Author: RoboRhythms

Compiled by: Deep Tide TechFlow

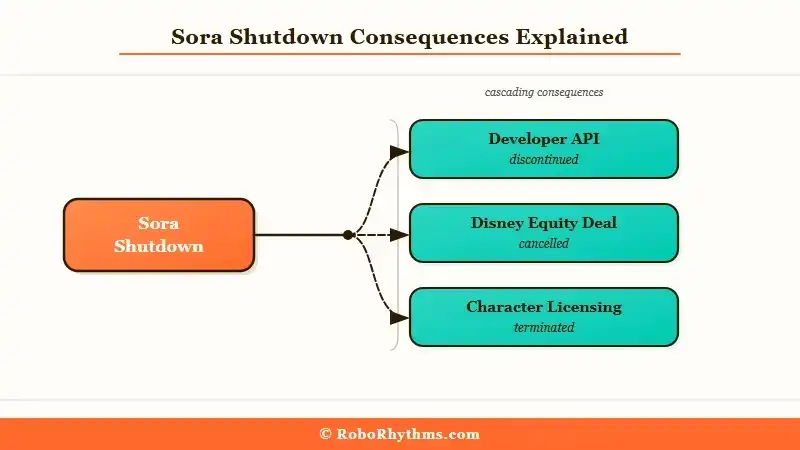

Deep Tide Guide: On March 24, 2026, OpenAI shut down Sora's App, API, and domain all at once. Disney's three-year licensing agreement and $1 billion investment subsequently collapsed.

The first reaction from the tech community was not regret, but "Did anyone actually use this thing?"—this statement speaks volumes more than any official announcement. Runway, Kling, and Google Veo are now the only real players left in the AI video space.

Full Text Below:

The product that was supposed to bring AI video generation to the masses has disappeared. OpenAI shut down Sora on March 24, 2026, taking down the standalone App, API, and sora.com, just about six months after the product's high-profile public release.

The timing is awkward. Disney signed a three-year licensing agreement in December 2025, authorizing OpenAI to use iconic characters like Mickey Mouse and Cinderella for Sora-generated content, and planned to invest $1 billion in OpenAI.

All of this is now canceled.

I think the most telling thing is the reaction from the tech community: the mainstream sentiment wasn't regret, but "Did anyone actually use this thing?" This statement reveals the product's actual trajectory more truthfully than any official announcement.

If you were using Sora or planning to build a product based on its API, here's what you need to know.

What Exactly Happened

Sora's shutdown is a complete product termination, covering the App, developer API, and the sora.com domain.

OpenAI confirmed on March 24 that the entire Sora product line would be completely shut down. This is not a pivot, a rebrand, or a merger into another product.

The App is gone, the API is being shut down, sora.com is being taken offline.

Here is everything that was terminated:

- Sora consumer App (text-to-video)

- Sora API (developer and enterprise access)

- sora.com website

Disney's planned $1 billion equity investment in OpenAI

The three-year character licensing agreement with Disney announced in December 2025

The Disney angle is not a footnote. A $1 billion deal collapsing within three months of its announcement suggests the relationship had already become complicated before the shutdown was officially announced.

Both Variety and Bloomberg confirmed that the deal was directly called off due to Sora's cessation of operations.

Only one part of Sora remains: the internal research team continues to advance what OpenAI calls "world simulation" research, aimed at robotics applications.

This project has nothing to do with the video product you might have used. OpenAI explicitly positions this as infrastructure research, not a future consumer product.

This also aligns with a pattern I've reported on before. OpenAI has a history of terminating products that no longer fit its revenue roadmap, and the timing—ahead of a planned IPO—follows the same logic.

Why This Is More Serious Than It Sounds

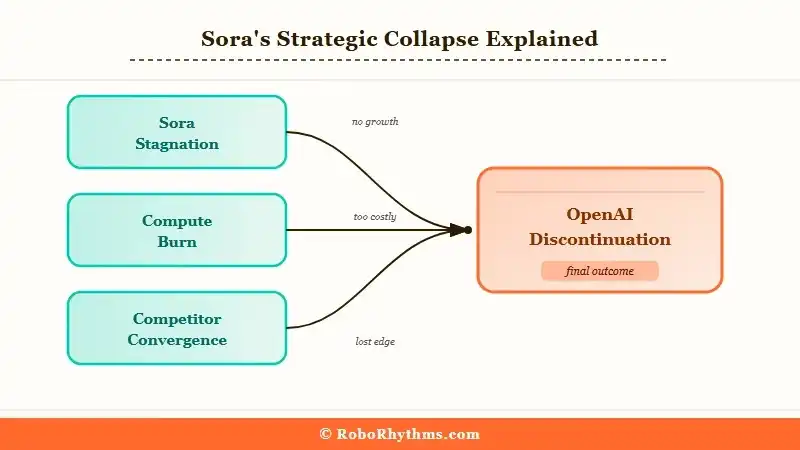

Sora's shutdown isn't just a product failure; it's OpenAI publicly conceding an entire AI category to the competitors it once looked down upon at its launch.

