Author:Ash

Compiled by: Deep Tide TechFlow

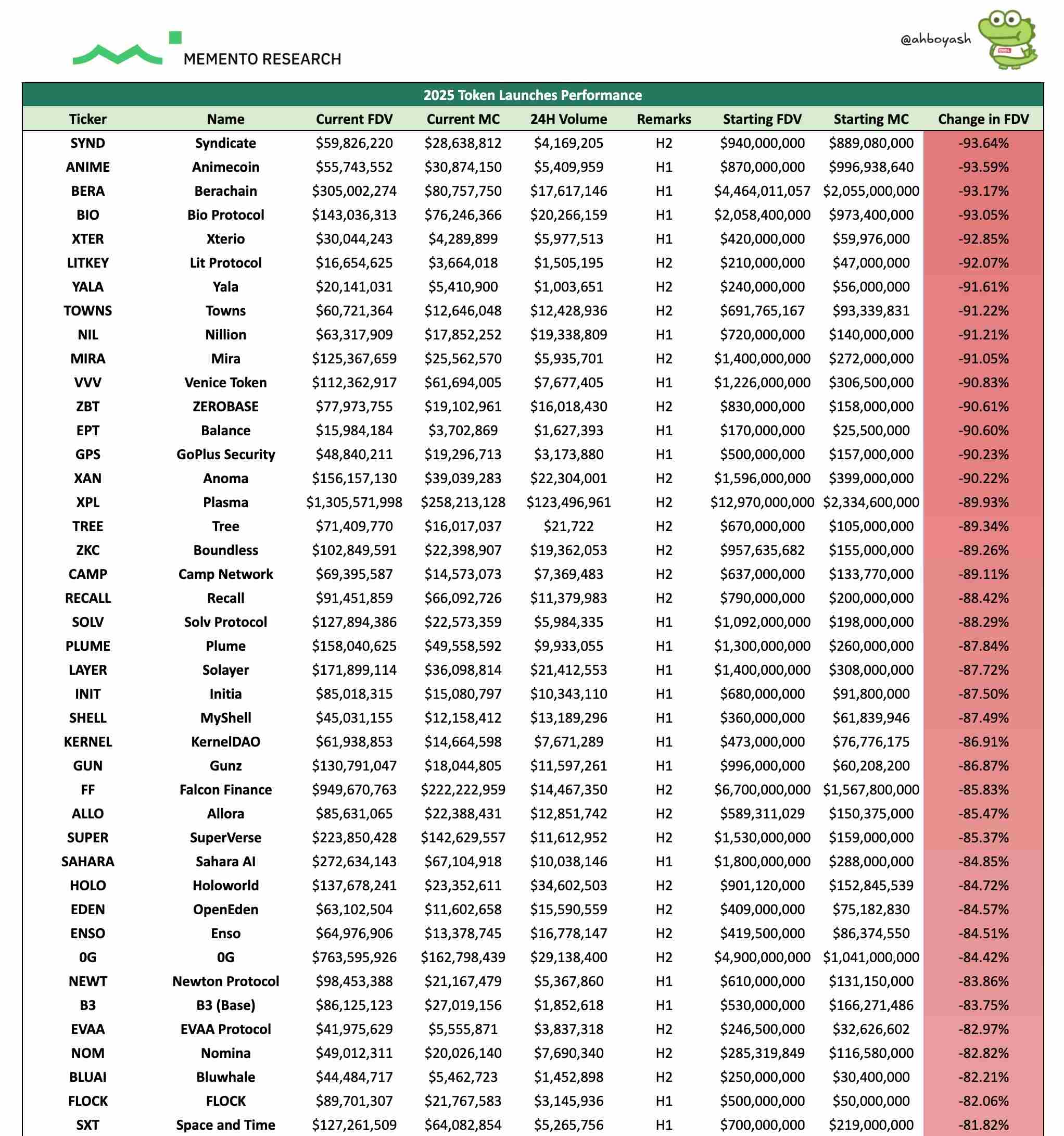

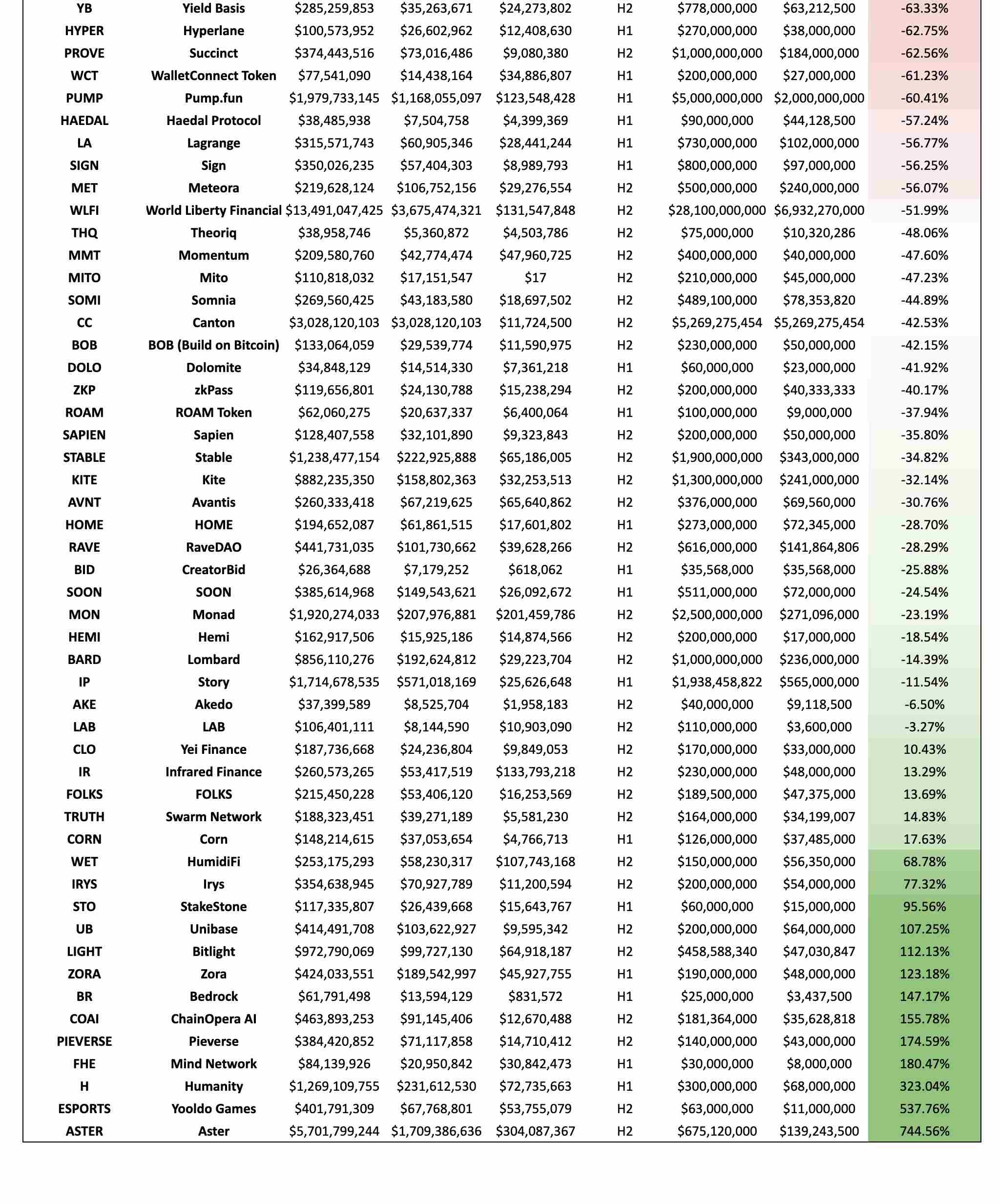

We tracked 118 Token Generation Events (TGEs) launched in 2025 and compared their current fully diluted valuation (FDV) with their valuation at issuance. The results are as follows:

-

84.7% (100 out of 118) currently have a valuation lower than at TGE;

-

This means approximately 4 out of every 5 newly issued tokens are valued below their issuance level;

-

The median token's fully diluted valuation (FDV) has fallen by 71% since issuance (market cap down 67%);

-

Only 15% of tokens remained "green" (i.e., above issuance valuation) after TGE.

Nowadays, participating in a TGE can hardly be considered "early investment" anymore. How lamentable.

View the complete data via the link