Original Author: Tyler Durden (ZeroHedge pseudonym)

Original Compilation: Source: ZeroHedge

Guide: SpaceX fell for three consecutive days, plummeting 16.4% on Monday alone, erasing $600 billion in market value, dropping back to the $150 opening price. This analysis bluntly argues that those who wanted to buy have already done so, and more critically, the selling pressure hasn't truly arrived yet. This pump-and-dump used only 5% of the float. Insiders could sell up to 44% of the shares by early September.

It began with a bang. SpaceX went public on June 12, opening at $150 per share, well above the $135 IPO price. Within two days, aggressive traders started furiously buying 380-strike call options expiring two days later, trying to launch the stock price into the stratosphere, creating a gamma squeeze.

@zerohedge tweet: They're really going to do it

In a report this morning, Canaccord described the "new wave of optimism" accompanying SpaceX's listing:

"The SPCX tape shows the market has entered a new phase of euphoria. Prior to this historic IPO, we felt AI optimism was already full, sometimes excessive, but buying was primarily from rational (albeit exuberant) institutions—large, well-funded public companies and PE investors. In our view, SPCX has turned a new page, with dramatically heightened retail participation, propelling the stock into the global top six by market cap and adding the equivalent of half of META's market value in its first week. Its market cap far surpasses that of its sister company TSLA, while revenue is only about one-fifth. Despite the company being named SpaceX, revenue is actually skewed towards connectivity—Starlink contributed $113.9B, launch services only $41B, and AI compute capacity was $32B in 2025."

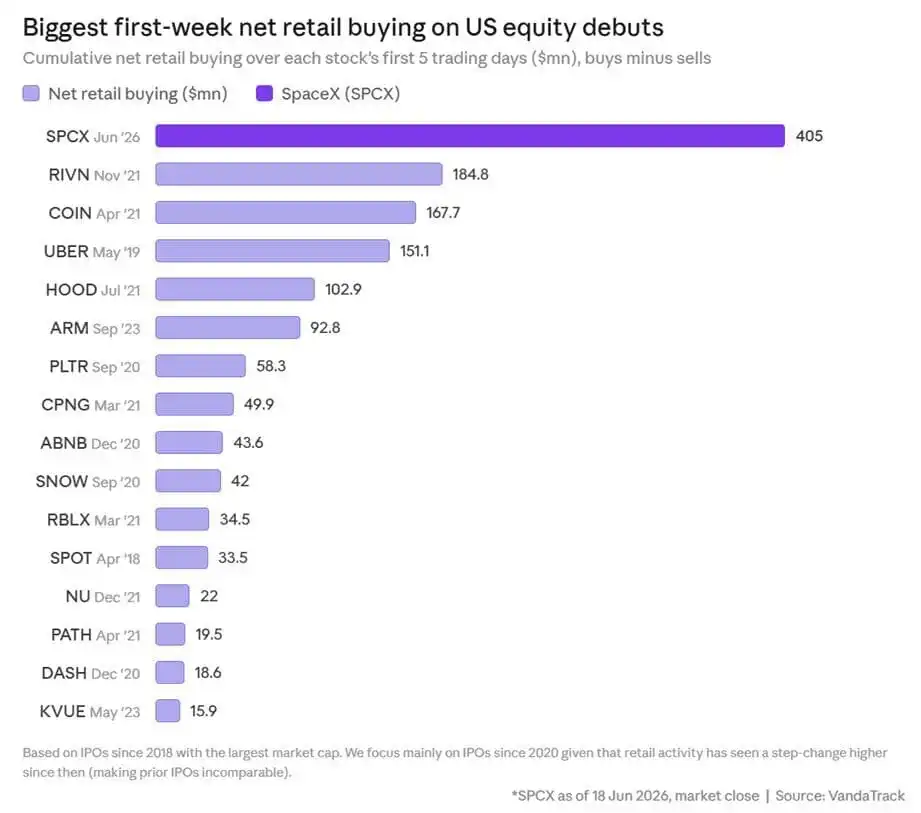

Vanda Track put it even more starkly. In a review published earlier Monday, it wrote: "SpaceX's debut week set records. Retail investors net bought $405 million of SPCX in the first five trading days, the strongest retail participation in an IPO in recent years. Buying was extremely aggressive in the first few days, cooling somewhat towards the week's end. The flow characteristics increasingly resemble building a long-term position, not chasing a short-term meme stock."

Caption: Retail flow for SPCX in its first five trading days

Source: Vanda Track

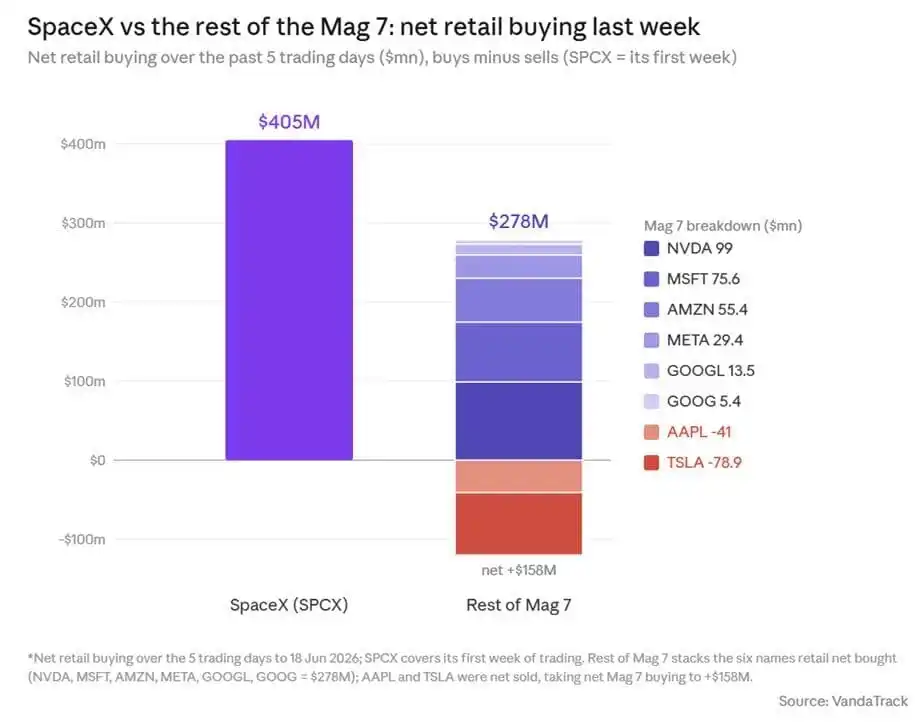

The scale of retail buying in SPCX becomes even more staggering in context. Last week's retail purchases of SPCX exceeded their combined buying of all other Mag 7 stocks—NVDA, MSFT, AMZN, META, GOOGL, and GOOG totaled only $278 million over those five days. Retail buying of SPCX also surpassed the combined retail flow into the SPY and QQQ ETFs ($352 million). A stock that began trading just last week is already competing with the market's largest individual stocks and ETFs for retail dollars.

Caption: SPCX retail buying vs. Mag 7 stock retail buying

Source: Vanda Track

The old playbook unfolded again. Alongside the explosive buying of the stock, retail investors rapidly poured into various SpaceX leveraged products, with similarly strong demand. In the first few trading days, retail bought $65.8 million worth of the Leverage Shares 2x Long SPCX Daily ETF—a significant number, but still well below typical levels during speculative retail manias. Even so, it crushed recent thematic new issues: Roundhill's Memory ETF (DRAM) attracted only $5.6 million in its first four days. It took DRAM 22 trading days to surpass the cumulative retail buying that the SpaceX leveraged ETF had already absorbed.

Caption: SPCX leveraged ETF retail flow vs. contemporaneous thematic ETF retail flow

Source: Vanda Track

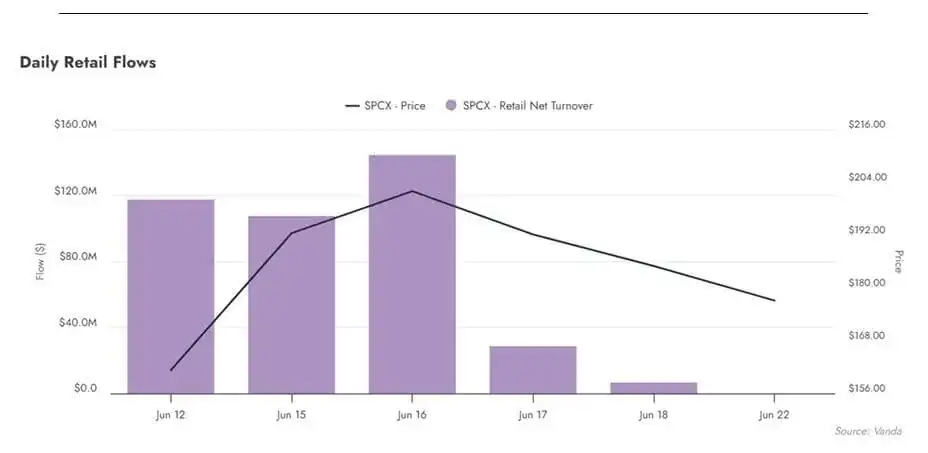

Out of the gate, the momentum quickly stalled, and the fantasy of "riding a reusable rocket all the way into orbit via gamma squeeze" evaporated. June 16th was the peak, when SPCX hit a record high of $225, briefly surpassing Microsoft in market cap. Since then, daily retail flows have collapsed, with retail turnover almost vanishing.

Caption: SPCX daily retail flow—cliff-like drop after peaking on June 16

Source: Vanda Track

This brings us back to Canaccord's statement. Based on SpaceX's early trading, the firm judged that "tech stocks likely have enough momentum to sustain them in the near term," but it also warned: "There's now an added layer of dangerous vacuum beneath these stocks."

Sure enough, once momentum dissipated, coupled with market awareness of trillions of shares about to unlock, the stock fell for three consecutive days, culminating in Monday's crash. On that day, as SpaceX sought to issue over $20 billion in investment-grade bonds for the first time—taking advantage of still-euphoric debt markets to replace a much higher-interest bridge loan before the window closed—SPCX plunged 16.4%, erasing a record $600 billion in market value in a single day. Including Wednesday's 5% drop and Thursday's 3.5% decline, the stock is now only slightly above its $150 opening price from two weeks ago.

Caption: SPCX price action since IPO—retreat from $225 high to around $150

Source: ZeroHedge

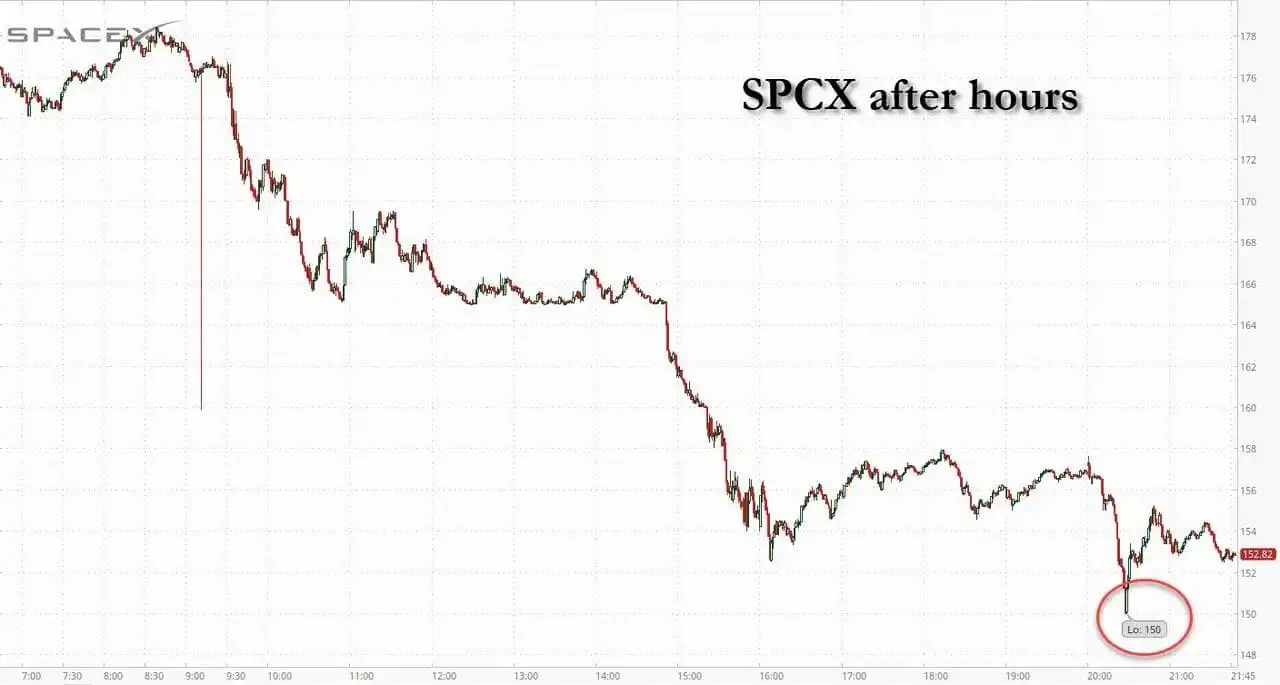

Worse, after hours, SPCX briefly touched the $150 IPO opening price. If it opens below that level tomorrow, everyone who bought and held in the secondary market will be underwater.

Caption: SPCX after-hours drop to near $150 IPO opening price

Source: ZeroHedge

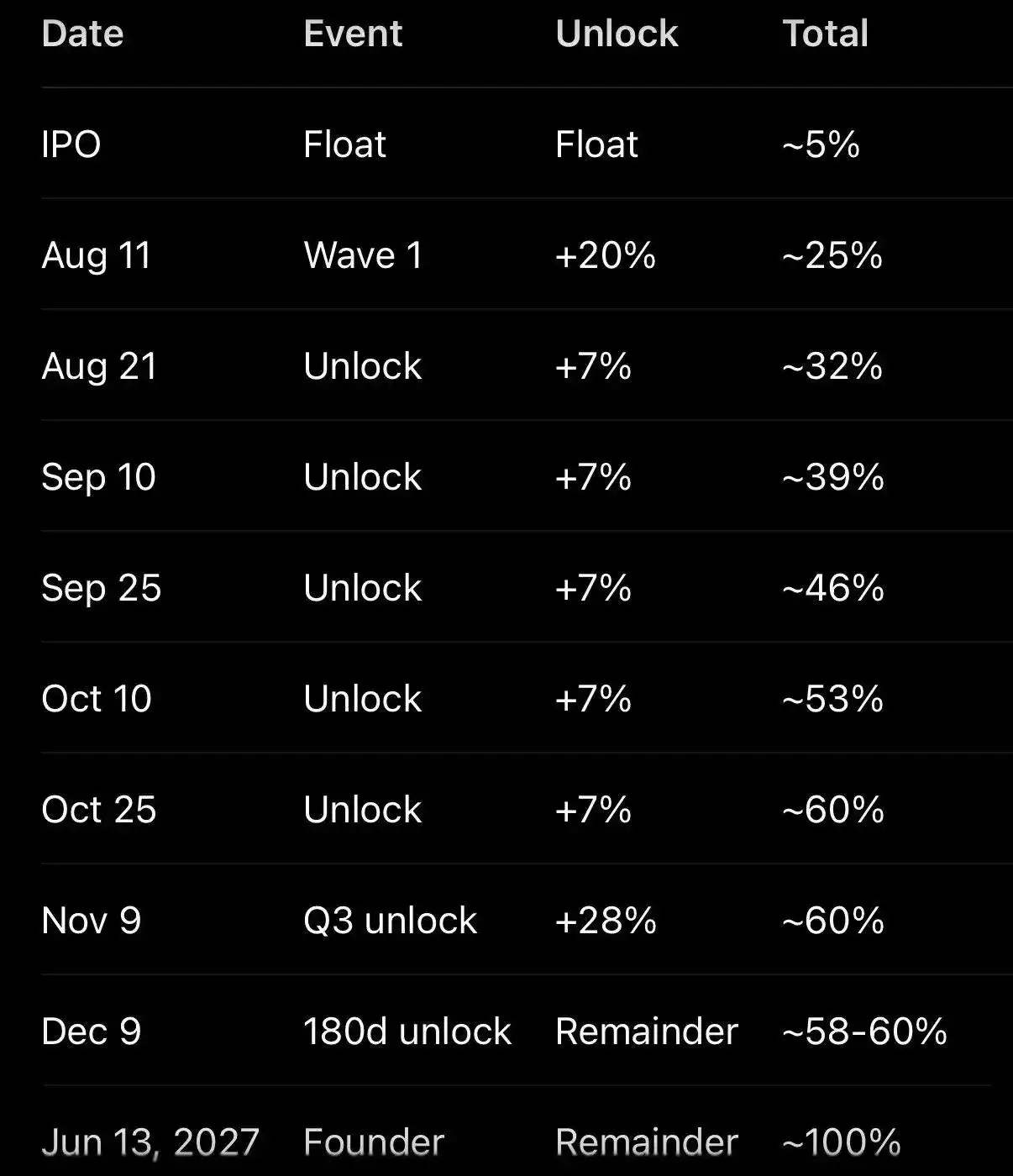

Particularly noteworthy is that this pump-and-dump occurred with only 5% of the float available for trading—95% of shares are still locked up. But that will change soon.

Caption: SPCX lock-up structure—currently only 5% float, 95% locked

Source: ZeroHedge

22V Research strategist Jeff Jacobson says that after SpaceX reports earnings in early to mid-August, a 20% block of insider shares will unlock. Additionally, if the stock price remains 30% above the IPO price, a further 10% will unlock. Another 7% unlocks around August 21st and September 10th.

Caption: SPCX lock-up expiration schedule

Source: 22V Research

Jacobson says insiders could potentially sell up to 44% of SpaceX shares by early September, expanding the current float by approximately 900%.

In other words, lifting the stock price from here will only become increasingly difficult. Meanwhile, JonesTrading chief market strategist Michael O'Rourke says "the sellers have regained control," adding: "Everyone in the world who wanted to buy, has already bought."

Bloomberg, commenting on today's decline, wrote that SpaceX's slide today "dragged down most of the market."

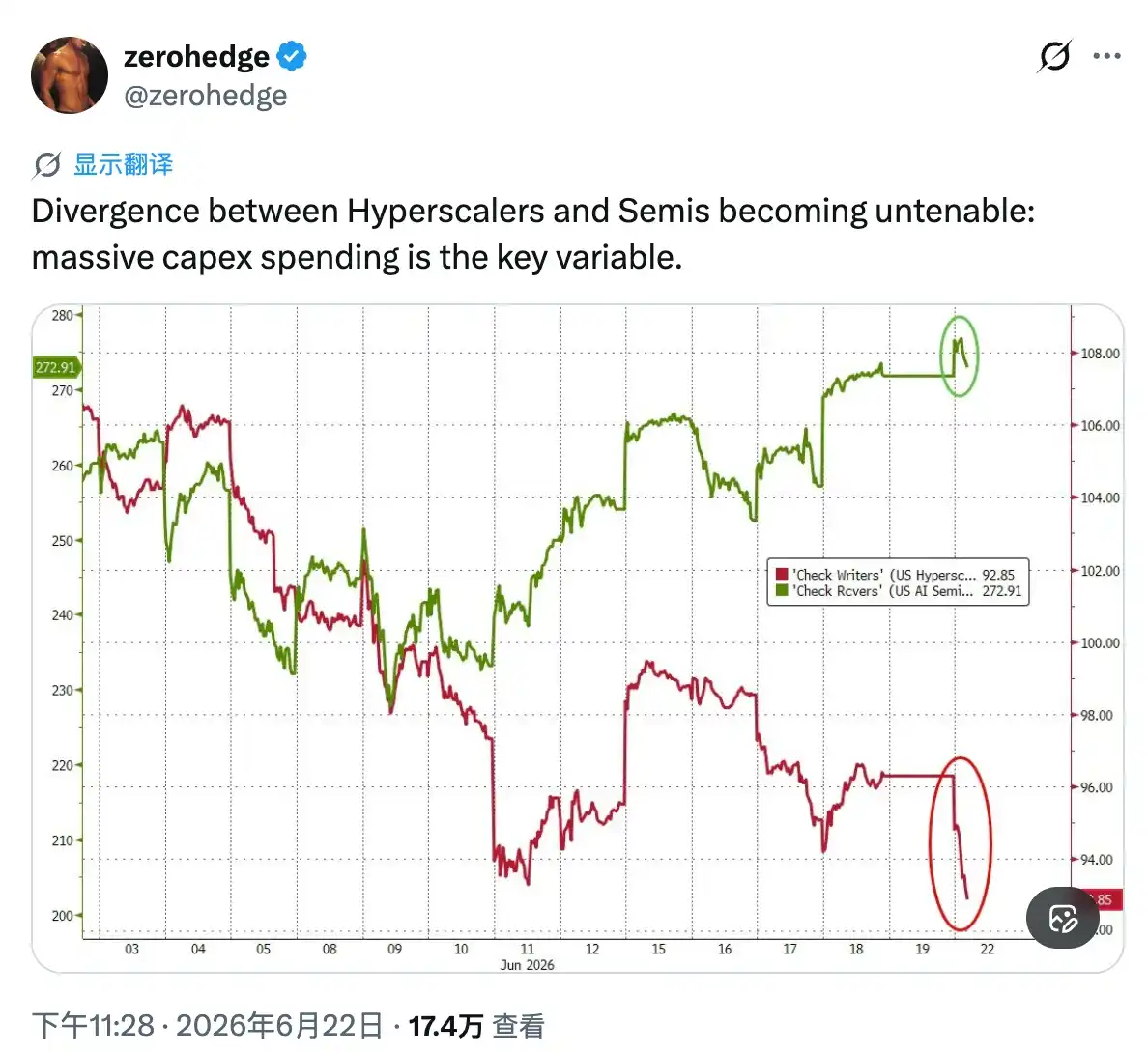

Whether that's truly the case remains to be seen. But in this market—which has run almost entirely on retail euphoria and momentum-chasing since the March lows—once retail truly gets cold feet, starting with SpaceX, then the memory bubble, and finally the semiconductor stocks that have feasted on the AI trade...

@zerohedge tweet: The divergence between hyperscale cloud providers and semiconductors is unsustainable: massive capital expenditure is the key variable.

...then, it will be time to invert Eliot's line: The whimper of selling will become a bang.