Автор: Memento Research

Перевод: Deep Tide TechFlow

Резюме Deep Tide: Данные о криптофинансировании за первые 4 месяца 2026 года раскрывают суровую реальность: потоки финансирования в сферах игр и DePIN практически иссякли, в то время как две компании, занимающиеся прогнозирующими рынками, Kalshi и Polymarket, привлекли больше денег, чем все проекты DeFi за год вместе взятые. Что ещё более настораживает, количество сделок по слияниям и поглощениям сравнялось с количеством раундов seed-финансирования, что означает, что капитал перетекает от финансирования новых идей к приобретению существующих лидеров рынка.

Обзор финансирования: взрыв в марте — всего лишь иллюзия

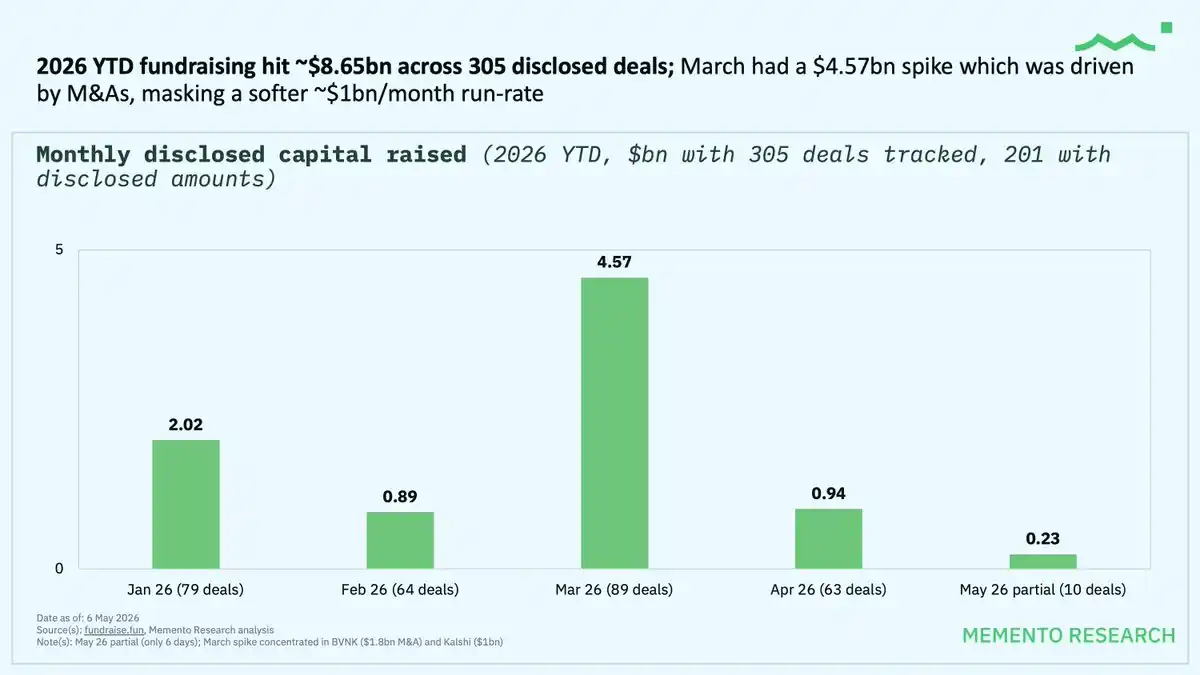

С 1 января по 6 мая 2026 года в криптоиндустрии было завершено 305 сделок по привлечению финансирования на общую сумму 8,65 миллиарда долларов США. Однако "взрыв" в марте на 4,57 миллиарда долларов на самом деле был результатом всего двух сверхкрупных сделок по слияниям и поглощениям: BVNK — 1,8 миллиарда долларов и Kalshi — 1 миллиард долларов.

Если исключить эти две сделки, реальный темп привлечения финансирования составляет около 1 миллиарда долларов в месяц, что ещё слабее, чем в конце 2025 года.

