Since late February 2025, tensions in the Middle East have escalated sharply. The United States and Israel launched large-scale airstrikes against Iran, sending shockwaves through global financial markets.

During that war-torn weekend, while traditional financial markets were closed and Wall Street traders could only wait for Monday's opening in anxiety, another wave of investors was trading frantically on on-chain platforms.

They weren't trading cryptocurrencies; they were trading gold, crude oil, and silver.

Prediction markets like Polymarket and Kalshi saw trading volumes surge due to war-related contracts, becoming the focus of market attention.

But on the other side of the lens, Perp DEXs, including Hyperliquid, were also "profiting handsomely from the war": trading volumes for commodity contracts on these platforms soared, and on-chain derivatives for traditional assets like gold, crude oil, and silver experienced an unprecedented liquidity explosion.

The War Dividend for Prediction Markets

Before delving into Perp DEXs, it's necessary to first review the performance of prediction markets during this geopolitical crisis. After all, it was the impressive data from Polymarket and Kalshi that made people truly feel for the first time that the era of "betting on anything" has arrived.

According to data from Dune Analytics, for the week ending March 1, 2025, traders wagered a whopping $425.4 million on geopolitical issues on Polymarket, far exceeding the $163.9 million from the previous week. The platform's total trading volume reached a record $2.4 billion, a significant increase from the previous week's $1.8 billion. Kalshi also performed well, with its contract on "Whether Khamenei will step down" attracting over $54.5 million in trading volume.

Behind these numbers is the strong stimulation of users' trading欲望 (desire to trade) by a globally known event like war. When missiles streaked across Tehran's night sky, when Trump announced on social media that "Khamenei is dead," the price curves on prediction markets reflected the "truth" faster than any news release.

But it's important to clarify that "profiting from the war" here is not meant pejoratively. Prediction markets provide an unprecedented way for people to express their judgment on major events with real money. As Kalshi CEO Tarek Mansour said, the essence of these platforms is to "make uncertainty priceable," and war simply pushes this pricing demand to the extreme.

"Crazy Saturday" on Hyperliquid

Prediction markets are undoubtedly the role directly benefiting from the war in the Web3 space, but another slightly "outdated"赛道 (sector) also opened the door to a new world because of this conflict.

On March 1st, the second day after the US-Iran war officially started, the Iranian side admitted that morning that Supreme Leader Khamenei had been killed in the war. That day, the cryptocurrency market briefly fell before quickly recovering, with Bitcoin's intraday fluctuation slightly exceeding 7%, a reaction not considered particularly drastic.

It happened to be a weekend, and most people's focus was still on cryptocurrencies because, in their eyes, cryptocurrency was the only "commodity" that could be traded without restrictions on weekends. But in fact, this has long not been the case.

Bloomberg reported on March 1st that on the first day of the war, Saturday, the price of oil perpetual contracts on Hyperliquid rose about 5% to $70.6 per barrel, while gold and silver perpetual contract prices rose about 1.3% and 2% to $5,323 and $94.9 per ounce, respectively. Silver futures trading volume exceeded $227 million within 24 hours, and gold futures trading volume was about $173 million.

The perpetual contract markets for gold, silver, and crude oil were already launched on Hyperliquid's largest HIP-3 market, trade.xyz, in late 2025 and early 2026.

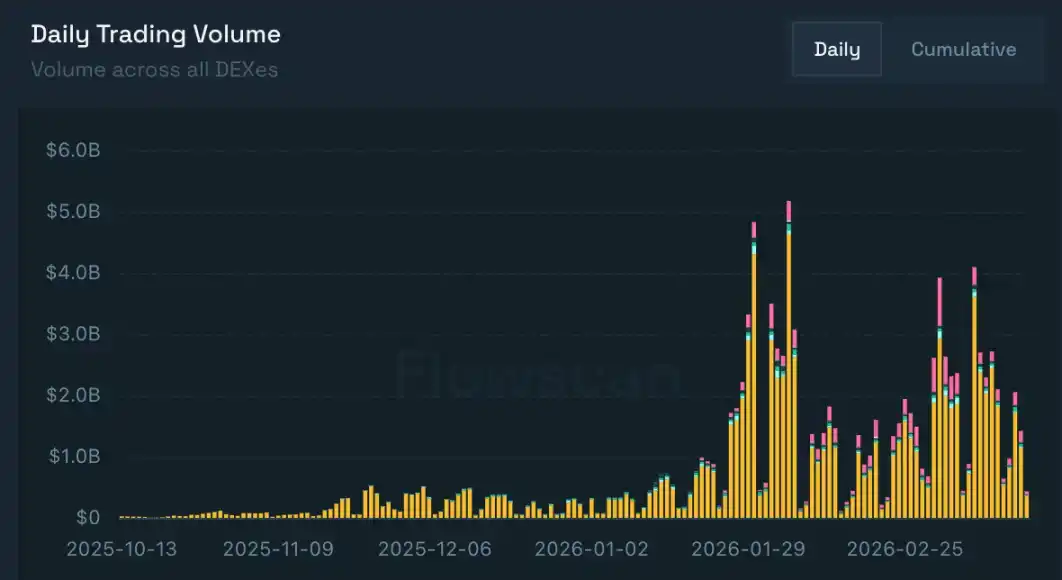

Furthermore, February 28th was not the peak of daily trading volume. On January 29th, when silver hit a historic high of $120/oz, the daily trading volume of silver contracts on Hyperliquid exceeded $1.2 billion. On February 5th, this number was刷新 (refreshed) to over $3.5 billion, accounting for 68% of the total trading volume of the HIP-3 RWA market that day.

Crude oil, newly arrived on the on-chain market, also performed impressively.

Before the conflict broke out, the average daily trading volume of crude oil contracts on Hyperliquid was only around $20 million. After the war broke out, as oil prices kept rising, the daily trading volume of crude oil contracts on Hyperliquid quickly broke through $100 million. On March 9th, this number reached nearly $2 billion, second only to the trading volume of Bitcoin contracts on the platform and far surpassing Ethereum.

According to data from Flowscan, on March 8th, the trading volume of Hyperliquid's HIP-3 market exceeded $880 million, setting a historical record for weekend trading volume. Just a week later, this number was刷新 (refreshed) again to nearly $966 million.

The ample weekend liquidity not only provided investors with a place where "money never sleeps" but also brought a better pricing mechanism to traditional financial markets. The managing partner of Arete.xyz stated on X that this is the first time decentralized platforms have achieved price discovery for traditional assets.

If this continues to develop, traders won't need to scramble frantically after Monday opens. Perhaps they already completed their trades on Hyperliquid over the weekend, or perhaps the opening price will be very fair, with little arbitrage opportunity.

Of course, it's not just on-chain platforms eyeing this lucrative piece.

Who's Watching Closely?

Major exchanges also smelled the opportunity early.

Well-known exchanges like Binance, OKX, Bitget, etc., have long listed RWA tokenized assets. OKX listed gold perpetual contracts as early as last May, while Binance and Bitget did so in December last year.

Exchanges might not have taken these assets seriously in the past because their volatility was low, with "investment" outweighing "trading" attributes, not worthy of attention. But with Trump first capturing Maduro and then decapitating Khamenei, the volatility of大宗资产 (bulk assets) like gold, silver, and crude oil rivals that of former altcoins, while现在的山寨币 (current altcoins) have long since躺下装死 (laid down playing dead).

Cryptocurrencies can't seem to rise, traditional financial markets party every day, anyone would be envious seeing this. Cryptocurrency exchanges are inherently never closed, the listed大宗资产 (bulk asset) markets also have no settlement, just like trading "air" like altcoins, one more doesn't matter.

Not just cryptocurrency exchanges, the holy temples of global quality assets: Nasdaq and NYSE are also unwilling to give up pricing power for commodities.

As early as last year, the rivals Nasdaq and NYSE hinted to the market that they were not only researching security tokenization but also wanted to support 7x24 trading. But obviously, it's not easy for traditional institutions to take this step. Rules that have lasted for a hundred years, if they want to change, the entire upstream and downstream need to change simultaneously: who will make the market? Who will clear? Can T+0 be achieved? These are all issues on the table.

The specific details are still hidden under the table. But just this month, Nasdaq announced a cooperation with xStocks, a subsidiary of the US-based cryptocurrency exchange Kraken, while NYSE's parent company ICE officially announced an investment in OKX at a $25 billion valuation. Clearly, they don't want to拱手让人 (surrender) the territory they've conquered; the arrow is already on the string, waiting for the order to launch.

On the second weekend of March, Bloomberg again reported Hyperliquid's commodity trading data. This kind of reporting twice in a short period made many sensitive people feel the change: a platform that makes money from data and information began paying attention to on-chain exchanges and used the trading prices of commodities on them as a reference. But this also raises another question: why did the leading cryptocurrency exchanges get an early start but didn't attract as much attention as Hyperliquid?

Taking the silver perpetual contract as an example, on March 9th, the trading volume of the XAGUSDT contract on Binance was $6.464 billion, while on Hyperliquid it was over $3.5 billion. Although numerically, Hyperliquid's trading volume in this single market was only 54% of Binance's, Binance has over 300 million users, while Hyperliquid's total user count is only接近 (close to) 1.7 million.

Winner Takes All

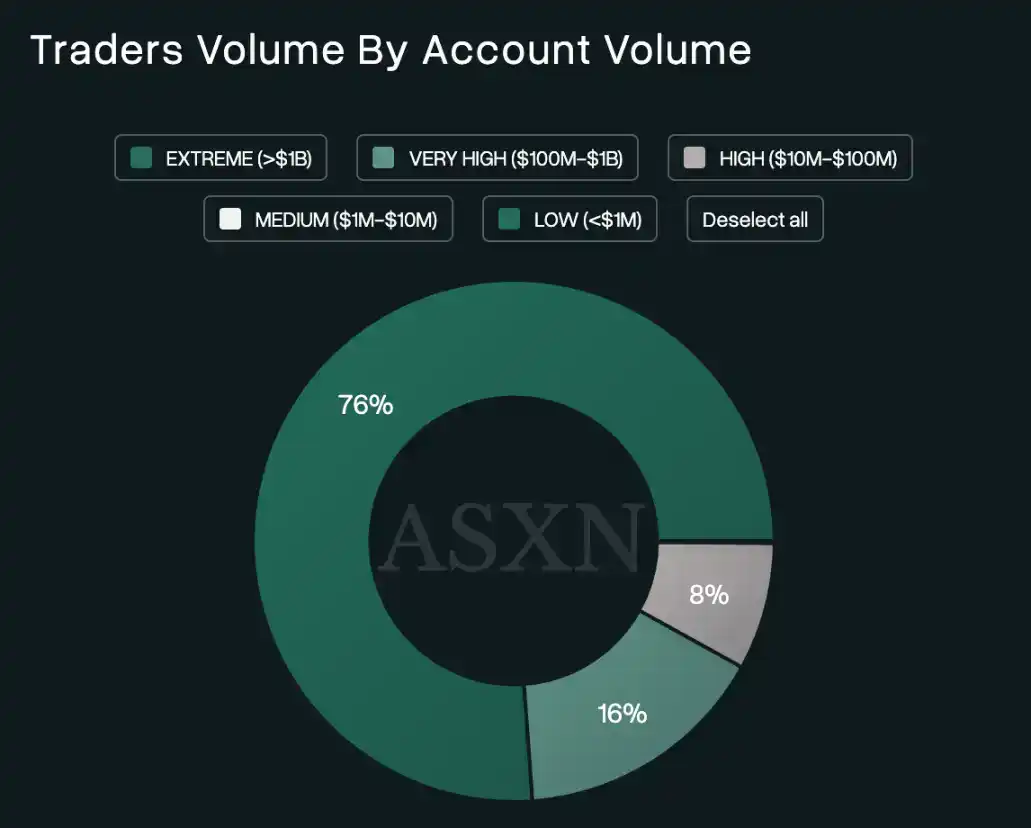

According to statistics from crypto asset researcher ASXN, Hyperliquid's total trading volume exceeded $8 trillion (other data shows $4 trillion, possibly ASXN double-counted the volume of both trading parties). Accounts with trading volumes exceeding $1 billion accounted for 76% of the total volume, and accounts with trading volumes between $100 million and $1 billion accounted for 16%.

There are no specific market maker accounts on Hyperliquid; some accounts with trading volumes reaching hundreds of billions of dollars should likely be controlled by market makers. But even so, the 76% ratio is enough to prove that most users trading on Hyperliquid are actually whale investors. Although the overall volume might not match CEXs, the price traded by whales with real money indeed has more reference value.

But this still doesn't answer why the market consistently chooses and favors perp DEXs. The author once compiled the views of Chinese users on perp DEXs in the article "Choosing Perp DEX is a Rebellion of 'The World is Tired of Qin's Tyranny for Too Long'". Not many people said CEXs did poorly; more turned to DEXs out of profit-seeking or airdrop farming needs.

But for foreigners, it's a different story.

The founder of Equation News, the genius 00s trader Vida, once shared some insights on Telegram to explain why foreigners are疯狂看好 (crazy bullish on) Hyperliquid. According to a screenshot provided by X user JinMu, Vida attributed the reasons to strict KYC and the糟糕的用户体验 (poor user experience) of US-based exchanges.

Several investment institutions within the Web3 industry have also told the author that high-net-worth investors and family offices in China with large funds have relatively low trust in crypto. Even Li Lin, the founder of Huobi, holds Bitcoin positions indirectly through BlackRock's IBIT in his Hong Kong family office. In contrast, large funds or high-net-worth individuals abroad have a higher acceptance of crypto, and many traditional financial institutions are testing Web3 products.

