Original | Odaily Planet Daily (@OdailyChina)

Author | Asher (@Asher_ 0210)

Last Saturday, Mustafa, a member of the Polymarket official team, posted on X platform that major news would be announced on Monday.

Activity of Polymarket official team member last weekend

As expected, Polymarket official released multiple major updates from last night to today. Next, Odaily Planet Daily will break them down for you one by one.

Updated Market Integrity Rules: Anti-Insider Trading, Anti-Manipulation

Last night, Polymarket announced updates to its market integrity rules for both its DeFi platform and its CFTC-regulated US exchange, further clarifying regulatory requirements regarding insider trading and market manipulation. Neal Kumar, Chief Legal Officer of Polymarket, stated: "Market prosperity relies on transparency. The refinement of these rules makes our expectations for all participants on both platforms clear and highlights the compliance infrastructure we have established. As Polymarket continues to grow, we will continue to solidify our foundation, ensuring our markets achieve their greatest strength—revealing the truth—through clear communication with users."

The new rules detail three types of prohibited behaviors, specifically including:

- Trading using non-public information: If a participant possesses confidential information about the outcome or potential outcome of the subject event, and using this information would violate a pre-existing duty of trust or confidence owed to another person or entity, the participant must not trade any contracts.

- Building positions based on illegal information sources: Participants must not trade using confidential information provided to them by others if the information was provided by someone who owes a pre-existing duty of trust or confidence to another, and the participant knows or has reason to know that the person providing the information would themselves be prohibited from using it for trading;

- Entities with the ability to influence event outcomes participating in trading: If a participant has sufficient authority or influence to affect the outcome of the subject event, they must not participate in trading any contracts.

Simultaneously, the platform explicitly prohibits behaviors such as wash trading, matched orders, and price manipulation, and has launched a dedicated page to explain the rules and provide a channel for reporting anomalous behavior. Furthermore, Polymarket stated that its DeFi platform identifies risks through on-chain transparency mechanisms and a multi-layer monitoring system, while its US platform combines technical monitoring with collaboration from industry regulators to investigate and penalize violations.

This round of rule updates essentially redefines the market boundaries of Polymarket: which information can be traded, and which behaviors are directly excluded. Surrounding insider information, information sources, and the ability to influence event outcomes, the platform has turned previously ambiguous gray areas into clear "no-go" red lines, while simultaneously introducing monitoring and reporting mechanisms to bring trading behavior into a more traceable framework.

More importantly, this points to a change in the platform's positioning. Polymarket is shifting from the external perception of a "high-risk gambling arena" towards emphasizing information pricing and transparency as market infrastructure. By proactively strengthening compliance and rule expression, it aims to gain trust at the regulatory and public levels, laying the groundwork for subsequent broader expansion.

The Era of "Big Fees" Arrives: Fees Applied to All Except Geopolitical Events

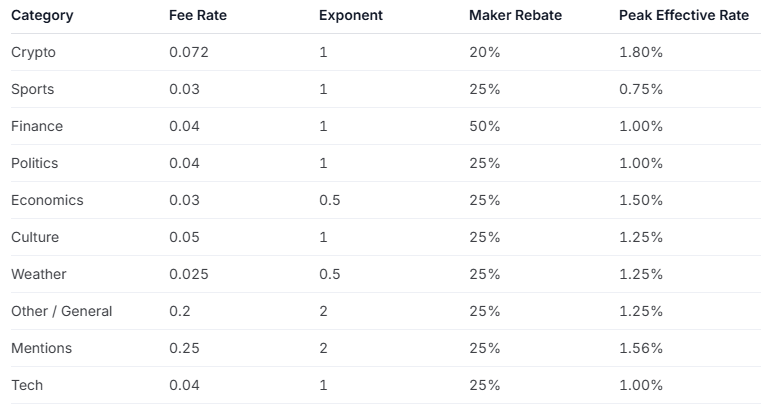

According to the latest official Polymarket documentation, the platform will adjust its fee mechanism starting March 30, 2026. Building on the current Crypto and Sports categories, it will add multiple market categories such as Finance, Politics, Economics, Culture, Weather, etc., into the scope of taker fee charges.

The new fee rate is calculated using a dynamic formula directly related to price intervals. Overall, the new fee structure shows a distribution of "high in the middle, low at the ends": when the price is close to a 50% probability, the effective rate peaks, while in extreme intervals near 0% or 100%, the fee significantly decreases, potentially even being rounded down to 0 for very small trades.

Under the current fee system, the peak effective rate for Crypto markets is about 1.56%, and for Sports about 0.44%. In the new fee structure about to take effect, the differences between categories are further widened. For example, Crypto peaks at about 1.80%, Finance and Politics at about 1.00%, and Economics can reach 1.50%. Simultaneously, the corresponding maker rebate ratios for various categories are also set, e.g., Finance is as high as 50%, with most other categories around 25%.

The fee calculation is based on a unified formula, dynamically calculated by combining trade shares, price, and different market parameters. Fees are denominated in USDC but are charged in "share form" for buy orders and deducted in USDC for sell orders.

New fee charging standards for various markets

Not News Related to Financing or Token Airdrops, But Opening a Referral Program

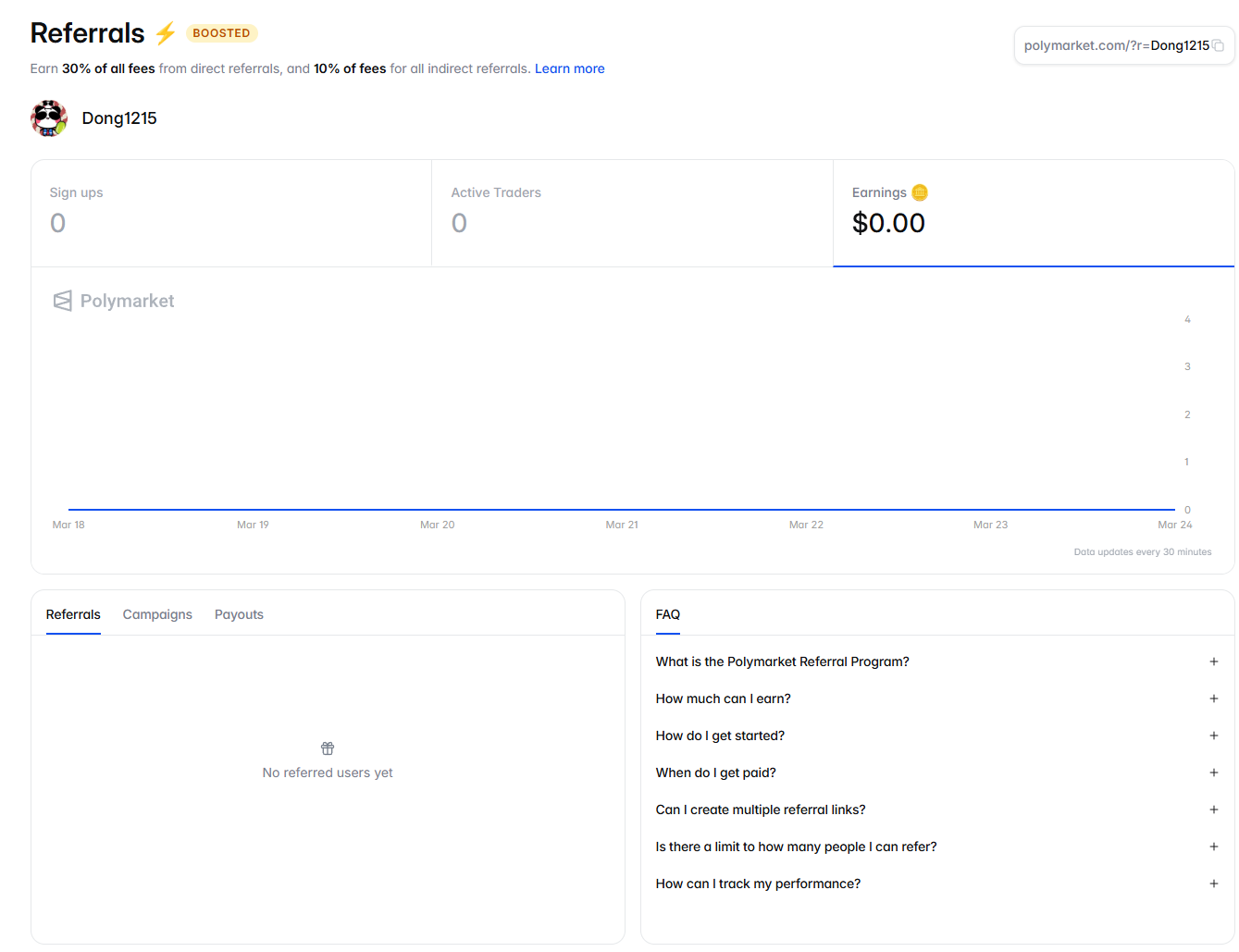

This morning, Polymarket posted on X platform announcing that the referral program has been expanded from the internal testing phase to all traders with a trading volume exceeding $10, 000. Eligible users can receive rewards proportional to the trading volume of the new users they refer. Specific invitation details are as follows:

- 30% fee rebate from direct referrals, 10% fee rebate from secondary referrals (rewards will be valid for the first 180 days after the user registers with Polymarket, this period may be subject to change without notice);

- Fee rebate rewards are distributed daily (UTC);

- Rewards are uncapped; the more your referred users trade on the platform, the more you earn.

Polymarket invitation interface

Launch of Market Maker Rebate Program

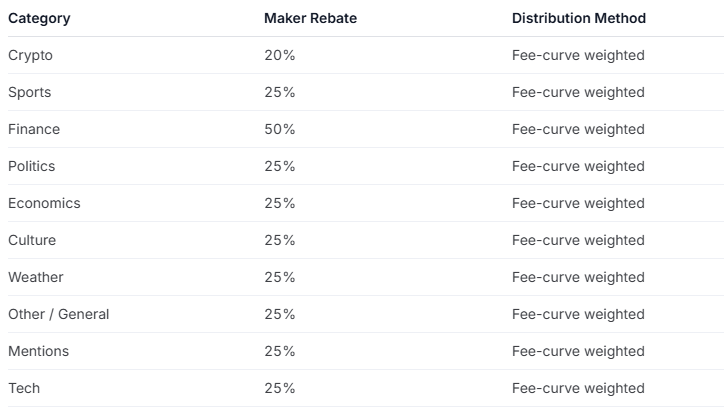

In addition to opening the referral program, to incentivize continuous and competitive quoting, thereby providing a better trading experience for all traders, Polymarket has launched a market maker rebate program. Specifically, this mechanism redistributes a portion of the taker fees to liquidity providers (market makers), effectively redistributing trading costs among market participants.

Rebates are settled and distributed daily in USDC. Only successfully placed orders that are executed contribute to the allocation. The overall profit is not a fixed value but is calculated based on the proportion of liquidity contribution in the actual executed trades. The more trades executed and the higher the contribution, the corresponding rebate received is greater.

In terms of allocation logic, the system calculates the "fee equivalent value" for each executed trade, synthesizing the executed quantity, price, and fee parameters of different markets, and aggregates this within the same market. The final rebate is allocated according to each market maker's contribution share, meaning competition exists not only in whether the quote is executed but also in the price range of the quote and the fee contribution it brings. Overall, this rebate comes from the taker-paid fees, with varying rebate ratios across different markets, e.g., Crypto is 20%, Finance can be 50%, and most categories are around 25%.

Rebate ratio situation across markets

No Information on Token Airdrops, But Overall Community Sentiment is Optimistic

Although the community previously anticipated that the "major news" might point to a token or airdrop, what ultimately materialized was a combination of updates to fees, rebates, and the referral system. Looking at the outcome, this mechanism leans more towards long-term incentive design rather than a one-time release of expectations. However, sentiment did not cool down because of this; instead, with clear, actionable paths for participation, the overall feedback from the trading community has been positive.

Many users already see the referral program as a "de facto airdrop entry," especially KOLs with their own traffic or community resources, who have noticeably increased their sharing efforts, with some even treating it as a long-term income stream; after the market maker rebate went live, feedback from the LP side was also direct, with more people reassessing their market making strategies, showing a clear increase in willingness to participate.

In contrast, arbitrage traders and those scanning for end-of-market opportunities are calmer. With the arrival of the new fee rules, some previously viable arbitrage spaces will be compressed, strategies need recalculation, and trading rhythms consequently tend to收敛 (converge, become more conservative), relying more on precise execution and cost control.

However, after Polymarket and Kalshi came under regulatory scrutiny, their valuations in the coming period will likely be worn down by policy tensions. (Related news:US lawmakers to propose bipartisan bill banning sports predictions on prediction markets like Polymarket)