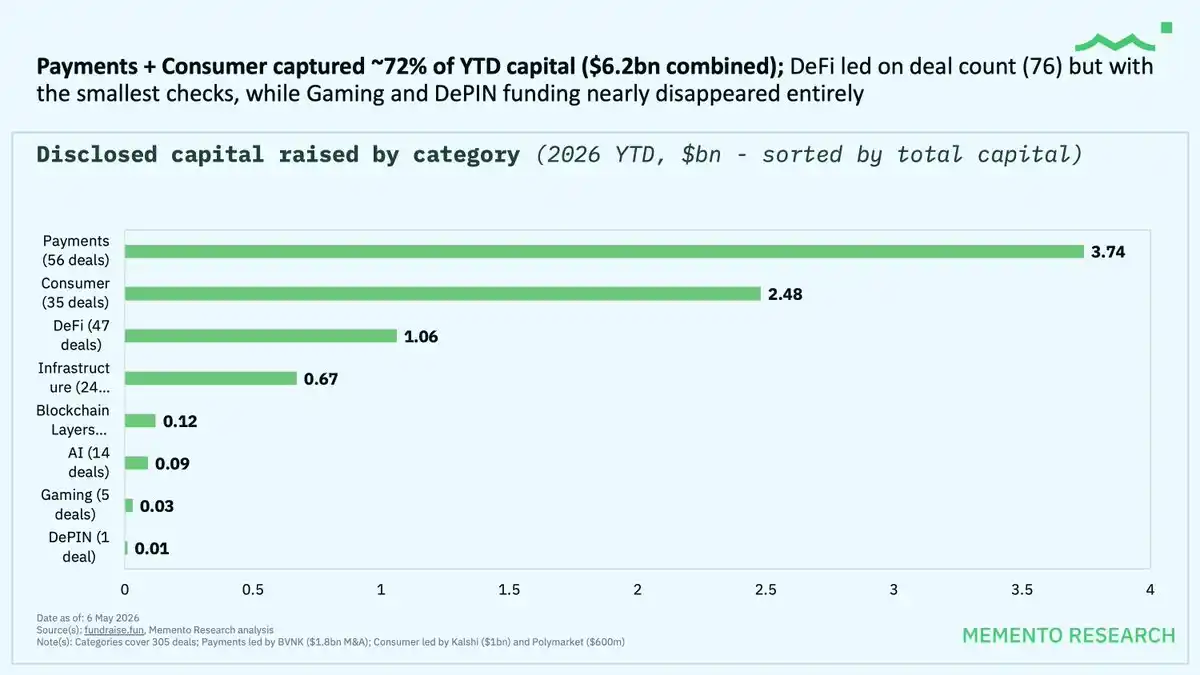

Потоки капитала: платежи и потребление поглотили 72%

Распределение по секторам:

Платежи: 3,74 млрд долларов (56 сделок)

Потребительский сектор: 2,48 млрд долларов (35 сделок)

DeFi: 1,06 млрд долларов (47 сделок, наибольшее количество транзакций)

Два сектора — платежи и потребительский сектор — вместе составили 72% годового финансирования. Финансирование в сферах игр и DePIN практически исчезло.

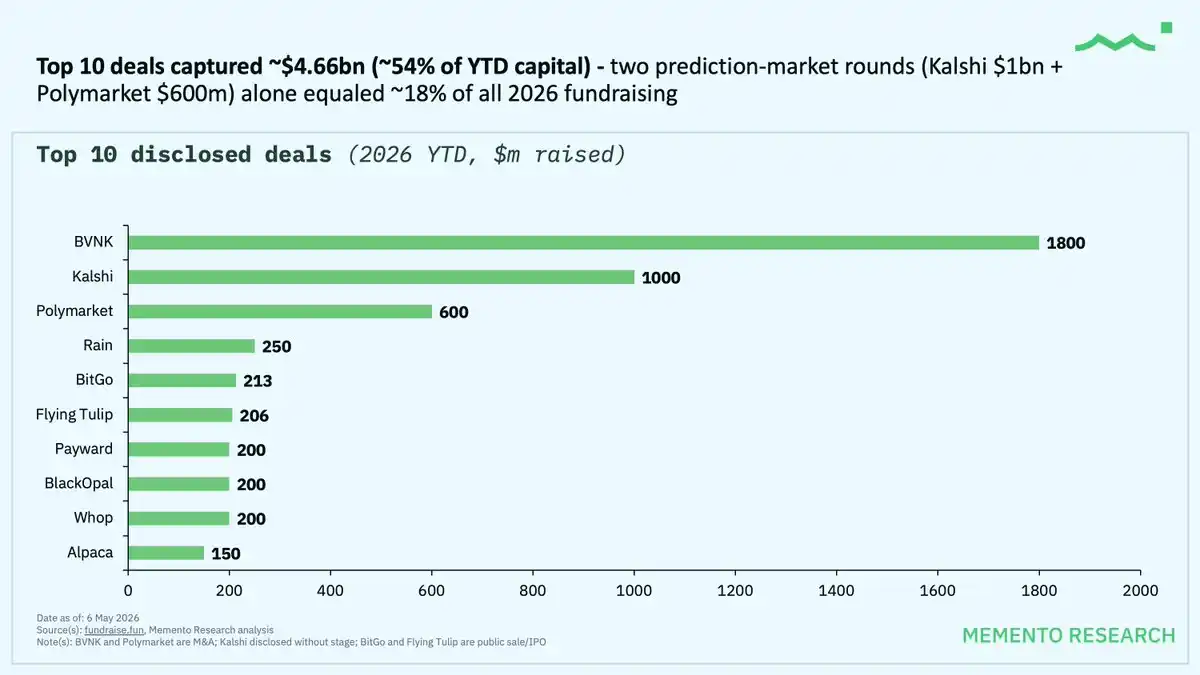

Господство прогнозирующих рынков в потребительском секторе

Две компании, занимающиеся прогнозирующими рынками, привлекли 18% годового финансирования:

Kalshi: 1 миллиард долларов

Polymarket: 600 миллионов долларов

Эти две сделки на общую сумму 1,6 миллиарда долларов превысили сумму всех 47 сделок по финансированию DeFi.

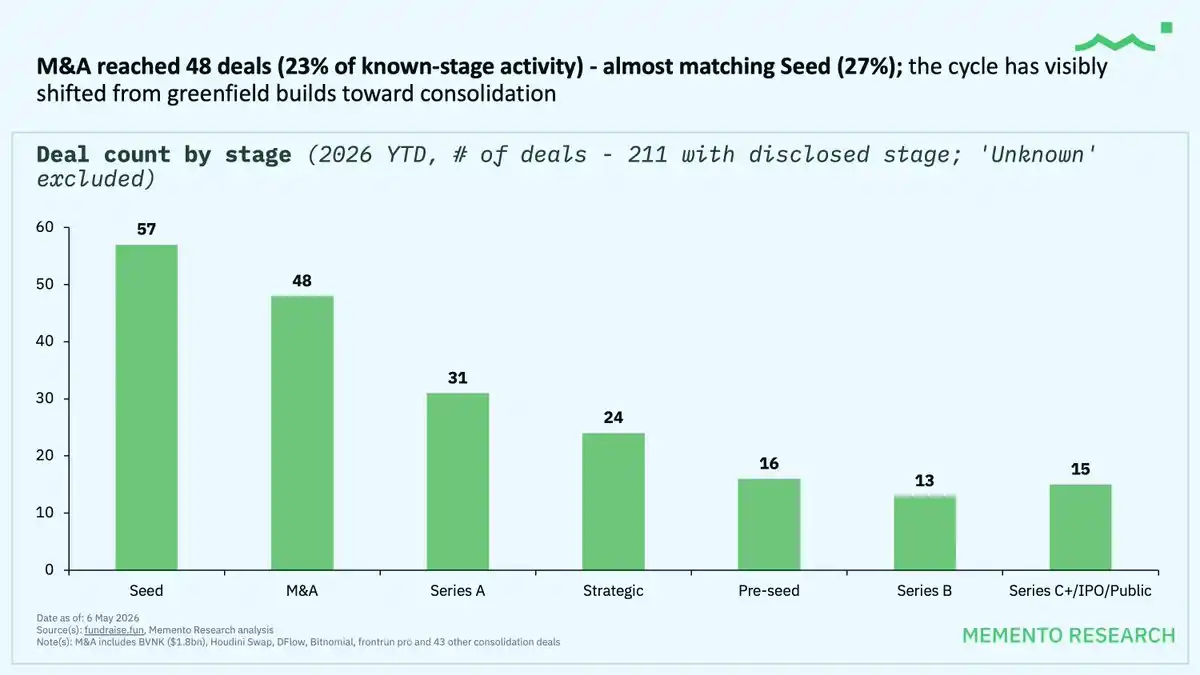

Слияния и поглощения становятся основным трендом

Количество сделок по слияниям и поглощениям достигло 48 (23% от известных сделок на определённой стадии), что почти сравнялось с 57 сделками seed-раундов (27%). Этот цикл перешёл от инвестиций в новые идеи на ранней стадии к приобретению лидеров отрасли.

Перестановки в рейтинге инвестиционных институтов

Самые активные фонды в 2026 году:

Coinbase Ventures: 18 сделок (2-е место в период 2021-26 гг.)

Tether: 13 сделок (новый лидер по числу лид-инвестиций)

Animoca Brands: 11 сделок (1-е место в период 2021-26 гг.)

GSR: 11 сделок

a16z: 7 сделок (значительное снижение по сравнению с примерно 200 сделками в период 2021-26 гг.)