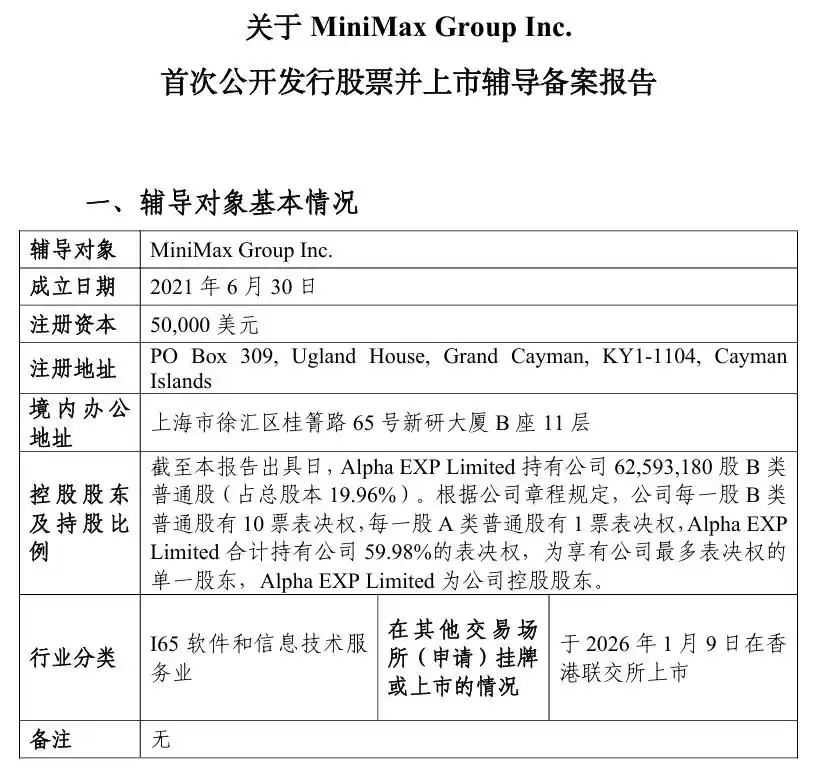

Zhidongxi May 30 report, as shown on the CSRC official website, Shanghai AI large model leader MiniMax submitted an IPO tutoring filing report to the Shanghai Securities Regulatory Bureau on May 29, initiating its A-share listing process, with CITIC Securities serving as the tutoring institution.

This also means that MiniMax, together with Zhipu AI which has also submitted its A-share IPO tutoring filing, will sprint to become the first large model stock on the A-share market.

MiniMax was established in January 2022 and completed its Hong Kong IPO in January this year. After the Hong Kong IPO, MiniMax's stock price skyrocketed. As of the Hong Kong market close on May 29, its stock price was HK$840 (approximately RMB 725.24), up 409.09% compared to the issue price of HK$165 (approximately RMB 142.46), with a market capitalization of HK$263.454 billion (approximately RMB 227.545 billion). Starting from June 8 this year, MiniMax will also be included in the Hang Seng Tech Index.

Behind the surging stock price, there is fundamental business performance as support.

On May 28, MiniMax disclosed some business data. Over the past two months, MiniMax's ARR (Annualized Recurring Revenue) achieved growth exceeding 100%. The number of global enterprise and developer customers served has exceeded one million, a fivefold increase compared to six months ago; its global user base is approximately 300 million.

In March this year, MiniMax released its first annual report after listing. During the earnings call, founder and CEO Yan Junjie revealed that the company's ARR had reached USD 150 million by February 2026.

That is to say, combined with the over 100% growth in the past two months, MiniMax's current ARR has exceeded USD 300 million.

For the full year 2025, MiniMax achieved revenue of USD 79.038 million (approximately RMB 535 million), of which revenue from AI-native products was USD 53.075 million (approximately RMB 359 million), and revenue from the open platform and other AI-based enterprise services was USD 25.963 million (approximately RMB 177 million).

Its gross profit margin improved to 25.4%, with an adjusted net loss of USD 250 million (approximately RMB 1.69 billion), and the loss ratio narrowed significantly year-on-year.

▲ Part of MiniMax's 2025 Financial Data

Regarding products, since the beginning of this year, MiniMax has successively launched three flagship large language models: MiniMax-M2.5, MiniMax-M2.6, and MiniMax-M2.7, and open-sourced the M2.5 and M2.7 models.

▲ Some open-sourced models from MiniMax (Source: ModelScope)

Thanks to its high cost-performance ratio, MiniMax-M2.5 gained popularity among many developers during the "Lobster Craze" (the open-source AI Agent framework OpenClaw) earlier this year and was even recommended by "Lobster Father" Peter Steinberger in a post.

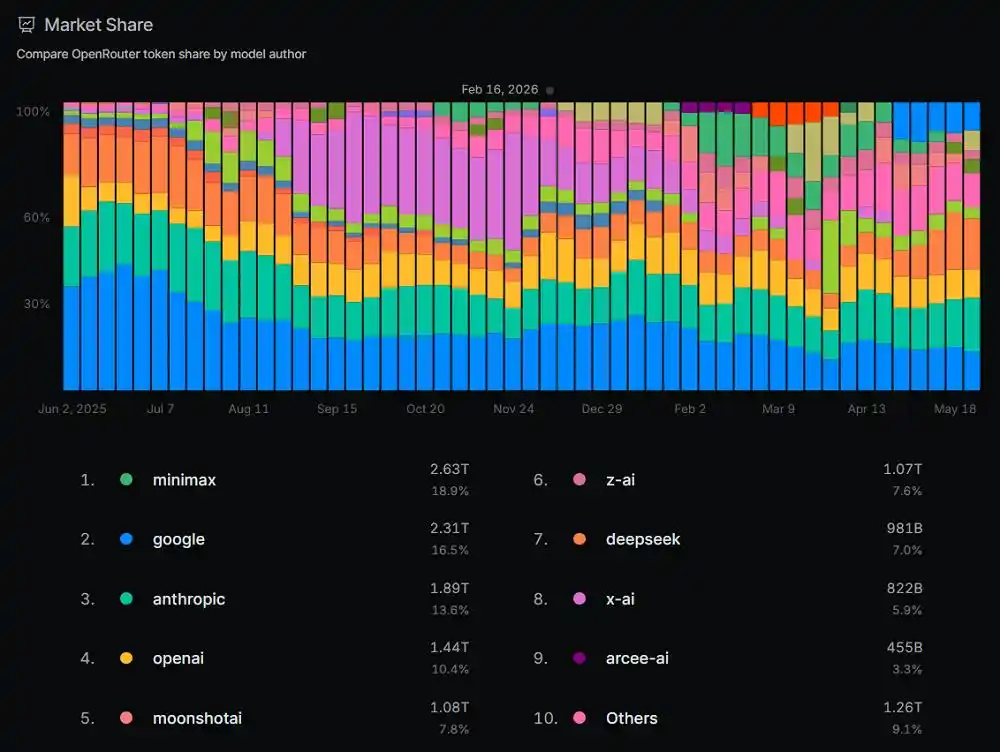

In mid-February this year, on the AI model aggregation routing platform OpenRouter, MiniMax once became the model vendor with the highest market share, capturing 18.9% of model calls on OpenRouter. However, MiniMax has currently fallen out of the top 10 of this list.

▲ OpenRouter Model Vendor Ranking in mid-February this year (Source: OpenRouter)

Additionally, in May this year, MiniMax upgraded its Agent product and renamed it Mavis, providing a multi-Agent parallel working mode, which can be used to improve the completion rate of complex long tasks.

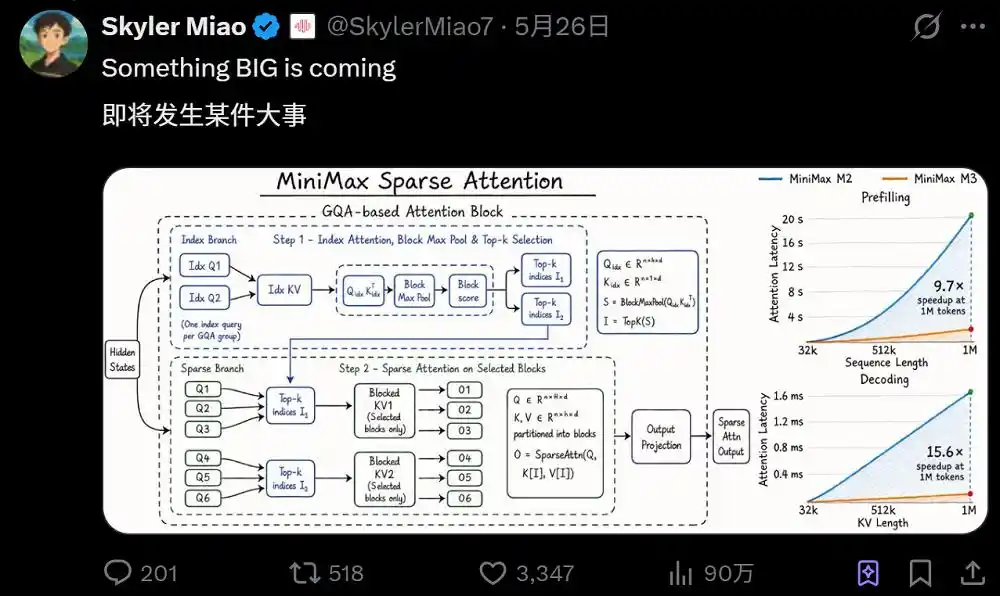

At the end of May, the MiniMax official account hinted that MiniMax-M3 is即将发布.

▲ MiniMax official account teases M3 model (Source: X platform @MiniMax_AI)

MiniMax Engineering Head Skyler Miao revealed more technical details about MiniMax-M3. MiniMax-M3 adopts the MiniMax Sparse Attention mechanism. Compared to MiniMax M2, in the Prefilling stage, MiniMax-M3's inference speed when processing 1 million tokens increased to 9.7 times faster; in the Decoding stage, when the KV length reaches 1 million, the speed increased to 15.6 times faster, effectively reducing attention latency.

The MiniMax Sparse Attention mechanism is based on the GQA (Grouped Query Attention) architecture. First, through the Index Branch, it uses compressed index queries (Idx Q) and keys (Idx KV) to calculate block scores and perform max pooling, selecting the Top-k block indices most relevant to the current query. Subsequently, it enters the Sparse Branch, performing sparse attention calculations only on these selected key blocks, thereby significantly reducing computational load.

▲ Technical details of MiniMax Sparse Attention (Source: X platform @SkylerMiao7)

Conclusion: China's Leading Large Model Players Rush for Listing

Entering 2026, the moves of China's leading large model companies in the capital market have been accelerating. Besides MiniMax, Zhipu AI submitted its A-share IPO tutoring filing in April 2025 but later completed its IPO in Hong Kong first. In February this year, Zhipu withdrew its previous A-share IPO tutoring filing and registered for a new one, adding Guotai Haitong as a tutoring institution.

Furthermore, Moonshot AI, Stepfun, and 01.ai have also reportedly planned Hong Kong IPOs.

Facing high computing power investments and a not yet fully closed commercialization path, leading large model players are opening up more diverse financing channels through listings.

This article is from the WeChat public account "Zhidongxi" (ID: zhidxcom), author: Chen Junda