Author: Oluwapelumi Adejumo

Translation: Chopper, Foresight News

BitMine aggressively built up its Ethereum holdings, attempting to transform them into a stable source of cash flow, with its staking business generating nearly $46 million in revenue last quarter.

However, a $92.1 million loss on derivatives and options completely offset these staking gains. Combined with persistently high asset management costs and the company's aggressive issuance of new shares, the profit potential for existing shareholders was significantly compressed.

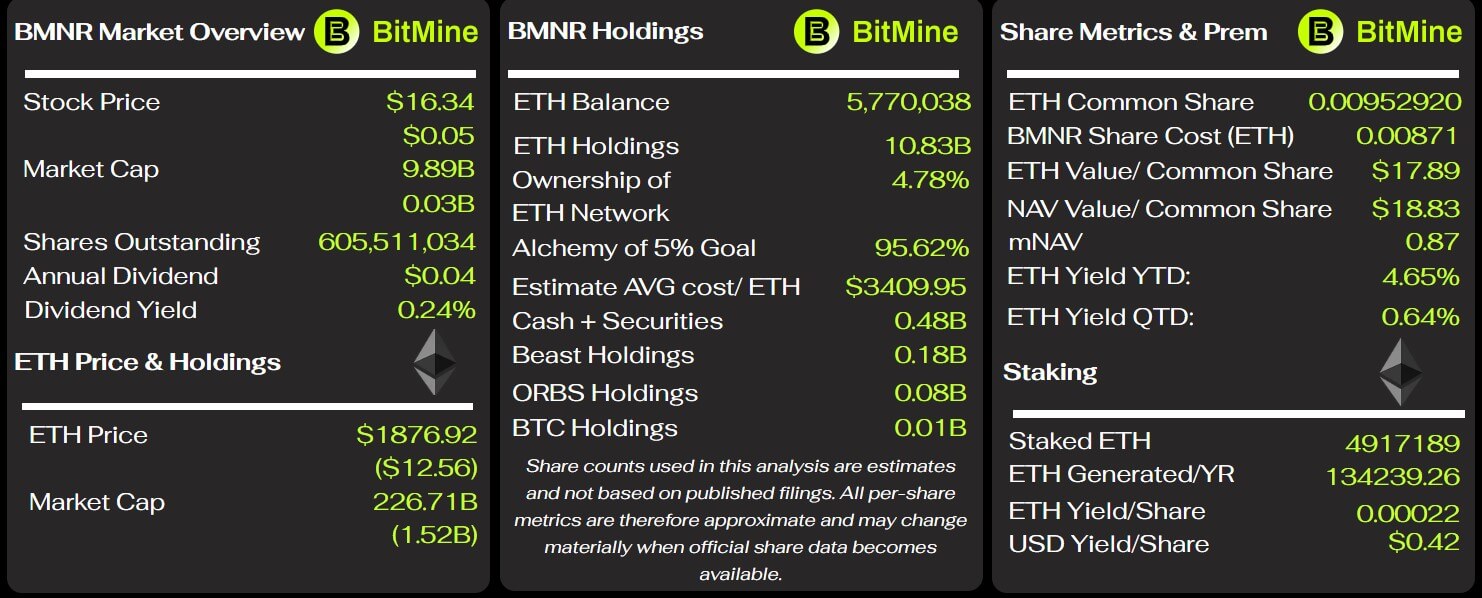

The Q3 FY2026 financial report, for the period ending May 31, shows company revenue soared to $46.5 million from $2.1 million in the same period last year; 98% ($45.7 million) of this came from staking and node validation services. BitMine is accelerating its exit from Bitcoin mining to fully transition to an Ethereum treasury model.

Despite the substantial revenue growth, the company reported a net loss of $83.6 million for the quarter, a dramatic increase compared to a modest loss of $623,000 in the same period last year.

Massive Options Losses Wipe Out All Ethereum Staking Gains

The core factor dragging down this quarter's performance was the company's Ethereum derivatives and options trading strategy. BitMine incurred a combined loss of $92.1 million on Ethereum-related derivatives this quarter, approximately double the total revenue from its staking business during the same period. This included $78.6 million in net losses from expired option contracts and $14 million from exercised positions. Gains of only $534,000 from unsettled contracts provided negligible offset.

The company engaged in no derivatives trading during the same period last year, marking a qualitative leap in its asset management risk exposure. For the first nine months of the fiscal year, cumulative derivatives losses totaled $133.3 million, consisting of $79.3 million from exercised losses and $54.5 million from expired contracts, with only $515,000 in gains from unsettled positions. During the same period, staking and validation services generated only $56.9 million, making derivatives losses more than double the staking income.

BitMine stated that its options strategy primarily involves selling put options as part of its overall portfolio management. While selling puts can generate premium income and allow for asset accumulation at lower prices, it can result in massive losses if the market moves against the position and contracts are exercised under unfavorable conditions. The scale of this loss clearly demonstrates that the attempt to enhance returns with options has, for now, completely negated the stable income generated by the node staking business.

Simultaneously, the company's general and administrative expenses surged to $37.3 million from $744,000 a year ago. Management explained that the increase was primarily due to digital asset custody and management service fees, salary adjustments, and increased cash and stock-based compensation for directors.

Excluding changes in the valuation of crypto assets, staking income was sufficient to cover the quarter's cost of sales and administrative expenses. Even after adjusting for several non-cash items, the company's own adjusted non-GAAP net loss still reached $70.8 million. This financial report indicates that while the node validation business has generated a substantial and stable cash flow, the overall portfolio trading strategy continues to consume staking profits.

