Author: Trend Research

Original Title: Under Global Easing Expectations, ETH Has Entered the Value 'Sweet Spot'

Since the market crash on October 11, the entire cryptocurrency market has been sluggish, with market makers and investors suffering heavy losses. The recovery of capital and sentiment will take time.

However, the cryptocurrency market is never short of new fluctuations and opportunities, and we remain optimistic about the future market.

This is because the trend of mainstream crypto assets integrating with traditional finance to form new ecosystems has not changed; instead, it has rapidly built moats during the market downturn.

I. Wall Street Consensus Strengthens

On December 3, U.S. SEC Chairman Paul Atkins stated in an exclusive interview with FOX on the New York Stock Exchange: "In the coming years, the entire U.S. financial market may migrate to the blockchain."

Atkins said:

-

The core advantage of tokenization is that if assets exist on the blockchain, the ownership structure and asset attributes will be highly transparent. Currently, listed companies often do not know who their shareholders are, where they are located, or where the shares are held.

-

Tokenization is also expected to achieve "T+0" settlement, replacing the current "T+1" trading settlement cycle. In principle, the delivery versus payment (DVP)/receive versus payment (RVP) mechanism on-chain can reduce market risks and improve transparency. The time gap between clearing, settlement, and fund delivery is currently a source of systemic risk.

-

Tokenization is seen as an inevitable trend in financial services, with mainstream banks and brokerages already moving toward tokenization. The world may not even take 10 years... perhaps it will become a reality in just a few years. We are actively embracing new technologies to ensure the U.S. remains at the forefront in areas like cryptocurrency.

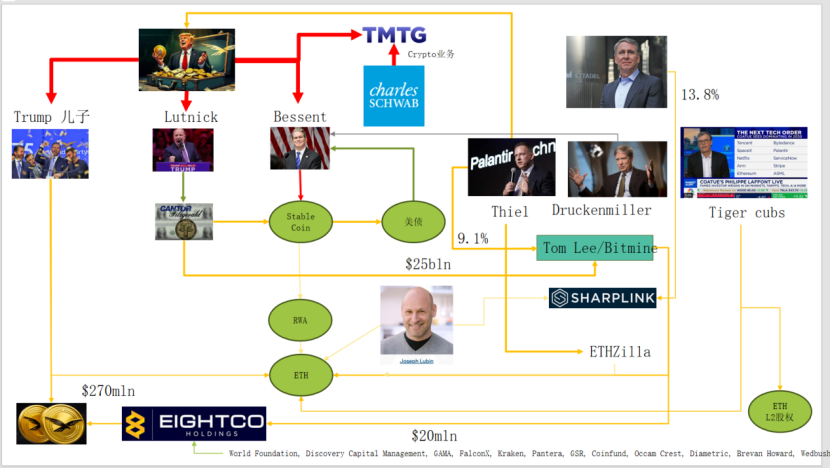

In reality, Wall Street and Washington have already built a capital network deeply embedded in crypto, forming a new narrative chain: U.S. political and economic elites → U.S. bonds (Treasury bonds) → Stablecoins / Crypto treasury companies → Ethereum + RWA + L2

From this chart, we can see the intricate connections between the Trump family, traditional bond market makers, the Treasury, tech companies, and crypto companies, with the green elliptical links forming the backbone:

(1) Stable Coins (USDT, USDC, dollar assets behind WLD, etc.)

The majority of reserve assets are short-term U.S. bonds + bank deposits, held through brokers like Cantor.

(2) U.S. Bonds (U.S. Treasuries)

Issued and managed by the Treasury / Bessent side.

Used by Palantir, Druckenmiller, Tiger Cubs, etc., as low-risk interest rate base holdings.

Also the yield assets pursued by stablecoins / treasury companies.

(3) RWA (Real World Assets)

From U.S. bonds, mortgages, accounts receivable to housing finance.

Tokenized through Ethereum L1 / L2 protocols.

(4) ETH & ETH L2 Equity

Ethereum is the main chain承接 RWA, stablecoins, DeFi, and AI-DeFi.

L2 equity / Token represents a claim on future trading volume and fee cash flows.

This chain expresses:

U.S. dollar credit → U.S. bonds → Stablecoin reserves → Various crypto treasury / RWA protocols → Ultimately沉淀 on ETH / L2.

In terms of RWA TVL, compared to other public chains that declined after the October 11 crash, ETH is the only public chain that quickly recovered and rose. Its current TVL is $12.4 billion, accounting for 64.5% of the total crypto market.

II. Ethereum Explores Value Capture

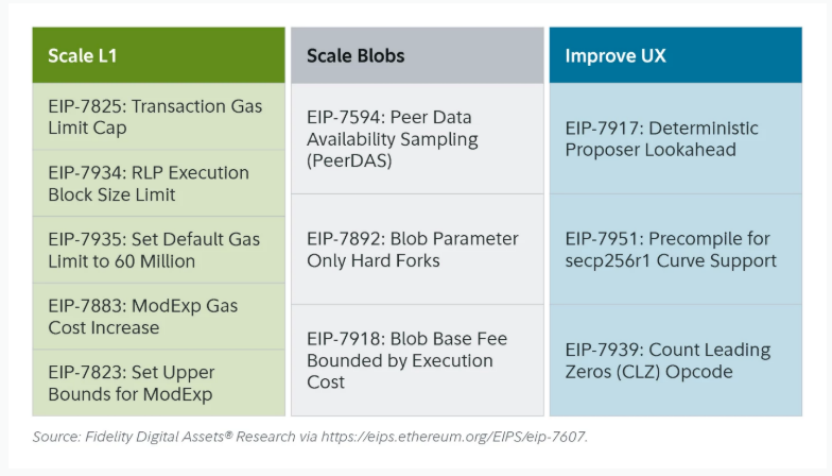

The recent Ethereum Fusaka upgrade did not cause much stir in the market, but from the perspective of network structure and economic model evolution, it is a "milestone event." Fusaka is not just about scaling through EIPs like PeerDAS but also attempts to address the issue of insufficient value capture by the L1 mainnet due to L2 development.

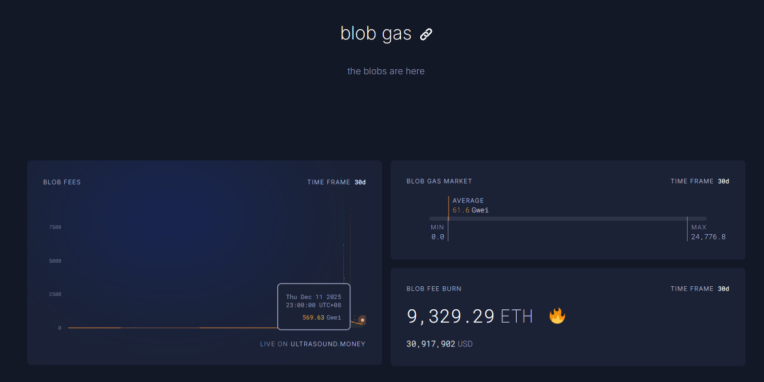

Through EIP-7918, ETH introduces a "dynamic floor price" for blob base fees, binding its lower limit to the L1 execution layer base fee, requiring blobs to pay at least about 1/16 of the L1 base fee unit price for DA fees. This means Rollups can no longer occupy blob bandwidth at near-zero cost for extended periods, and the corresponding fees will be burned and回流 to ETH holders.

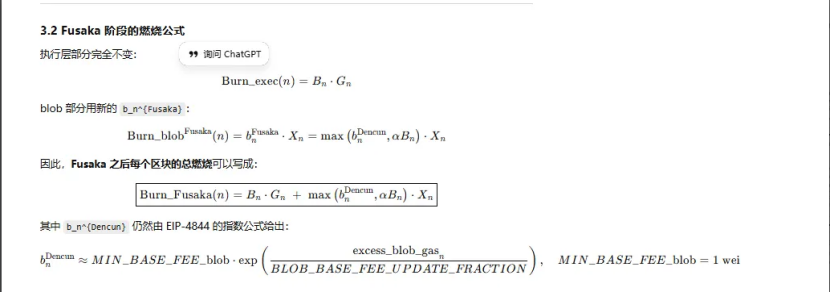

There have been three upgrades related to "burning" in Ethereum:

(1) London (Single-dimension): Only burned the execution layer; ETH began to experience structural burning due to L1 usage.

(2) Dencun (Dual-dimension + independent blob market): Burned execution layer + blob; L2 data写入 blob also burned ETH, but during low demand, the blob portion was almost 0.

(3) Fusaka (Dual-dimension + blob bound to L1): To use L2 (blob), one must pay at least a fixed proportion of the L1 base fee, which is burned. L2 activity is more stably mapped to ETH burning.

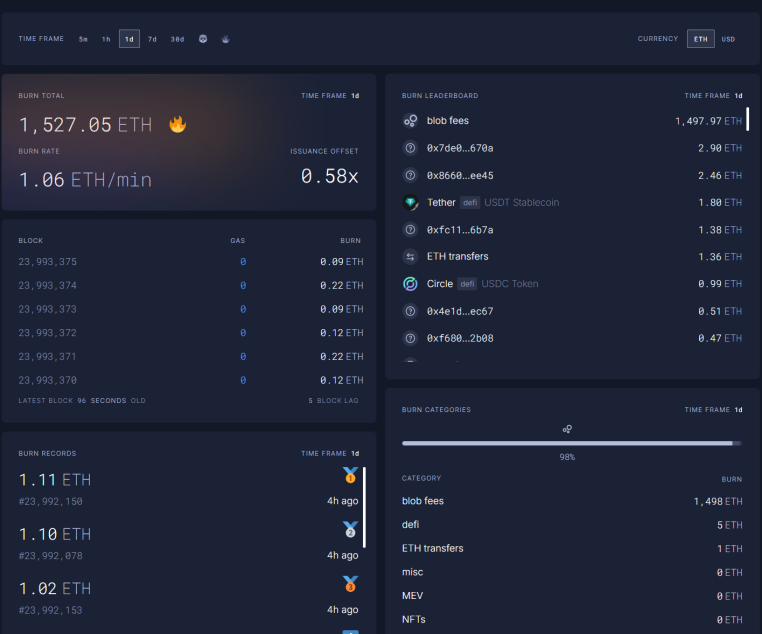

As of December 11, 23:00, the 1-hour blob fees have reached 569.63 billion times the pre-Fusaka upgrade level, burning 1,527 ETH in one day. Blob fees now contribute the highest proportion to burning,高达 98%. As ETH L2 becomes more active, this upgrade is expected to return ETH to deflation.

III. Ethereum Technicals Strengthen

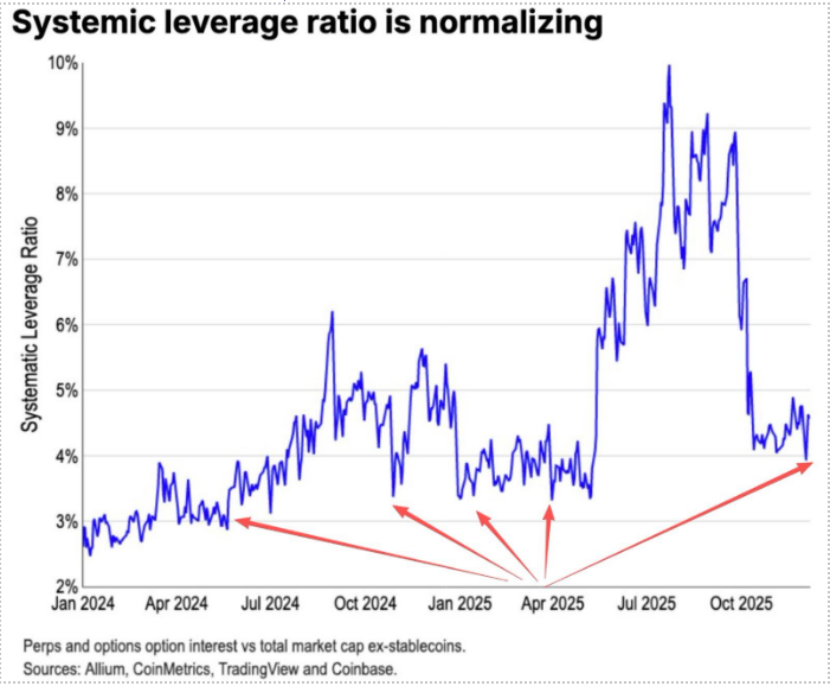

During the October 11 crash, ETH's futures leverage was thoroughly cleared, eventually reaching the spot leverage盘. At the same time, many with insufficient faith in ETH led to many early OG investors reducing their holdings and fleeing. According to Coinbase data, speculative leverage in the crypto圈 has dropped to a historically low region of 4%.

In the past, a significant portion of ETH short positions came from traditional Long BTC/Short ETH paired trades, which generally performed very well during bear markets. However, this time an意外 occurred. The ETH/BTC ratio has maintained a sideways resistance trend since November.

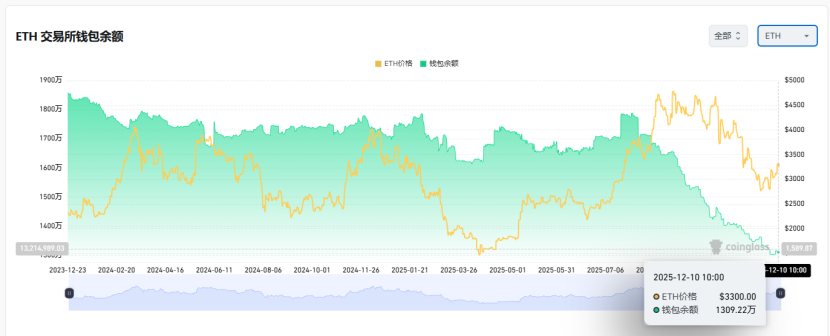

ETH's current存量 on exchanges is 13 million coins, about 10% of the total supply, at a historical low. As the Long BTC/Short ETH pairing has failed since November, during extreme panic, a "short squeeze" opportunity may gradually emerge.

As we approach the interaction between 2025 and 2026, future monetary and fiscal policies from both China and the U.S. have released friendly signals:

The U.S. will actively pursue tax cuts, interest rate reductions, and relaxed crypto regulations. China will implement appropriate easing and financial stability (suppressing volatility).

Under the expectations of relative easing in China and the U.S., and scenarios suppressing downward asset volatility, during extreme panic when capital and sentiment have not fully recovered, ETH is still in a good buying "sweet spot."

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush