Author: Gu Yu, ChainCatcher

For a long time, Paradigm has been an iconic venture capital firm in the crypto industry, representing the top-tier investment style and aesthetic, with its research-driven crypto VC approach highly praised. However, affected by the industry's cyclical downturn, Paradigm has not been immune to the current widespread VC slump. One manifestation is an unprecedented wave of executive departures, with at least seven employees leaving since April this year, including several partners.

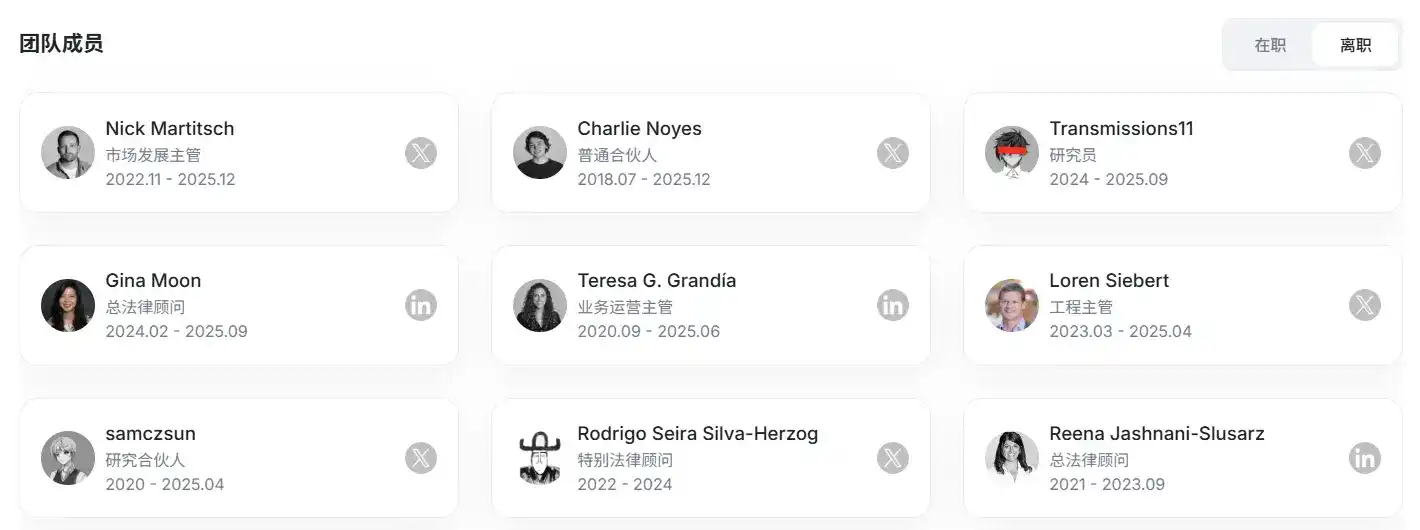

In December, Charlie Noyes, Paradigm's first employee and general partner, and Nick Martitsch, Head of Market Development at Paradigm, announced their departures successively.

In September, Gina Moon, General Counsel at Paradigm, and researcher Transmissions11 left.

In June, Teresa G. Grandía, Head of Business Operations at Paradigm, departed.

In April, Loren Siebert, Head of Engineering at Paradigm, and research partner samczsun left successively.

Source: RootData

Such a wave of departures is extremely rare among first-tier VCs, reflecting that Paradigm is in a rather difficult phase. Judging from its public portfolio and transaction frequency, Paradigm's investment pace has significantly slowed over the past two to three years, lacking industry-consensus "masterpiece" investments and missing out on many high-return projects, which are likely the main sources of Paradigm's predicament.

Frequently Taking Over Late Rounds, Missing Star Projects

Paradigm's golden era roughly spanned 2019 to 2021. During this period, it completed investments in key projects like Uniswap, Optimism, Lido, and Flashbots, thereby establishing a strong brand identity: technical infrastructure, Ethereum core ecosystem, long-termism, which also earned Paradigm considerable reputation within crypto entrepreneur and investor circles.

These typical investments shared several common features: they were not short-term trends but rather underlying protocols or critical middleware; the investment timing was relatively early but not extremely so; and they were highly aligned with Paradigm's internal research directions.

It was during this phase that Paradigm formed its clear and repeatedly emphasized investment strategy: research-driven. However, the problem is that this methodology gradually revealed its lack of adaptability in subsequent cycles, facing rapid changes in industry logic, leading to a noticeable gap between Paradigm's investment performance and its influence.

Starting in 2022, the new generation of high-growth projects began to emerge more in areas like the application layer, financial structure innovation, mechanism design, and product experience, such as prediction markets, yield structuring protocols, and perpetual contract protocols. This wave of projects often iterated quickly, were more product-oriented, tolerated higher levels of "technical correctness," and were more sensitive to "user growth" and "mechanism efficiency."

In the last cycle, Paradigm notably supported and invested in the hit projects Blur and Friend.tech, becoming one of the main drivers behind their popularity. However, both projects declined rapidly after token launches, with teams dumping large amounts of tokens and becoming inactive, leading the market to question Paradigm's investment acumen and style.

Simultaneously, Paradigm also took over later-stage financing rounds for many high-valuation projects. While this strategy had been profitable during the bull market, due to the continued slump in the altcoin market and issues with the invested projects themselves, Paradigm's heavily invested projects almost all fell below their cost price quickly after token launches or faced poor development and sought transformations.