No wonder Bloomberg started paying frequent attention to Hyperliquid in March, as the whale users on the platform might include some traditional financial institutions找不到流动性 (unable to find liquidity) on weekends.

As for CEXs, no matter how high the trading volume, you never know who is actually trading. From the single dimension of "reference value," they确实比不上 (really can't compare to) DEXs. Additionally, DEX's self-custody, transparent trading, and unrestricted leverage also provide fertile ground for financial traders to发挥 freely (play freely).

"Such an unregulated platform will eventually be taken down by regulators."

I believe this is a sentiment many have seen recently. Listing new assets without review,不问来源 (not asking the source) of funds, uniform leverage for all—these are indeed behaviors dancing on regulatory red lines. But this might be a platform默许存在于 (tacitly allowed to exist in) a gray area. Just like TikTok, the government can shut it down on grounds of "national security," but the American people won't agree, and the stakeholders and officials hoping to profit from it won't agree either.

In the future, when certain international events affect the prices of metals, grains, raw materials, etc., Hyperliquid can still replicate the miracle of gold and crude oil. The author believes that regulation will not target Hyperliquid in the short term.

The当年的 (former) "Golden Triangle" region, which was unregulated, was eliminated not entirely because of the harm of drugs themselves, but perhaps because someone wanted to make this money themselves. The fact that S&P Dow Jones Indices authorized Hyperliquid, rather than any CEX, to launch the S&P 500 index perpetual contract is the best proof.

The same logic applies to Hyperliquid and other perp DEXs. As long as they don't touch certain core interests, they have value in existing.

Pricing "Uncertainty"

While HIP-3 is in full swing, HIP-4 is also quietly gaining momentum.

Launched on the testnet on February 2, 2026, HIP-4 introduced the "Outcome Trading" function, a type of fully collateralized contract that settles within a fixed price range, specifically designed for prediction markets and option-like products.

Unlike Hyperliquid's core perpetual contracts, HIP-4 outcome contracts have an expiration date, require no leverage, have no liquidation risk, and settle within a predefined price range. For example, if you believe Bitcoin will break through $80,000 by the end of March, you can buy the corresponding outcome contract. At expiration, if Bitcoin确实超过 (indeed exceeds) $80k, the contract settles at the upper limit for profit; if not, it settles at the lower limit, with losses limited to the initial investment.

The market普遍将 (generally interprets) HIP-4 as "Hyperliquid entering the prediction market," but this might underestimate its strategic significance. The true value of HIP-4 lies in expanding Hyperliquid from a pure derivatives trading platform to a more comprehensive "uncertainty pricing platform."

Doesn't Polymarket price uncertainty? Not really. Prediction markets display更多的是概率 (more of probability). When you believe an event has an 80% chance of happening, but the amount you intend to invest would directly pull the probability to 99%, you would naturally choose to reduce the funds.

Outcome contracts, however, can reveal risk appetite through the amount of capital. Taking the example of whether Bitcoin will break $80k by the end of March, many on Polymarket might choose "no," but on Hyperliquid, you might see many people buying call options. This means that although many are indeed bearish, they are not that pessimistic, or these investors believe they need to hedge against a possible rise.

If Bitcoin真的 (really) rises to $80k by the end of March, waiting until 79,000 and watching the probability on Polymarket rise from 20% to 80% is too late.

Furthermore, HIP-4 complements Hyperliquid's existing perpetual contracts. Traders can seamlessly switch between linear derivatives (perpetual contracts) and non-linear derivatives (outcome contracts) under the same account and margin system, building more precise and efficient investment portfolios. This "composability" is Hyperliquid's advantage over specialized prediction market platforms.

Money Never Sleeps

We are witnessing the era where "money never sleeps" becomes reality.

On one hand, prediction markets, a sector treading the edge of gambling, allow events with deterministic outcomes to be wagered on with money; on the other hand, on-chain exchanges allow ample liquidity to price unexpected events even on holidays when markets are traditionally closed.

The arbitrage space created by information asymmetry has become the survival foundation of a "platform." The boundaries of platforms will continuously expand. Now暂时被限制 (temporarily restricted) to Earth; ten or twenty years later, you might be able to trade lunar minerals on a spaceship heading to Mars.

We are pleased to see finance, a product invented by humans, advance further with the加持 (empowerment) of blockchain, but we must also remind:

My life is finite, but knowledge is infinite. To pursue the infinite with the finite is perilous! (吾生也有涯,而知也无涯。以有涯随无涯,殆已!)