Author: Eric, Foresight News

Original Title: Paradigm Invested in a Brazilian Stablecoin Company, But Why Brazil?

Recently, the Brazilian stablecoin company Crown completed a $13.5 million Series A funding round led by Paradigm at a valuation of $90 million. The Block's press release explicitly highlighted that this is Paradigm's first investment in a Brazilian company. This funding round also marks Crown's second round of financing within two months. In mid-October, Crown had just completed an $8.1 million seed round led by Framework Ventures, with participation from Coinbase Ventures, Paxos, and others.

This might not be front-page headline news, but there are two points in the article worth noting: Why Crown? And why Brazil?

Why is Crown Worth Investing In?

Analyzing something usually requires considering both internal and external factors.

In terms of external factors, the author believes that investment opportunities in U.S.-based stablecoin issuers are becoming increasingly scarce. Tether and Circle already dominate the vast majority of the market, forcing investment institutions to look outside for greater alpha if they want to find larger opportunities. Furthermore, there are not many targets that both allow foreign capital to invest in companies related to their national fiat currency *and* have a domestic market for stablecoins.

Brazil is a rare 'treasure land' in the Americas that meets most of these conditions. We'll discuss why later.

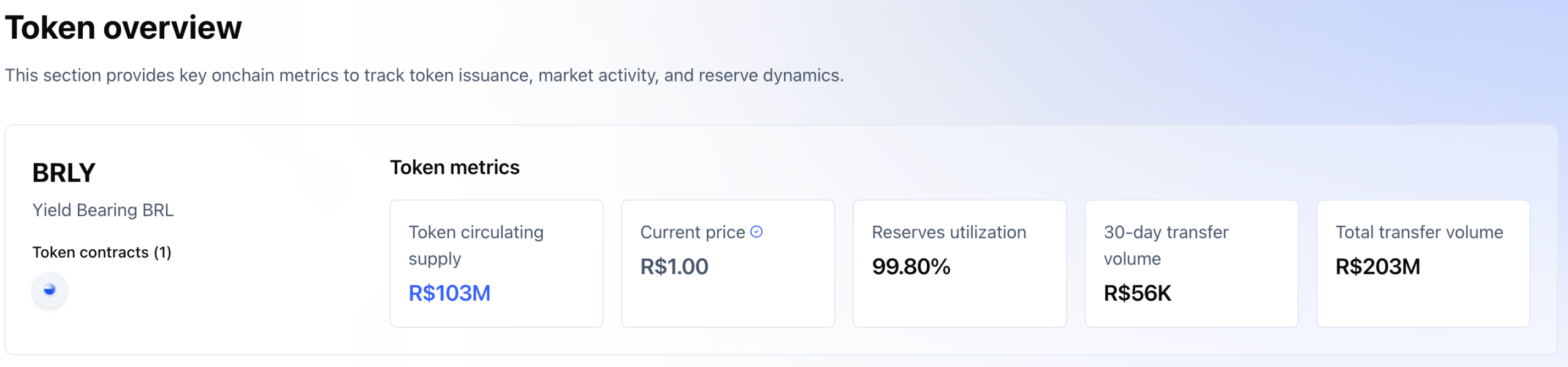

First, back to Crown. According to disclosed data, the total supply of BRLV, the Real (Brazilian fiat)-backed stablecoin issued by Crown, is currently just over 100 million tokens, which translates to a value of less than $20 million USD. Its trading volume over the past 30 days is only $56,000. This shows that the market for domestic currency stablecoins in Brazil is not large yet, especially since Crown currently only serves institutional clients.

Clearly, the logic behind investing in Crown is betting that the team behind it can achieve success in this market in the future.

Crown's co-founder and CEO, John Delaney, was formerly a lawyer in international finance and also the COO of Xerpa, a prominent local Brazilian company that received investment from Founders Fund. In 2019, Xerpa launched an "Earned Wage Access" platform, allowing employees to withdraw their earned wages for days already worked at any time (instead of waiting for the end of the month), helping them avoid high-interest credit. This was particularly popular in Brazil's high-interest rate and financially stressful environment, seen as a tool for employee financial well-being. The company charges a small fixed fee, not involving interest.

Co-founder and Chief Engineer Vinicius Correa was an early engineer at the Brazilian digital bank Nubank. Nubank's investor list is also impressive. In multiple funding rounds totaling $2 billion, participating institutions included Sequoia Capital, Tiger Global, Goldman Sachs, Founders Fund, Tencent, and Berkshire Hathaway. Nubank IPO'd on the NYSE in 2021 with a valuation of $41.5 billion and currently has a market cap of nearly $80 billion.

Founding Partner and Ecosystem Lead Alex Gorra previously served as Managing Partner at the family office Brainvest, which manages $5 billion in assets, and had prior management roles at ARX Investments, UBS, Rothschild Bank, and J.P. Morgan. COO Bruno "BL" Passos previously led cross-functional teams at Hashdex.

Crown's founding team can be described as a veritable all-star team. Both founders have also been involved in the process of building Brazilian local businesses from 0 to 1. Although BRLV's current data is not impressive, it hasn't prevented them from raising over $20 million in total within two months.

Furthermore, the Crown team stated in a blog post that the essence of launching BRLV was also seeing the contribution USDT and USDC made by purchasing government bonds. Issuing stablecoins locally in Brazil can similarly provide purchasing power for government bonds, thereby stabilizing the economy, which in turn further stimulates the use of stablecoins. This is a win-win situation. If dollar stablecoins just help the US "extend its lifespan," then the Real stablecoin can be said to concretely help the country.

Why Bet on Brazil?

In terms of the underlying fiat currency for the stablecoin, there seem to be many choices than the Brazilian Real. So why Brazil?

You might not believe it, but this country, which many born in the 80s and 90s might last have heard of due to football, has become one of the largest and leading innovation hubs in Latin America, with over 1,500 fintech companies and more than 100 million users.

As a capitalist country, Brazil's banking sector has long been dominated by five major banks (Itaú, Banco do Brasil, Bradesco, Caixa, Santander), which account for over 80% of assets, far higher than the US (~50%). Traditional banking services were rigid, expensive (credit card APRs often exceeded 300%), and bureaucratic, excluding tens of millions of low- and middle-income individuals and the unbanked (historically up to 55 million) from the system.

But this also created a huge demand gap. Fintech companies like Nubank切入 (entered the market) with no-fee credit cards, offering simple, low-cost services, quickly filling the market void.

The Brazilian Central Bank, although unable to change the monopoly of traditional banking, surprisingly actively promoted competition and inclusion, even becoming a classic case in global digital financial regulation. Its biggest contribution was launching the instant payment system Pix in 2020. Pix supports free and 24/7 real-time transfers. In 2025, transaction volume exceeded one trillion Reais, with user coverage exceeding 90% of the population. Upon its launch, Pix quickly replaced cash and credit cards, becoming the preferred payment method for 76% of Brazilians, significantly improving financial inclusion and providing low-cost infrastructure for Fintech (such as payment and credit innovations integrated with Pix).

I believe everyone often sees integrations of Pix by various exchanges or Crypto payment tools in Web3 industry news. It is indeed not easy for the central bank of a capitalist country to主导 (lead) the launch of a payment system powerful enough to shake the original banking system. But this "pro-people" direction has also given local fintech companies better development prospects because they can reach more users.

Precisely because of this, the acceptance of new financial forms like cryptocurrency is very high in Brazil. Brazil's population exceeds 200 million, smartphone penetration rate is nearly 90%, internet users exceed 180 million, and average daily online time exceeds 5 hours. Young, digital natives, especially Gen Z, have a strong demand for mobile finance. Last September, Circle directly began supporting the direct exchange of Reais for USDC.

The popularity of dollar stablecoins in Brazil has been analyzed in many articles as being due to the instability of the country's own currency. But according to the author's research from multiple sources, even if this is part of the reason, it only accounts for a very small portion. It seems now that if this reason held true, investment institutions like Paradigm would not place such heavy bets on Brazil's domestic fiat stablecoins and fintech companies.

In fact, Brazil did experience multiple episodes of hyperinflation in the 1980s and 1990s, even reaching extreme monthly inflation rates of 80%. But in recent years, although the Real's volatility is still not small, for a country like Brazil, it has achieved good results in stabilizing the currency value and reducing inflation. Brazil's inflation rate hovered between 4.5% and 5% in 2025. Although still above the central bank's target, it is good enough compared to neighboring Argentina.

Some local Brazilian residents holding dollar stablecoins indeed do so to hedge against the depreciation of the Real, especially against the backdrop of the Fed's interest rate hikes in previous years. But actually, more do so for practical purposes such as foreign trade, tax avoidance, facilitating capital flow, and trading cryptocurrencies.

