Author: Shen Hui, Yuanchuan Investment Review

Hong Hao's knowledge planet officially announced a price increase, tagged at 1499 yuan/year, equivalent to a bottle of Moutai.

Before the price hike, the annual fee was 899 yuan. Based on 14,000 recharges, in just two months, Hong Hao's GMV on the knowledge planet reached 12.586 million yuan.

Similarly, Hong Hao's friend Li Bei also ventured into knowledge payment. A course worth 12,888 yuan, with 200 spots, sold out in two days. That is to say, in just two days, Li Bei's course sales revenue reached 2.57 million yuan.

As is well known, media is a notoriously bad business. This conclusion is easily drawn from the media sector's consistently poor performance among the 31 primary sectors of Shenwan. However, in this sunset industry, private domains and selling courses stand out as exceptions, attracting countless financial professionals to bend their backs.

Former Guohai Fixed Income Chief Jin Yi's Douyin account "Bai Nian Talks Politics and Economics" gained 1.6 million followers in three months, with membership for one-on-one consulting services from Chief Jin priced at 4,283 yuan per month; Tan Jun is about to launch the "Industry Decision-Maker Internal Reference Circle," limited to 30 seats, priced at 159,880 yuan; the more upscale-sounding "Bull Bear Beast Club" offers paid members not only access to Fu Peng's financial intelligence courses but also the opportunity to ski with him in Changbai Mountain.

Compared to their American counterparts, who show a stronger willingness to pay, financial consumers in the U.S. are different. The big short seller Michael Burry simply closed his hedge fund and switched to launching an electronic newsletter on Substack priced at $379 per year, attracting 187,000 subscribers in just two months—shorting Nvidia isn't as easy as making money.

Suddenly, financial big shots are jumping in, not competing on who has more investment ideas, but on who has more subscribers. Is investing too hard to make money, or is the business of headcounts too easy?

Three Types of Leverage

Silicon Valley investor Naval Ravikant mentioned that to achieve financial freedom, one needs to use three types of leverage:

- The first is labor leverage, which means being the boss and having others work for you;

- The second is capital leverage, like Warren Buffett using capital leverage to expand influence and make money with money;

- The third, which he considers the most important leverage, is "products with zero marginal cost of reproduction," mainly including code and media.

In Naval's view, the wealth of the new generation of millionaires is created through code and media.

Joe Rogan relies on podcasts to earn $50-100 million annually [1]. Using this new type of leverage, simply by increasing paid memberships and online course sales, one can amplify the results of their labor hundreds or thousands of times. Its advantage is that the cost of reproduction is almost zero, and anyone with a computer and internet access can easily earn passive income.

And Hong Hao and Li Bei恰恰同时拥有这三种杠杆。

Li Bei founded Banxia in 2017, and by 2022, its scale had exceeded 10 billion yuan. She had already achieved financial freedom through labor and capital leverage. As she herself said, she doesn't lack the tens of millions of yuan generated annually from knowledge payment. But it cannot be denied that these tens of millions are far more certain in the short term than waiting for a reversal in China's real estate market.

Compared to Li Bei's colorful业余生活 of baking, gardening, and playing tennis, Hong Hao's recent experiences have been more turbulent.

Earlier, Hong Hao was the Chief Global Strategist at CICC and had worked at Citigroup and Morgan Stanley. In 2022, after leaving Bank of Communications International, he switched between buy-side and sell-side roles,先后 joining Srui Group and Huafu International. He is now the Managing Partner and Chief Investment Officer of Lianhua Capital.

However, Hong Hao's performance has always been a mystery.

In August 2023, he launched the Lotus-AAA fund with Srui and Lianhua Capital. Except for a single-month surge of 8.98% in September 2024, its performance had been lukewarm before. Perhaps because the fund's operation time was too short, when展示业绩, backtested simulated historical performance dating back to September 2002 was also included. At least the chart shows that Hong Hao似乎真有20年累计高达718.77%的投资收益。

You can question Hong Hao's actual performance, but you cannot question his chart-making ability

Hong Hao and Li Bei are skilled at building IPs and generating traffic. Their熟练运用 of the third type of leverage gives them stronger money-making abilities than their peers in knowledge payment.

In terms of赛道选择, the macro sector where Hong Hao and Li Bei operate naturally reaches a wider audience. Not everyone cares about what Nvidia's open-sourced VLA model is called, but everyone cares whether gold will continue to rise in the future and whether the stock market in the Year of the Red Horse and Red Goat will have the Nine Purple Fire luck.

In terms of表达方式, compared to being lulled to sleep by the ambiguous views of economic grandmasters at roundtable forums, people prefer to listen with wide-eyed interest to Hong Hao predicting the fifth wave of the bull market and Li Bei analyzing the escape from the micro-cap fire. Even if they are evasive, they might意外收获 "MaiMaiMai" (BuyBuyBuy/SellSellSell)的艺术表达—after all, if they win, it's buy buy buy; if they lose, it's sell sell sell.

In terms of写作文体开发, Hong Hao is good at mixing classical Chinese and obscure characters into macro analysis, mysteriously citing various sources, giving people a reading experience that is hard to understand yet greatly震撼. Hong Hao once explained that the best article sounds like废话 but has some unexpected consequences [2]. Li Bei, on the other hand, can skillfully combine her emotional journey with macro analysis, occasionally posting相亲贴 (matchmaking posts), providing some low-participation-threshold topics.

Precisely because people love macro literature掺杂 with "fortune-telling" and "gossip," Hong Hao and Li Bei have captured the huge流量 in the financial circle, also creating a broader entry point for their transition into knowledge payment.

It's All Business

Fund managers are usually cautious about using the third type of leverage.

Because once a fund manager starts writing articles or selling courses, they are seen as not focusing on their main job, diverting time that should be devoted to investment research. Moreover, transitioning to media won't gain more professional recognition, just as people always criticize financial influencers—if their investment ability is strong enough, why would they take time out to teach others how to make money?

Whether it's Hong Hao creating a星球 (knowledge planet) or Li Bei selling courses, their purpose in涉足知识付费 is not simply to transition into self-media.

Compared to Li Bei, Hong Hao transitioned to investment relatively late, and he can't even show a three-year continuous net value curve. Therefore, he更需要 to constantly market the accuracy of his predictions on social media to背书 his investment ability.

On November 28 last year, Business Weekly brought Hong Hao, Li Bei, and Fu Peng together at a roundtable. When the three discussed gold, Fu Peng's views were ambiguous, Li Bei was clearing positions and bearish,只有洪灏公布了详细的卖点—selling all when the gold price reaches $4500/ounce.

This led to质疑, because the price of the main Comex gold futures contract had never reached $4500/ounce at that time. Non-main contracts had briefly reached it, but it was almost impossible for large institutional funds like Hong Hao's to exit at the peak in such low-liquidity contracts.

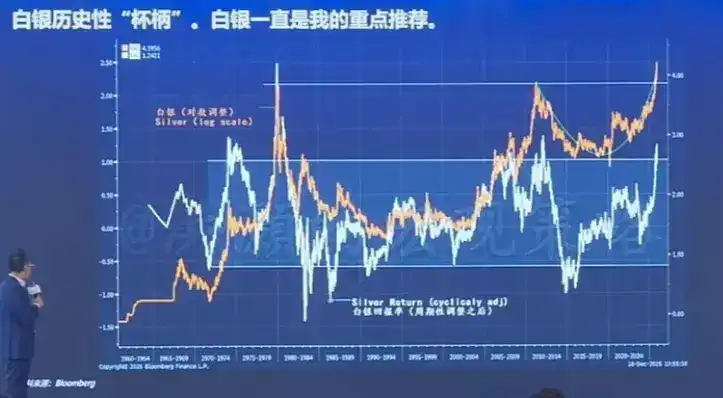

Hong Hao did not公开详细的黄金交易平仓单, but instead marketed on his星球 "Ten Thousand Witness the Miracle of Predicting Silver." He publicly predicted:

Silver hasn't finished its run; how deep the cup is, how high the target is. If 4500 is a fair price for gold, then for others, we need to use our imagination. New highs are for buying; those who fear heights are destined for hardship.

As written in "The Crowd," he who掌握了影响群众想象力的艺术, also掌握了统治他们的艺术.

Hong Hao believes silver has formed a giant 60-year "cup and handle" pattern

Ultimately, Lianhua Capital is still not well-known. Posting粉丝的好评 (fan praise) on the星球, creating涨价预期 (price increase expectations) for the星球, and selling more "星球茅台" (Planet Moutai) can孵化 more future私募客户 (private fund clients). Compared to collecting management fees and performance fees, it has higher short-term economic benefits.

After all, outputting a "bullish on silver" view is easy—like the two sides of a coin, you can brag if it goes up—while "heavily betting on silver" involves multi-dimensional博弈 with the market, human nature, rules, and scale.

Compared to Hong Hao, Li Bei faces a different situation. After Banxia crossed the 10-billion-yuan threshold, its performance growth weakened, and it dropped out of the camp of billion-yuan私募 early this year. In an environment where Bridgewater China remains strong and quantitative macro opponents are formidable, the urgent task is to stabilize old clients and avoid redemptions.

Li Bei's approach is to免费赠送 online courses to all Banxia investors and offline courses to investors who have held the fund for more than 2 years or invested more than 5 million yuan. Thus, before the course starts on January 24th, investors wanting to redeem get a赎回冷静期 (redemption cooling-off period).

In November, Minghong's macro product sold out upon launch; in December, Two Sigma's "CTA + Index Enhanced"复合策略 product, with a 2 billion yuan quota, was instantly snapped up across three major channels. This type of multi-strategy product from quantitative私募无形之中 forms a substitute for Li Bei's macro strategy.

Moreover, subjective私募 are gradually declining on the distribution side, and mainstream channels are somewhat avoiding them. In the future, subjective managers will inevitably need to invest more energy in direct sales.

A clever way is to first筛出 (screen out) the customer base with payment ability from fans with a price of 12,888 yuan, and then use slogans like "easily achieving long-term annualized returns of over 10% by taking the course" to锁定 (lock in) those customers who are dissatisfied with wealth management returns and渴望致富 (eager to get rich).

Fans with purchasing power and purchasing desire, after attending Li Bei's offline classes for答疑解惑 (Q&A), can naturally be converted into私募 clients with极少的 time cost and极高的 conversion rate.

Astute managers not only skillfully use the third type of leverage but also善于叠加 use all three types of leverage.

Epilogue

When discussing knowledge payment becoming a trend in the asset management industry, many people think of two aspects:

- First, the pressure from salary cuts in the financial industry prompts practitioners to seek other sources of income;

- Second, switching from investment to media is like降维打击 (attacking from a higher dimension). Precisely because of this, financial self-media is the首选副业 (preferred side job) for most financial practitioners.

But looking deeper, this actually stems from the bidirectional需求 of investors and managers—investors need reliable sources of information, and managers need loyal clients.

It's like Jensen Huang gave a speech at CES, and the next day there were dozens of interpretations利好 (beneficial) to which market sectors. It seems information is equalized, but in reality, it adds countless噪音 (noises). The advancement of AI allows more noise to be produced at low cost. For both investors and managers, attention and trust are the scarcest resources.

Who wouldn't want to spend some money to buy a professional fund manager's knowledge planet to gain an information edge, or even follow their operations? Many people know that Hong Hao's predictions will eventually翻车 (fail), but what they are buying is not a 100% win rate, but rather, in the chaotic market, through his repeated analysis and confirmation, they can obtain an emotional anchor and comfort.

Some subjective fund managers are also gradually realizing that they are no longer the first choice for institutions, distribution channels, or high-net-worth clients. So they can only work harder to reach more precise clients through私域 (private domains) and courses. Some skilled subjective私募 have even screened their clients into executives or industry experts of invested companies—making money for clients while also obtaining the most前沿 (cutting-edge) industry information差 (information gap) from them.

I asked him why he doesn't ask sell-side analysts. He replied that sell-side can only be bullish on their own industry and mislead him, while invested clients can tell him the most real and objective views on the industry.

When gold becomes harder to dig and shovels are in excess, having a矿藏地图 (mineral deposit map) is the important thing, and the person selling the map becomes the one who makes the most money.