Author: Gallina, CryptoPulse Labs

At the end of April, the South Korean National Tax Service formally initiated preparatory work for taxation on virtual assets, with plans to implement it in January 2027 and prepare for comprehensive income tax declarations in May 2028.

This taxation covers income from the transfer and leasing of virtual assets, applying a 22% tax rate to annual gains exceeding 2.5 million won. It is expected to involve approximately 13.26 million people.

To this end, the National Tax Service plans to obtain data from domestic trading platforms such as Upbit, Bithumb, and Coinone and promote the launch of a comprehensive virtual asset analysis system to establish a complete taxation infrastructure.

South Korea's virtual asset taxation is transitioning from policy preparation to institutional enforcement, while simultaneously facing practical challenges regarding cooperation from trading platforms and regulatory coordination. This may serve as an important window for observing the global crypto market.

1. Preparations Before Tax Implementation: How the National Tax Service is Building the Virtual Asset System

The South Korean National Tax Service categorizes income from the transfer and leasing of virtual assets as "other income," setting a clear tax rate of 22%, with the aim of establishing a systematic and operational taxation mechanism.

Previously, virtual asset taxation experienced two postponements in 2022 and 2024, reflecting the difficulty in coordinating technology, law, and the market. The clarification of the target timeline this time indicates that the taxation infrastructure has entered its final preparatory stage.

The National Tax Service plans to acquire transaction data from major domestic exchanges while constructing a comprehensive virtual asset analysis system to promote cross-platform data integration. The launch of this system will enable tax authorities to monitor capital flows, track profit distribution, and provide data support for future tax declarations.

More importantly, this taxation plan will also rely on the OECD's CARF international information exchange agreement, sharing data on overseas investors starting next year to prevent capital flight and tax evasion.

By classifying virtual assets under the "other income" category rather than traditional capital gains, the South Korean tax system simplifies the collection process while laying the groundwork for future regulatory classification.

This move reflects the South Korean government's shift from fragmented regulation to institutionalized management in the digital asset field, aiming to establish a transparent and enforceable tax framework while balancing compliance and market stability.

2. The Tug-of-War Between Regulation and Crypto Platforms: Data Sharing and Compliance Challenges

During the implementation of taxation preparatory work, a delicate tension has emerged in the relationship between South Korean authorities and various trading platforms.

Recently, the South Korean Personal Information Protection Commission launched an investigation into Upbit and Bithumb, focusing on whether the two platforms shared order book data with overseas platforms without user consent.

These cross-border data transfers are primarily used to enhance trading liquidity but may violate relevant provisions of the Personal Information Protection Act. The investigation has completed written inquiries and on-site inspections, with results expected in the second half of 2026.

Previously, the two trading platforms have been subject to multiple reviews for inadequate fulfillment of anti-money laundering obligations or other compliance issues, with Bithumb even facing record fines for violations.

Similarly, recently, the South Korean crypto industry collectively opposed further tightening of anti-money laundering regulations.

According to Yonhap News Agency reports, the Digital Asset eXchange Alliance (DAXA), representing 27 registered Virtual Asset Service Providers (VASPs), submitted comments on the proposed amendment to the Enforcement Decree of the Specific Financial Information Act.

The new regulations require domestic VASPs to report as a Suspicious Transaction Report (STR) any virtual asset transfers to or from overseas VASPs, regardless of risk level, if the amount reaches 10 million won (approximately $6,800) or more.

While intended to strengthen anti-money laundering monitoring, the requirement for "non-discriminatory reporting of large cross-border transfers" may lead to a disconnect between regulatory objectives and the industry's practical operational capabilities.

DAXA pointed out that the rule, ignoring transaction risk levels, reduces the value of AI risk control systems invested in by exchanges, such as Upbit's abnormal transaction detection, to mere formality, degrading intelligent compliance to mechanical reporting.

Furthermore, the new regulation would cause the annual report volume of South Korea's five major trading platforms—Upbit, Bithumb, Coinone, Korbit, and Gopax—to surge from about 63,000 cases last year to over 5.4 million cases, an 85-fold increase, posing extreme operational difficulties.

The industry also opposes the proposed additional requirement to verify the accuracy of customer information, viewing it as imposing obligations not clearly stipulated by law.

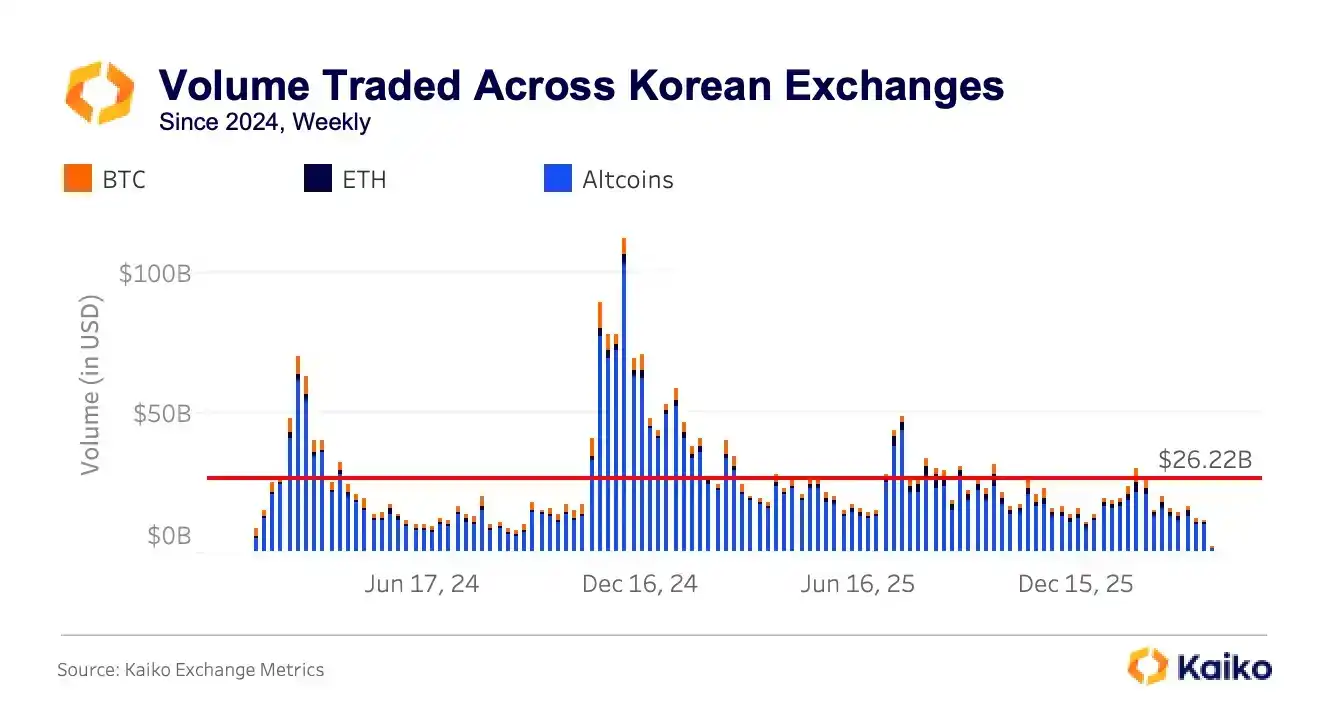

The highly localized nature of the South Korean virtual asset market is also noteworthy, with its trading volume accounting for 30% of the global total, altcoins comprising up to 85%, while the proportion of Bitcoin and Ethereum is relatively low. The main market participants are retail investors, exhibiting obvious speculative characteristics.

This structure places continuous pressure on trading platforms to balance maintaining liquidity and fulfilling compliance obligations. The friction between regulatory demands and platform business objectives, to some extent, reflects the unique investor behavior and institutional environment of the South Korean market.

3. Capital Flows and Price Volatility: Potential Transmission of Tax Policy

The advancement of virtual asset taxation in South Korea has a direct impact on its domestic market. Taxation will regulate investor behavior, making taxes transparent and potentially curbing short-term speculative activities.

Simultaneously, relying on cross-border information exchange agreements, the space for capital flight is limited, promoting greater stability in the local market order. Tax policy will also influence exchange operating strategies, forcing platforms to adjust between ensuring liquidity and compliance.

From a global perspective, while the South Korean market has a large trading volume, its high proportion of altcoins and relatively insufficient market depth mean its price volatility has a significant spillover effect on global markets.

After tax implementation, market funds may be redistributed. Trading enthusiasm for high-volatility assets domestically may decline, affecting international investors' participation strategies in Asian markets.

South Korea's regulatory model and information-sharing experience can serve as a reference for other countries, potentially influencing the global virtual asset taxation and compliance system.

The clear timeline and technical infrastructure construction for this taxation also provide institutional expectations for international capital, offering clearer references for the global market regarding price discovery, liquidity risks, and investment strategies in the South Korean market.

Especially in the areas of cross-border capital management and personal information protection, South Korea's practices may become reference cases for other jurisdictions when formulating policies.

Conclusion

The initiation of virtual asset taxation by the South Korean National Tax Service marks a critical step from policy deliberation to institutionalized management. Although friction exists between domestic trading platforms and regulatory agencies, the construction of tax and data infrastructure helps standardize the market and control capital flows.

The highly speculative nature and cross-border transaction characteristics of the South Korean market mean its taxation practice will not only affect the domestic ecosystem but may also serve as a reference for global cryptocurrency regulation and tax models. Observing market reactions after the final tax implementation will aid in understanding the trends and challenges in the global virtual asset market's institutionalization process.