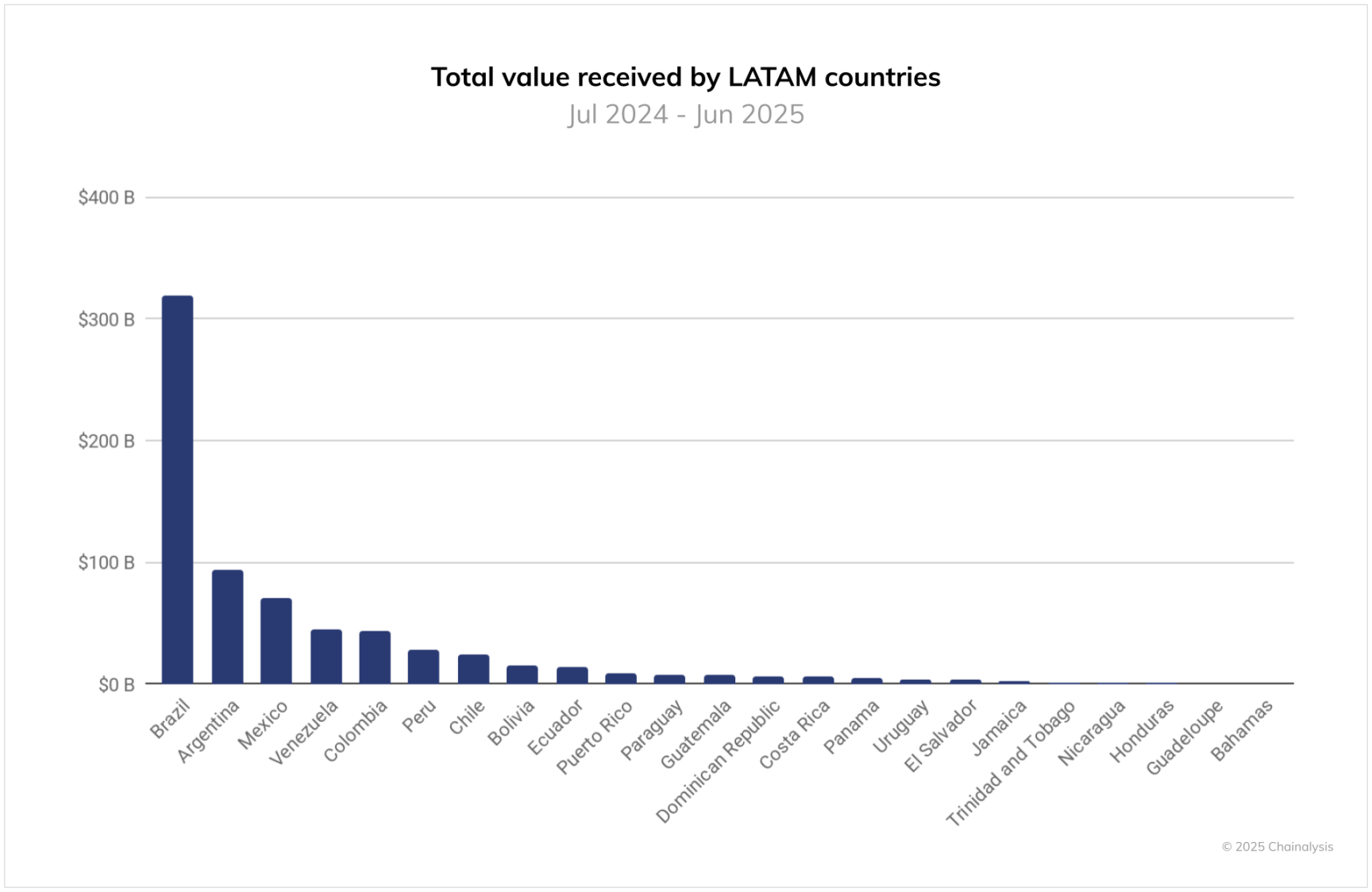

According to Chainalysis data, Brazil's cryptocurrency adoption index ranks fifth globally, behind only the US, India, Pakistan, and Vietnam. Its cryptocurrency inflow volume from July 2024 to July 2025 reached $318.8 billion, far surpassing other Latin American countries.

Furthermore, according to data provided by cryptocurrency market maker Gravity Team, Brazil has already adopted stablecoins as a tool for investment and cross-border payments. Stablecoins currently account for about 70% of indirect fund flows from local Brazilian exchanges to international exchanges.

At this point, some might ask, since they already have a national payment tool like Pix, what is the significance of stablecoins?

BRLV, launched by Crown, has a feature not explicitly stated on its official website but mentioned in the press release: it shares the interest income from government bonds with stablecoin holders. And in Brazil, that number is 15%. Although it's impossible to distribute all of it to holders, even half is a very attractive yield.

In the future, BRLV could also be integrated into the Pix system. For ordinary people or even the poor, there might be no motivation to exchange for stablecoins. But for those with ample funds, stablecoins not only do not affect payments but even simply holding them allows one to "earn interest." In the future, they could also be seamlessly traded with dollar stablecoins, and even participate in DeFi. In short, all sorts of possibilities will certainly create sufficient demand and scenarios for stablecoins in this land.

In most countries with weaker national strength, unable to maintain long-term stability of their currency and with scarce foreign exchange reserves, the US dollar and dollar stablecoins are a lifeline for the people. Brazil is precisely an exception among them.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush