Written by: Oluwapelumi Adejumo

Compiled by: Saoirse, Foresight News

Key Points at a Glance

- BitMine plans to issue 3 million perpetual Class A preferred shares to raise up to $300 million for Ethereum position deployment.

- The 9.5% annualized dividend will provide the company with new funds for token purchases and staking node expansion, but will also incur approximately $28.5 million in annual new dividend costs.

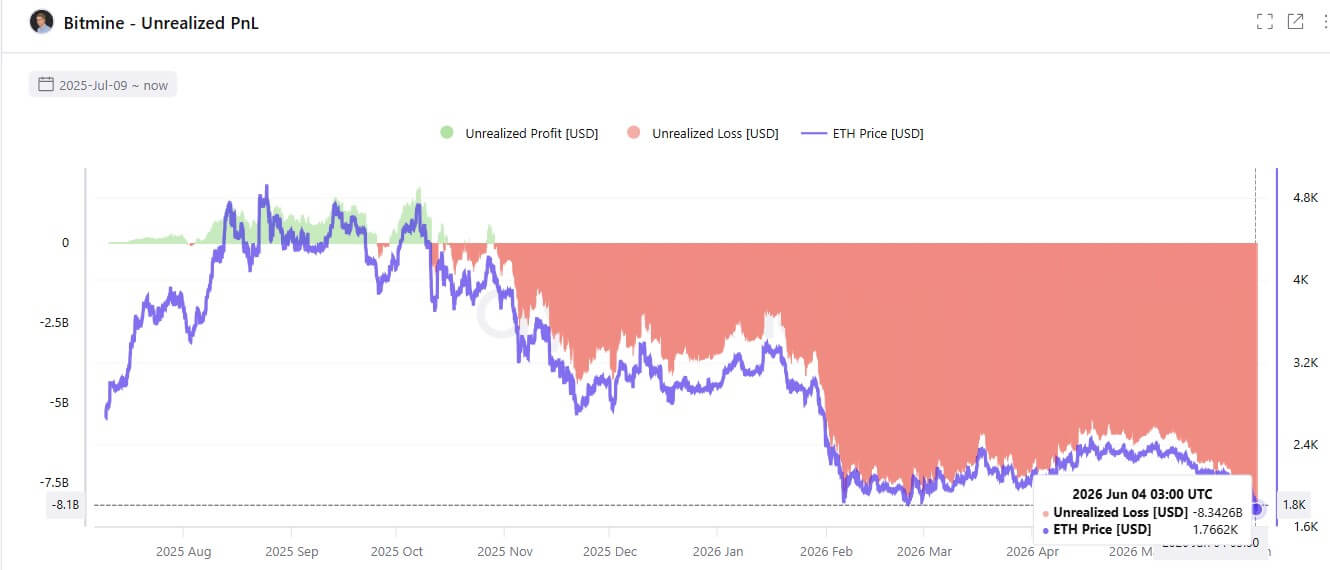

- The company's unrealized loss on its Ethereum holdings exceeds $8.5 billion; if staking yields fall short of expectations, dividend payments may rely on internal cash, asset sales, or subsequent refinancing.

Led by Thomas Lee, BitMine intends to raise funds through the preferred stock market, leveraging a fixed 9.5% annualized dividend to attract capital for increasing its Ethereum exposure. The company disclosed the plan on June 3rd: issuing 3 million Class A perpetual preferred shares with a face value of $100 and a fixed annual dividend of 9.5%, aiming to raise up to $300 million. Once approved, the securities will be listed on the New York Stock Exchange under the ticker BMNP, with Moelis & Company and Cantor acting as joint book-running managers.

If all shares are sold, the company's annual dividend obligation will increase by $28.5 million, payable weekly following board approval. This fundraising comes at a time when this heavily Ethereum-weighted company faces a severe test for its business model: dragged down by persistently low token prices, Ethereum's market price is far below the company's average cost basis, with BitMine's unrealized losses on related holdings exceeding $8.5 billion.

Unrealized Loss on Ethereum Assets Held by BitMine (Data Source: CryptoQuant)

This financing will further tie the company's balance sheet, staking operations, and public market investors, helping the company continue accumulating Ethereum at low prices.

Relying on Ethereum Staking Yields to Support the Dividend Logic

BitMine stated that the proceeds can be used for general corporate purposes: increasing holdings of Ethereum and other digital assets, expanding staking validator nodes, supplementing operational working capital, making strategic investments in the Ethereum ecosystem, and repurchasing its own common stock. This fundraising is not only for patching up book losses but also aids the company in continuously accumulating tokens during the bear market, solidifying its position as a leading publicly listed Ethereum treasury company globally.

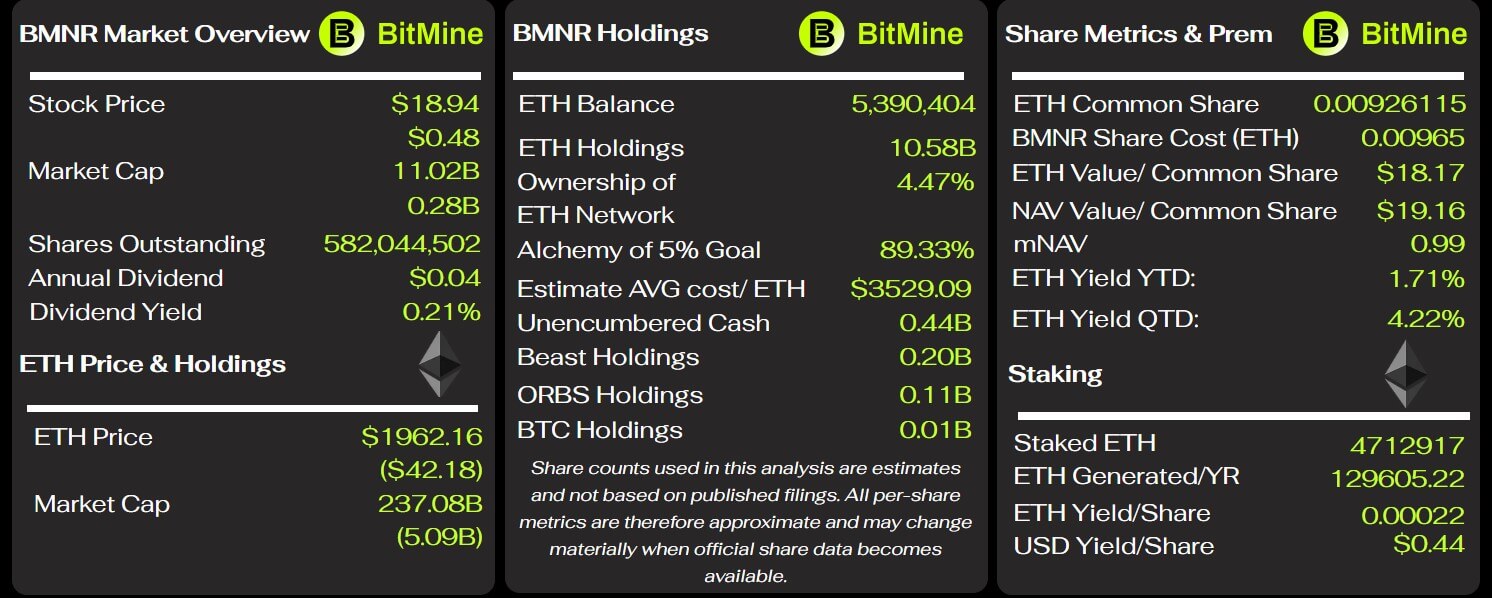

Over the past year, the company has consistently made large-scale purchases of Ethereum, currently holding over 5.3 million tokens, accounting for approximately 4.5% of Ethereum's circulating supply; the vast majority of these holdings are in a staked state, continuously earning on-chain block rewards.

BitMine Key Metrics (Data Source: BitMineTracker)

Chairman Thomas Lee posited that yield generation through staking is the core advantage of Ethereum treasury companies compared to Bitcoin-heavy counterparts. Bitcoin cannot generate passive income, but Ethereum can continuously profit through staking, allowing holders to obtain cash flow without selling the principal. This income logic forms the fundamental support for this preferred share issuance: with the full $300 million raised, weekly dividend expenses amount to approximately $548,000. BitMine disclosed its annualized staking yield reaches hundreds of millions of dollars; under normal market conditions, the dividend cost is far lower than the income generated from staking.

Research by staking service provider Everstake shows: in 2025, among all publicly listed Ethereum treasury companies in the industry, staking income accounted for 60% of total disclosed revenue, indicating that monetizing staking has become the mainstream profit model in the sector. Industry data corroborates that BitMine's business model of using Ethereum-generated yield to cover fixed dividends shares common industry characteristics.

The company is not merely hoarding and locking tokens but is transforming its massive Ethereum reserves into sustainable cash flow to access capital market financing. However, as seen in the offering documents, this model is not without risks.

BitMine has not established a dedicated staking yield fund pool for preferred share dividends. The document states that dividend payments may be sourced from the company's internal cash, staking profits, sales of held securities, subsequent refinancing, or other channels. The company also warns of extreme market risks: staked Ethereum cannot be instantly redeemed and liquidated during market stress periods, and staking yields may fall short of expectations. Essentially, the preferred share issuance converts BitMine's Ethereum investment position into a rigid, regular cash payment obligation.

Benchmarked Against the Strategy Model, but Product Terms Show Significant Differences

BitMine's financing approach is benchmarked against Michael Saylor's Bitcoin-heavy Strategy: both companies rely on issuing listed preferred shares to raise funds, using public market capital to continuously accumulate tokens and optimize capital structure; by creating income-generating securities, they allow ordinary investors to gain exposure to the crypto treasury sector without directly holding the tokens. Both face the market risk of severe underlying asset price volatility and the rigid payment obligation of fixed dividends.

However, the rules of the two preferred share products differ markedly: Strategy's issued STRC preferred shares are floating-rate products, with dividends adjusted monthly to stabilize the share price close to the $100 face value; BitMine's Class A preferred shares feature a fixed 9.5% annualized rate, payable weekly upon resolution, lacking a floating rate adjustment mechanism to stabilize the share price. If BitMine fails to pay dividends on time, unpaid interest accrues weekly on a compound basis, with a penalty interest cap of 15% per annum.

The liquidation reference price for these preferred shares is initially $100, dynamically adjusted according to a market price formula, with a floor not lower than the face value; redemption includes investor put rights triggered by change of control events.

The fixed 9.5% annualized dividend payout can attract fixed-income investors but also reflects the higher risk premium required for financing by companies heavily exposed to Ethereum assets in a bear market environment.