On February 24, the Financial Times' Alphaville column published an article titled "Mirror mirror on the wall, what is the most shorted stock of them all?" providing some very interesting data.

The article shows that the median short interest in S&P 500 index constituents has climbed to 2.7%, reaching one of the highest levels in nearly a decade. Among all the constituents, Strategy leads with a short interest accounting for 14% of its market value, while Coinbase ranks fourth with 11%. This means that among all U.S. listed companies with a market capitalization exceeding $25 billion, Strategy is the least favored.

Articles published in the Alphaville column do not represent the views of the Financial Times; its characteristic is sharp and unsparing language. Even as cryptocurrency has gradually moved into the mainstream today, articles about cryptocurrency in the Alphaville column still spare no effort in criticizing it. Whether Bitcoin is $10 or $100,000, they consistently believe cryptocurrency is meaningless.

On February 2, Craig Coben, a veteran investment banker and former Vice Chairman of Global Capital Markets and Head of Global Equity Capital Markets at Merrill Lynch, also published an article in the Alphaville column criticizing Strategy's model.

Craig Coben's views are not extreme; he similarly believes that Strategy does not face a short-term "run" risk and currently has no liquidity crisis. However, he pointed out some core issues, such as the fact that the model of hoarding Bitcoin does not generate cash flow, thus requiring constant financing and diluting common shareholders' equity. Additionally, Strategy's tendency to buy when market sentiment is high and Bitcoin prices are elevated is a systemic, unsolvable problem.

Regarding Strategy's high short interest, some analysts believe that not all short positions are "naked shorts" against Strategy; some may be used by hedge funds to hedge their Bitcoin spot holdings. Nevertheless, it still indicates that there are many people bearish on Strategy, at the very least, everyone believes that if Bitcoin falls, Strategy cannot remain unscathed.

