Author: Brayden Lindrea

Compiled by: Deep Tide TechFlow

Deep Tide TechFlow Summary: Bitcoin miner MARA Holdings has delivered a dismal Q1 report: revenue fell 18% year-on-year, net loss expanded from $530 million to $1.3 billion, and the stock erased all its intraday gains after hours. The bulk of the loss stemmed from unrealized losses on its BTC holdings. More notably, MARA has clearly stated it will no longer purchase new mining rigs, pivoting entirely to AI data centers—its ranking as the largest miner by market capitalization has already slipped to seventh place.

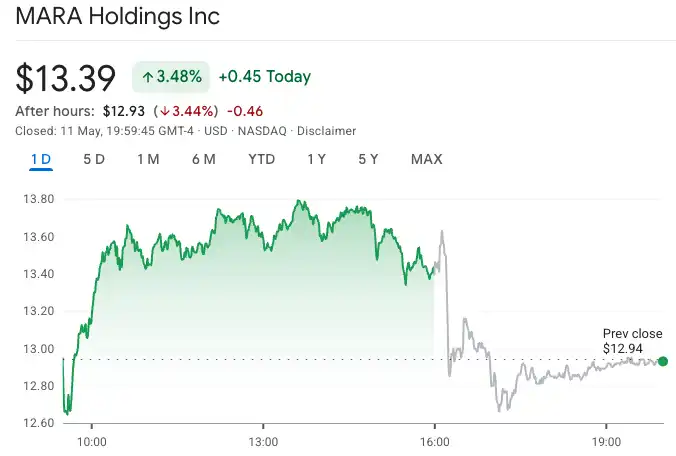

MARA Holdings' stock fell 3.44% after hours on Monday, closing at $12.93, completely wiping out its 3.48% gain from the day. The reason is simple: its Q1 earnings report missed expectations across the board.

Revenue and Profit Both Miss

According to the report filed by MARA, revenue for the quarter ended March 31 was $174.6 million, down 18% year-on-year, falling short of Wall Street's expectation of $192.7 million.

Net loss was $1.3 billion, compared to a loss of $533.4 million in the same period last year, expanding by nearly 1.5 times. Loss per share was $3.31, also significantly exceeding analysts' forecast of $2.20.

Caption: MARA's after-hours stock price movement, source: Google Finance

Where Did the $1.3 Billion Loss Come From?

The main reason for the loss was the unrealized losses on MARA's holdings of 38,689 bitcoins. Bitcoin price fell 23% in Q1, directly dragging down the book value.

MARA sold over 15,100 bitcoins in the final week of March, worth approximately $1.1 billion, to repurchase its debt at a discount.

Mining Environment Continues to Deteriorate

MARA's predicament is not an isolated case. The entire U.S. Bitcoin mining sector is sliding from profit to loss.

Two core pressures: Bitcoin is down over 35% from its all-time high of $126,080, significantly reducing miner revenue per block; simultaneously, mining difficulty has increased by nearly 30% over the past year, pushing hashing costs consistently higher.

MARA's industry standing is also declining. By market cap, it has fallen from being the largest Bitcoin miner to seventh place, as competitors move faster in their AI pivots.

Full Pivot to AI Data Centers

MARA says Bitcoin mining remains the "operational foundation" of the company, but its actions are already clear.

The company's AI strategy has two main thrusts: first, collaborating with Starwood Capital to convert existing mining sites into AI and High-Performance Computing (HPC) data centers; second, acquiring Long Ridge Energy & Power for $1.5 billion in late April, a natural gas power plant with an associated data center.

MARA's statement is:

"Our strategy is to colocate new infrastructure with our existing Bitcoin mining sites. The flexibility this creates is that we can generate revenue through mining today while preserving the option to divert power to AI and other critical IT loads."

The Long Ridge acquisition ultimately supports 600 MW of AI compute power, and approximately 90% of MARA's non-custodial mining capacity could be redeployed for AI and IT computing.

A one-sentence summary of its transformation resolve: The company explicitly stated it has no plans to purchase new mining rigs in the future.