比特币 ( BTC ) 的价格小幅下跌至 28,500 美元以下,此前美国央行采取了普遍预期的行动并将利率提高 25 个基点 (bps) 。此次上调将联邦基金利率上调至 5% 至 5.25% 的目标区间。

根据 CoinDesk 数据,按市值计算最大的加密货币最近交易价格约为 28,350 美元,在过去 24 小时内下跌了约一个百分点。

美联储周三的决定标志着 14 个月内第 10 次加息。美联储联邦公开市场委员会 (FOMC) 在加息声明中表示,“家庭和企业信贷条件收紧可能会对经济活动、就业和通胀造成压力”,并将密切关注通胀风险.

在宣布利率后的新闻发布会上,美联储主席杰罗姆鲍威尔表示,尽管价格“自去年年中以来有所缓和......通胀压力继续居高不下,并且将通胀率回落至 2% 的过程有一个任重而道远。”

鲍威尔还表示,暂停加息的决定“不是今天做出的”,不过他指出,当前的声明并不像之前的声明那样暗示进一步加息。他说:“对进一步收紧政策的适当程度的评估将是一个持续的会议,一次又一次地召开会议,”他指出信贷状况的不确定性。

鲍威尔补充说:“我们可能会遇到我希望的温和衰退。”

CME FedWatch Tool显示,目前超过 93% 的交易员认为美联储将在 6 月的政策会议上暂停加息计划。

按市值计算的第二大加密货币以太币 ( ETH ) 最近上涨约 0.3%,徘徊在 1,878 美元左右。衡量加密市场整体表现的CoinDesk 市场指数(CMI) 当天下跌 1%。

加密交易公司 Dexterity Capital 的执行合伙人迈克尔萨法伊在给 CoinDesk 的一封电子邮件中表示,美联储的最新决定可能会给加密交易员带来“喜忧参半的结果”。 “虽然关于未来加息的措辞有所软化,但美联储表示未来的决定将取决于宏观数据,因此敞开了大门。通货膨胀数据正在改善,但仍不足以激发加密货币交易者的乐观情绪,”Safai 在一封电子邮件评论中表示。

“加密货币现在很安静,这意味着前 10 大代币的退出速度不足以打破宏观相关性,”他补充道。 “比特币和以太坊更有可能在区间波动,直到我们看到通货膨胀走向的线索。如果经济复苏步伐缓慢,市场可能会度过一个缓慢的夏季。”

加密分析公司 Amberdata 的衍生品主管 Greg Magadini 在美联储决定之前的一封电子邮件中指出,在美联储 6 月中旬的下次会议之前,将有两个消费者价格指数 (CPI) 通胀数据,这意味着有可能加息仍然摆在桌面上。

Magadini 表示,今年BTC一直受到宏观事件的推动,周三的加息已经反映在价格中。

股市周三收盘下跌,标准普尔 500 指数小幅下跌 0.7%。道琼斯工业平均指数 (DJIA) 和以科技股为主的纳斯达克综合指数分别下跌 0.8% 和 0.4%。

债券市场方面,2 年期国债收益率近期下跌 12 个基点至 3.86%,而 10 年期国债收益率下跌 7 个基点至 3.35%。

加密货币投资者一直在努力了解近期银行倒闭和加密货币监管争端对市场的潜在影响。

外汇做市商 Oanda 的高级市场分析师爱德华莫亚在周三的一份报告中写道:“比特币仍处于锚定状态,不太可能反弹至 30,000 美元上方,直到美国获得一些监管明确性。”

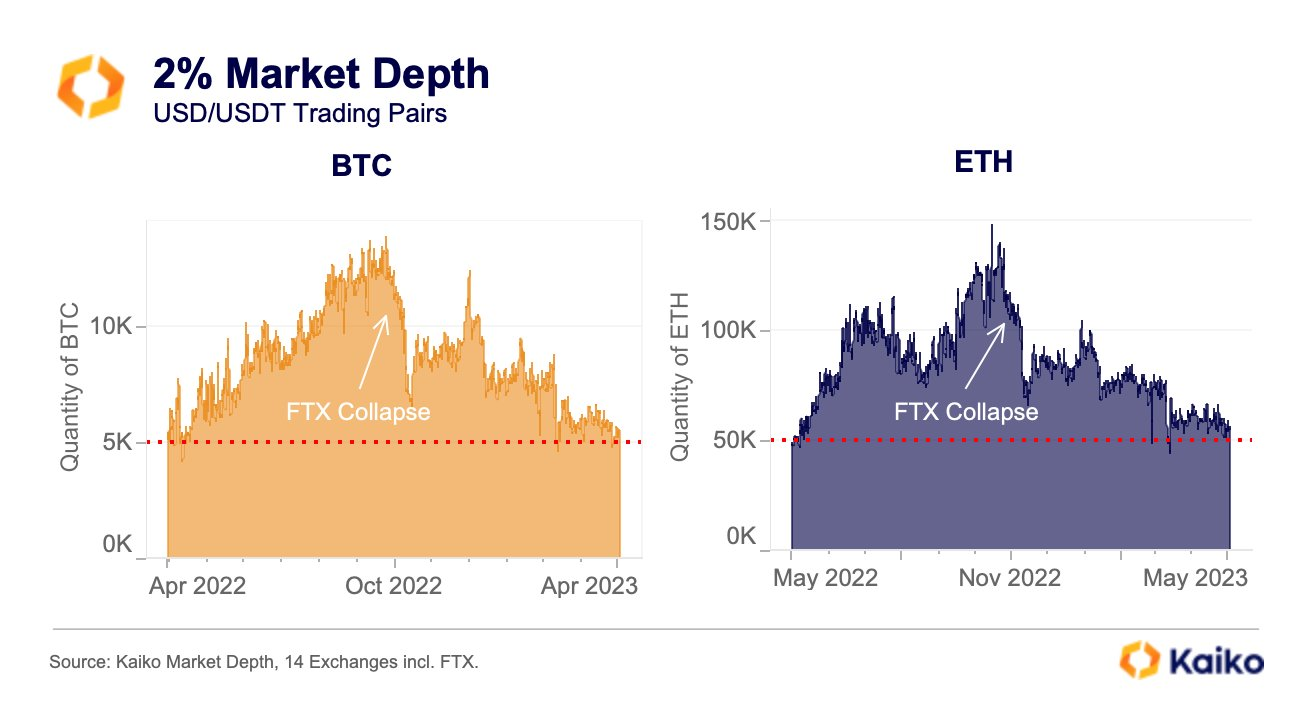

与此同时,加密数据公司 Kaiko 的图表显示, BTC和 ETH 的 2% 市场深度(评估流动性状况的指标)已接近一年低点。

BTC和ETH的2%市场深度(Kaiko)

Kaiko 的研究分析师 Dessislava Ianeva 向 CoinDesk 指出,尽管今年比特币的价格上涨了 70% 以上,但集中交易所的交易量低于去年同期。她表示,成交量低的部分原因是“更大的宏观和监管不确定性”。

Ianeva 表示:“做市商仍对增加流动性持谨慎态度,并且可能已经修改了他们的风险管理策略。”他补充说,去年 11 月交易所 FTX 及其交易部门 Alameda Research 倒闭后出现的流动性缺口“证明是持续存在的。 ”

“流动性有望及时恢复,临界质量将建立在数字资产领域的新领域,但在这种情况发生之前——或者一个主要头条新闻加强或挑战加密货币的吸引力——比特币将继续追踪更广泛的市场,”Dexterity Capital 的 Safai 说.