This article is jointly published by K1 Research & Klein Labs

2025 Monthly Event Review Calendar source:Klein Labs

Looking back at 2025, this year was not simply a bull or bear market, but a repositioning of the crypto industry within the multiple coordinates of politics, finance, and technology—laying the foundation for a more mature and institutionalized cycle in 2026.

At the beginning of the year, Trump's inauguration and the executive order on digital asset strategy significantly changed regulatory expectations. At the same time, the issuance of the $TRUMP token brought cryptocurrencies out of their niche circle, rapidly increasing market risk appetite. Bitcoin historically broke through $100,000, completing its first leap from a "speculative asset" to a "political and macro asset".

Subsequently, the market quickly faced a reality check. The retreat of celebrity coins, the Ethereum flash crash event, and the epic hack on Bybit collectively exposed issues of high leverage, weak risk control, and narrative overextension. The crypto market gradually cooled down from its frenzy between February and April. Macro tariff policies resonated with traditional risk assets, and investors began to re-evaluate the weighting of safety, liquidity, and fundamental value in asset pricing.

During this phase, Ethereum's performance was particularly representative: ETH was under pressure relative to Bitcoin, but this weakness did not stem from degradation in technology or infrastructure. On the contrary, Ethereum made continuous progress in the first half of 2025 on key roadmaps such as gas limits, Blob capacity, node stability, zkEVM, and PeerDAS, with infrastructure capabilities steadily improving. However, the market did not price these long-term developments accordingly.

Entering the middle of the year, structural repair and institutionalization processes unfolded simultaneously. The Ethereum Pectra upgrade and the Bitcoin 2025 conference provided support for technology and narrative, while the Circle IPO marked the deep integration of stablecoins and compliant finance. The formal enactment of the GENIUS Act in July became the most symbolic turning point of the year—the crypto industry received clear, systematic legislative endorsement in the United States for the first time. Against this backdrop, Bitcoin refreshed its annual high. Meanwhile, on-chain derivative platforms like Hyperliquid grew rapidly, and new forms such as stock tokenization and Equity Perps began to enter the market's view.

In the second half of the year, capital and narratives showed a clear divergence in trends. Accelerated ETF approvals, expectations of pension fund entry, and the start of the interest rate cut cycle collectively lifted valuations of mainstream assets, while celebrity coins, memes, and high-leverage structures frequently experienced liquidations. The large-scale liquidation event in October was a concentrated embodiment of the year's risk release; at the same time, the privacy sector saw阶段性 strength, and new narratives like AI payments and Perp DEX quietly took shape in局部 sectors.

At the end of the year, the market closed with a高位阴跌 (high-level gradual decline) and low liquidity. Bitcoin fell below $90,000, while traditional safe-haven assets like gold and silver performed strongly, showing that the crypto market is deeply embedded in the global asset allocation system. At this juncture, mainstream crypto assets entered a阶段性筑底区间 (phase of bottoming out): whether the market in 2026 will follow the traditional four-year cycle by rebounding and then entering a bear market decline, or break the cycle law and hit new highs driven by continued institutional capital inflows and improved regulatory frameworks, will become the core research proposition for the next phase of market trends.

Macro Environment and Policy: Structural Changes in 2025

1. Shift in Policy Direction: The Essential Difference of 2025 from Past Cycles

Reviewing past cycles of the crypto industry, policy and regulation have always been important exogenous variables affecting market expectations, but their mode of action changed fundamentally in 2025. Unlike the laissez-faire growth of 2017, the宽松放任 (lenient laissez-faire) of 2021, and the comprehensive suppression of 2022–2024, what 2025 presented was an institutional shift from suppression to permission, from ambiguity to standardization.

In past cycles, regulation intervened in the market more negatively: either interrupting risk appetite at market highs through bans, investigations, or enforcement, or releasing uncertainty集中 (centrally) in the form of accountability during bear markets. Under this model, policies often failed to effectively protect investors and could not provide long-term development expectations for the industry, instead exacerbating the violent fluctuations of the cycle. Entering 2025, this governance method began to undergo structural changes: executive orders先行 (taking the lead), regulatory agencies'口径趋同 (stances converging), and legislative frameworks gradually advancing,逐步取代 (gradually replacing) the previous regulatory model dominated by case-by-case enforcement.

Crypto Regulation Development Chart source:Messari

In this process, the advancement of ETFs and stablecoin legislation played a key role in "anchoring expectations." The approval of spot ETFs provided Bitcoin and Ethereum等加密资产 (and other crypto assets) with a compliant channel for long-term capital allocation through the traditional financial system for the first time; by the end of 2025, the scale of ETP/ETF products related to Bitcoin and Ethereum had reached the hundreds of billions of dollars, becoming the main vehicle for institutional capital allocation of crypto assets. At the same time, stablecoin-related legislation (like the GENIUS Act) clarified the stratification of crypto assets from an institutional perspective: which have "financial infrastructure attributes" and which are still high-risk speculative products. This distinction broke the笼统定价 (generalized pricing) of "crypto as a whole," prompting the market to begin valuing different assets and sectors differentially.

It is important to note that the 2025 policy environment did not create a "policy红利式爆发 (dividend-style explosion)" like in past cycles. Instead, its greater significance lies in providing the market with a relatively clear lower bound: defining the boundaries of permissible behavior, distinguishing between assets with long-term viability and those destined to be marginalized. Under this framework, the role of policy shifted from "driving market sentiment" to "constraining risk," from "creating volatility" to "stabilizing expectations." From this perspective, the 2025 policy shift was not the direct engine of a bull market, but rather an institutional foundation.

2. Capital First: The "Low-Risk Channels" Built by Stablecoins, RWA, ETF, and DAT

In the 2025 crypto market, a counterintuitive yet crucial phenomenon became clear: capital did not disappear, but prices did not respond. Stablecoin market capitalization and on-chain transfer volumes remained high, spot ETFs maintained net inflows during multiple time windows, and yet, apart from a few mainstream assets, the prices of most altcoins remained under pressure for a long time. This divergence between capital activity and price performance constitutes the core entry point for understanding the 2025 market structure.

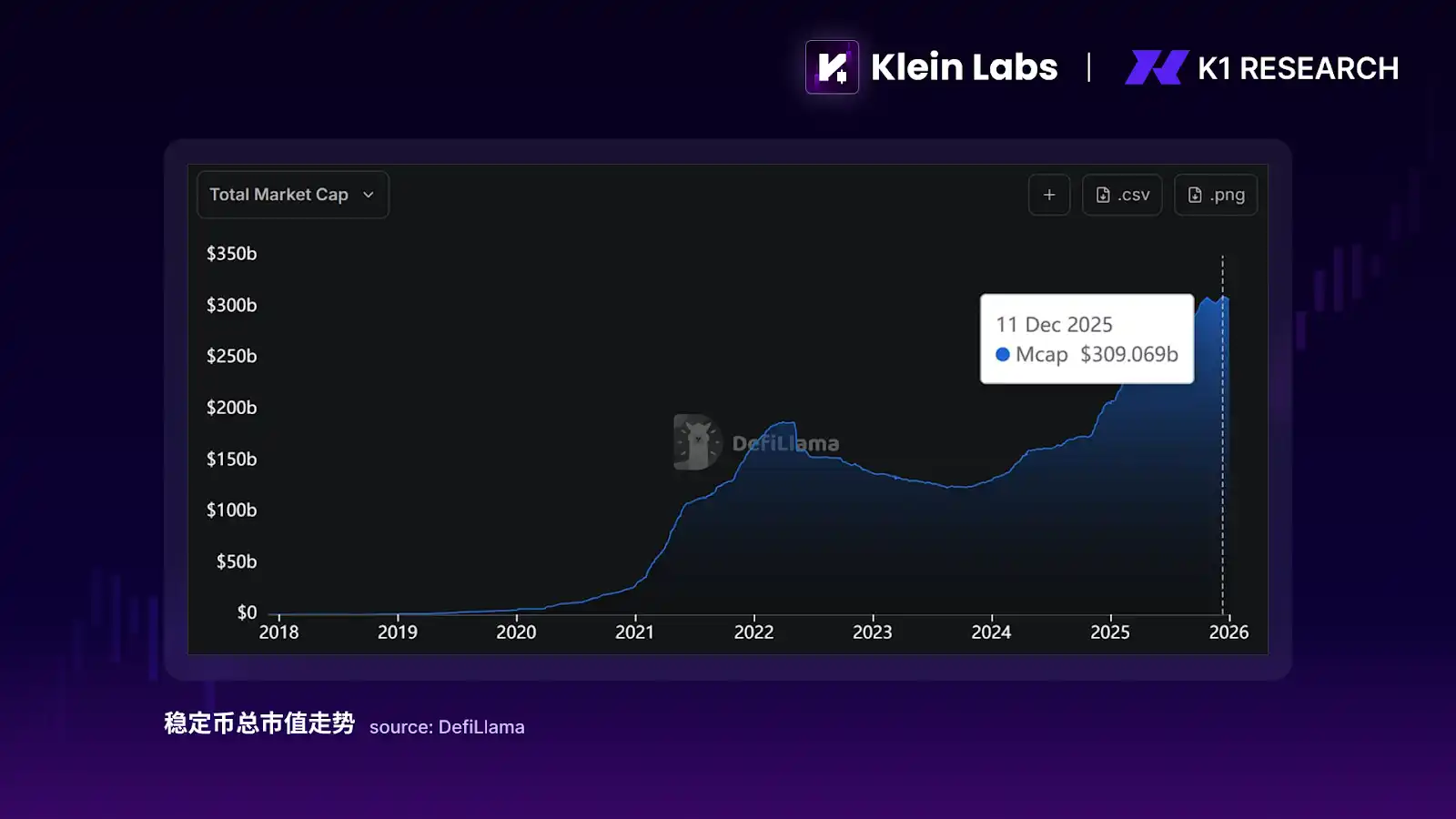

Stablecoins played a completely different role in this process compared to previous cycles. In the past, stablecoins were seen more as "intermediary currencies" within exchanges or leverage fuel in bull markets, their growth often highly correlated with speculative activity. In 2025, stablecoins gradually evolved into instruments for capital parking and settlement. The total stablecoin market cap grew from about $200 billion at the beginning of the year to over $300 billion by year-end, with a yearly increase of nearly $100 billion, but the overall market cap of alt assets did not expand simultaneously. Meanwhile, the annual on-chain settlement volume of stablecoins reached trillions of dollars, even nominally exceeding the annual transaction volume of traditional card networks. This shows that the growth of stablecoins in 2025 came mainly from payment,清算 (clearing), and capital management demands, rather than speculative leverage.

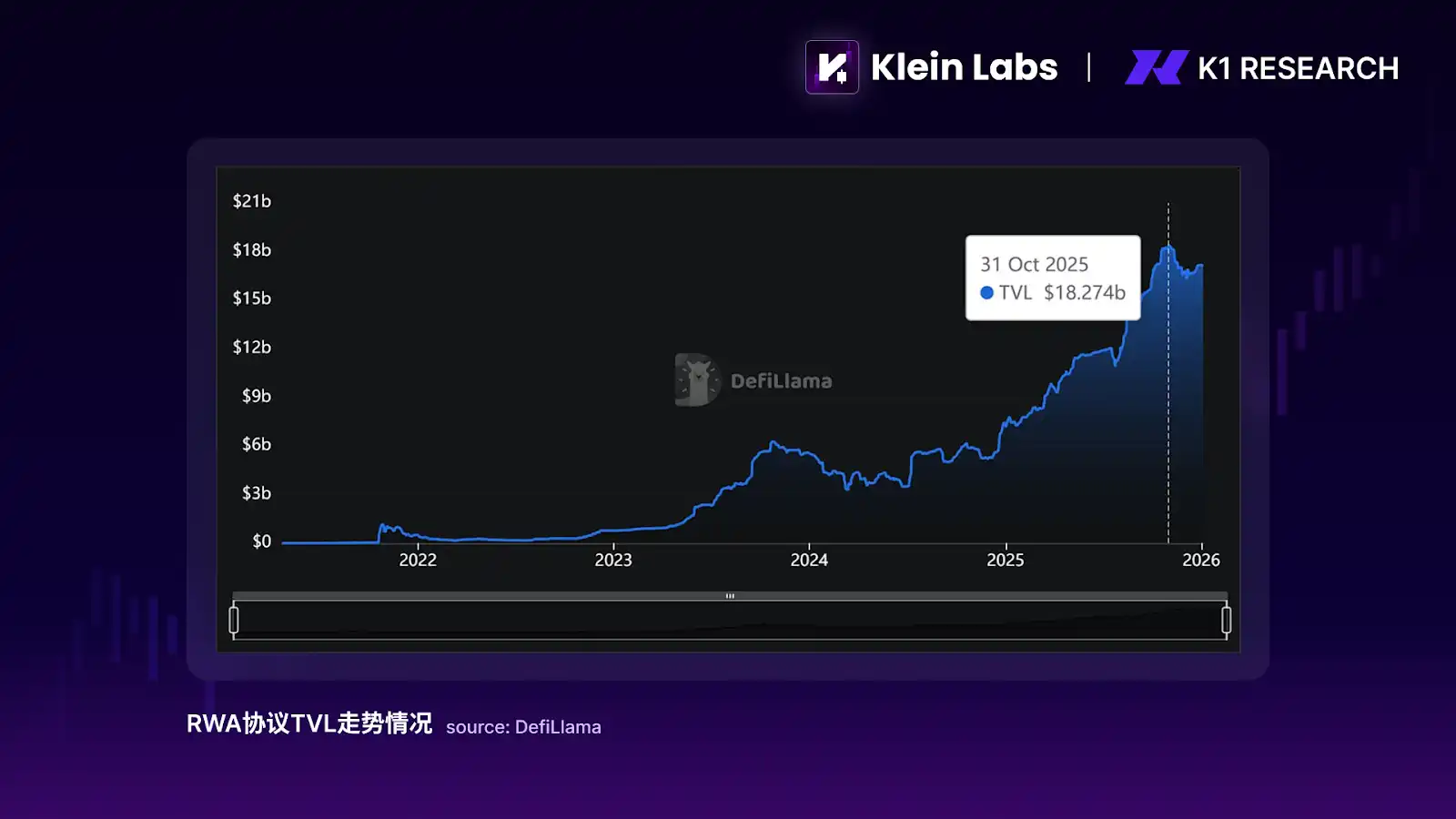

The development of RWA further reinforced this trend. The RWAs that真正落地 (truly landed) in 2025 were mainly concentrated in low-risk assets such as treasury bonds, money market fund shares, and short-duration notes. Their core significance lies not in creating new price elasticity, but in verifying the feasibility of compliant assets existing on-chain. From on-chain data, the TVL of RWA-related protocols began to accelerate growth in 2024 and continued to rise in 2025—by October 2025, the TVL of RWA protocols was close to $18 billion, several times higher than at the beginning of 2024.

Although this volume is still insufficient at the macro capital level to directly drive crypto asset prices, its structural impact is very clear: RWA provides on-chain capital with a parking option接近无风险收益 (close to risk-free returns), allowing some capital to "stay on-chain, but not participate in Crypto price fluctuations." Against the backdrop of still attractive interest rates and gradually clearer regulatory boundaries, this choice marginally weakened the traditional positive correlation between on-chain activity and token prices, further explaining the 2025 structural characteristic of "capital growth but decreased price elasticity."

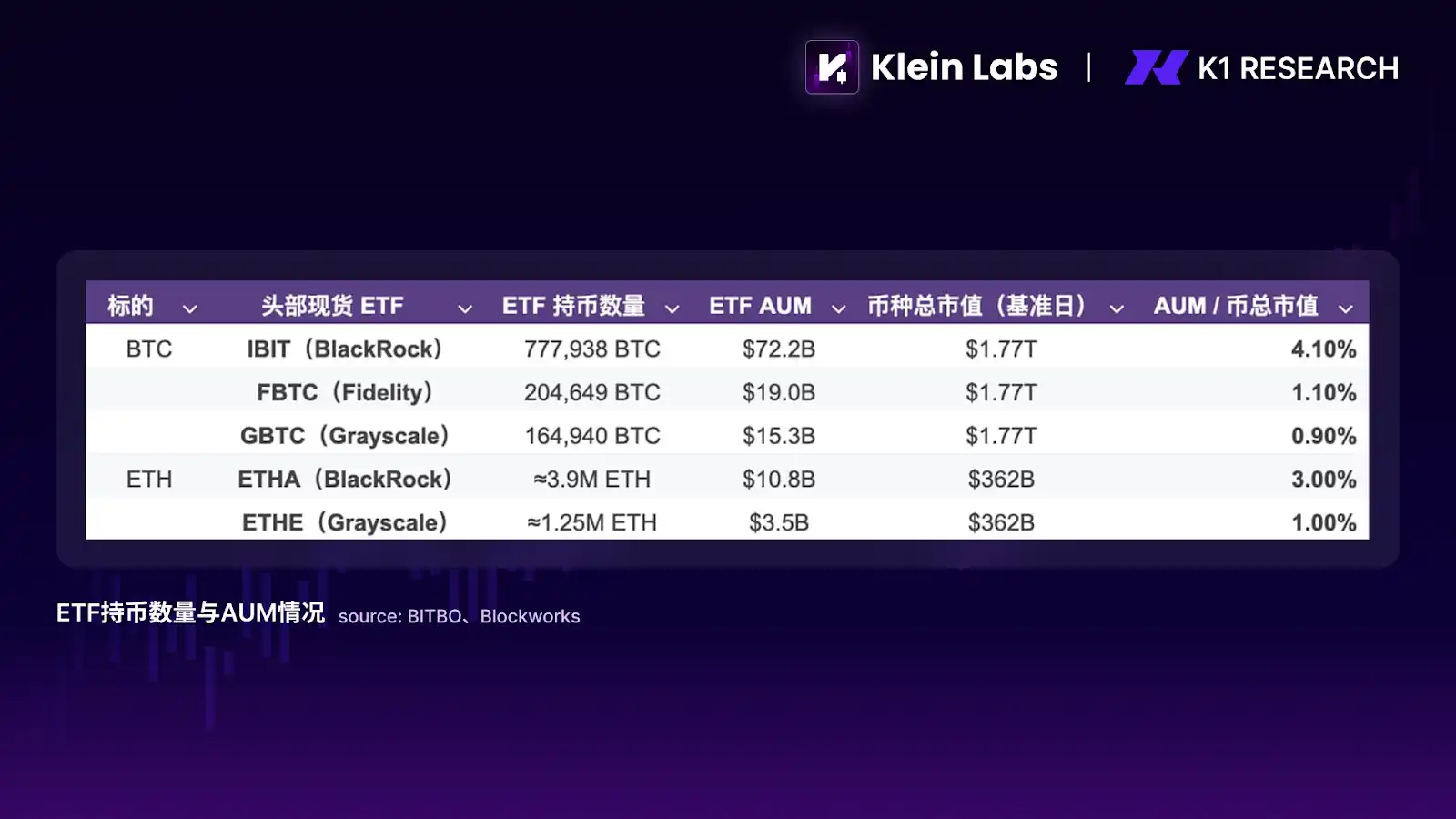

The impact of ETFs is more reflected in capital stratification rather than全面扩散 (comprehensive diffusion). Spot ETFs provided a compliant, low-friction allocation channel for mainstream crypto assets like Bitcoin and Ethereum, but this capital entry path is highly selective. In terms of actual承接规模 (absorption scale), by early 2026, top BTC/ETH spot ETFs were接近持有 (close to holding) over 6%/4% of the total circulating supply市值 (market cap) of each coin, forming a clear承接 (absorption) of institutional capital at the mainstream asset level. However, this increment did not spill over to broader asset tiers. During the ETF advancement, BTC Dominance did not experience the rapid decline常见 (commonly seen) in historical bull markets, but instead remained in a high range, reflecting that institutionalized capital did not diffuse into long-tail assets (usually referring to tokens outside the top 100 by market cap). The result is that ETFs strengthened the capital absorption capacity of top assets but objectively intensified the structural differentiation within the market.

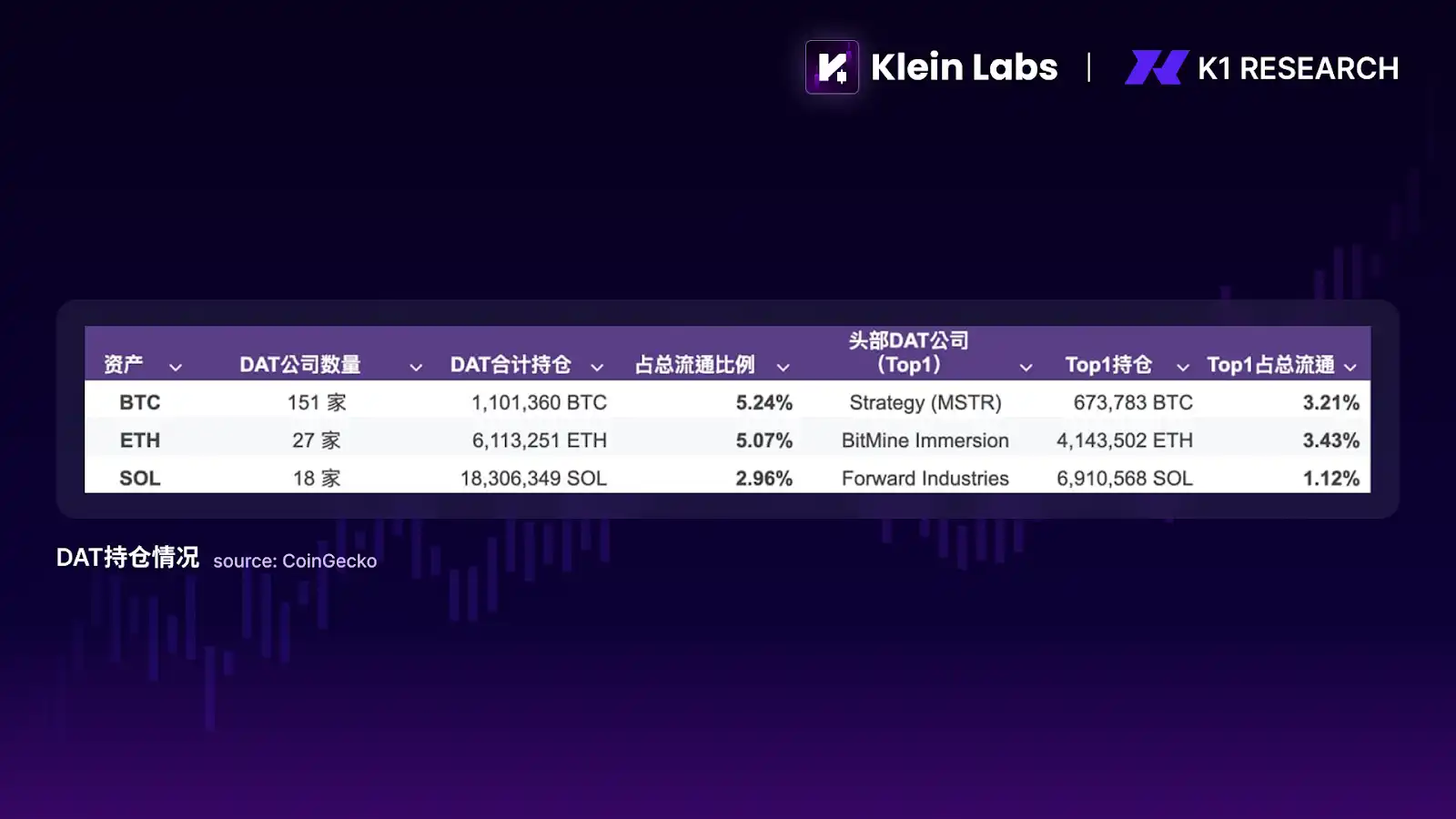

Equally noteworthy as ETFs is the rapidly emerging phenomenon of "coin-stock companies" DAT (Digital Asset Treasury Companies) in 2025: listed companies incorporate digital assets like BTC, ETH, and even SOL into their balance sheets and use capital market tools such as secondary offerings, convertible bond issuances, buybacks, and staking rewards to shape their stocks into "leveragable crypto exposure vehicles that can be financed." In terms of scale, nearly 200 companies have disclosed adopting类似 DAT (similar DAT) strategies, collectively holding over $130 billion in digital assets. DAT has evolved from individual cases into a class of trackable capital market structure. The structural significance of DAT lies in: like ETFs, it strengthens the capital absorption of mainstream assets, but its transmission mechanism is more "equitized"—capital enters the stock valuation and financing cycle, rather than directly entering the secondary liquidity of long-tail tokens, thereby further exacerbating the capital stratification between mainstream and alt assets.

Overall, the incremental capital in 2025 was not absent, but systematically flowed towards "compliant, low-volatility, long-term parking" channels.

3. Market Outcome: Structural Stratification Between Mainstream Assets and the Altcoin Market

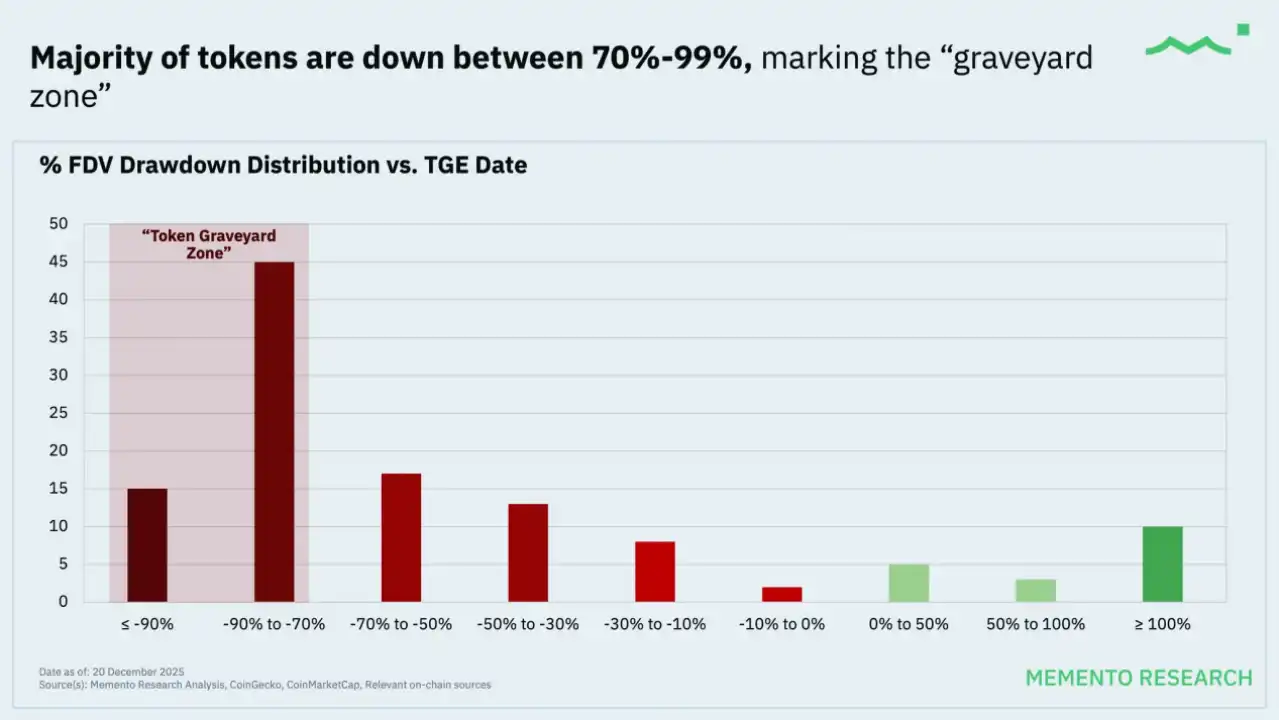

Looking at the final price outcome, the 2025 crypto market presented a highly counterintuitive but logically consistent state: the market did not collapse, but the vast majority of projects were in持续下跌 (continuous decline). According to Memento Research's statistics on 118 token launches in 2025, about 85% of tokens traded on secondary markets below their TGE price, with a median FDV drawdown exceeding 70%, and this performance did not significantly improve during subsequent market recovery phases.

2025 Token Issuance Situation source:MEMENTO RESEARCH

This phenomenon was not limited to尾部项目 (tail-end projects) but covered most small and mid-cap assets. Even some projects with high valuations at issuance and significant market attention significantly underperformed Bitcoin and Ethereum. Notably, even when calculated on an FDV-weighted basis, the overall performance was still significantly negative, meaning that larger projects with higher issuance valuations反而对市场形成更大拖累 (instead exerted a greater drag on the market). This result clearly indicates that the problem in 2025 was not "disappearing demand" but the directional migration of demand.

Against the backdrop of gradually clearer policies and regulatory environments, the capital structure of the crypto market is changing, but this change is not yet sufficient to completely replace the short-term dominance of narrative and sentiment on prices. Compared to past cycles, long-term capital and institutional funds began to enter assets and channels with compliant attributes and liquidity depth more selectively, such as mainstream coins, ETFs, stablecoins, and some low-risk RWAs. However, these funds acted more as "underlying absorbers" rather than short-term price engines.

At the same time, the main trading behavior in the market was still driven by high-frequency capital and sentiment, and the token supply side continued to use the issuance logic of the old cycle,持续扩张 (continuously expanding) under the assumption of a "universal bull market." The result was that the systemic "altseason" the market expected never materialized. New narratives could still receive short-term price feedback driven by sentiment, but they lacked the capital absorption capable of weathering volatile cycles. Price declines often occurred faster than narrative realization, leading to an obvious阶段性性与结构性错配 (phased and structural mismatch) in supply and demand.

It is under this dual structure that 2025 presented a new market state: at the large-cycle level, allocation logic began to concentrate towards mainstream coins and assets with institutional absorption capacity; at the short-cycle level, the crypto market remained a trading market driven by narrative and sentiment. Narrative did not fail, but its scope of effect was significantly compressed—it became more suitable for capturing sentiment fluctuations than for承载长期估值 (bearing long-term valuation).

Therefore, 2025 was not the end of narrative pricing, but the starting point where narratives began to be filtered by capital structure: prices still react to sentiment and stories, but only those assets that can attract long-term capital to stay after volatility can achieve true value沉淀 (sedimentation). In this sense, 2025 was more like a "transition period of pricing power" than an endgame.

Industry and Narrative: Key Directions Under Structural Stratification

1. Tokens with Real Yield: The First Sector to Adapt to Changes in Capital Structure

1.1 2025 Review: Yield-bearing Assets Become the Target of Capital Absorption

In an environment where narrative still dominates short-term prices but long-term capital begins to set absorption thresholds, tokens with real yield were the first to complete their adaptation to changes in capital structure. The reason this sector showed relative resilience in 2025 was not because its narrative was more attractive, but because it provided capital with a participation path that did not rely on持续情绪上行 (continuous sentiment rise)—even if prices stagnated, holding itself had a clear return logic. This change was first evident in the market acceptance of yield-bearing stablecoins. Represented by USDe, it gained rapid capital recognition not through complex narratives but through a clear, explainable yield structure. In 2025, the market cap of USDe once突破百亿美元 (broke through $10 billion), becoming the third-largest stablecoin after USDT and USDC. Its growth speed and scale were significantly faster than most risk assets during the same period. This result indicates that some capital已经开始将稳定币视为 (has begun to see stablecoins as) cash management tools rather than trading intermediaries. In the context of a high-interest-rate environment and gradually clearer regulatory boundaries, they began to stay on-chain long-term in the form of stablecoins. Its pricing logic也随之从 (accordingly shifted from) "whether it has narrative elasticity" to "whether the yield is real and sustainable." This does not mean the crypto market has fully entered a cash flow pricing stage, but it clearly shows: when narrative space is compressed, capital will优先选择 (prioritize) asset forms that can hold up without needing a story.

1.2 2026 Outlook: Capital Will Further Concentrate Towards Core Value Assets

When the market enters a phase of rapid decline or liquidity contraction, the so-called "assets worth watching" are essentially not about what narrative they tell, but whether they possess two types of pressure resistance: first, whether the protocol layer can truly continue to generate fees/revenue in a low-risk-preference environment; second, whether this revenue can form "weak support" for the token through buybacks, burns, fee switches, staking rewards, etc. Therefore, assets like BNB, SKY, HYPE, PUMP, ASTER, RAY, which have "more direct value capture mechanisms," are more likely to be prioritized for repair by capital during panic periods;而 (while) assets like ENA, PENDLE, ONDO, VIRTUAL, which have "clear functional positioning but greater differentiation in the intensity and stability of value capture," are more suitable for structural screening after a decline during sentiment recovery phases: those who can convert functional usage into sustained revenue and verifiable token absorption qualify to advance from "trading narratives" to "configurable targets."

DePIN is an extension of the real yield logic on a longer-term dimension. Unlike yield-bearing stablecoins and mature DeFi, the core of DePIN is not financial structure, but whether it can, through tokenized incentives, transform highly capital-intensive or inefficient infrastructure demands in the real world into sustainable distributed supply networks. The market completed preliminary screening in 2025: projects that could not prove they had cost advantages or relied heavily on subsidies to maintain operations quickly lost capital patience;而 DePIN projects capable of对接真实需求 (connecting with real demand) (computing power, storage, communication, AI inference, etc.) began to be seen as potential "revenue-generating infrastructure." At the current stage, DePIN is more like a direction that is重点观察 (closely watched) by capital against the backdrop of accelerating AI demand but has not yet been fully priced. Whether it can enter the mainstream pricing range in 2026 depends on whether real demand can be transformed into scalable, sustainable on-chain revenue.

Overall, the reason tokens with real yield became the first sector to be retained is not because they have entered a mature value investment stage, but because in an environment where narratives are filtered by capital structure and altseason is absent, they were the first to meet a very practical condition: giving capital a reason to stay without relying on continuous price appreciation. This also determines that the key question for this sector in 2026 will no longer be "whether there is a narrative," but "whether the yield still holds true after scaling."

2. AI and Robotics × Crypto: Key Variables in the Productivity Revolution

2.1 2025 Review: AI and Robotics Narrative Cools Down

If there was any sector that "failed" in terms of price in 2025 but became more important in the long-term sense, then AI and Robotics × Crypto is undoubtedly the most typical representative. Over the past year, DeAI's investment heat in primary and secondary markets明显降温 (significantly cooled down) compared to 2024. Related tokens overall underperformed mainstream assets, and narrative premiums were quickly compressed. But this cooling was not due to the direction itself failing, but because the productivity changes brought by AI are more reflected in the systematic improvement of production efficiency, and its pricing logic experienced a阶段性错位 (phased misalignment) with the crypto market's pricing mechanism.

From 2024 to 2025, a series of structural changes occurred within the AI industry: inference demand rose rapidly compared to training demand, the importance of post-training and data quality significantly increased, competition between open-source models intensified, and Agent economies began to move from concept to practical application. These changes collectively point to one fact—AI is transitioning from a "model capability competition" to a systems engineering phase of "computing power, data, collaboration, and settlement efficiency." And these are precisely the areas where blockchain could play a role in the long term: decentralized computing power and data markets, composable incentive mechanisms, and native value settlement and permission management.

2.2 2026 Outlook: Productivity Revolution Remains Key to Unlocking the Upper Limit of Narrative

Looking ahead to 2026, the significance of AI × Crypto is shifting. It is no longer a short-term narrative of "AI projects issuing tokens," but rather providing complementary infrastructure and coordination tools for the AI industry. Robotics × Crypto is the same; its true value lies not in the robots themselves, but in how to achieve automated management of identity, permissions, incentives, and settlement in multi-agent systems. As AI Agents and robotic systems gradually gain autonomous execution and collaboration capabilities, the friction of traditional centralized systems in permission allocation and cross-entity settlement becomes apparent, and on-chain mechanisms offer a potential solution path.

However, the reason this sector did not receive systematic pricing in 2025 lies precisely in its long productivity value realization cycle. Unlike DeFi or trading protocols, the business闭环 (closed loop) for AI and Robotics has not yet fully formed. Real demand is growing but difficult to transform into scalable, predictable on-chain revenue in the short term. Therefore, in the current market structure where "narratives are compressed and capital prefers absorbable assets," AI × Crypto is more like a direction that is持续跟踪 (continuously tracked) but has not yet entered the mainstream allocation range.

AI and Robotics × Crypto should be understood as a layered narrative: in the long term, DeAI is a potential productivity transformation infrastructure; in the medium to short term, protocol-level innovations represented by x402 may率先成为 (be the first to become) high-elasticity narratives反复验证 (repeatedly verified) by sentiment and capital. The core value of this sector lies not in whether it is immediately priced, but in the significantly higher上限 (upper limit) it can unlock once it enters the pricing range compared to traditional application narratives.

3. Prediction Markets and Perp DEX: Speculative Demand Reshaped by Institutions and Technology

3.1 2025 Review: Speculative Demand Remains Stable

In an environment where narratives are compressed and long-term capital is becoming more cautious, prediction markets and decentralized perpetual合约 (contract) exchanges (Perp DEX) became one of the few sectors that achieved counter-trend growth in 2025. The reason is not complicated: they承接 (absorb) the crypto market's most native and hardest-to-eliminate demand—pricing uncertainty and the demand for leveraged trading. Unlike most application narratives, these products do not "create new demand" but migrate existing demand.

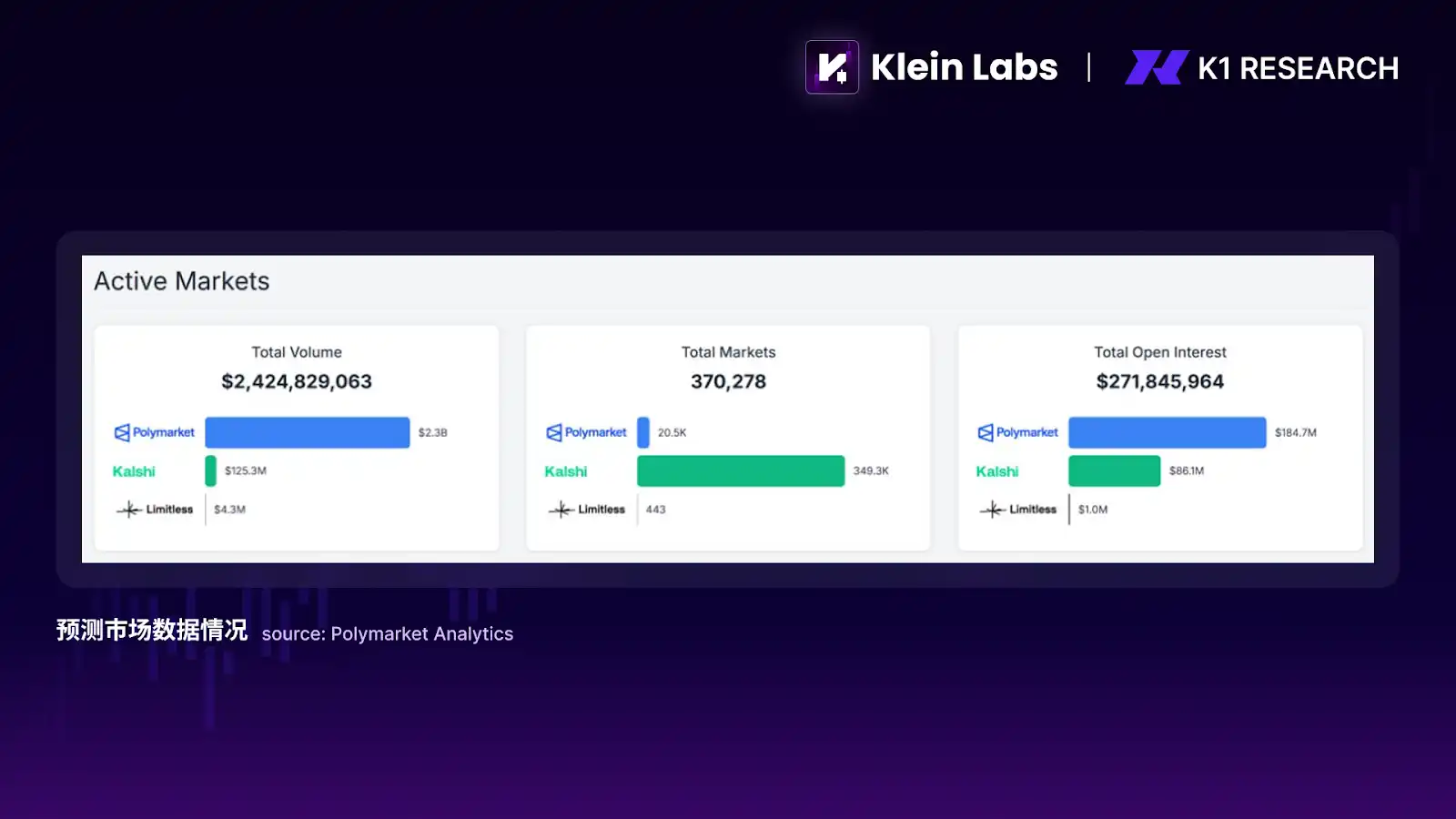

The essence of prediction markets is information aggregation. Capital "votes" on future events through betting行为 (behavior), and the price continuously corrects to approach collective consensus. Structurally, this is a naturally existing and relatively more compliant "casino form": there is no house manipulating odds, outcomes are determined by real-world events, and the platform only profits by charging fees. This sector's first high-profile appearance was during the US presidential election. Prediction markets围绕选举结果 (surrounding the election results) quickly gathered liquidity and public attention on-chain, elevating them from边缘 DeFi 产品 (fringe DeFi products) to a narrative direction with real influence. In 2025, this narrative did not fade but continued to发酵 (ferment) as infrastructure maturity improved and multiple protocol token issuance expectations arose. From a data perspective, prediction markets in 2025 were no longer小众实验 (niche experiments). The cumulative transaction volume of prediction markets had exceeded $2.4 billion. Meanwhile, the全市场未平仓合约 (total market Open Interest) remained at around $270 million, indicating this was not short-term博弈流量 (gaming traffic) but that there was truly capital持续承担 (continuously bearing) event outcome risk.

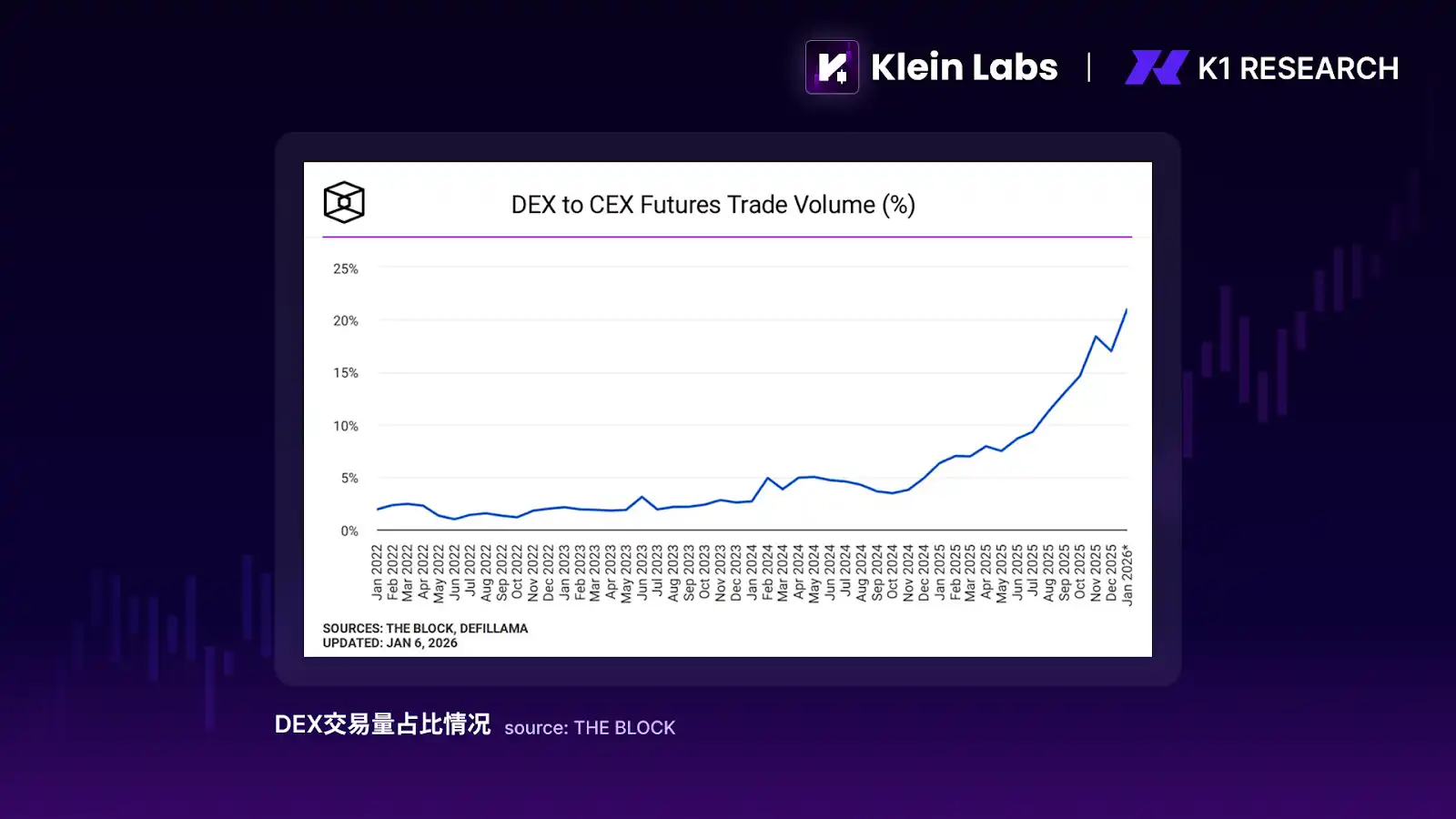

The rise of Perp DEX更直接地指向 (points more directly to) the core product form of the crypto industry—contract trading. Its significance does not lie in "whether on-chain is faster than off-chain," but in introducing an opaque, high-counterparty-risk contract market into a verifiable, liquidatable, trustless environment. Transparent positions, liquidation rules, and capital pool structures give Perp DEX security attributes different from centralized exchanges. However, it must be admitted that the vast majority of contract trading volume in 2025 was still concentrated on CEXs. This is not a trust issue but a result of efficiency and experience problems.

3.2 2026 Outlook: Institutions and Technology Will Determine If They Can Become Cross-Cycle Products

Looking ahead to 2026, Polymarket and Parcl's合作推出 (co-launch) of a real estate prediction market gives prediction markets the opportunity to reach a broader non-crypto user base and become a破圈应用 (breakout application). Furthermore, the World Cup, a global event with天然存在博弈 (inherent gambling), could极有可能成为 (very likely become) the next流量拐点 (traffic inflection point) for prediction markets. Additionally, a more important variable is the improvement in infrastructure maturity: continued improvement in liquidity depth, including market-making mechanisms, cross-event capital reuse capabilities, and price承载能力 (bearing capacity) for large orders; and the perfection of outcome adjudication and dispute resolution mechanisms. These two will determine whether prediction markets can evolve from "event-based gambling products" into a probability pricing infrastructure that can long-term承载 (bear) macro, political, financial, and social uncertainties. If the above conditions gradually mature, the upper limit of prediction markets will not be limited to short-term traffic but lie in whether they can become one of the few core application forms in the crypto system with跨周期生命力 (cross-cycle vitality).

Whether Perp DEX can continue to expand depends not on "whether it is decentralized," but on whether it can provide incremental value on the demand side that centralized platforms暂时无法给出 (temporarily cannot offer). For example, further improvement in capital usage efficiency: by deeply integrating unused contract margin with DeFi protocols, allowing it to participate in lending, market making, or yield strategies without significantly increasing liquidation risk, thereby improving overall capital utilization. If Perp DEX can unlock this type of structural innovation on top of safety and transparency, its competitiveness will no longer be just "safer" but "more efficient."

From a more macro perspective, the commonality between prediction markets and Perp DEX is: they do not rely on long-term narrative premiums but on repeatable, scalable speculative and trading demand. In an environment where narratives are filtered and altseason is absent, such sectors反而更容易获得 (are反而 more likely to receive) sustained attention. They may not be the first choice for long-term allocation capital, but they are highly likely to become the core stage in 2026 where sentiment capital, trading capital, and technological innovation repeatedly converge.

Summary

Reviewing the overall situation, 2025 was not a "failed bull market" but a deep reshaping围绕 (centering around) the pricing power, participant structure, and value sources of the crypto market. At the policy level, regulatory logic shifted from a highly uncertain state of suppression towards clear delineation of boundaries and functions; at the capital level, long-term capital did not directly return to high-volatility assets but first established compliant, auditable, low-volatility absorption channels through structural tools like ETFs, DAT, stablecoins, and low-risk RWAs; at the market level, the price mechanism underwent substantial changes, narrative diffusion no longer automatically triggered linear upward feedback, universal altseasons gradually failed, and structural differentiation became the norm.

But this does not mean that narrative itself has exited the market. On the contrary, on shorter time scales and in more局部赛道 (localized sectors), narrative and sentiment remain the most important trading drivers. The repeated activity in directions like prediction markets, Perp DEX, AI payments, and Meme indicates that the crypto market is still a highly speculative, decentralized information and risk gaming field. The difference is that these narratives are increasingly finding it difficult to沉淀为 (precipitate into) long-term valuation foundations across cycles. They are more like阶段性机会 (phased opportunities)围绕真实使用场景 (surrounding real use cases), trading demand, or risk expression that are constantly filtered by capital structure, quickly verified, and rapidly cleared.

Therefore, entering 2026, a more realistic and operational framework is taking shape: at the large-cycle level, the market will continue to concentrate towards mainstream assets and infrastructure with real utility, distribution capability, and institutional absorption capacity; at the small-cycle level, narrative is still worth participating in but no longer worth believing in. For investors, the key is no longer betting on the arrival of the "next full bull market," but more pragmatically judging which assets and sectors can not only survive in an environment of market contraction, regulatory constraints, and intensified competition but also率先获得弹性与定价权 (be the first to gain elasticity and pricing power) when sentiment warms and risk appetite is released in phases.