In May 2024, Paradigm led a $150 million Series A round for Farcaster at a $1 billion valuation. Farcaster has now announced abandoning the social track to pivot to the wallet space.

In May 2024, Paradigm led a $70 million round for Babylon at an $800 million valuation. Babylon's token FDV is now only $180 million.

In April 2024, Paradigm led a $225 million round for Monad at a $3 billion valuation. Monad's token FDV is now only $1.7 billion.

In June 2022, Paradigm participated in a $130 million round for Magic Eden at a $1.6 billion valuation. Magic Eden's token FDV is now only $200 million.

More difficult for Paradigm to accept is that it also missed early investments in many high-return projects in recent years, such as Ethena, Pump.fun, Ondo Finance, MYX, etc. In the hot derivatives and RWA sectors, Paradigm has not invested in any projects in recent years.

Regarding the prediction market sector, which has been highly favored by the capital market in the crypto industry these past few years, Paradigm invested in the prediction market project Veil as early as January 2019, but the project ceased operations less than a year later.

The prediction market model is not novel in theory, and the technical difficulty is not top-tier. The failed investment experience led to Paradigm not participating in any of the first five funding rounds of Polymarket. Perhaps it wasn't until Polymarket announced a $150 million funding round at a $1.2 billion valuation in January this year that Paradigm realized the value of this sector,转而开始 heavily betting on Polymarket's competitor Kalshi. It first led an $185 million round for Kalshi at a $2 billion valuation in June this year, then participated in two subsequent rounds within six months at valuations of $5 billion and $11 billion respectively. This is also the highest valuation project Paradigm has invested in historically.

This shows that Paradigm is determined not to miss core investment targets in the hottest sectors, even to the point of having a "FOMO" (fear of missing out) mentality.

Stalled Incubation

Deep involvement in project incubation has long been a signature style of Paradigm, with Uniswap and Flashbots being representative cases from previous cycles.

In a previously published article, the firm stated that Paradigm is a group of developers aimed at supporting other developers. The most fruitful collaborations often involve deep cooperation with startup teams to solve important business and research challenges together.

For a VC, joining a project at the conceptual stage allows for better influence on product design and strategic direction, thereby unlocking greater value potential and achieving higher bargaining power and returns on investment.

With several success cases, Paradigm continued to explore the incubation model in recent years and even introduced an institutionalized EIR (Entrepreneurs-in-Residence) model, where both parties work together in the same office, with the VC providing substantive support in strategy, technology, recruitment, etc. However, judging from recent cases, this model has also hit a wall for Paradigm.

In December 2023, Paradigm co-developed the on-chain developer platform Shadow through the EIR mechanism and invested $9 million, but the project ceased development this year, with the founding team转而 launching Ventuals, a platform for derivatives on unlisted company equity.

The decentralized fixed-rate protocol Yield Protocol, in which Paradigm previously participated in writing the whitepaper, development, and investment, also announced it was ceasing operations in October 2023.

Subsequently, Paradigm shifted its focus to the infrastructure track. In October 2024, crypto VC firm Paradigm announced a $20 million investment in its spin-off company Ithaca. Ithaca is developing a new Layer 2 blockchain called Odyssey, with Paradigm's CTO and General Partner Georgios Konstantopoulos serving as CEO of Ithaca while retaining his position at Paradigm. Paradigm co-founder Matt Huang serves as Chairman of Ithaca.

This team structure shows that Ithaca is entirely developed by Paradigm's core team, with deeper involvement than previous projects like Uniswap. Choosing the Layer 2 sector at this time点, in hindsight, was not a wise choice. In the following year, Ithaca had almost no significant developments in the market.

Earlier this year, the crypto industry's trend completely towards stablecoins and the payments sector, and Paradigm once again "followed the trend," jointly launching Tempo, a high-performance Layer 1 public chain for payment scenarios, with internet payment giant Stripe in August this year. Paradigm co-founder Matt Huang serves as CEO of the project. In October, Tempo acquired Ithaca, with all members of the latter joining Tempo.

By this time, the payments sector already had powerhouse projects like Arc, RedotPay, Plasma, Stable, 1Money, and BVNK making efforts. Tempo holds a leading position in terms of funding amount and has the resource support of Stripe, giving it a relatively leading position in the fierce competition.

The battle for payments with Tempo will become a decisive campaign for Paradigm to prove its product and research capabilities once again.

Conclusion

Whether Paradigm will find its rhythm again remains to be seen. But one thing is certain: it is at a position where change is necessary.

Since January this year, Paradigm's investment frequency has increased significantly, from an average of 1 deal per month in 2023-2024 to an average of 2 deals per month, with a明显 increase in the proportion of early-stage investments. In June last year, Paradigm also announced the completion of an $850 million fund raise, remaining one of the VCs with the largest cash reserves today.

Team turnover and setbacks in investment strategy are not unique to any single VC but are inevitable challenges almost all long-term institutions face during cross-cycle development. If the past Paradigm represented the "engineer era" of the crypto industry, then what it must face next is perhaps a stage that is more pragmatic and more results-oriented. The success or failure of this adjustment will also determine whether it can continue to play the role of a definer rather than a bystander in the next cycle.