料来源:Jarsy

Jarsy 采用 1:1 资产背书的代币化模型。其核心机制是直接收购 Pre-IPO 股票,并为每持有一股发行一枚代币。例如,如果 Jarsy 持有 1000 股 SpaceX 股票,它将铸造 1000 枚 JSPAX 代币。尽管投资者不直接持有标的股票,但他们享有所有相关的经济权利,包括股息和股价增值。

资料来源:Jarsy

这一模式依赖于 Jarsy 作为资产管理实体的角色。平台首先通过预售代币测试投资者需求,然后利用募集的资金购买实际股票。如果购买成功,预售代币将转换为正式代币;否则,资金将被退还。所有资产由特殊目的载体(SPV)持有,并通过储备证明页面提供实时验证。

该平台还大幅降低了投资门槛,最低投资额仅为 10 美元。对于美国以外的投资者,没有资质要求,从而扩大了全球准入性。所有交易记录和资产持有情况均存储在链上,确保了可审计性和透明度。

然而该模式存在结构性限制。最紧迫的问题是流动性,这源于平台对每家公司的资产持有规模有限。例如,Jarsy 目前持有的 X.AI、Circle 和 SpaceX 股票总值分别约为 35 万美元、49 万美元和 67 万美元。在这种低流动性市场中,即使是大型持有者的少量卖单也可能引发显著的价格波动。由于私募股权本身不透明且流动性差,价格发现尤为困难,进一步放大了波动性。

此外尽管资产背书模式提供了稳定性,但它限制了可扩展性。每个新代币的发行都需要实际购买股票,这一过程涉及谈判、监管协调和潜在的采购延迟,从而阻碍了平台对快速变化的市场趋势作出反应。

尽管如此 Jarsy 仍处于早期阶段,上线仅一年多。随着用户基础和资产管理规模(AUM)的增长,流动性问题可能会逐渐缓解。随着平台的扩展,更广泛的覆盖面和更深的代币化股权池可能自然形成更稳定、更高效的市场。

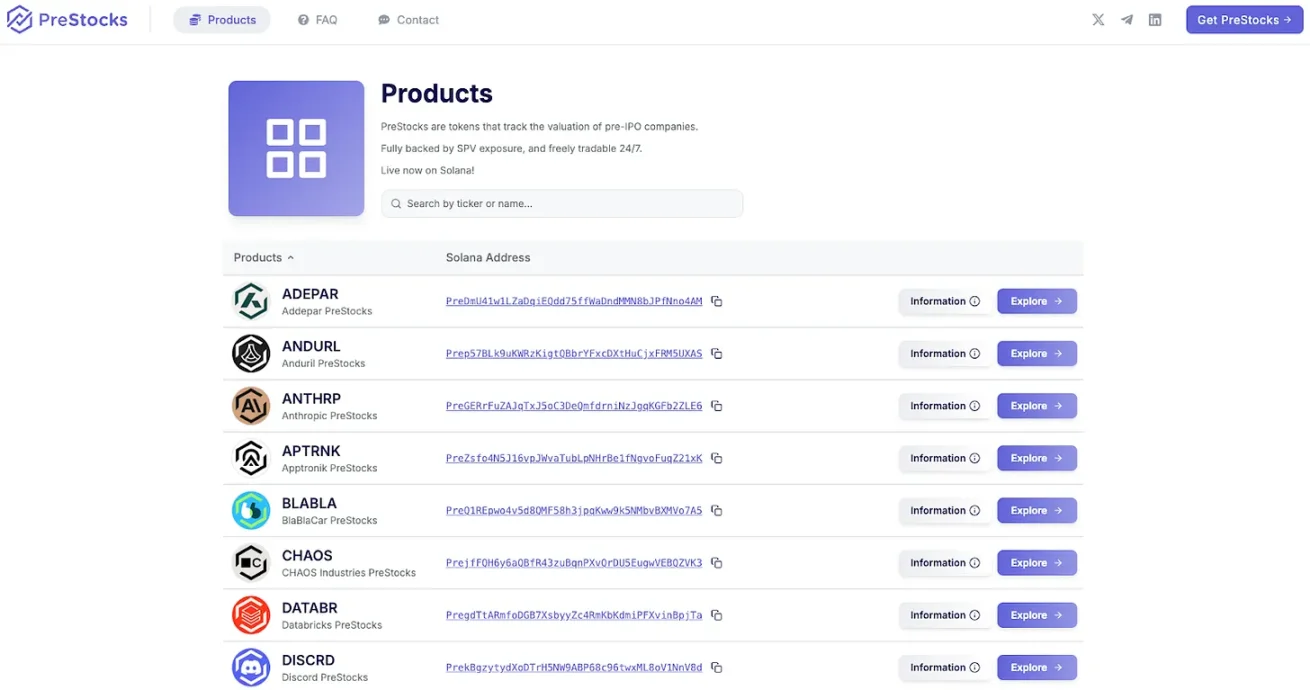

PreStocks

资料来源:PreStock

PreStocks 采用与 Jarsy 类似的模型,购买私募公司股票并按 1:1 比例发行背书的代币。该平台目前支持 22 种 Pre-IPO 股票的交易,并已向公众开放产品。

PreStocks 基于 Solana 区块链构建,通过与 Jupiter 和 Meteora 的集成实现交易。它提供全天候交易和即时结算,不收取管理费。没有最低投资要求,任何拥有 Solana 兼容钱包的人都可以参与,进一步降低了准入门槛。

然而该平台也存在一些限制,美国和其他主要司法管辖区的用户无法访问。尽管所有代币据称均由标的股票全额抵押,但 PreStocks 尚未公开详细的持仓验证文件。团队表示将定期发布外部审计报告,并可根据要求提供付费的个别验证服务。

与 Jarsy 相比,PreStocks 与去中心化交易所(DEX)的集成更紧密,这可能为代币借贷等更广泛的二级用例提供支持。在 Solana 生态系统中,代币化公开股票(如 xStock)已经活跃使用,PreStocks 可能会受益于生态系统层面的协同效应。

Pre-IPO 股票代币化尚未解决的障碍

代币化股票市场正在初步形成。尽管 Ventuals、Jarsy 和 PreStocks 等平台显示出早期发展势头,但重大结构性挑战仍然存在。

首先,监管不确定性是最根本的障碍。大多数司法管辖区仍缺乏针对代币化证券的明确法律框架。因此许多平台在监管灰色地带运作,利用司法套利活跃,而无需直接合规。

其次,私募公司的抵制仍是关键障碍。2025 年 6 月,Robinhood 宣布为欧盟客户推出一项新服务,提供对 OpenAI 和 SpaceX 等公司的代币化投资敞口。OpenAI 立即公开反对,声明称:“这些代币不代表 OpenAI 的股权,我们与 Robinhood 没有合作关系。”这一回应凸显了私募公司不愿放弃对股权结构和投资者管理的控制权,这是它们严密守护的核心功能。

第三,技术和运营的复杂性不容忽视。维持现实世界资产与代币之间的可靠联系、处理跨境合规问题、应对税务影响以及实现股东权利执行,都是非平凡的挑战。这些问题可能严重限制用户体验和可扩展性。

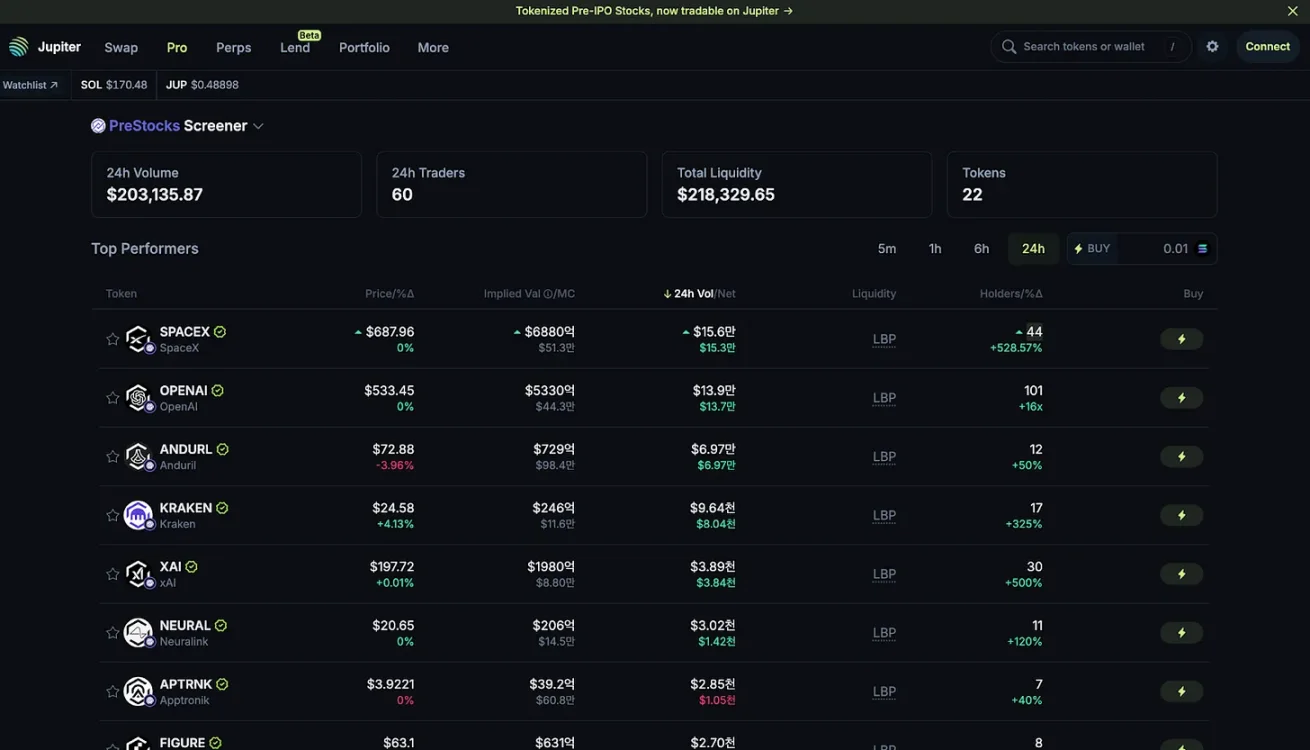

尽管存在这些限制,市场参与者仍在积极寻求解决方案。例如 Robinhood 表示计划在年底前将其代币产品扩展到数千种资产,尽管在公开市场面临重重挑战。Ventuals、Jarsy 和 PreStocks 等平台也通过差异化代币化股权准入方式持续推进。

简而言之,代币化为改善私募股权市场的准入性提供了一条有希望的路径,但这一领域仍处于起步阶段。当前的限制是现实存在的,但加密领域的历史表明,技术突破和快速的市场适应能够,而且常常会重新定义可能性。