Author:Zhou, ChainCatcher

On February 25, stablecoin issuer Circle (NYSE code: CRCL) released its 2025 fiscal year fourth quarter and full-year financial report.

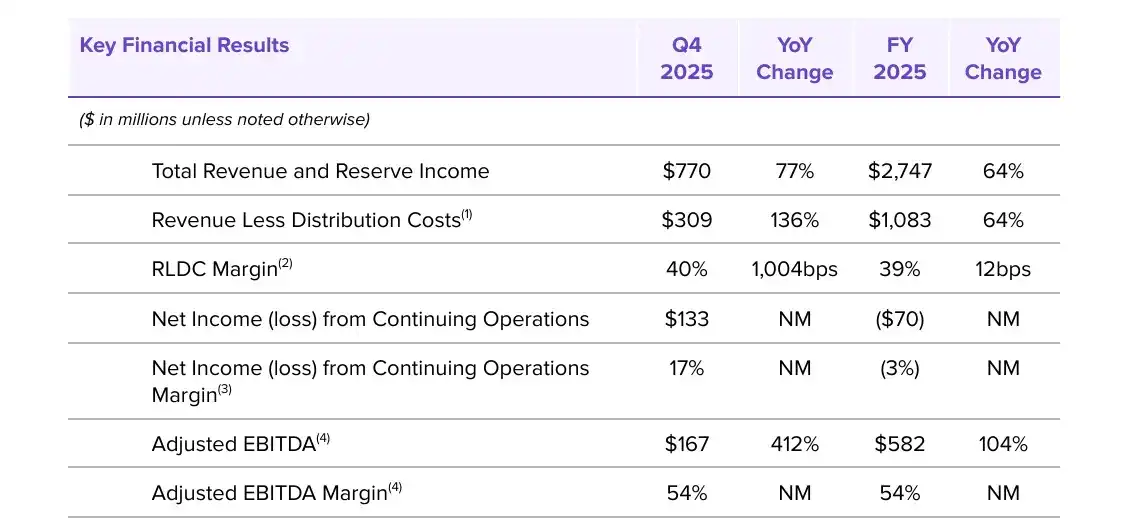

The report shows that the company's total revenue and reserve income for the fourth quarter reached $770 million, a year-on-year increase of 77%, exceeding market expectations.

Driven by this, CRCL stock price rose over 35% at Wednesday's close.

Specifically, the growth of its stablecoin USDC was the core highlight of this earnings report. As of year-end, the circulation of USDC reached $75.3 billion, a year-on-year increase of 72%.

Meanwhile, network activity showed explosive growth, with on-chain transaction volume in the fourth quarter reaching $11.9 trillion, a year-on-year increase of 247%.

In terms of revenue composition, reserve income remains the company's main revenue pillar, contributing $733 million in Q4, a year-on-year increase of 69%.

Although market yields decreased by 68 basis points during the period, this pressure was offset by the significant expansion of USDC's average circulation scale.

At the same time, non-interest income reached $37 million, mainly due to the steady accumulation of subscription services and transaction fees.

Looking at the full-year performance, the company's total revenue and reserve income was $2.7 billion, a year-on-year increase of 64%.

Although continuing operations recorded a net loss of $70 million, this was mainly affected by the one-time inclusion of $424 million in stock-based compensation expenses during the IPO process.

As this expense is non-cash in nature, the company's core business is profitable after exclusion. Adjusted EBITDA reached $582 million, doubling year-on-year, showing that operating leverage is gradually emerging.

In terms of strategic layout, Circle is gradually transforming from a pure stablecoin issuer to an internet financial infrastructure provider, strengthening its underlying position in the real-time transaction field through various technological initiatives.

The report shows that the Arc public blockchain testnet is running stably, with transaction finality time shortened to about half a second, and total transactions have exceeded 166 million. The mainnet is expected to be officially launched within the year.

In terms of the payment network, the ecosystem of the Circle Payments Network continues to expand. Currently, 55 financial institutions have officially joined, with another 74 in the qualification review stage. The annualized transaction volume over the past 30 days has reached $5.7 billion.

It is worth mentioning that the strategic cooperation with Polymarket further highlights the value of USDC in emerging fields. As one of the world's largest prediction market platforms, Polymarket will gradually switch all betting and settlement to native USDC.

This cooperation not only eliminates bridging risks and improves capital efficiency but also directly converts the user growth of the prediction market into long-term increments in USDC circulation and transaction volume.

In addition, Circle is also gradually penetrating the traditional financial ecosystem. The company has not only achieved all-day settlement cooperation with Visa but also broadened application scenarios through platform integration with Intuit.

At the regulatory compliance level, the company received conditional approval from the U.S. Office of the Comptroller of the Currency to establish a national trust bank in December 2025, and further consolidated its first-mover advantage in compliance under the GENIUS Act framework.

The secondary market has given a relatively positive response. Technically, before the earnings release, the company's stock price had rebounded from its low and stabilized above the 7-day and 30-day moving averages.

On the institutional side, ARK Invest, under Cathie Wood, increased its holdings of Circle stock multiple times during market corrections. The latest holdings are about 4.14 million shares, worth approximately $261 million.

Mizuho Securities upgraded CRCL's rating from underweight to neutral at the end of January, setting a target price of $77. The institution believes that the growth of Polymarket will directly drive the expansion of USDC scale and revenue.

However, Circle still needs to deal with potential headwinds in the future.

On the one hand, the downward trend in interest rates may continue to put pressure on reserve income, which has been reflected in the decline in yield in the fourth quarter.

On the other hand, the stablecoin competitive landscape is changing. The USAT stablecoin, launched by Tether and issued by Anchorage Digital, is targeting the U.S. institutional market and is regarded as the first substantive compliant competitor for USDC domestically. This competition may lead to some diversion in the compliant institutional share.

In addition, overall cryptocurrency market volatility and macro cycles will still create uncertainty for circulation growth. According to Coinglass data, the current total stablecoin market capitalization is about $264 billion, with USDC accounting for about 28.5%. Although USDC leads the industry in growth rate, Tether still dominates.

Worthy of special attention from investors is Circle management's expectations and execution plans for the future. The company provided clear guidance for the 2026 fiscal year:

- USDC circulation targets a compound annual growth rate of 40% over a multi-year cycle;

- Other income (subscription, service, and transaction fees) is expected to be $150 to $170 million;

- RLDC margin (revenue minus distribution and transaction cost margin) remains in the high range of 38% to 40%;

- Adjusted operating expenses are expected to be $570 to $585 million.

These guidelines also reflect management's confidence in continued scale expansion, cost control, and accelerated growth in non-interest income.

Furthermore, Circle CEO Jeremy Allaire repeatedly mentioned AI agents and their payment needs during the earnings call.

He said, we are about to enter a world where there may be billions or even hundreds of billions of AI agents interacting on the internet and performing economic functions.

These AI agents need programmable digital dollars and open infrastructure to enable autonomous transactions, and Circle's products are built for this.

Specifically, Circle is heavily investing in agent-based payment infrastructure.

Currently, Circle Gateway has entered the test network phase, supporting AI agents to autonomously initiate cross-chain USDC transactions, with a single transaction cost as low as $0.00001 (extremely low fees, suitable for micro-payments and high-frequency machine-to-machine transactions).

It was also mentioned in the meeting that currently about 99% of agent-based payments use USDC, thanks to Circle's cross-chain deployment and participation in agent payment standards (such as the x402 standard, in cooperation with Google etc.).

Overall, this earnings report validates Circle's strategic execution capability in a complex regulatory environment, and the new story of AI+ payments has expanded the company's valuation imagination space. Despite facing yield fluctuations and emerging competitive challenges, Circle continues to exert efforts on the track of "financial infrastructure-ization" and "compliant expansion".