When Sora first debuted in 2024, the demos were stunning. Posts on r/singularity garnered hundreds of thousands of views, with a widespread belief that OpenAI had once again leapfrogged all competitors overnight.

Runway, Pika, and Kling were supposed to become irrelevant.

But the product stalled after its public launch. Runway Gen-4 kept iterating and shipping, Kuaishou's Kling 3.0 closed the quality gap faster than most analysts expected.

Google Veo's compute advantages were something OpenAI couldn't easily match in this non-core revenue赛道 (market).

Compute cost is the most staggering number. Analysts estimate Sora's compute cost peaked at around $15 million per day during peak usage.

For a company focused on pre-IPO financials, this was an extremely difficult expense to justify when the models that actually drive revenue (GPT-5 series, Operator API, enterprise contracts) all require more investment.

Then there was the deepfake issue. TechCrunch, in its shutdown report, called Sora "the most disturbing app on your phone," referring to the cameo feature that allowed users to insert real people into AI-generated scenes.

The backlash from this feature was significant, and in my view, the reputational drag made the shutdown decision easier than it otherwise might have been.

The industry impact is now clear: Runway, Kling, and Google Veo are the true players in AI video. The strategic uncertainty that OpenAI's presence created for every competitor has now been removed.

What This Means For You

If you were using Sora or accessing its API, you need to act immediately. The shutdown timeline is effective now.

The three tools currently best positioned to absorb Sora's former user base:

Runway Gen-4—Technically closest to Sora's cinematic quality goals, with a mature API and an active developer community. Best for professional long-form video production.

Kling 3.0—Kuaishou's model has become the community's top choice for realistic motion effects and is the tool most recommended by former Sora users in migration discussions. Developer API available.

Pika 2.0—Faster, cheaper, and easier to use than the above two. Plans start around $8/month. Best for content creators prioritizing speed over cinematic quality.

If your primary use case is for virtual avatars or talking head videos, rather than purely generative scenes, the tool choice differs.

What Happens Next

The AI video market is about to consolidate, and prices will rise.

With OpenAI's exit, Runway, Kling, and Google Veo no longer operate in a market where a well-funded new entrant could颠覆 (disrupt) everyone's pricing expectations at any moment.

This changes the commercial dynamics for all remaining players.

My predictions for the next six months:

Runway will raise subscription prices. Demand will surge with the influx of Sora users, and Runway's pricing has been below what its competitive position could support. The diminished threat from OpenAI gives them clear room to reprice.

Google Veo will more aggressively push a consumer product. Google had been deliberately quiet about a public rollout for Veo; the addressable market is now clearer. Expect a more prominent consumer product before the end of 2026.

Kling will target the enterprise contracts Disney's departure leaves behind. Kuaishou has been building Kling as a professional-grade product. The OpenAI-Disney deal effectively blocked some enterprise relationships that are now reopening.

An outcome I don't see happening: OpenAI returning to AI video with a consumer product. Internal signals point to video being recast as robotics infrastructure research, and the window for re-entering the market is shorter than this company's typical development cycles.

From my experience observing every AI category, the company that wins is the one that accumulates iterations over time, not the one that released the best demo. Sora peaked at the demo; Runway has been accumulating for three years.

Frequently Asked Questions

Q: As of March 2026, is the Sora App still usable?

As of March 24, 2026, Sora has entered the shutdown process. OpenAI has not announced a specific final access date for all users, but the termination process has begun. Do not rely on its continued availability for any production environment work.

Q: What is the best alternative to Sora for API developers?

Runway Gen-4 currently has the most mature and stable developer API among AI video tools. Kling 3.0 also offers API access and is widely recommended in developer migration discussions. It's advisable to test both before fully migrating.

Q: Why did Disney cancel its $1 billion investment in OpenAI?

Disney's investment and the three-year licensing agreement were directly tied to the Sora product line, including rights to use Disney characters in AI-generated videos. With Sora's shutdown, the licensing arrangement lost its foundation. Both parties have called it off, according to Bloomberg and Variety.

Q: What will happen to the internal Sora research team at OpenAI?

The team continues to work on world simulation research for robotics. This work will not result in any consumer or developer-facing video products. OpenAI positions it as infrastructure research, not something on the product roadmap.

Q: Does this mean OpenAI is broadly scaling back consumer products?

OpenAI has made it clear that pre-IPO resources are focused on enterprise software, programming tools, and agent products. Sora's shutdown aligns directly with this direction.

Q: Is Google Veo now the best Sora alternative?

Veo is technically strong, but for developers and content creators, Runway Gen-4 and Kling 3.0 are currently more accessible and better supported. For most users needing to migrate today, Runway or Kling is the more practical choice.