Continuous BMNR Share Issuance to Hoard Ethereum, Sharply Diluting Shareholder Equity

The funds for BitMine's large-scale Ethereum accumulation came almost entirely from public market offerings of common stock, with the cost fully borne by existing shareholders. In the nine months ending May 31, the company sold 340.7 million shares of BMNR common stock through its at-the-market offering program, raising $11.87 billion net of issuance costs; during the same period, it spent $11.69 billion purchasing Ethereum.

Shareholder equity was significantly diluted. The number of common shares outstanding increased by 149% over nine months, from 232.4 million as of August 31, 2025, to 579.7 million by the end of May 2026; issuance continued after the quarter ended, with total shares reaching 603.2 million as of July 9.

Fueled by equity financing, BitMine had accumulated holdings of 5.42 million Ethereum by May 31, with a combined acquisition cost of $19.05 billion; holdings had increased to 5.7 million Ethereum at the time of writing.

Key Metrics for BitMine, Source: BitMine Tracker

As of the end of May, this Ethereum portfolio was valued at only $10.86 billion, representing an unrealized loss of approximately $8.2 billion, a 43% decline from cost.

This portfolio devaluation was the primary source of the $9.04 billion unrealized loss on digital assets for the first nine months of the fiscal year, during which the company reported a cumulative net loss of $9.1 billion. The massive unrealized loss vividly illustrates that BitMine's share issuances purchased Ethereum at high prices, with all the risk borne by shareholders.

A shareholder meeting in January approved an increase in the company's authorized common shares from 500 million to 50 billion. This authorization does not obligate the company to issue all shares but grants management ample room to continue issuing stock for purchasing digital assets and other investments.

BitMine cautioned that its ability to expand its Ethereum holdings is highly dependent on continuous and unimpeded access to financing. A decline in Ethereum's price, weakness in the company's stock price, or a decrease in investor appetite for its offerings could all increase the cost of future financing or even restrict the company's ability to issue securities on favorable terms.

The viability of this business model depends not only on staking yields and future Ethereum price appreciation but also on shareholders accepting significant equity dilution and the portfolio carrying billions in unrealized losses, while continuously providing capital for the company's coin accumulation.

Long-Term Service Contracts Increase Staking Operating Costs, Compressing Profit Margins

BitMine relies on its staking business to hedge against portfolio price volatility, but accompanying long-term cooperation agreements generate fixed fees and profit-sharing, continuously compressing overall profitability. The company has a ten-year consulting agreement with third-party service provider Ethereum Tower, incurring an expense of $12.8 million this quarter, representing about 28% of the period's total staking revenue. Cumulative fees for the first nine months amounted to $37.5 million; the company estimates annual fees in the range of $40 to $50 million, calculated on a tiered basis against the total value of managed digital assets.

The agreement can only be terminated under a few specific conditions. If BitMine terminates without cause, it must pay Ethereum Tower 85% of all estimated service fees for the remaining contract term.

Furthermore, following its acquisition of node operator Pier Two, BitMine entered into a separate ten-year management services agreement. This agreement grants Ethereum Tower a 2% equity stake in the MAVAN platform, with monthly profit-sharing based on a percentage of the platform's native staking rewards. As of May 31, the company had not accrued any expenses related to this agreement, so the profit-sharing costs are not yet reflected in the staking business's income statement.

BitMine stated that the vast majority of its Ethereum is staked through MAVAN, and over the long term, staking rewards are expected to cover asset custody costs. Looking solely at the operational level this quarter, staking revenue did cover sales and administrative expenses excluding crypto asset valuation changes. However, the combination of a decade-long fixed consulting fee, future profit-sharing, and various other asset management expenses means that relying solely on staking income does not accurately reflect the business's true profitability.

Despite No Debt, BitMine's Dependence on Capital Markets Deepens

As of the end of May, BitMine's balance sheet showed extremely low leverage, with $340.3 million in cash, working capital of $433.1 million, and no traditional debt. Total assets were $11.63 billion, with total liabilities of only $30.1 million, and assets predominantly consisting of Ethereum and other digital assets. On paper, the company faces no immediate debt crisis, but operating activities used $287.6 million in cash during the first nine months. The company attributed the cash burn primarily to legal, consulting, and investment banking fundraising fees associated with expanding its Ethereum holdings.

After the quarter ended, BitMine issued an additional 3.5 million shares of its 9.5% annual perpetual preferred stock, BMNP, raising $273.8 million. While this offering supplemented short-term liquidity, it adds a new, rigid annual dividend expense of approximately $33.25 million for the preferred shares. Although this security is equity, not debt, it has priority over common shares in liquidation, and its high dividend continuously consumes company cash flow.

Management believes existing cash, expected operating cash flow, and the at-the-market offering facility are sufficient to fund operations for at least the next 12 months. This assessment assumes the capital markets remain open: if Ethereum prices remain depressed long-term, the company's stock price weakens, or investor appetite wanes, the company's financing costs will rise, and its operational flexibility will be constrained.

Synthesizing the latest financial report, BitMine presents a set of contradictory realities: On one hand, the company has established a mature staking business generating tens of millions in quarterly revenue, enough to cover core operational expenses. On the other hand, massive options losses completely devour staking profits, long-term contracts persistently increase management costs, and Ethereum accumulation relies entirely on share issuance, with the total share count more than doubling.

Therefore, BitMine's long-term economic viability depends on whether staking income can stably cover various asset management costs and options losses, whether the company can sustainably secure equity financing, and whether Ethereum's price can stage a significant recovery.