Author: Connor King, Founder of Novora

Compiled by: Hu Tao, ChainCatcher

Last month, we released our "Does Investor Relations Matter in Crypto?" This is the follow-up. We expanded the initial dataset of 53 protocols to over 150 protocols, covering all major sectors: DEX, lending, perpetuals, liquid staking, L1, L2, bridges, DePIN, AI, stablecoins, infrastructure, and CEX tokens. The fully diluted valuation (FDV) of the protocols ranges from $40 million to $45 billion.

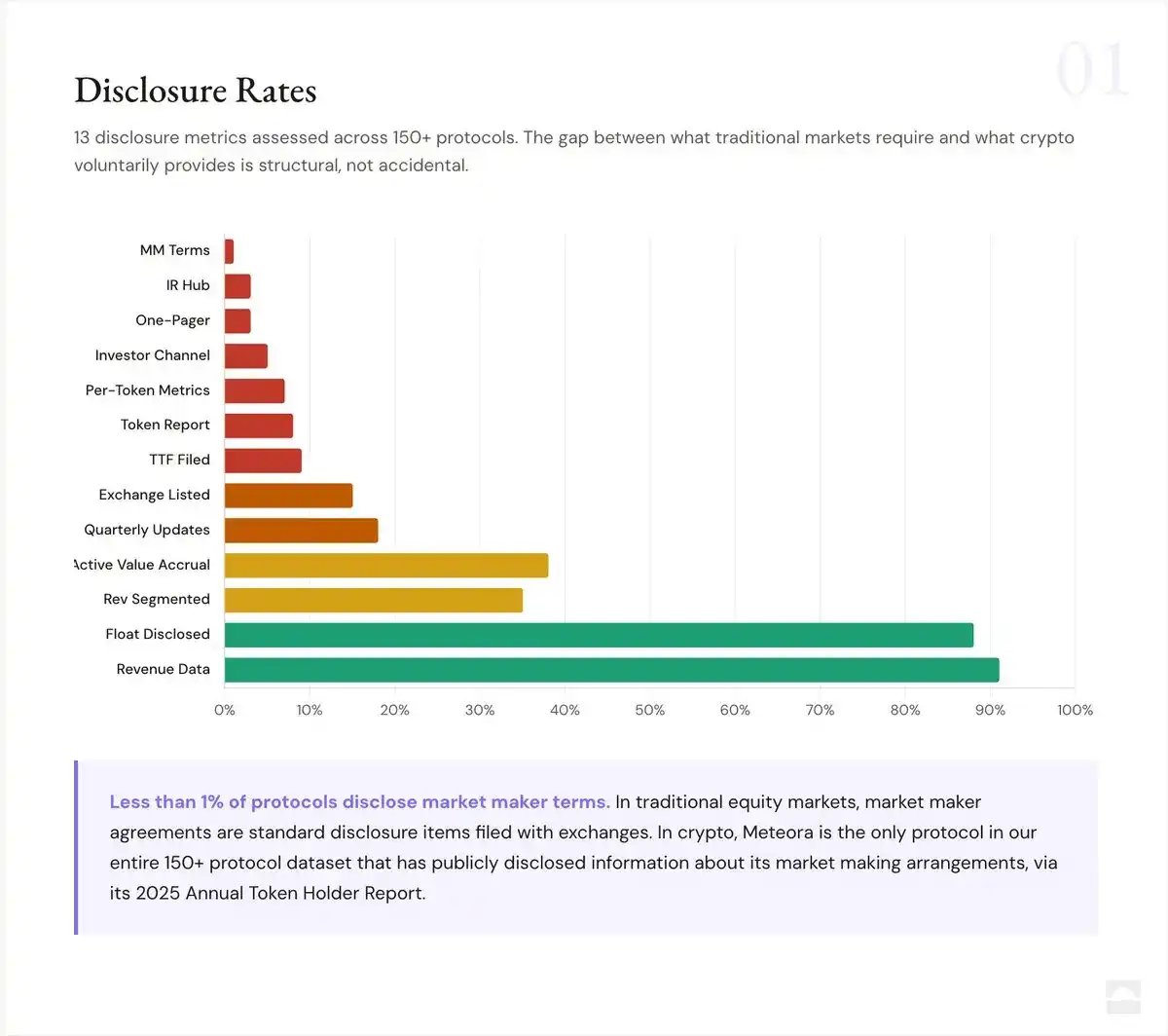

We checked 15 binary, verifiable indicators for each protocol: Does the protocol disclose this information? Yes/No. Each data point was cross-verified through public sources: Artemis, Tokenterminal, Blockworks, Dune, DefiLlama.

Here's what we found:

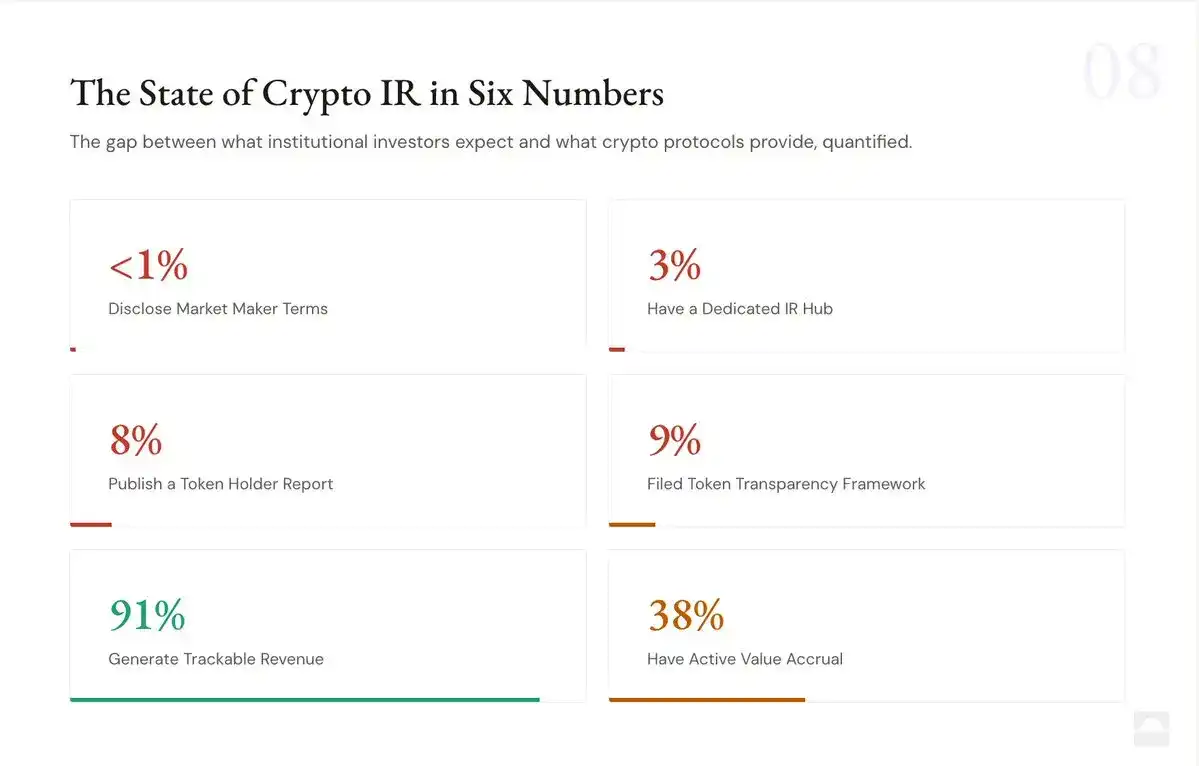

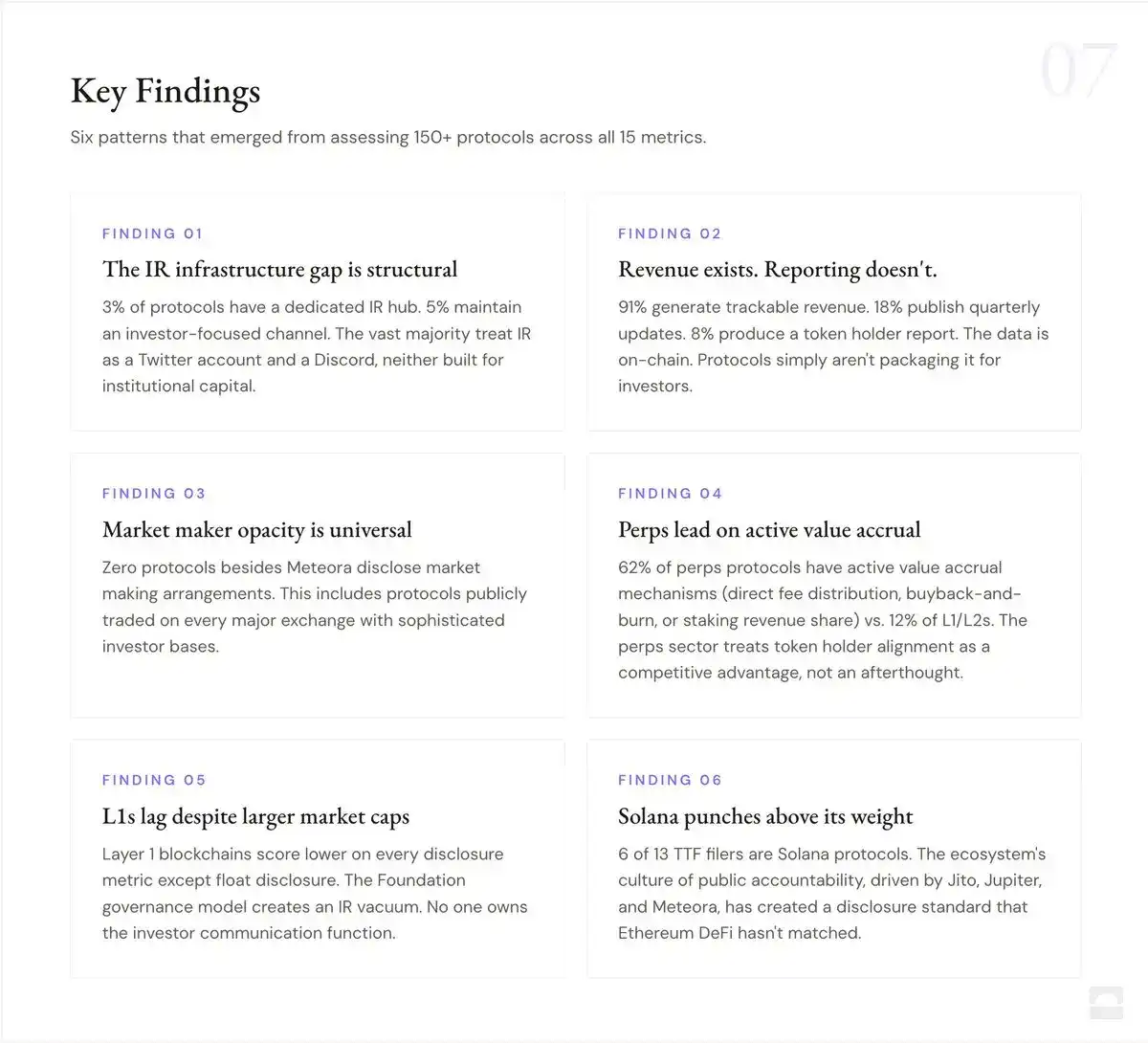

Less than 1% of market makers disclose their market maker terms.

50 protocols. Billions in daily trading volume combined. But only one protocol publicly disclosed information about its market making arrangements.

Market makers set the terms for token trading. These agreements often include token lending, option structures, and performance incentives that directly impact price discovery. In traditional markets, such material agreements are disclosed. But in crypto, every market participant is trading in the dark.

Meteora was the only protocol in the dataset that disclosed its market making arrangements through its 2025 Token Holder Annual Report. One out of over 150.

This is the most impactful transparency gap in the industry.

91% have revenue data. 3% have an Investor Relations hub.

Nearly every protocol in this audit publicly provides revenue data, either through third-party platforms or their own data dashboards. The raw data exists.

But only 3% have built a dedicated Investor Relations hub that consolidates this data into an investor-facing experience. The exceptions include Meteora, Jito, Jupiter, Raydium, MetaDAO. Every other protocol scatters information across blogs, governance forums, X threads, and third-party platforms. There is no centralized, institutional-grade investor experience. The gap isn't data availability, it's communication infrastructure.

9% submitted the Blockworks TTF

The Blockworks Token Transparency Framework was submitted to the U.S. SEC in June 2025, covering 18 disclosure standards across supply, distribution, financials, and market structure, backed by Pantera, L1D, and Theia. Out of the 150+ protocols reviewed, only 13 submitted the framework: Jito, Jupiter, Raydium, Morpho, Aerodrome, MetaDAO, Maple, dYdX, Euler, Marinade, EtherFi, Gains Network, and Meteora.

This is a material improvement from zero submissions. But the submission rate dropped from 25% in the initial 53 protocols to 9% at 150+. The original dataset was skewed towards early TTF-adopting DeFi protocols. With a broader sample, the picture is clearer: the vast majority of the market is not opting in. Zero L1s, zero L2s, zero infrastructure protocols submitted the framework. The framework exists. More protocols should use it.

38% have active value accrual, 62% return nothing

We used a broad definition of "active value accrual": Does the protocol have at least one live mechanism that directs economic value directly to token holders (excluding governance rights)? Across 150+ protocols, we identified six distinct models:

- Direct fee sharing (JUP, DYDX, GMX)

- Buyback and burn (HYPE, RAY, MET)

- Staking revenue share (PENDLE, AAVE, ETHFI)

- Conditional buybacks (LDO)

- ve-model epoch distribution (AERO)

- Governance-only, no economic rights (MORPHO, LINK, ARB)

62% of protocols fall into the last category – governance-only tokens with no value accrual, including some of the largest market cap projects in the industry. Sector differences are stark: 62% of Perpetuals protocols have active value accrual, versus just 12% of L1/L2 tokens. Perpetuals treat token holder alignment as a competitive advantage. L1 foundations have not yet done the same. A deep dive into which models actually work is coming next week.

The data layer is built, the communication layer is not

We checked five major third-party platforms: Token Terminal, Dune Analytics, Artemis, DefiLlama, and Blockworks Research. The first four platforms each cover 85-95% of the dataset. 72% of protocols appear on 4 or more platforms. Every protocol in the audit appears on at least one platform. The raw data infrastructure for institutional analysis is largely built. What's missing is the interpretation, packaging, and communication layer that turns data into investable narratives.

The full disclosure breakdown for 150+ protocols is as follows:

<1% —— Disclose Market Maker Terms

3% —— Dedicated IR Hub

3% —— Provide a One-Pager

5% —— Dedicated Investor Channel

7% —— Publish Single-Token Metrics

8% —— Token Holder Reports

9% —— Submitted TTF

15% —— Disclose Exchange Listings

18% —— Quarterly Updates

35% —— Disaggregated Revenue Disclosure

38% —— Active Value Accrual

88% —— Disclose Circulating Supply

91% —— Revenue Data Available

What this means

The thesis from "Does Investor Relations Matter in Crypto?" holds. The data is even more sobering with the sample size expanded to 150+. Crypto protocols aren't hiding the fundamentals, they're failing to present them. The raw inputs for fundamental analysis exist on-chain and on third-party platforms, but the "translation layer and IR infrastructure that turns data into institutional confidence barely exists. Only 3% have an IR hub, <1% disclose market maker terms, and 91% of the market has not adopted the only available standardized disclosure framework.

The opportunity for protocols is clear: the cost of building IR infrastructure is negligible relative to capital markets upside. Protocols investing in this now will be the first to earn the trust of institutional allocators. The full interactive report with all 150+ protocols is live now:

http://novora.co/research/ir-transparency-2026.html

Next week, we will release the comparative report for this series: "Which Token Value Accrual Model Works?". That report will break down the six token value accrual mechanisms we identified, their empirical performance, and what this means for token classification and institutional adoption.