Written by: @0xBenniee

Original title: The Next Stop for Tokens: Does a Project with Cash Flow Really Need to Issue a Token?

Token issuance is no longer the only solution: For teams with clear cash flow, channels, and compliance paths, TGE is not a mandatory option.

Short- to medium-term prices are primarily driven by three factors: liquidity, attention, and token distribution structure.

The long-term value of a token depends on value capture; how value is captured is crucial to the token's long-term value.

The next stop for tokens may be the "machine economy": Payments between Agents and native protocols like x402, promoting pay-per-call and profit-sharing based on contributions.

This article is inspired by @DrPayFi (Co-founder of Huma.Finance)'s response to the author's question:

Q:

Over the past year, Huma has built a complete Payfi infrastructure network. However, tokens in the ecosystem often limit project development. For example, issued tokens are essentially liabilities and place retail investors as counterparties. Not all stakeholders can benefit, and the team must invest significant effort in market cap management or token distribution.

Of course, during TGE, no early participants were disadvantaged, which seems out of place in a market where "no one looks at the long term."

Detailed reply as follows:

First, TGE is a harvesting sickle for some projects with no substance, but for long-term projects, it may be an "accelerator"

This was a recurring topic at Consensus: For the vast majority of projects with stable cash flow, token issuance may not be the more profitable choice, and often the disadvantages outweigh the benefits.

Once TGE begins, the team must not only focus on product development and growth but also manage additional external variables such as price expectation management, liquidity structure and market-making arrangements, complex communications with exchanges, and market sentiment fluctuations. These uncertainties continuously consume organizational attention and may even affect product节奏 and strategic decisions.

- What is an "accelerator"?

In the Payfi network, compared to traditional Fintech growth paths that rely more on licenses, channels, and regional networks, scaling liquidity and quickly converting it into TAL (Total Active Liquidity) that can be genuinely used typically requires more time.

TGE provides a more efficient "global distribution and attention aggregation" mechanism: Unlike the门槛 and geographical limitations of stock market listings, tokens allow global users to participate, hold, and trade绑定 to network growth through DEX/CEX from anywhere, providing additional momentum for ecological collaboration and growth flywheels. To some extent, this helps projects gain user attention faster and increase real user growth.

- What is a "sickle"?

Conversely, for projects without products or users, TGE → selling tokens becomes the only way to exit or profit. By repeatedly pumping and dumping, they can simply extract liquidity from the market and exit.