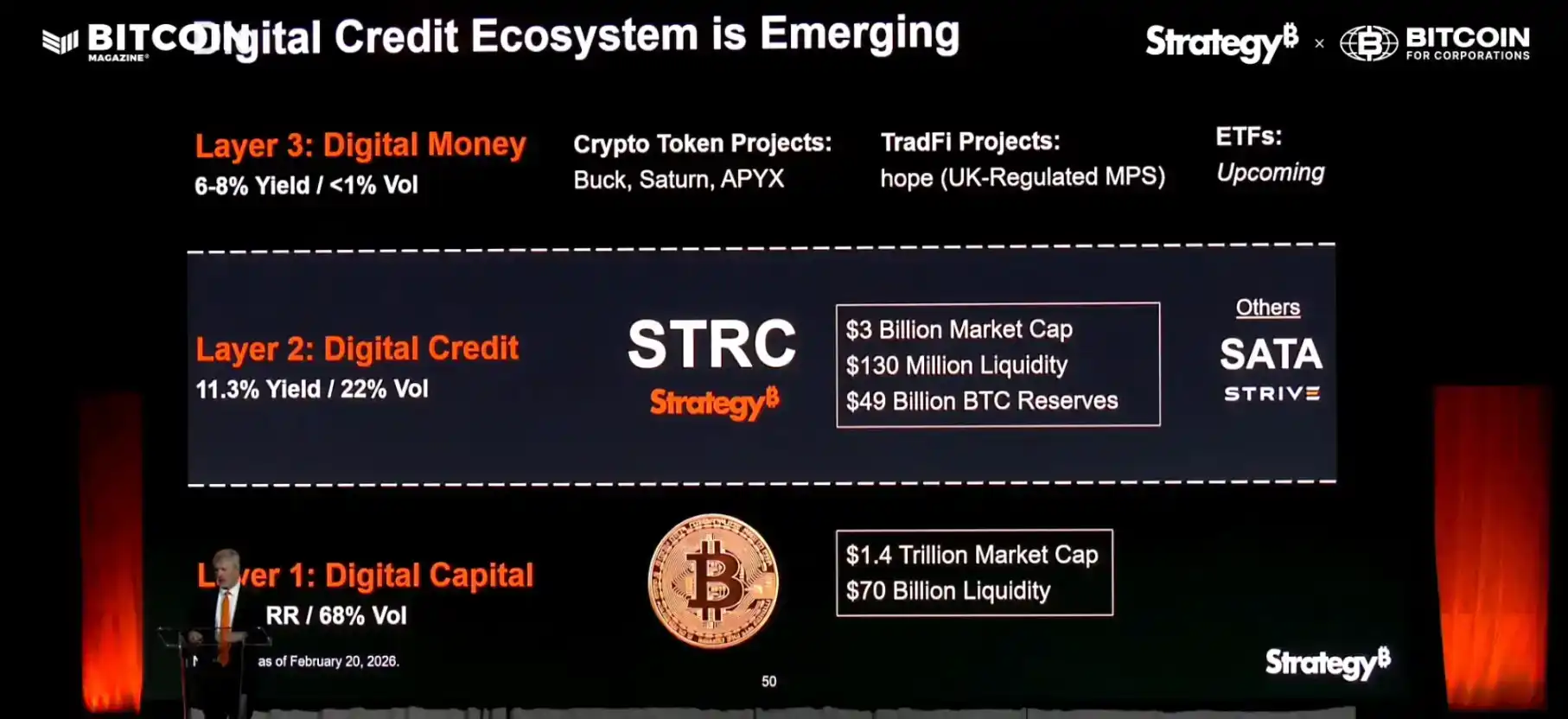

In Craig Coben's article, he mentioned that Strategy refers to the five types of perpetual preferred stock it issued as "digital credit," a concept that Michael Saylor has been emphasizing since the end of last year.

In this conceptual framework, the first layer, "digital capital," is Bitcoin. The second layer, "digital credit (or digital debt)," consists of the various perpetual preferred stocks issued by Strategy. These preferred stocks come with high yields, and Strategy must pay corresponding interest to holders annually.

The third layer is "digital currency," which refers to currencies, including stablecoins, issued based on the financial products in the second layer for trading. For example, Saturn in the diagram above plans to issue the USDat stablecoin based on STRC and U.S. Treasury bonds; this project has also received investment from YZi Labs.

If this logic isn't clear, you can draw an analogy with the United States. The U.S. continuously issues Treasury bonds based on its influence, only needing to pay interest before maturity and using new debt to repay old debt upon maturity. As long as the U.S.'s international influence and the status of the dollar do not weaken, this game can continue indefinitely. For Strategy, Bitcoin is like the U.S. influence, digital credit is like U.S. Treasury bonds, and Strategy also needs to borrow new debt to pay the annual preferred stock interest. However, as long as the price of Bitcoin continues to rise in the long term and drives Strategy's stock price up, the company can continuously issue new shares to finance the purchase of more Bitcoin and pay interest, continuing this cycle.

Michael Saylor is a firm believer that Bitcoin will change everything. In his view, Bitcoin's infinite rise is a more reliable bet than the U.S. winning forever, so he is more willing to issue currency based on an asset that is "destined" to continuously appreciate, just as the U.S. dollar was initially pegged to gold.

Strategy's strategy is not new; it only needs to ensure it has enough cash to pay interest to continuously finance the purchase of Bitcoin. Like U.S. Treasury bonds, this is a game that everyone knows will eventually reach its end one day, but no one can determine how long it can last. Strategy's current financial reserves are also sufficient; its CEO stated that Strategy would only be forced to sell Bitcoin if the price remained below $8,000 for 4 to 5 consecutive years.

If this extreme condition were actually met, not just Strategy, but the entire Web3 industry might disappear.

Even an old-school banker like Craig Coben must admit that Strategy will not face financial problems in the short term. However, for hedge funds, Strategy is a good tool for hedging against a decline in Bitcoin; for short sellers, it is reasonable to short a system that only functions normally when Bitcoin rises during a cryptocurrency downturn. At least for now, there aren't many reasons to be bullish on Strategy.

Michael Saylor's ambition to leverage Bitcoin to launch a new currency is itself interesting. The U.S. dollar is used to buy Bitcoin, and the U.S. dollar is also used to pay interest. The goal of a system built with billions of U.S. dollars is ultimately to destroy the very bricks and mortar that built it. Perhaps the elites on Wall Street are also chuckling; after all, they have no interest in researching whether Strategy can truly become a century-old company. They only care about when your stock price will rise and when it will fall.

Michael Saylor believes Bitcoin will inevitably continue to hit new highs, so he uses it as the cornerstone of everything; holders and users of the U.S. dollar believe the United States will continue to prosper, so they tacitly allow the constant raising of the U.S. debt ceiling. Both are acts of belief—so which is more advanced than the other?