Original Author: Xu Chao

Original Source: Wall Street News

SpaceX is about to usher in its historic IPO this Friday, with the offering price set at $135 and an initial notional market capitalization reaching $1.75 trillion. As a super unicorn of rare scale in Wall Street's history, its post-listing stock price trajectory and share float dynamics have sparked frenzied interest from global investors.

Well-known Tesla community opinion leader and former Wall Street analyst Alexandra Mertz (online alias Tesla Boomer Mama) recently engaged in an in-depth discussion with host Herbert. Mertz believes that due to the extremely low initial free float (only 4.3%), SpaceX may experience an epic supply vacuum in the early stages post-IPO.

According to a Bloomberg report on Wednesday, predictive index rebalancing firm Intropic estimated that because Nasdaq, FTSE Russell, and MSCI all plan to rapidly include SpaceX in their respective indices, passive investors are projected to hold approximately 30% of SpaceX's free float merely 15 trading days after listing. In contrast, if the previous slower inclusion rules were followed, this proportion would only be about 4%.

Academics and market observers warn that mechanical demand of this scale, combined with market frenzy for Musk, SpaceX, and artificial intelligence, could form a self-reinforcing feedback loop, pushing the stock price continuously higher.

Mertz believes investors need to closely watch two key time points of significant trading value: "The peak passive buying wave brought by the formal inclusion in the Nasdaq 100 on July 7th" and "the overlap period of early shareholder lockup expiration and potential merger announcement around two days after the Q2 earnings call in the latter half of July." Behind this highly meticulously designed IPO lies a vast capital chess game where Musk resolves his own $7 billion tax event and utilizes Wall Street investment banks for interest exchange.

Core Viewpoint Summary

July 7th Nasdaq Inclusion Day: Passive fund building positions across the US will collide head-on with the historically lowest free float. Market estimates place this passive buying volume between $80 billion and $180 billion (closer to $150 billion). As old shareholders cannot sell stock at this time, the market free float reaches its lowest point.

Lockup Expiration Two Days Post-Q2 Earnings Call: The first tranche for lockup expiration seemingly amounts to 30%, but after deducting the 1-year absolute lockup period for Musk's own 50% share, the actual selling pressure is only 10%-15%.

July "Merger of Equals" Conjecture: Musk faces a $7 billion tax pressure triggered by exercising Tesla options before August 15th. Announcing a "stock-for-stock" merger of equals between the two companies between the July 7th SpaceX price peak and the late-July earnings lockup expiration is an extremely clever capital script fitting Musk's style.

Wall Street Banks' Interest Exchange: Charles Schwab, Morgan Stanley, J.P. Morgan—former institutional "arch-nemeses" of Tesla—rarely received slices of the lucrative SpaceX IPO quota. This could be Musk securing institutional "yes votes" in advance for the November shareholder meeting merger vote.

I. Extremely Low Free Float (4.3%): Grok Model Predicts Stock Price Could Double by July 7th

SpaceX (tentative stock code SPCX) priced its IPO at $135, with an initial notional market cap of $1.75 trillion. The planned issuance is 555 million Class A ordinary shares (approximately $7.5 billion in financing). As current market subscription interest is already oversubscribed by up to 2 times, underwriters are highly likely to fully exercise the "greenshoe option" (over-allotment option) within 30 days, increasing the total financing amount to $8.6 billion.

Despite the large financing scale, the issued Class A shares only represent 4.3% of the total market capitalization. This means SpaceX's free float is extremely tight in the early post-IPO period, leading to a period of intense supply vacuum within the first 15 trading days.

The first key time point: July 7th This is the first trading day after the Independence Day weekend and the 15th trading day post-IPO, when the Nasdaq 100 index inclusion for SpaceX formally begins.

At that time, index funds such as Vanguard CRSP and FTSE Russell must unconditionally build positions in the open market based on the free-float-adjusted mechanism.

Market estimates place this passive buying volume between $80 billion and $180 billion (closer to $150 billion). As old shareholders cannot sell stock at this time, the market free float reaches its lowest point.

II. "Precision Lockup Expiration" Tied to Earnings Call: Selling Pressure Halved, $135 Forms a Solid Price Level

Conventional IPO lockup periods are usually straightforward (e.g., 180 days), but SpaceX's lockup expiration schedule is intricately tied to the Q2 earnings conference call.

The second key time point: Two business days after the Q2 earnings conference call (estimated around July 22nd or 29th)

Market rumors suggest that following the Q2 earnings conference call, early insider shareholders will face their first large-scale lockup expiration of up to 30%, sparking market panic about selling pressure.

However, Alexandra clarified unequivocally during the discussion that market analysts are missing the core equity structure: Among the early insider shareholders, the majority (approximately 50%) is Musk himself. And as the founder, his shares are subject to a strict 366-day lockup period.

Therefore, two days after the Q2 earnings call concludes, the actual potential newly unlocked shares flowing into the open market are not 30%, but actually only 10% to 15%.

Furthermore, the intentions of early major shareholders are highly aligned:

Ron Baron has explicitly stated he will "not sell a single share, and will add $1 billion more in the open market";

BlackRock has publicly expressed a strong intention to buy $5 billion to $10 billion at IPO, exceeding the readily available supply;

Ark Invest (ARC) will selectively sell some old shares due to its single-stock 10% position limit but plans to add SpaceX to its other newly opened funds.

III. The July "Goldilocks" Script: $7 Billion Tax Event and "Merger of Equals" Conjecture

Savvy capital on Wall Street is connecting all the breadcrumbs. Alexandra points out that Musk faces a major personal timeline: He must exercise the stock options from his 2018 Tesla compensation package by August 15th this year, which will trigger a massive personal tax event of approximately $7 billion (tax payable in January 2028).

In the days around exercising the options by August 15th, the higher Tesla's stock price, the more beneficial it is for Musk's personal net settlement or pledged loans of shares. This is not a small amount but a massive game involving tens of billions of dollars.

Thus, Wall Street's most logical "Goldilocks scenario" conjecture emerges:

- Timing Selection: In the power vacuum between the July 7th Nasdaq inclusion completion (SpaceX stock price potentially more than doubled, market cap surging to a peak) and the late-July earnings lockup expiration (fresh shares flowing in).

- Strategic Move: SpaceX and Tesla announce a stock-for-stock merger of equals.

Such a merger would cause the stock prices of both companies to automatically enter a perfectly synchronized "lock step" driven by market arbitrage funds. Through this strategy of mutual positive feedback and elevating market cap via the public market's "non-sellers," Musk's tax funding pressure would be perfectly resolved.

IV. Wall Street Banks' "Political Arbitrage": Exchanging IPO Spoils for November Merger Votes

The biggest suspense for the merger script lies in the November shareholder meeting vote.

According to Alexandra's precise calculation: After Musk exercises his options, he will have about 17.5% voting power in Tesla. Passing a merger proposal requires an absolute majority of "50% plus one vote" of all outstanding shares, meaning Musk still needs to secure 32.5% of affirmative votes externally.

Currently, Tesla's retail ownership has decreased from over half historically to 31%, while institutional "Big Whales" engaged in frenzied secret accumulation in Q1 this year. To pass, support from major whales like Vanguard and BlackRock must be obtained (together they account for over 15%). Currently, BlackRock's CEO Larry Fink has mended relations with Musk at forums like Davos, and the basic institutional vote base (about 35%) is preliminarily secured. The remaining 15% gap requires mobilizing half of the 31% retail base.

Intriguingly, SpaceX's IPO unusually includes Charles Schwab, Morgan Stanley, and J.P. Morgan as core underwriters and distributors. These three institutions were the "arch-nemeses" leading the opposition votes in past Tesla compensation and Texas relocation cases:

Wall Street's Political Gambit: As one of the most profitable and prestigious IPO quotas in Wall Street history, no investment bank can resist the tens of billions in commissions and client prestige.

By offering this "spoils" to these three firms now, the implicit quid pro quo is: Having taken SpaceX's money, they must manipulate the shares they custodian to switch sides and vote "yes" for the merger at the November Tesla shareholder meeting.

Wall Street is profit-driven; faced with massive economic interests, they will not hesitate to compromise.

V. "The Perfect Defensive Fortress": Why Must SpaceX Acquire Tesla?

Addressing some investors' technical queries, the interview provides answers with profound legal and corporate governance depth:

1. SpaceX doesn't have hundreds of billions in cash on its books. How can it complete the acquisition?

This would absolutely not be a cash deal but a 100% pure equity swap. SpaceX currently has an authorized share capital limit of up to 36 billion shares. Post-IPO, only about 13 billion shares are actually issued, leaving an enormous room for share issuance. They can directly issue new shares to exchange for all of Tesla's shares.

2. Why can't the reverse happen, with Tesla acquiring SpaceX?

Because SpaceX's S-1 prospectus establishes a perfect "founder defensive fortress."

Musk suffered greatly from short sellers, activist investors, and Delaware judges during his Tesla era. SpaceX's governance architecture is meticulously fortified from the ground up:

Super-Voting Rights: SpaceX's Class B shares have 10x super-voting power, and 97% are firmly controlled by Musk himself;

Judicial Firewall: All shareholder lawsuits must be compelled to private arbitration, not filed in open court, directly disarming hostile litigation lawyers;

Succession Clause: Even if Musk passes away, the super-control rights of his Class B shares will directly transfer to his family.

Tesla's current governance structure has inherent flaws, preventing Musk from gaining absolute control. Therefore, only by merging Tesla entirely into SpaceX's legal framework can Musk's absolute control over the entire business empire be permanently protected from activist investors and local court interference.

The following is the full interview, AI-assisted translation.

Herbert:

Alright, everyone, welcome, and thank you for joining us today. We have invited Alexandra Mertz, also known as Tesla Boomer Mama. I think today will be a very special episode where she will share the most authoritative guide to the SpaceX IPO. We'll also share a few very important slides; I want to give a little preview now.

First, Alexandra has done a massive amount of work. She outlined the step-by-step process one can expect if a merger is announced; then, she will also list in detail what will happen on IPO day, when Nasdaq inclusion occurs, and when shareholders can sell after lockup. So, thank you very much for all this work, Alexandra. I know the IPO is this Friday, so many people have been asking about this. Tell us, what are you prepared to share with us today?

Alexandra:

Hi, Herbert, thank you for having me. Well, this all started—I mean, obviously, we've been discussing this merger idea for weeks, months. I am a firm believer in this merger. I want to state upfront that nothing that follows constitutes financial advice.

But personally, I bought quite a few call options for this August because I firmly believe this will happen. I did not participate in the Tesla—wait, correct, Tesla—I did not participate in the SpaceX IPO because, in my projected scenario, a merger will be announced sometime in July or early August this year.

Now, the timing of the SpaceX IPO actually gives me great confidence, which is why I wanted to do this episode. We've talked before about why this is important for those investing in SpaceX, those staying in Tesla, and those invested in both. Because I think there are several key dates you must pay attention to, as SpaceX's stock price might jump all over the place; nobody knows what will happen, not even Elon. So, Herbert, let's go slide by slide. Where would you like to start?

Herbert:

Yes, this one looks like the most important one. First, thanks to Aurelius for putting this together, right?

Alexandra:

Exactly. Aurelius read my article on SpaceX IPO details, which is pinned on my X (formerly Twitter) profile; you can go there to see it. Then you'll see his comment below where he said, "I fed all your data into Grok."

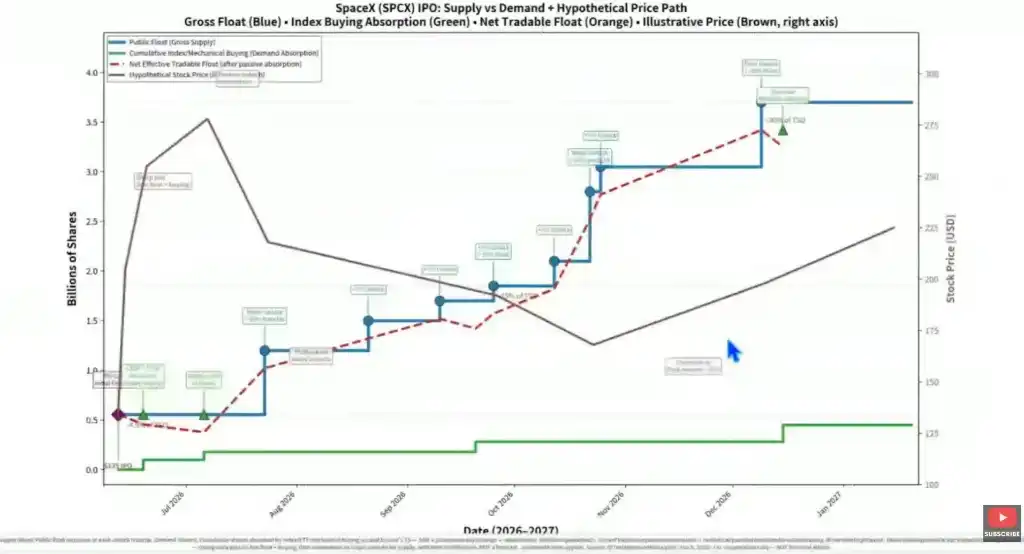

Then Grok gave me this chart, which is highly interesting. You might need to zoom in a bit so everyone can see clearly. But, um, maybe they don't need to see us anymore, I don't know. Move it a bit more to the left, if possible—I can't operate that. Okay. This all starts with the IPO this Friday, that's the brown dot, IPO price at $135, that inverted brown square, right.

Then you see this blue line, representing that early investors currently cannot sell. As you can see, this continues until the Q2 earnings call, where they will get their first potential large-scale unlock, up to 30%. That's the blue line; I'll detail later what happens after that. The green line below represents index fund demand to buy SpaceX stock.

This is relative to the free float. The first wave of dilution they put into the market is 555 billion shares (Note: This likely refers to a value or share count equivalent; clarified later), representing 4.3% of the notional market cap. This market cap will fluctuate, you'll see, but that's how it starts.

So we have 555, that's 0.5 on the left axis. On the green axis—sorry, on the green line, it shows what will happen with index funds. There's a lot of talk about index fund numbers on CNBC and elsewhere, but they don't understand these funds must buy based on free-float adjustment. Since this free float is only 4.3%, they won't buy as much as some expect. They will buy a lot, don't be disappointed, but not those crazy numbers. I think it's roughly between $80 billion and $180 billion, probably closer to $150 billion.

This will come in two waves: the first wave on the 5th trading day. We start on the 12th, but June 19th is actually Juneteenth holiday, so markets are closed. That means next Friday is a holiday, so there's a big question mark whether the first Vanguard CRSP and FTSE Russell index fund buys will happen on Thursday, June 18th, or be delayed to Monday, June 22nd. I don't have a definitive answer for that one yet. But regardless, that's the first upward jump in the green line.

Then 10 days later, which happens to fall on the July 4th Independence Day weekend, so it will be after that weekend. That is, on July 7th, the Nasdaq 100 index inclusion part formally kicks in. Okay. During this entire period, as you can see, the blue line for early investors remains flat.

Then you see this red line, which is Grok interpreting what will actually happen to the free float, because obviously, those buying now won't want to turn around and sell immediately. So you can see, on the Nasdaq inclusion day, when the green line takes its second upward step, that red line is at its lowest point. What does this mean for the stock price? Grok predicted this brown line. Now you need to move up a bit more so we can see—it predicts the stock price will shoot straight up. The stock price is actually on the right.

Did we lose your picture, Alexandra? Can you not hear me? Oh no, I'm here, my mic is fine. Alexandra, did we lose you?

Alexandra:

Yes, I'm here, my microphone is working. Can you hear me?

Herbert:

Okay, you're back, you're back, thank you.

Alexandra:

Alright, sorry. So the brown line is the stock price, predicted by Grok. If you're not happy with it, complain to Grok, not to me or Aurelius. But it predicts the stock price will reach a peak; I think in this chart, it's between $275 and $300. That's more than double the $135 offering price. Well, not exactly double; $135 doubled is $270, and it's $275-$300, so it's more than double.

Grok thinks it will double sometime in July. July 4th? No, not July 4th; it's on the 15th trading day, which is July 7th, precisely when Nasdaq 100 starts to intervene. Okay, now everyone must be very, very careful. There will be some options traders, as smart as me or smarter, who will anticipate all this. But let's make an exception and pretend the market is rational and honest, okay?

So at that critical moment, as you see from that red dashed line, the actual free float is at its lowest, and the stock price prediction is at its highest.

Yes, then comes a day, which is the Q2 earnings call. Grok predicts that once the first wave of early investors unlocks, the stock price might drop. So you see that corner on the brown line. Let me clarify, it won't be a vertical drop; I actually believe the price will stay high and then fall off a cliff-like pattern, not this diagonal slope. But whatever, let's just look at the chart for now.

And obviously, the whole question is how many early investors will actually exit. We've already heard BlackRock wants to buy $5 billion to $10 billion.

You've already seen there isn't $5-$10 billion worth of ready stock lying around; if they start buying, it could push it even higher. We've also heard Ron Baron say, "I'm not selling; I'm actually going to buy more." They have some on hand, and he wants to buy another $1 billion. Right. So he is one of those early investors who could exit but doesn't want to. We've also heard Ark Invest (ARC) explain, yes, they will sell a bit because they are constrained by a single-stock 10% position limit, but they will also allocate SpaceX across more funds since now it's a publicly traded entity, it's more accessible to their other funds.

So the most complex part of this chart is: how much will early investors actually sell? So my first prediction is this one, which is my most realistic scenario, right? This is the data Grok input for the height of the blue line rise. You'll see there are two other scenarios that make it clearer. But as you can see, the moment the Q2 earnings call happens, which is the first rise of the blue line, the stock price should come down because that's two business days after the earnings call when they are unlocked to sell shares. We obviously don't know the exact earnings date yet. That will unlock them, enabling them to sell. So we might see as much as 30% of that tranche of fresh shares flooding the market.

Now, what is that tranche? As you know, about 50% of early investors is actually Elon. And Elon absolutely cannot sell for 366 days. So when you hear 20% to 30%, it's not 20%-30% of the whole; it's actually only 10% to 15% because half of that—Elon's half—can't be sold. Okay. Then I made the assumption that only a portion of that will sell.

Alexandra:

My assumption is that there will be an event before the Q2 earnings call: Elon must exercise the stock options from his 2018 Tesla compensation package. That's a $7 billion event. So everyone, don't feel pressured, but it will trigger a tax event in January 2028.

For all this, for how he nets or pledges or whatnot, the August 15th event and the January 2028 tax event—the higher Tesla's stock price is on or around August 15th, the better it is for him. Because he can do it any day before August 15th. This isn't small money; it's big money, okay?

So we have an event by August 15th at the latest, by which time the stock price should be at its highest; we have an event in the latter half of July when early investors can start to exit; and we have a peak on July 7th when Nasdaq 100 kicks in. Okay, are you still following me? I know this is completely insane.

Herbert:

So your guess is he will exercise his options here, or at some high point?

Alexandra:

Exactly. So my ideal scenario—the Goldilocks scenario—what do I know, don't take my word for it, this is not financial advice. But I'd love to share what I'm thinking: Between the July 7th Nasdaq inclusion and the earnings call (when these people can exit), they will announce a merger of equals, and Tesla will merge into whatever market cap SpaceX has at that point, because that's the peak in the whole scenario.

Okay. So as you know, I just bought these August options because I'm very strongly believing this. Again, I know nothing; this is just me trying to connect all these breadcrumbs, and I could be completely off track.

But this looks too engineered, too thought out. I mean, they went to the Nasdaq committee, FTSE committee, CRSP committee, S&P committee (though that S&P one didn't work out, whatever), and got them to change index rules. They structured these lockup expiration dates precisely in a certain way, then tied the earnings call into it.

I mean, you have certain dates; that's normal, and you want to stagger them slightly from the index times so the inclusion can work its effect. All that makes sense. But why tie the two major chunks of when early investors can exit to the earnings call? That's crazy.

I've never seen anything like it. Usually, these lockup structures are very simple: 180 days, then they can exit. This is someone who thought extremely deeply. So my question is, why did they think this way? Hmm, because they want SpaceX's price to go up. Why do they want SpaceX's price to go up? That's where my breadcrumb comes from.

Herbert:

Let me ask a question. So now, you've explained that from Friday until the July 4th—sorry, the Nasdaq inclusion day—there's absolutely no selling. Sorry, until the Q2 earnings day. When is the earnings call? When is the Q2 earnings call? I don't know; are we talking July 22nd or 28th?

Alexandra:

Well, could be July 22nd, 29th, both are Wednesdays.

Herbert:

Yes, Wednesday is traditionally when Tesla holds earnings calls. Will they hold a SpaceX earnings call? Because there's never been a SpaceX earnings call before, right? It was a private company. Your theory is, at that earnings call—because a few days after the earnings call, 30% of people unlock (not 30% of the whole, but the first unlock where shareholders can sell)—on that day, Elon might announce SpaceX's intent to acquire Tesla?

Alexandra:

Actually, I have two theories: One is they would do it on a Monday morning, which is very traditional for merger announcement press releases. My second theory, because it fits Elon's style so perfectly, I'm laughing before I even say it—is that he holds the earnings call, everything is serious, you know, talking about how many launches, how many contracts, how many AI customers, how many this and that, and then at the end he says, "Oh, and one more thing, we just filed an S-8 with the SEC, everyone can go check it out." I mean, that would be hilarious, right? If he actually did that, I don't know if I could breathe.

By the way, a side comment: someone said, "Oh, you bought options, and then Tesla dropped 5%." I bought my call options at $385. Beautiful, well done, perfect timing. Okay.

So, wow. This chart does not include this potential acquisition. It's just a straightforward analysis of when shareholder unlocks happen and when index inclusions happen. These inclusions are just these first two—three, because we know S&P probably won't happen until at least September this year or next January, June.

Alexandra:

Let me clarify. All three—FTSE, CRSP, and Nasdaq—complete their moves from June to early July (July 7th being the last). But this won't yet reach the full scale of SpaceX's market cap. You know, eventually, all these indices are market-cap weighted, but because there isn't enough free float, they can only do it by rebalancing in the next quarter, seeing where the market cap is then. That's why we have these staggered moments; new free-float shares will come in.

So, in September and December, Nasdaq, FTSE, and CRSP inclusions will happen again. We'll know those dates around early September and early December; I'll keep everyone updated. They might actually be larger than the initial one, entirely depending on how much free float exists by then.

As for S&P, S&P considered doing a 6-month inclusion instead of 12-month, but they ultimately didn't pass it. And I didn't even put that in this chart. They did include it in a small part of their overall market index, but not the S&P 500, 400, 600; those are another basket that uses the old rules. But in another basket, they are including it, so there will be some S&P demand too; I just don't know those dates yet, but they will also be early.

Then for the big one, S&P 500 inclusion—I mean, it has to get into the S&P 500 eventually; it will be a top 10 company.

There are two scenarios: If they merge, at the moment the merger is formally consummated—by the way, thanks to everyone who corrected me, you're right, I'm learning. So this date really refers to consummation, meaning regulators have reviewed, we've voted yes on everything, all green lights, and then comes the closing date. That will be the day the Tesla ticker disappears from the S&P 500 and the SpaceX ticker replaces it, or whatever the new entity is called.

That will be a massive buying day because suddenly, two market caps will be combined. All those S&P index funds that only had the Tesla portion in their funds now have to buy the SpaceX portion in one go. So that could be bigger than the 2020 event. We just don't know the timing. So it either happens at the moment of merger, or we're back to the headache with S&P—that is, when S&P deems SpaceX profitable enough for enough quarters and finishes all their machinations, meetings, etc., and finally includes it. So that could be anytime from mid to late 2027. But if a merger happens, the merger precedes everything.

Herbert:

You said this could happen in January, February, March 2027?

Alexandra:

Actually, the best-case scenario is Q1 2027; my most realistic prediction is Q2. In the first chart you showed, I wrote down all the regulators that must approve this, right. So there's an article with that chart at the top detailing how the merger would work. Point 6 there is HSR, SEC, and Department of Defense—they have to review. Well, you know, firewalls—has Tesla China been sufficiently firewalled from SpaceX's government contracts and other stuff? So it will be a bit of a headache. We don't know how many weeks that will take. But closing the deal, consummation of the deal, will be in the first half of 2027. I'm very confident and hopeful for the first three months; very possible in months four to six. Yes.

Herbert:

Okay, I see your logic. So July, you believe around the late-July SpaceX earnings call, at the latest maybe early August, they will announce the Tesla acquisition. The Tesla vote might happen in November, sometime around fall. Then it might close in Q1 next year. Once you do that, they'll be included in the S&P 500 anyway. So when you look at this table here, you know, the stock might drop because who knows what supports it, because all these unlocks are happening.

Alexandra:

Well, well, but by then we'll have Roadster 2, we'll have RoboTaxi.

Herbert:

Yes, let's clarify. That's why you can't view this as set in stone; this is just what Grok says based solely on unlocks and buying. But the reality is, if they announce an acquisition in July, by then Tesla milestones will help boost SpaceX stock, and vice versa. So you're saying RoboTaxi actually launches in August, you see Roadster announcement in September, you see those things, and then maybe the stock won't drop as much. That's exactly what you're implying, right?

Alexandra:

Absolutely correct. So there are many assumptions here: one is how much early investors will exit; but then comes the scenario of announcing a merger, which isn't plotted on this chart at all. In that case, the two stocks would walk in lock step. Meaning if SpaceX gets good news and rises 1% today, Tesla would automatically rise 1%. There are arbitrage funds in the market that do nothing but this arbitrage.

So what is their arbitrage theory? If the probability of regulators and Tesla shareholders approving this is so high that they start establishing the belief it will succeed, then it would be a perfect lock step. If they give it an 80% probability, there might be some wiggle room between the two, but still strong correlation. So actually, yes, my theory is that good news for one pulls the other up, yes.

Herbert:

Yes, the likelihood of shareholder meeting approval—the Tesla shareholder meeting approval is really key. We already did a big episode last week discussing what the actual deal terms would be. So, depending on what the deal terms are, we'll then know how likely Tesla shareholders are to approve it in November. You're saying, if SpaceX stock is at a $3 trillion market cap, SpaceX's market cap is $3 trillion, Tesla stock will rise to $3 trillion because it might be a merger of equals. Or, as Joe said, it could actually be they acquire Tesla at a premium to SpaceX's price, which is crazy, but that might just be to provide a sweetener to convince Tesla shareholders to vote yes.

Alexandra:

Okay. So why don't you take us through everything else we know about the SpaceX IPO? You've compiled all the key metrics.

Alexandra:

Give me a second, give me a second. I made two other, I think three charts; I just want to quickly show the impact of free float. Okay, let's go through this entire thing.

Okay, you can still see brown for stock price; this is still the same scenario, no merger, nothing, this is just, you know, SpaceX stock. In this scenario, it stays above $275 high and just goes up because no early investors exit. This is unrealistic, or only a negligible amount. People will sell; they won't sell all their holdings, they'll sell a small portion to make enough money because the gain is so significant. Say you were a welder, now you're a multi-millionaire; you wouldn't sell all your shares to cash out your millions, you might sell enough and say, "Hey, I have a few hundred thousand on hand," then keep the rest and let it grow because you believe it will continue rising.

Herbert:

Yes. And you know, many of these people will think, "I want my initial investment back." So they sell an amount equal to their initial investment back then, but that's only a tiny fraction of what they own now, right.

Alexandra:

Exactly. So this isn't entirely out of reality, but obviously unrealistic. Some people will definitely sell; I know ARC will sell; they've publicly said so due to their regulations, they have to.

Then the next chart is: What if everyone except Elon sells all their stock? Okay.

Herbert:

If everyone sells—if everyone sells all their stock, that's half, sorry, everyone sells exactly half.

Alexandra:

So you get the same peak, above $275, then you go a bit lower. The baseline scenario for the first chart is a bit more than half, right? So that's a bit more conservative than mine. All these charts are publicly available, so you can all study them.

Next is Scenario Three, please bring it up, Herbert. That's everyone sells all their stock. That's as unrealistic as the other. But you'll see, even in this scenario, the stock price doesn't drop below the IPO price. Okay. Now, can I guarantee it will never drop below? I have no clue. But these staggered index purchases (the green line below) do provide a nice floor each time they step in. Okay.

Again, this is engineered. This blue line is completely designed. The dates given aren't random; they're trying to achieve something here. You know, this ladder is someone's deep thought. Why? What do I know, but when you start plotting it, it makes sense.

Herbert:

Yes, the only thing I'd say is, this visual we're seeing here is only until the end of 2026, maybe the first part of January. SpaceX's real volatility—I was just talking to Joe Bacti about this—some say is after 2027. When you have all the commitments for SpaceX, you see Starlink milestones materializing, but you can't really show AI data centers as substantial revenue yet; potential space-based AI data centers might not be until late 2027 if you're lucky. So from that point on, it's still a story stock. Traditionally, some might, you know, like Tesla—you promised me all sorts of moonshots, literally moon shots, but, you know, people get tired; they wait for real revenue to materialize. That might happen then.

Alexandra:

Sure, sure. I mean, this is a very high-risk stock, just as Tesla was and still is a very high-risk stock. You're not investing in Alphabet, or even Nvidia to some degree; this is a stock with a higher beta. But you're saying, if everyone holding stock except Elon sells 100% in the first year, Grok estimates it drops to around $150, right. It still doesn't go below the IPO price; that's it. That's exactly what it's saying, and I find that very interesting. So let's go to the article. Yes, sorry, I interrupted you; what's this one?

Oh, so this is the three curves, with the earnings call cycle. Those are the pink ones. That's when they can sell the largest chunks, so it always happens two business days after the earnings call. That's where the stock price gets these corner notches. This is very important information for all shareholders: you must know when unlocks happen, and the major unlocks happen around earnings. We don't know exactly when they are yet, but you gave us a guide for when we expect them. I think it will be July 22nd.

Herbert:

Look, you're more precise than I am. I just got back from vacation; the day after I get back, we'll have a live stream the next morning. I'll be bleary-eyed. We'll do it like last time, right? You remember when you came back last time, we pulled you straight into the stream. My prediction is July 22nd, Wednesday. Okay, but we'll see.

Okay, so you've compiled all the key metrics about future expectations. By the way, I think SPCX is the ticker. When they actually merge with Tesla, we've already said if they do merge with Tesla, it's 100% certain. Your guess is SPCX disappears, TSLA disappears, and it will be replaced by X, that's your guess, right? And still available.

Alexandra:

You know, I'm sweating over this because I can't be called X Boomer Mama; I mean, that's not me. I don't want to put myself into X.

Herbert:

I was called Tesla Herbert for years, and when I switched to just Herbert, people hated it. So you should just—do you want to call yourself Ex Herbert? I mean, come on, that's sexy. Why not? Why not just Boomer Mama? You could do that.

Alexandra:

Yes, I think I'll try that. Yes, just Boomer. You better register it now. Okay, so SPCX price is $135, that's set in stone. It's already announced. $1.75 trillion is the market cap, issuing 555 million new Class A shares. I mean this number, right? I mean, with Elon, there's never a dull number; there's always some hidden meaning. Yes, what is this?

Herbert:

Oh, they can actually increase it if they decide to. So most likely, they won't stop at $7.5 billion; they'll go to $8.6 billion.

Alexandra:

Exactly, that's the underwriters' right (greenshoe right). They have 30 days to do it, which obviously would add to my free float scenarios. So that doesn't—

Herbert:

So if they think more people want to keep buying, it will increase from $7.5B to $8.6B. Sorry. Because currently, the estimate is that by this Friday's IPO, subscriptions are already oversubscribed by two times. That means there are twice as many people wanting to buy than the $7.5 billion worth of shares, so they say. So if they see that interest persists, they'll issue more shares. That wouldn't lower the price because you have buyers there, even though supply increases. Sorry. So it could reach up to $8.6 billion in issuance. That doesn't materially change my scenarios on the chart; we did run through it. I don't want—you know, nobody knows if the full greenshoe will be exercised. Very likely, you know, Elon tells them not to do it, whatever.

But I made a small table here. Now, first things that don't change: Class C shares are still all zero. These are non-voting shares; they might issue them to employees or use them when acquiring smaller companies and not want to give voting rights. So that's Class C, now ready for further acquisitions. Class B shares: 97% is Elon. So all that doesn't change. What gets diluted is Class A, right? One-to-one voting shares, not the others. So before IPO, it was 6.8 billion shares. If it's the minimum, 555 million, then it rises to 7.38 billion. If they do the full greenshoe, yes, greenshoe, then it might go up close to 7.5 billion. That's negligible, not huge, not many. Okay, just an extra 110 million shares. Yes, continue. Hmm.

So I think the number to remember is—because if my theory about the merger of equals is correct, you'll at some point see—understanding each company's market cap will be very important. Market cap is calculated from shares outstanding. So remember, SpaceX is around 13 billion shares, and Tesla shares then—because of this option exercise, Tesla after exercising options would be about 4 billion shares. One side 13 billion, the other 4 billion; if they walk in lock step, that will be the ratio.

Okay, key dates: So Thursday evening, once the market closes, they'll confirm the final price. I don't expect any number other than 135. They'll decide allocations, whether it's 555 million or maybe they already started the greenshoe; they'll announce all that after market close. So there will be an SEC announcement then.

Alexandra:

Is it true? I heard rumors, Alexandra, that Elon's unique demand for this specific IPO is that allocations are decided by SpaceX, not the bankers. Hmm. So some people—he's been yelling, that's for sure. Yes, he's telling the bankers, for instance, first, every retail investor who applies should get at least one share. If you asked, you'll get at least one or two shares; don't prioritize big shareholders. If you have huge funds, you don't necessarily get more than everyone; try to—we heard from Schwab, we heard some from Fidelity, remember Fidelity initially required $500k (threshold) in other accounts, now lowered to $2,000. So there's been some yelling happening; I think he's really explicitly saying he wants retail to get privilege—I mean, privilege as in being treated equally like everyone in this world.

Alexandra:

And, so the order is arranged that way. Does that mean bankers will execute? I doubt it, especially overseas ones. I mean, those guys usually think they're high and mighty, do as they please. So, I mean, I hope everyone who wants stock gets it, but I doubt it. Now especially Schwab, I don't trust them much. So Schwab still has a high limit, I think $100,000. But they pretend to favor smaller accounts compared to larger ones. Let's wait and see. I mean, for Schwab, my view is trust but verify; I just don't like it. Okay.

Okay, then the first trading day is Friday, June 12th. It starts in the morning, right? At 9:30 AM ET, 6:30 AM PT. No gap; I expect Elon to ring the bell. When does that bell-ringing happen? Well, at the 6:30 AM opening. Okay, 6:30, I'm just thinking if I should do a stream, and you said you're busy that day, right? Well, I mean, at 6:30 I could be there, then I have a call with ARC, then I'm on Bloomberg, and now it looks like I'm also on BBC, then I have clients. So, it'll be a busy day, but 6:30 will be busy for you.

Okay, we'll see what I end up doing at 6:30 in the morning. But, wow, watching Elon ring the bell, that's pretty cool. It's not his first time; he did it in 2010 too. Yes. Okay.

Options trading, what's this? So options trading, SpaceX options, some in the market pretend they'll be available immediately on Friday; I doubt that. So I went into a frenzy with my friend Grok researching. I looked at other large IPOs—I mean, there's never been an IPO this big. I do understand options traders want to make their money, but I also understand they want to protect their capital; if this price shoots up, you wouldn't want a lot of options exposure out there. So I think the best expectation is we won't have tradable options until Tuesday or Wednesday next week. Now what do I know; maybe there are some maniacs in the market who want to start pricing options on Friday; I doubt it, but suit yourself.

Okay, and you actually wrote the real dates here, thank you. Because that—yes, that's the data from the article pinned again, and below that article are Aurelius's charts. Those are the numbers; that's the explanation of when they come. Again, CRSP and FTSE might be Thursday, June 18th, or Monday, June 22nd, just because of the June 19th holiday. Then Nasdaq comes around the July 4th holiday, so that will be July 7th.

Then again, actually watch for those rebalances. These indices will keep us very busy over the next six months. And I gave, you know, how much assets they actually manage. CRSP is the biggest one; they're Vanguard. Now you also must know, Vanguard was an early investor in SpaceX; they already own a lot. So at one point, when I didn't know the lockup periods, I thought, okay, maybe Vanguard can sell to their funds so they don't have to buy in the open market, but they can't, right? We just learned they can't sell before the earnings call. So actually, CRSP must buy them in the market.

Then, FTSE Russell, that's London-based. There are many of them, but that's a larger index, so SpaceX's weight in it will be smaller. We'll see the numbers on the next slide in a second.

Herbert:

Yes, I'm surprised FTSE is actually the bigger one. Nasdaq isn't that small—that big. A quick aside, before we move on, because I forgot to ask you this. I'm told that if you buy at the IPO price, if you're a retail investor who bought SpaceX at the IPO price, there's a 60-day restriction before you can sell, you—so this?

Alexandra:

No, no. Fidelity imposes a two-week restriction because I think they're required to. Again, why? To protect the free float, right? They're always in the same scenario. But they can't really ban it. They're trying to say, don't sell within the first two weeks, or we'll never offer you an IPO again. But there will be some people who don't want the next IPO but still do it just because they want to make a quick buck, right? So, Fidelity is the only one I heard with a firm hold-two-weeks suggestion with consequences. Now those consequences, I mean, I doubt it can—what are they going to do—no, I'm talking about retail. Yes, I'm talking about retail; Fidelity is the only broker you heard having some restriction. Okay. Now I just saw a comment saying E-Trade does too. I don't know E-Trade's terms, but two weeks, I don't know. It says Fidelity is 15 days, so maybe 15 trading days, which would extend exactly to July 7th. Oh my God, I mean, everything culminates on July 7th. So I have a feeling they're trying to tell people they can't sell, but can they enforce it? I highly doubt it.

Now, again, again, I don't believe a retail investor wanting to make a quick buck would be stopped by Fidelity from selling their stock, right? If you're banned from future IPOs, maybe you want to take that risk, I don't know. But anyway, I mean, in my view, if you got this thing at 135, hold it, right? Don't be—it depends on each person's perspective.

Okay, let's move on to indices. Yes, I'm not sure we need to go through this entire thing because the initial chart already shows it all. If anyone wants to know all these details, it's in the pinned article. It shows the scale of necessary passive buying. It has different scenarios depending on where market cap goes. So if anyone is as number-crunchy as I am, they'll get immense joy from all this.

Herbert:

You could live on this. It's all different, different scenarios. The biggest takeaway is exactly that, which is the unlock moments. Okay. Unlock moments are what you want to watch if you're a SpaceX investor, but if you're a Tesla investor, you need to watch too because before that, I think things will happen. Yes, thank you for compiling it. So if you're planning to invest in SpaceX, you should go to Alexandra's X account; she has this pinned. I just skimmed through it quickly, but it contains lots of details, exact dates and rough numbers about when unlocks happen and when you get added—December 9th, all remaining shares eligible for early release are unlocked by then, except Elon's.

Alexandra:

Exactly. You know the discussion with S&P, which didn't pass, but was originally for a December 9th S&P inclusion. Can you believe it?

Herbert:

Oh, it was supposed to be perfectly timed; if S&P had agreed, it would have happened on December 9th, and that would have been when all shares would have already been sold out. So it's a perfect timing, like a—that's why things always make sense. I mean, who sat down to plan all this? It's insanely smart. Smart, smart, smart people.

But Cern made a suggestion. He said, "Okay, S&P came out a few days ago saying, 'We're not changing our rules; it's still 12 months,' meaning the next time you can include SpaceX in the S&P 500 is next June." Cern came out and said, "You know what, it's fine they say that today, but before then, they'll actually be forced to change and modify their rules. Because everyone will be buying SpaceX in other indices, and they'll start underperforming, then they'll say, we better include them." I agree, especially now with Anthropic and OpenAI. I mean, honestly, can you imagine? Because you know these aren't the last companies to IPO. Can you imagine the biggest index not representing—I mean, that's one thing, these three companies represent space.

Alexandra:

Exactly, absolutely correct. S&P sometimes talks about the S&P 1500 in their communications, so people came to me saying, "Yes, that's not the S&P 500 holdings." The S&P 1500 recombines three indices: S&P 500 (largest 500), then S&P 400 (next 400), then S&P 600. And a normal IPO does: a small company enters S&P 600 first, then it grows, grows, moves into 400, then grows, grows, moves into 500. Now we have these mega-caps that IPO directly at one trillion, or maybe two trillion, or maybe three trillion.

So S&P was never designed for that. S&P was designed for companies that, after going through all the rest, slowly grow into its top tier, the S&P 500. SpaceX would never appear in the 600 or 400; it would go straight into the top 10. So you can't just ignore these massive mega-caps because you have some rules written in stone and you additionally dislike Elon. You know, the market will demand it, or will say, "You know what I mean, you know I can live with the Nasdaq 100 because Nasdaq 100 is actually more tech-oriented and has all these OpenAI, Anthropic and has OpenAI, Anthropic and all those." They will move their money out of the S&P 500, and then S&P will be forced to say—this sounds exactly like a replay of the Delaware event. They made a statement on strategy, thinking they're so powerful, and then months later they realize, "Oops, we've hurt ourselves forever." Because we don't have—imagine OpenAI, Anthropic, and SpaceX not in your index. That's the most valuable companies everyone wants, right? Wow. I mean, even the US government is currently—

Herbert:

Exactly. But S&P, forgive me, is unwilling to touch because it could be volatile, right? So, even though they announced this, they might include it, and then it might be timed, who knows. And it could be—could you, could you just respond to this, because many say Elon is too evil, that he forced these indices to include SpaceX and they changed all the rules. That's not the reality at all, right?

Alexandra:

So, let me look at it from another angle. Suppose we were in a classic scenario where no index funds include anything for six months, and that would collide exactly with the traditional six-month lockup period, right? That would be a huge cliffhanger; you know, you'd have Nasdaq, FTSE, CRSP, everything all at once, all pressed on that mid-December date. Then all at once, early investors could all exit on day one, right? So instead of that, I think the idea was: Let's spread it out over time. That way it stabilizes; it achieves stability over multiple weeks.

Now, did they think about the merger announcement? I think so. Do I know anything for certain? I don't. But if you want to announce a merger ASAP (which I do believe is their intent), this staggered approach and this index inclusion to support the stock price is the smartest thing. Because meanwhile, I do believe there's a lot of good news coming. It starts just from Anthropic and Google on SpaceX's side. We know Tesla's pipelines have all that good news. So I just have a feeling this will actually reduce volatility and lift both stock prices.

Herbert:

So your theory about the announcement happening in late July is something only you are saying because it's too early for almost everyone else. But your—it's because of this chart, where you can see the highest possibility for SpaceX price—the highest possibility is actually in late July. Doing it then, versus, you know—these unlocks happen, and then the stock might get volatile then, makes sense. So you not only have three indices buying at the same time, with the lowest amount of shares available, the stock pops up, that's when you most likely would want to announce the Tesla acquisition.

Alexandra:

Exactly. Now I have a couple of questions. I see a comment asking, "If SpaceX has no cash, how can they acquire Tesla?" This wouldn't be a cash deal; it's a stock deal, stock for stock. That's why they have a 36 billion share authorized stock limit. Currently, as I showed, post-IPO they'll be at 13 billion shares, and then we'll see if there will be another 13 billion shares for Tesla.

Herbert:

Any other comments? You know, this is the most authoritative guide on future expectations. And I think every SpaceX shareholder, big whale, small retail, should watch these. And, you know, like this is made by Grok, so we don't know the stock price, but of course unlocks are pretty perfectly set in stone, index inclusions are set in stone. And then you can watch the percentages that will be released, and you can, you know, guess yourself from there what the stock will do. But those are—I want to respond to that question from Luke Jer: Why can't Tesla acquire SpaceX?

Alexandra:

Well, because of the way SpaceX's S-1 prospectus is set up in terms of governance, to maximize protection for Elon. So he has 10x voting power shares (Class B), and lawsuits must go through arbitration. And I mean, there are many provisions, including some I find a bit over the top, like if he passes away, his Class B shares go to his family. That's not quite to my taste, but anyway, the whole structure—the entire structure of the SpaceX company is designed to be ideal relative to everything that was never ideal inside Tesla. So there's no point in preserving the Tesla structure. The core idea is to give Elon this control and protect him from any activist investors and anything else, and that will happen inside SpaceX.

Herbert:

Yes, I think we've said several times, most of the MAG 7 companies are founder-controlled, founders have super-voting rights. So having SpaceX do this isn't—it's not evil; it's normal. In fact, Tesla is the outlier. Can you believe Elon even agreed to let Tesla be a company without giving him super-voting shares—you can—

Alexandra:

It's like this guy was really pure with his heart. But of course, it bit him in the back with lawsuits and all that. Okay.

Herbert:

So undoubtedly SpaceX would buy Tesla, but is there a possibility SpaceX would buy Tesla at twice SpaceX's price? That's a possibility, right? It doesn't have to be a merger of equals. Doesn't have to be today. Today Tesla's market cap is $1.5 trillion, right? Tesla. If I'm right, if Grok is right on his chart, SpaceX's market cap might at some point hit $3.5 trillion. Okay, let's say it's $3 trillion.

Alexandra:

Okay, say $3 trillion, then you have your one-to-two ratio.

Herbert:

Because now Tesla's stock price rises to the same level.

Alexandra:

No, no. So they would buy, if—if SpaceX is at $3 trillion, and Tesla is still at $1.5 trillion in late July. This—I honestly can't wrap my head around it because like we're about to IPO in a few days, SpaceX is moving forward. How can you go on vacation? I can't, I don't know. I'm going, I'm going; I'll be on vacation in July.

Herbert:

Next month is when the potential acquisition happens. So when they do it, let's say it's SpaceX at $3 trillion, and Tesla stuck at $1.3, $1.5 trillion, SpaceX would say, "I will acquire Tesla in a merger of equals at $3 trillion." And you think, your guess is Tesla stock would instantly jump from $1.5 trillion to $3 trillion, or rise all the way like that? So it's not about the number of shares; in a merger of equals, the number of shares is the same on both sides; the value of the shares would double.

Alexandra:

So if now, if they announce it in July, I will buy it on July 8th as a merger of equals; by November when they vote on it, Tesla shareholders would be voting on a—you know, would they want to go back below $400?

Herbert:

So you're saying, as long as Tesla stock doubles, that's very—that's a, that's a, that's a good premium, that's an excellent premium. And it's a premium paid by the market's non-sellers. I see. Because by that point, it will be a real merger; it will be Tesla stock that will double, and that's your guess. And that's why you're buying—again, this is you, because you normally don't do this, but you're just being transparent with everyone here. I haven't—you're being transparent with everyone here. You've bought because last time you bought options, you got burned, you lost that—I did poorly, I did poorly. You lost money. So don't trust, don't trust Alexandra. Okay, no financial advice, but I want to be transparent. I want to tell people what I'm doing because I don't want them to think I have any, you know, ulterior motives for saying this stuff. No, I'm putting my money where my belief is. So you bought options, guessing Tesla stock will jump in August, correct.

And you, but you didn't buy SpaceX because you believe Tesla stock will double anyway. No need to do that.

Alexandra:

That's correct. So what I did was, I closed the small position I had earlier in GUTS, remember I did that; it's a pharmaceutical company specifically for—yes, for the post-GLP-1 market. So I still believe in the whole concept, but I mean, obviously I don't see any upside; use that money to put it back into more, more Tesla. Now everything is in Tesla, 100%.

Okay, including now, actually it's over 100% because now I have these, these options. And, for me to buy the SpaceX IPO, aside from, you know, a footnote in history, would mean selling some Tesla. Because I'm 100% in; I don't have liquidity in any withdrawals anymore. Every time the stock drops, I buy as much as I can. So that's that. And that would trigger a tax event in specific accounts, and I'm not going to do that. Then once I figured that out, I thought even in non-tax accounts, no, I believe this, and I think actually the smarter play is to play the merger now.

Now the merger has a couple of hurdles; it might never be announced; I still believe it will, but who knows. Second, it might not pass the shareholder vote, right? The shareholder vote obviously depends on retail, but there are very, very many frustrated retail investors. Could you—could you share that, because I think it's very important for the audience to understand this. In the past, Tesla retail owned over 50% of the vote. So you, you know, you did a heroic job trying to make every retail investor aware there's a vote to cast. And it helped because, you know, we were fighting for Elon's comp package, and moving entirely to Texas was the most important thing. That all happened, and thank you for the work you did on that.

Today, I've been reporting all week, big whales, institutional investors were buying Tesla stock in Q1, the entire Q1. By the way, it's very interesting; it ties to 31%—retail now only owns 31%. Having said that, so for the November vote to happen, to make it actually win in favor of SpaceX buying—acquiring Tesla, you need to get the big whales. So you, but you believe—you count them in, you tell me: Vanguard, Ark Invest, Ron Baron, all these together.

And this I think is from your side: why did SpaceX choose to include in this war—include Charles Schwab, Morgan Stanley, J.P. Morgan? These three were the real jerks—what's the word? You're right, they were the biggest jerks. For Tesla, they voted against these things. Why would Elon allow them? Maybe SpaceX said, "Look, you do this, you better vote our way. Will you vote yes in our, in our interest now?" And they can't pass up the tens of billions they'll make on this IPO, so they say, "Sure." So that's why they included them. That's—are you willing to say that's how it is?

Alexandra:

Yes, that's my theory. I mean, will we ever know? Probably not. But, I mean, I've worked on Wall Street; they are mercenary, to the point they'd sell their own children if they had to, right? And, being one of the underwriters for SpaceX, or one of the distributors of SpaceX IPO shares, is the honor of a lifetime. It's also lucrative; it's both honor and honor and money, exactly. And, so, um, and do they want retail mad at them again? I mean, how many times have we shown, now we know you, Schwab, Schwab, right? We—the effort when that happened, we moved a lot of money, Tesla money out of Schwab, to the point they compromised and said, "Sorry, we'll vote."

Yes, yes. You know, I'm still waiting for August 31st. Because since last year's vote was in the second half, they're only included in the August 31st SEC filing. So August 31st we'll know how they actually voted last year. I mean, they said they voted yes, right? We'll, but we'll see on Schwab. For Schwab, I'm very, whatever. But we'll make sure between August and if there's this vote in November, everyone knows what Schwab is doing, whether they kept their promise or not. Okay.

But anyway, you're getting to the point; can you explain like you think, for Tesla shareholders to vote yes on an acquisition, you'll need to convince the big whales first, and then of course we still need to mobilize retail, but right now what's really more important are the big whales.

Let me run the numbers. So currently Elon owns 20%, but as I told you, there are options and his restricted shares. You need to get to 50% plus one vote of all shares in favor. And all shares will be 4 billion, so we need to reach 2 billion, okay. And Elon will be at over 700 million shares, so it'll actually be 17.5%. So the number to remember: we have Elon's 17.5%, so we still need 32.5%. I mean, ARC isn't that big anymore, Baron is sweet but not that big either. The big whales are Vanguard and BlackRock.

Now, Vanguard is not only in Tesla but also an early investor in BlackRock—in SpaceX. BlackRock wasn't before but has publicly stated they want $5-$10 billion at IPO. So they'll be in both too. So I do believe—and we've already seen, somewhere at Davos, Larry Fink there praising—praising Elon, BlackRock, yes. I think those relationships have been smoothed over, right? So, I think we can count on Vanguard and BlackRock.

So now we have about 17.5% and 15%, so we're around 32.5% level. Now plus Baron and whatever, we're around 35% level. Okay, now 35%, we need to get to 15—50%, right? We need another 15%. So how do we get 15%? Well, retail is 31%. If half of retail votes yes, we're done. Okay. But, but, but, yes, half of all retail must vote yes, not just those—you know, it's not a slam dunk; it's not a slam dunk. We'll have an extremely tough job. But, make sure you can vote, and make sure you vote yes.

And again, that's why I think the offer must be very attractive. It must be so attractive. I mean, we hear many Tesla retail saying, "I'm not voting." That's fair. Or, "I will, I will vote no." And not voting is effectively a no; abstaining in this case is a no. That's what I was trying to say earlier. If you don't vote, it's effectively a no vote. Yes, yes, make sure you vote.

Wow, okay. So we need—we have a massive job. We'll see, we'll see; we don't know. I'm not, I'm not saying I want a Tesla merger. We'll have to wait and see what the proposal is. If it's double, yes, I'd say okay; if it's triple, okay.

He just agreed, I'd do it. Yes, so for transparency, I do not own—at this moment I do not own any SpaceX stock. You do not own SpaceX stock at this moment. So people have been, you know, criticizing us or whatever, saying, "You guys are pumping SpaceX." I don't own any of this stock; I'm just reporting. I haven't decided if I'll do anything on Friday or, you know, today if we're going to do anything, you'd have to hurry.

And let me add a, let me add a risk factor. Because in that discussion with Joe Bacti, by the way, he traumatized me. You know, I think I'm actually a fairly decent debater; I'm obviously a woman, I interrupt, I'm more emotional. He interrupted you, sorry, I just did that. Well, anyway, I, I felt he beat me. But he also raised this idea about rigid or floor. Meaning, you know, once there's this offer, say at the $3 trillion level, then SpaceX must guarantee Tesla's price doesn't drop; the ratio is locked in.

I thought about this, I thought and thought, I thought and thought; it's completely contrary to my understanding of how markets work. I mean, has there ever been a merger announcement with a collar where the stock price at acquisition is between some price and another? Very possible. But I just don't think Elon thinks that way. Now again, as we just calculated, the offer must be attractive enough to Tesla retail to get them to vote yes, even to other institutions to get them to vote yes.

So, having said all that, I disagree with his strict floor or rigid. I don't believe that's how Elon would want to handle this. If SpaceX drops, Tesla drops. I mean, he sees it as one company. I think he already—did you catch that slip? When he was at that SpaceX IPO pitch. Yes. So, the truth is, you know, it's one. I don't think he'd say, "Okay, you know what, SpaceX investors, tough luck, you have to guarantee a floor for Tesla investors." I don't see that happening. I just want to throw that out because I felt when I discussed with Joe, I didn't have enough arguments. That thing traumatized me, I tell you; it's been a week I've been thinking, "I should have said more, better, calmer, more whatever." But here, I—

Herbert:

Well, I, I don't know why you say that. Because at the end of the day, you won that debate; he changed his mind, and he agreed with you. So, and he backed off—he was so strong on that idea before, his proposition was SpaceX would acquire Tesla at two times, maybe even three times SpaceX's market cap. And you, and you showed very well that, you know, outstanding market share count doesn't mean—or authorized shares don't in any way—you shared data to show that has any metric. So, and I thought he changed his mind, he backed off, and he, or he dialed back the strength of his conviction. So I, I thought you, you actually persuaded.

Alexandra:

Not a bad debater; I think I should take his class; he's a really good debater; he's a smart guy.

Herbert:

So you're smart, and we—the most important thing is the audience must decide for themselves, see what you think. But you have the data. Some of that data is precise, like very, very perfectly set in stone; and some is made by Grok, or guesses, assumptions. And you actually in your, in your post on X, you actually listed a whole table of assumptions. You said, "These are all the assumptions I made to arrive at this conclusion." So people should check her X account and have a look.

This is so exciting. I, I was so, so skeptical when you started saying Tesla will—SpaceX will announce Tesla acquisition in July; I kept saying, "Ah, August 15th, later, later, later, later." I couldn't establish in my head it would be earlier than that. Now you somewhat convinced me because you shared so many breadcrumbs kind of pointing to this being the case. So I'm getting excited for July. Somewhere between the 7th and 28th is my best guess currently, if it happens.

Alexandra:

If it happens somewhere between July 7th and 28th, I'll have to send you—I'll buy you something. I'll buy you something, nothing big; we're talking coffee.

Herbert:

We're talking a real crown.

Alexandra:

A real crown. We'll see.

Herbert:

Alright, folks. Thank you, everyone.