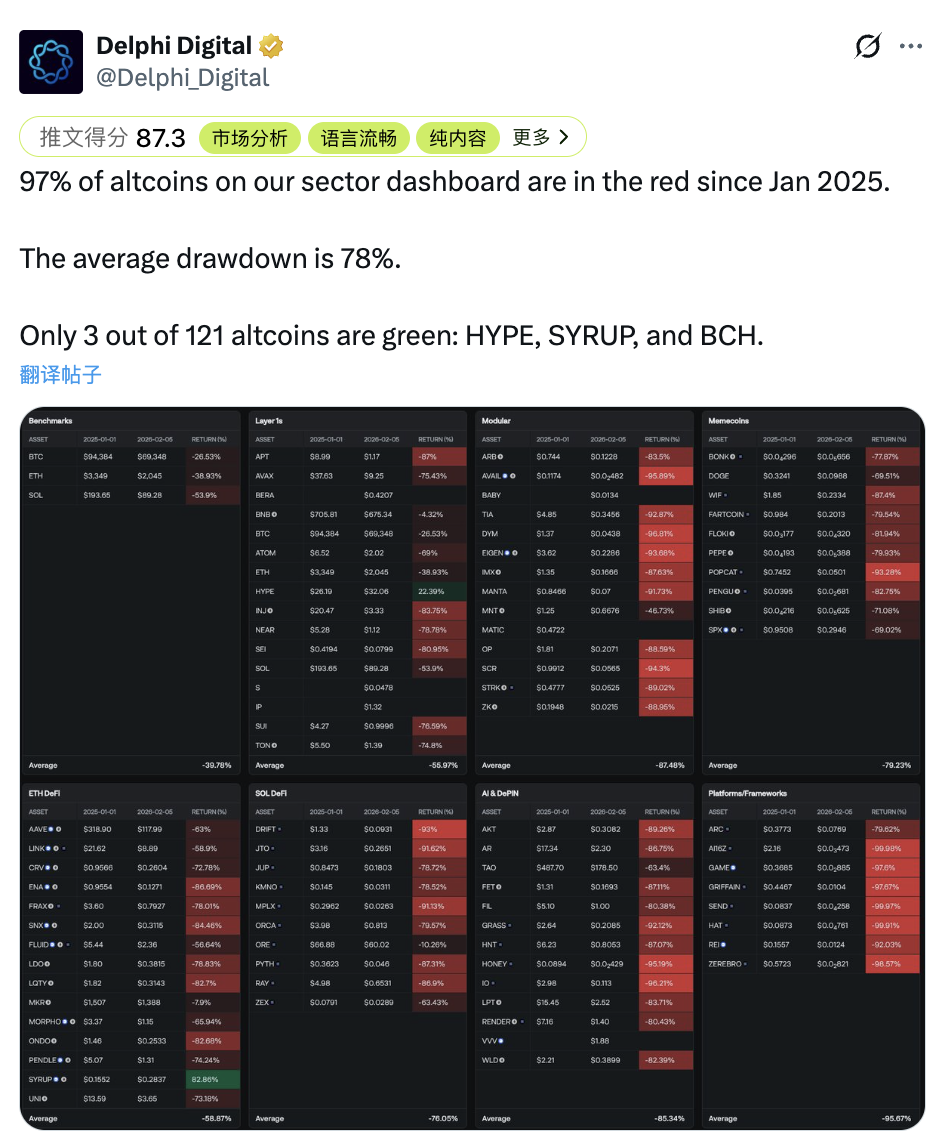

More残酷的是, this is not an exception but the norm in the current market. Over the past year, the vast majority of newly issued tokens have experienced significant pullbacks, with 97% of tokens shrinking by an average of 78% in price. As market liquidity becomes thinner and exits rely more on secondary markets, this "blood-sucking" secondary market strategy becomes more frequent, effective, and irreversible.

Factors determining token price after TGE and potential external benefits

Currently, Crypto projects still have some structural issues, such as the long-term mismatch between "exit channels" and "external growth."

