Author: Curry, Deep Tide TechFlow

Original Title: The Bustle Belongs to the 'Epsteins', Saylor Just Wants to Hoard Coins

There's a reason why one person can hoard 710,000 Bitcoins.

Last Friday, the U.S. Department of Justice released documents related to the Epstein case, spanning 3 million pages. Politicians, billionaires, celebrities—a string of names are popping up from these materials. And the founder of Strategy (formerly MicroStrategy), Michael Saylor, is also in there.

However, Saylor's appearance is a bit special; he was at the table that was looked down upon.

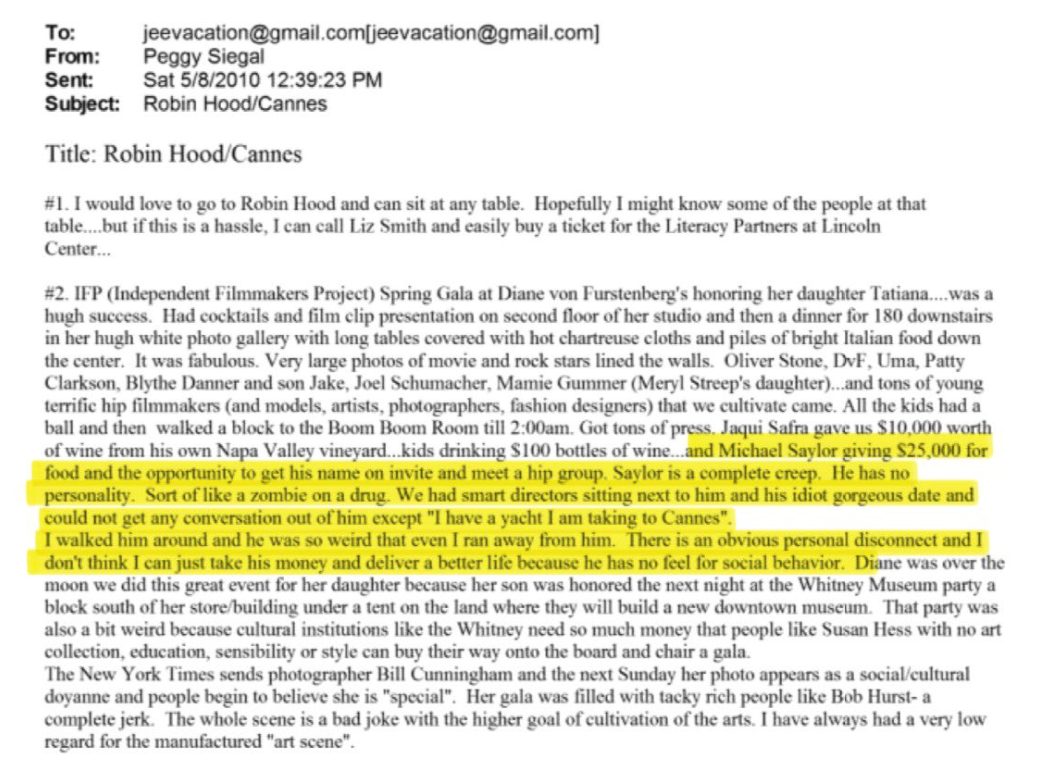

From the currently disclosed information, in 2010, Epstein's publicist Peggy Siegal once complained in a private email:

"There's a guy named Saylor who spent twenty-five thousand dollars on a dinner ticket, and I was responsible for socializing with him. But this guy was completely unapproachable, like a drugged zombie. I couldn't stand it and ran away halfway through."

Peggy's main job is as a Hollywood movie publicist, and her side hustle is helping Epstein organize dinners—essentially scouting for wealthy people to pull into the circle.

Socializing with the rich, helping them meet the right people at parties and dinners, ensuring they have a good time and spend their money comfortably. Having been in the business for decades, she's按理说 seen all kinds of billionaires.

But Saylor, she couldn't handle.

The reason wasn't that he had character flaws; it was that he was too dull. He paid to get in, sat there unable to chat, showed no interest in socializing at all.

Peggy's exact words were, "I don't even know if I can take his money, couldn't figure out how to handle him... He has no personality, completely ignorant of social etiquette."

Now that the Epstein case has exploded, people on the list are busy distancing themselves. Saylor, on the other hand, never managed to squeeze in back then.

Being overly boring and reclusive became a protective shield.

But when this "boredom" is placed in a different context, it's another story.

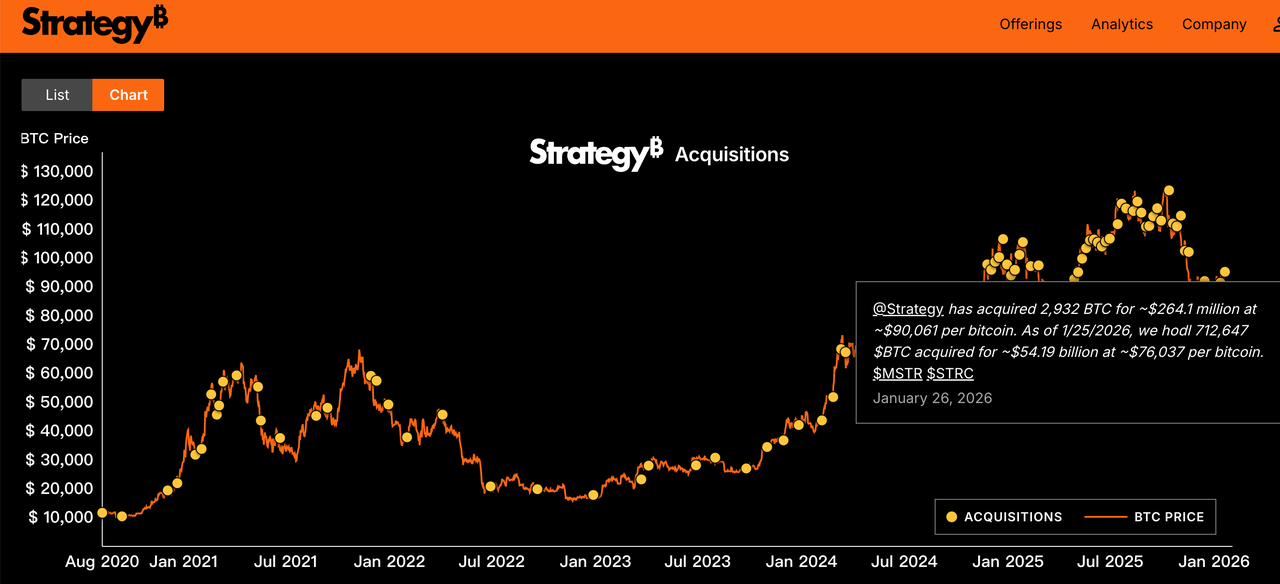

Saylor's company, Strategy (formerly MicroStrategy), is the publicly traded company holding the most Bitcoin globally. This January, when Bitcoin was still fluctuating around $90,000, they bought over 37,000 more Bitcoins, spending $3.5 billion.

Buying almost every week, rain or shine.

As of now, Strategy holds 712,647 Bitcoins, with an average cost of $76,037. And today, Bitcoin just fell below $76,000, meaning Saylor's position is right on the break-even line.

The market fear index hit a 20-week high, and the crypto world is filled with cries of despair. Strategy's stock price has also dropped 60% from its peak.

But Saylor tweeted "More Orange," implying he'll keep buying next week.

Back then, Peggy called him a zombie. Looking at it now, hoarding coins might just be a job for zombies.

No explanations, no timing the market, no getting off the ride. Feeling nothing from the outside world, and feeling good about oneself.

And while Peggy complained back then about not knowing how to help him spend money, Saylor has clearly found his way to spend it now: buying Bitcoin, all of it.

From that email, Saylor was an outsider in the world of fame and fortune. He couldn't sit still, couldn't chat, spent a night as if he never came. But such people are反而 steady in trading.

No need to socialize, no need to build relationships, no need to guess what others are thinking. Just focus on one thing, buy every week, and never sell.

Dull, uninteresting, insensitive to the outside world... These traits are flaws in social settings, but when it comes to hoarding coins, they might be a talent.

After this news spread, classic memes have already appeared on Twitter, roughly meaning that Saylor has no interest in underage girls but is extremely obsessed with underage assets (referring to young/early Bitcoin).

From a hindsight perspective, this exposure has, to some extent, also built a positive image for Saylor.

After the Epstein case broke out in 2019, Peggy, the publicist, had all her contracts canceled by clients like Netflix and FX, which basically ended her PR career; meanwhile, Saylor is now one of the world's largest Bitcoin holders.

The rejected one is still buying coins; the one who rejected him is already out of the game.

But to be fair, Saylor's current situation isn't that easy either.

The new Fed Chairman Warsh is hawkish, and the market expects he won't aggressively cut interest rates after taking office. Once interest rate expectations change, all kinds of assets worldwide come under pressure collectively.

Gold fell, silver fell, and Bitcoin fell even harder.

Coupled with tariff friction and tense U.S.-Europe relations, capital is starting to flow towards traditional safe-haven assets. The narrative of Bitcoin as "digital gold" is gradually fading.

If Bitcoin continues to fall, Strategy's ability to raise funds by issuing new shares will weaken, and the flywheel of coin-stock rotation could turn into a death spiral.

But Saylor really doesn't seem to care about any of this; this might be the other side of "boredom."

Ordinary investors can't do what Saylor does, not because they lack money, but because they are too "normal." Normal people read news, look at K-lines, see what others say. When the fear index soars, their hands start to itch, and their hearts start to ache.

Making decisions every day, each decision consuming willpower.

But in Saylor's strategy, there seems to be no "decision-making"环节. Buying is the only action; not selling is the only principle.

In his own words: "Bitcoin is the best asset ever invented by humanity, why would I sell?"

You can call this faith, or you can call it obsession. But from an execution perspective, the biggest advantage of this system is:

It doesn't require you to be smart; it only requires you to be boring.

Of course, this is not advice to imitate him. Saylor's底气 comes from being a publicly traded company—he can issue stock, borrow money. Ordinary people don't have these;模仿 his approach will most likely only lead to losses.

But there is one thing that might be worth learning from.

In investing, "fun" is often the source of losses.

Frequent trading, chasing hot trends, following news, using leverage... these behaviors that make investing "fun" are precisely the enemies of returns.

And the strategies that truly make money are often so boring they make people want to sleep.

Saylor's case is a bit extreme, but the logic holds. In a market full of noise, "boredom" might be the rarest ability.

Those who were socially adept at the parties back then are now either distancing themselves, under investigation, or have completely disappeared.

Perhaps, hoarding coins and being a person share the same principle:

Don't linger in lively places; boring things are worth doing long-term.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush