Original Author: Axis

Original Compilation: AididiaoJP, Foresight News

On March 15th, South Korea's financial regulator imposed a six-month partial suspension of business on the country's second-largest cryptocurrency exchange, Bithumb. English-language media reported this event as a routine compliance case involving anti-money laundering enforcement and regulatory crackdowns. However, most of these reports overlooked the more important underlying information.

In fact, this event is evolving into a market structure event occurring within one of the deepest fiat-backed liquidity pools in the on-chain financial system, with an impact far beyond South Korea's borders. Upbit and Bithumb together handle about 96% of South Korea's cryptocurrency trading volume. Bithumb's suspension is not only reshaping the operational landscape of the domestic market but also weakening the quality of signals this market has transmitted to global traders for years.

Overall, South Korean cryptocurrency users are active traders, but the system they operate in is shaped by capital controls, high exchange concentration, and persistent language barrier. The combined effect of these three factors is that price-related information often appears first locally in South Korea before being reflected in global markets, creating a window where the markets are briefly out of sync.

The reason global traders fail to receive news promptly is structural, not coincidental

South Korea is not a peripheral market but one of the most important markets globally for understanding where on-chain opportunities originate. The Korean Won is the second-largest fiat currency in global cryptocurrency trading by volume, with year-to-date trading volume of approximately $663 billion, accounting for nearly 30% of global fiat-to-crypto trading volume. Nearly one-third of South Korean adults hold digital assets, a rate twice that of the United States.

The current government, elected in June 2025, ran on one of the most explicitly pro-cryptocurrency platforms in political history. Since taking office, nearly half of the top 30 performing stocks on the Korea Composite Stock Price Index have been related to digital assets. The stock market quickly digested this signal, while the vast majority of the cryptocurrency community did not.

This is not a one-off market dislocation. South Korea's political and regulatory dynamics typically first appear in Korean-language media and local CT (Crypto Twitter), subsequently affecting KRW trading pairs on Upbit and Bithumb, and are only reported by English-language media hours to days later. The reverse process also exists: global macro changes originating in English-speaking markets often take a long time to be priced into local trading pairs. By the time the information is translated, the initial price reaction has usually already occurred.

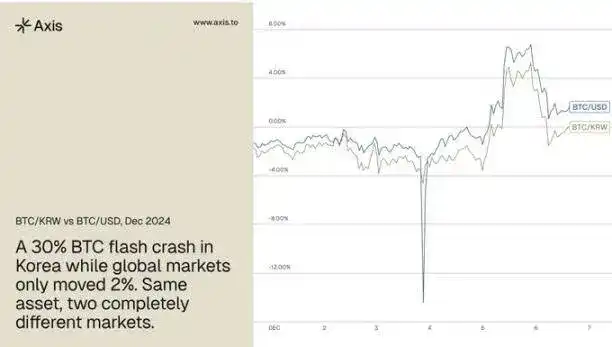

The clearest record occurred on December 3, 2024, when South Korean President Yoon Suk-yeol declared martial law. The price of Bitcoin in South Korea fell about 30% intraday, while the global price fell only about 2%, a difference of 28 percentage points, entirely triggered by domestic political shock. The total sell-off was approximately $33.3 billion, and the South Korean market once recorded the highest global trading volume. This event is a classic case of the typical unfolding of South Korean market dislocations.

At that time, buy-side liquidity quickly dried up, sell-side pressure accumulated, and the selling pressure was entirely concentrated on KRW trading pairs. Even stablecoins depegged, with USDT trading as low as $0.75 on South Korean exchanges, while Bitcoin and altcoins traded at discounts of 50% or more compared to global prices. Onshore users, believing they were selling into the last available liquidity, engaged in heavy market selling even though global prices barely moved. On-chain data showed arbitrageurs transferring millions of USDT per transaction to narrow the spread. Front-end systems of major exchanges crashed under traffic pressure, retail users couldn't log in to buy discounted assets, and only traders using APIs could execute trades during that window. By most measures, this was a significant and highly tradable event, but the window closed within hours.

The Bithumb suspension event is following the same pattern. It has been brewing in Korean-language information flows for weeks, but most English-speaking traders are only learning about it now.

The "Kimchi Premium" is widely tracked but often misunderstood

For traders without access to Korean-language information sources, the Kimchi Premium has been the most direct proxy for understanding South Korean market dynamics. This premium measures the gap between the price of cryptocurrencies denominated in Korean Won and the global price denominated in US Dollars. For this reason, experienced traders have long monitored KRW trading volume. The South Korean spot altcoin market is one of the highest volume markets globally and has historically been a reliable early indicator of broader market movements.

The problem is that most traders misinterpret this signal. The Kimchi Premium is widely seen as a measure of retail sentiment among Korean traders. While this is indeed part of it, the premium also reflects the intensity of structural capital pressures in a market where cross-border capital flows face regulatory friction. When this friction increases, pricing dislocations tend to widen accordingly.

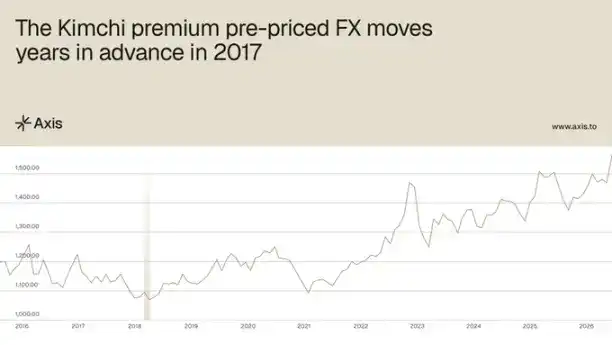

The historical record clearly illustrates this. As early as 2017, when the USD/KRW exchange rate was around 1060, the Kimchi Premium peaked at about 40%, implying an effective USDT/KRW rate of around 1480. Then in December 2024, the actual USD/KRW exchange rate broke through 1480. The Kimchi Premium had priced in this foreign exchange move years in advance. This information was encoded in publicly visible data but required结合 Korean market information flows to be interpreted correctly.

A persistent feature is that the Kimchi Premium does not naturally revert to zero. Research shows that as long as capital controls persist, Bitcoin's Kimchi Premium maintains a structural non-zero floor of approximately 1.24%. This means that when the premium compresses near this level, it often reflects changes in underlying capital pressures, not simply normalization. In 2025, periods where the premium approached zero were followed by positive returns for Bitcoin over both one-week and one-month time horizons: the average seven-day return was 1.7%, and the average thirty-day return was 6.2%. For traders, the important signal is not the absolute level of the Kimchi Premium, but its trend over time.

Bithumb's suspension makes Korean market dislocations harder to foresee, thus more asymmetric

The effectiveness of the Kimchi Premium as a signal depends on how price discovery is achieved among South Korean exchanges. When multiple trading venues compete to price the same capital flows, the resulting spreads tend to carry more information. As liquidity becomes more concentrated, this clarity begins to decline. Therefore, Bithumb's suspension is removing the competitive price discovery mechanism that the premium relies on.

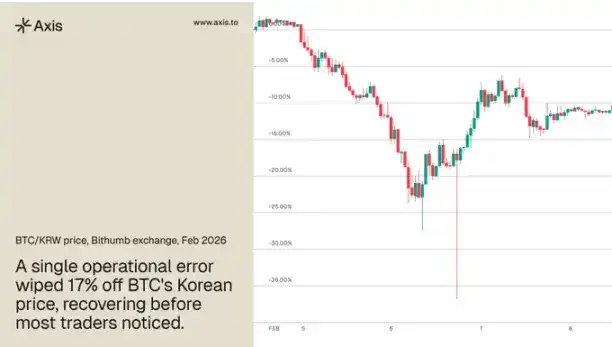

Following the announcement, capital rapidly migrated to Upbit, further deepening the concentration. In February 2026, Bithumb experienced an operational error, mistakenly crediting user accounts with 620,000 Bitcoin, causing a 17% flash crash in the BTC/KRW pair before prices recovered. This event vividly illustrates what happens when price discovery relies on a single trading venue operating under stress.

The degradation of the premium does not mean that Korean market dislocations stop occurring; it means these dislocations become harder to predict before they appear, thereby widening the information gap between participants who directly monitor the Korean market and those who rely on English-language reports.

Meanwhile, the underlying conditions that generate these dislocations are becoming more severe. In 2025, under strict trading rules, $110 billion worth of cryptocurrency flowed out of South Korea. Under the new government, capital that was previously structurally squeezed out is being reintroduced through new institutional channels, while the exchange infrastructure relied upon by retail flows is simultaneously being tightened. Historically, this kind of policy divergence has been the precursor to the most violent and short-lived dislocations produced by this market.

South Korea's market structure creates recurring information asymmetry for global traders

The Kimchi Premium is not an isolated phenomenon unique to the South Korean market. It is the most widely observed example of a mechanism that operates to some extent in every capital-controlled market where cryptocurrency has developed as a parallel financial channel. Both the December 2024 martial law event and the Bithumb suspension event illustrate the same dynamic. Dislocations in this market appear rapidly, reward participants with the right information sources, and disappear before the rest of the market catches up.

The traders who acted on December 3rd were not faster or smarter; they were monitoring the correct signals beforehand and understood how Korean political events map onto exchange-level price mechanisms, while the broader market was not yet aware of what was happening.

As stablecoin infrastructure deepens globally, more markets will produce the kind of capital pressure signals that South Korea has been releasing for the past decade. The challenge lies not in identifying the existence of these signals, but in building the infrastructure and discipline required to consistently capture them.