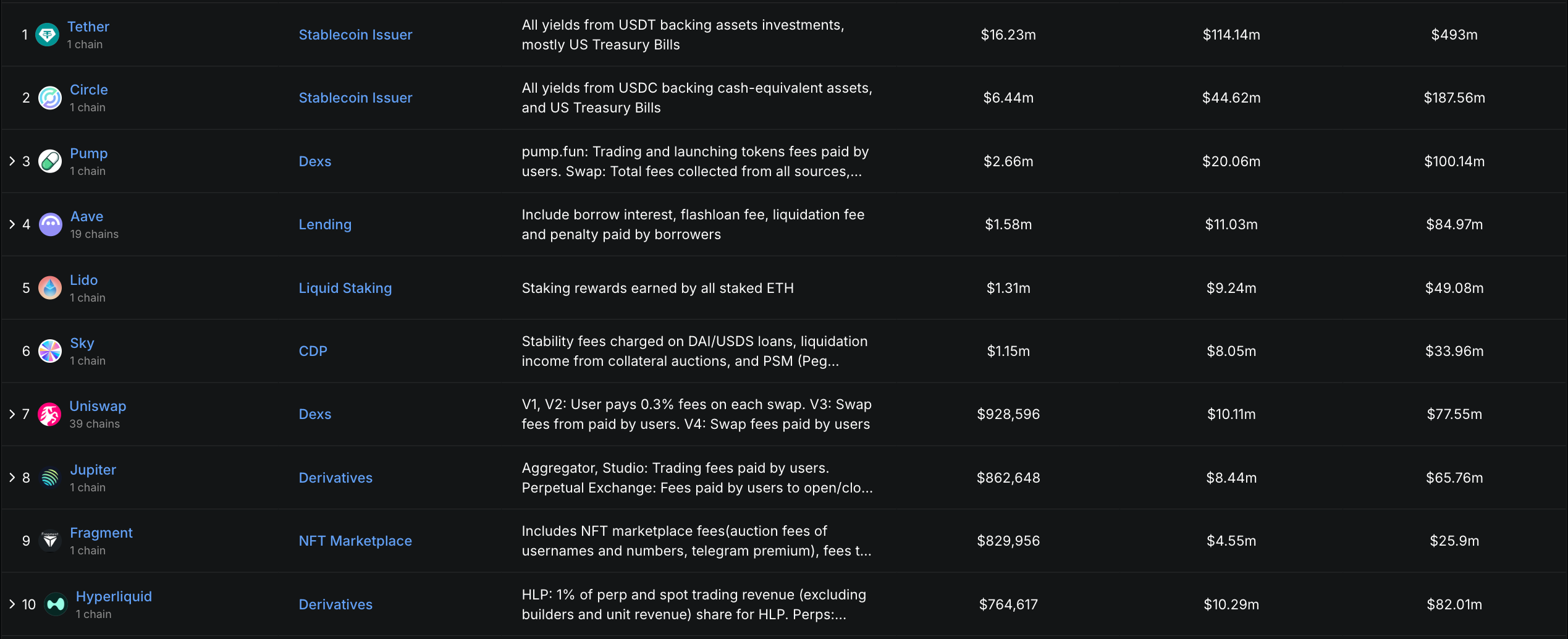

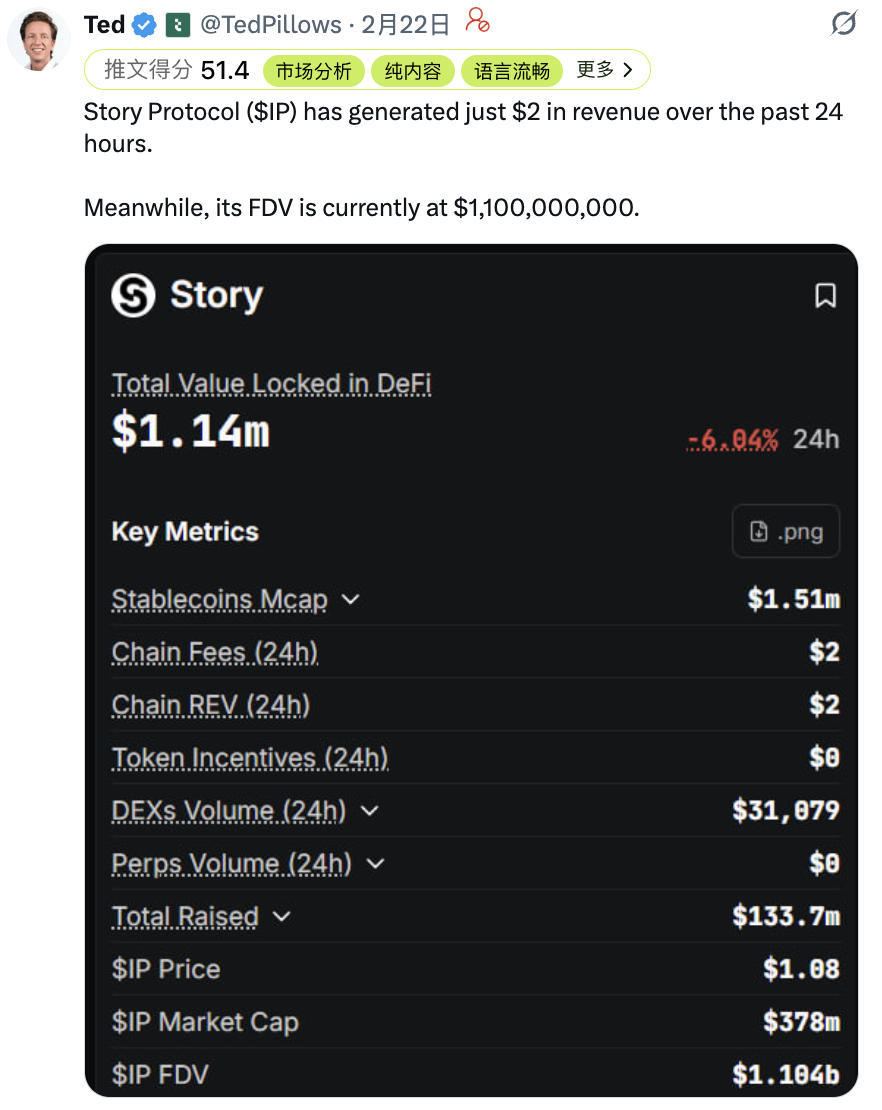

On one hand, the supply side of public chains and projects is长期 "over-issued," but the market's capital size and on-chain transaction intensity are insufficient to support continuously rising FDV/market cap. Most projects struggle to form stable, scalable protocol revenue solely through their products, let alone use this cash flow to消化 future large unlocking pressures.

Taking DeFiLlama's统计口径 as an example, only 6 protocols had protocol revenue exceeding $1M in the past 24 hours, and only 49 had protocol revenue exceeding $5M in the past 30 days. This means that relying solely on protocol revenue often cannot support excessively high valuations,更难承接 the supply impact of tokens during subsequent unlocking cycles.

On the other hand, factors such as market makers, exchanges, and users also play highly uncertain roles in token prices. When early capital exits rely more on secondary markets, prices are naturally dominated by interested parties.

Apart from early VCs who can still exit partially through mergers and acquisitions or follow-up financing, more projects, when cash flow is not yet formed and financing windows are tightening, tend to shift financing functions to secondary markets: through phased unlocking and so-called "reasonable减持," they transfer the already scarce market liquidity from retail investors to the project side.

In the short term, this can keep projects afloat, but in the long run, it pushes the market into a negative cycle, eventually evolving into an irreversible development of "bad money driving out good."

This corresponds to what @ChaseWang mentioned in an interview: in the current environment, the short- to medium-term trends of many assets often revolve around the following three variables:

- Liquidity: Whether there is money in the market, the willingness/risk appetite to buy, and whether there are more attractive alternative assets determine the upper limit of price increases.

- Traffic (attention): The spread by top KOLs,投放 by agencies and channel resources, and the concentration of retail attention often determine the amplitude of short-term fluctuations.

- Token distribution structure: The size of the circulating supply after TGE, token distribution, the unlocking and release节奏 of token economics, and arrangements around liquidity.

The thinner the liquidity, the more the market relies on narratives and prices; the more it relies on prices, the more it damages user and long-term capital confidence, eventually evolving into a筹码博弈 between projects and retail investors.

But in reality, projects, retail investors, and exchanges are not天然对立面. The common interest of all three parties is to maximize the "upper limit & imagination of the leader," attract incremental capital and real-use scenarios from outside, rather than repeatedly PVP in存量资金, treating the secondary market as an endless ATM.

Flowing water does not compete to be first; it competes to be endless.

Product value and value capture

Many projects do have "product value," but the value does not feed back into the Token.

Returning to today's topic, you will find a more counterintuitive fact: a project not issuing a token does not mean it is not great. For example, @Pumpfun proved that "product value" itself can be established in Web3, but whether the project's token can be priced long-term depends on value capture: without a clear回流机制, token value can often only be supported by sentiment and token distribution structure.

A typical positive example is Hyperliquid. Its "token value capture" is widely recognized by the market: real revenue generated by the protocol → forms continuous buy-side回流 (e.g., buyback mechanisms) → directly binds token value to trading activity. The more active the trading and the more revenue, the stronger the token's承接力, and the clearer the pricing anchor.

Conversely, common counterexamples usually fall into three structures:

-

The product has revenue, but the token price does not reflect it: The money earned by the protocol stays with the team/company/channel side. The token itself is only responsible for "governance voting" or "narrative performance." Value回流 is absent, and long-term pricing can only rely on sentiment.

-

The token has incentives, but no real demand/users: Data (TVL/trading volume looks good) is inflated through high inflation subsidies, but once incentives are removed, data plummets, leaving only unlocking and selling pressure.

-

Using the secondary market as a financing and exit channel: When the project's cash flow is not yet sustainable, it chooses to use the secondary market to bear financing pressure. The token becomes the project's "liability side," and the pricing logic gradually degenerates into a筹码博弈.

So, where is the future path?

If the "path" of traditional payments in the past is understood as a major breakthrough that solved geographical isolation: enabling people and merchants, banks and banks to complete trusted settlements under unified rules even thousands of miles apart. Then the next twenty years' main theme may shift from "people paying people" to "programs paying for programs." Payments between Agents using Crypto will become a new high-frequency transaction form.

If we turn the timeline back to 2006, Mastercard completed its IPO on May 24, 2006, at $39.00 per share. At that time, it was更多的是被视为 a traditional financial infrastructure for "bank card networks/clearing processing."

Today, Mastercard's network connectivity covers 210+ countries and regions, with 150M+ merchant acceptance networks and 3.5B+ circulating cards. Mastercard implemented a 10:1 stock split in January 2014. At the current price of approximately $521.93, investors holding Mastercard stock have achieved 134-fold growth over the past 20 years.

What about crypto? Blockchain may not be born solely for transfers between humans; it is more like a settlement language prepared for the next generation of automation.

In the future Agent economy, the payment demand for API calls will likely become a new high-frequency scenario: Agents will not only exchange information and tasks but also engage in "pay-per-use, instant settlement" around data, models, computing power, and service calls. Experiments like Clawbot, which allows Agents to transfer money to each other to "earn," are already验证 the feasibility of this path to some extent.

Precisely because of this, the 24/7 efficient settlement, programmable funds, and traceable ledger provided by blockchain have the opportunity to become a more universal payment base for the future robot society.

In the next stage, retail investors need not place all their hopes on TGE. Increasing regulation is not necessarily the end of tokens but更像是在逼 the industry to separate two things: financing and exit, returning to the more replicable path of equity/IPOs; Tokens should return to what they are supposed to do (on-chain incentives, node collaboration, resource allocation).

Meanwhile, TGE may still exist, but it should more be the "lubricant" of the network. Especially in the future Agent economy, tokens叠加 protocols like x402 that embed payment into HTTP may become infrastructure for pay-per-call and profit-sharing based on contributions.

Final thoughts

It is undeniable that we are in a colder/more残酷 four-year cycle.阵痛 is inevitable, just like the body's self-protection expelling toxins. The industry also needs to squeeze out the toxins in the system (bubbles, Scams,劣质项目). If劣币 are not驱逐,真正的基础设施 can hardly be seen. At present, we are更像 sitting on a high-speed train. The scenery outside the window is changing, the people around us may change, but our direction has never changed.

I would like to end with a quote from Richard: "The current winter is like the bursting of the Internet bubble in 2000. It清洗的是一众不靠谱的 .com, leaving behind Amazon and Google. Regulation will挤掉骗局, and the protocols that truly solve problems will reshape the global financial infrastructure in the next 5 years."

If we had the chance to go back to those days, would we have the courage and cognition to catch unicorns like Amazon and Google? If the next cycle is a game for institutions, then all past patterns will be reshuffled. By the time the new格局 arrives, I hope we can still be at the table.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush