On December 10th, the high-performance public chain Sei announced a partnership with Xiaomi, the world's third-largest smartphone manufacturer. The Sei Foundation will develop a new generation of crypto wallets and a decentralized application (DApp) discovery platform, which will be pre-installed directly on Xiaomi's new smartphones targeting the global market (excluding Mainland China and the United States).

The two parties plan to utilize Multi-Party Computation (MPC) technology, allowing users to log into the wallet directly via their Google or Xiaomi accounts, eliminating the intimidating 'seed phrases' for average users. They also plan to pilot a stablecoin payment system in regions like Hong Kong and the European Union in the second quarter of 2026, enabling users to directly use tokens like USDC to purchase electronics at Xiaomi's over 20,000 offline retail stores.

Retrospective: The Seven-Year Evolution of Web3 Phones

First-Generation Attempts (2018–2020): Hardcore Security and Wild Imagination

Image source: Internet, compiled by AI

Around 2018, alongside the first major crypto market bull run, the first batch of 'blockchain phones' was born. The representatives of this era were Sirin Labs' Finney and HTC's Exodus 1, whose design philosophies were 'hardware sovereignty' and 'ultimate security'.

Taking Sirin Labs' Finney as an example, this phone featured a unique slide-out 'security screen' that used physical isolation specifically for displaying transaction details and entering passwords, ensuring funds remained safe even if the main system was compromised. HTC, in collaboration with Binance, developed the Exodus 1, introducing the 'Zion Vault', which utilized the phone chip's Trusted Execution Environment (TEE) to store private keys.

Besides Sirin and HTC, another device worth mentioning is the SikurPhone, which represented an attempt at a 'closed system' at the time. Launched by a Brazilian security company, the SikurPhone focused on being 'hacker-proof' and having a built-in cold wallet. Its extreme approach was running the highly closed SikurOS, which did not allow users to install third-party applications themselves (requiring manufacturer evaluation), thereby reducing the attack surface.

Beyond secure storage, entrepreneurs of the time had even more cyberpunk imaginations. Pundi X launched the Blok On Blok (BOB) phone, attempting to solve the problem of decentralized communication. This modular phone allowed users to switch between 'Android mode' and 'blockchain mode', claiming to enable calls and data transmission over a decentralized network without going through mobile carriers.

During this phase, Electroneum released the M1 phone priced at just $80. It targeted developing countries, allowing users to perform 'cloud mining' on the phone to earn tokens for paying phone bills. Although it didn't gain traction at the time due to poor user experience, it was actually the precursor to the later 'phone-as-a-miner' and JamboPhone models.

However, these devices ultimately could not escape commercial failure. The Finney was priced as high as $999 and had dismal sales, while Pundi X's decentralized communication failed to take off due to a lack of user base. The technological features of the time overly emphasized turning the phone into a 'cold wallet' or 'full node', which posed too high a barrier for ordinary users, resulting in products that only circulated within geek circles.

Mainstream Manufacturers Testing the Waters (2019–2022): Cautious Exploration

Image source: Internet, compiled by AI

Seeing the attempts of early startups, mainstream phone manufacturers began testing the waters in a more cautious manner. Samsung integrated the Samsung Blockchain Keystore into its Galaxy S10 series, theoretically giving tens of millions of flagship phone users a hardware-level encrypted wallet.

It is worth noting that Samsung actually laid the groundwork for 'buy a phone, get tokens' as early as 2019. In its 'KlaytnPhone' special edition of the Galaxy Note 10, Samsung partnered with the Korean internet giant Kakao to randomly include 2,000 KLAY tokens. This can be seen as the earliest雏形 (prototype) of the later successful Solana Saga model, although it was confined to the Korean market at the time and did not cause a global sensation.

This period also saw attempts targeting specific niche markets. For example, Vertu launched the Metavertu, priced at tens of thousands of dollars, promoting 'dual-system' switching and luxury services, aiming to attract crypto tycoons. HTC also pivoted to launch the Desire 22 Pro, focusing on the metaverse concept.

Although the involvement of major manufacturers brought better hardware experiences, the limitations of this stage were still evident: Web3 functions were often hidden in deep menus or used merely as marketing gimmicks, failing to fundamentally change user habits.

Besides the 'hardware wallet' attempts by big manufacturers (Samsung) and 'luxury gimmicks' (Vertu), this stage also saw a lightweight path of 'software-defined membership' with the Nothing Phone. Nothing Phone partnered with Polygon to establish a decentralized membership loyalty program through the 'Black Dot' NFT.

The New Wave (2023–2025): Ecosystem Binding and Infrastructure-ization

Image source: Internet, compiled by AI

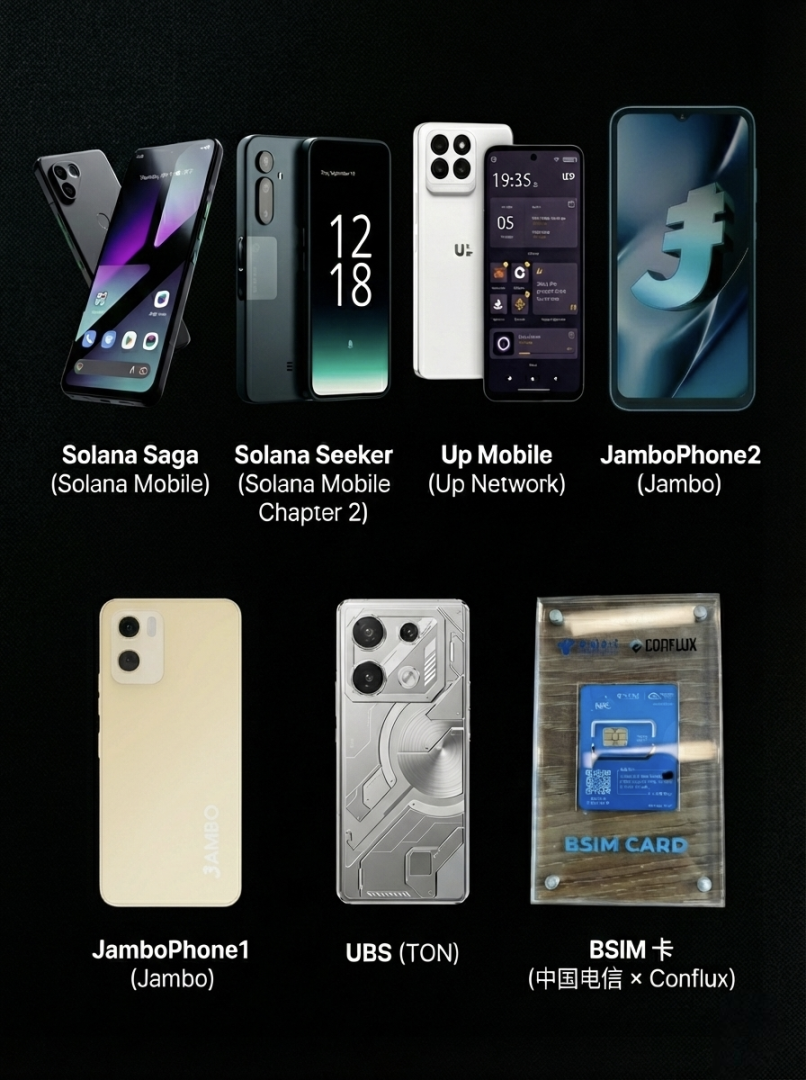

Entering 2023, the Web3 phone market was completely activated by the Solana Saga, ushering in a new era of 'ecosystem binding' and 'token incentives'. The Solana Saga initially had stagnant sales due to poor cost-performance, but after the value of the included BONK token airdrop exceeded the phone's price, it sold out instantly, earning the nickname 'dividend phone'.

The subsequent Solana Seeker (Chapter 2) continued this airdrop logic, using 'Soulbound Tokens' (SBT) to prevent scalping and introducing the TEEPIN architecture to support decentralized infrastructure networks.

Meanwhile, ecosystem competition intensified. The TON ecosystem launched the Universal Basic Smartphone (UBS), also priced at $99, directly challenging the JamboPhone. The TON phone leverages Telegram's massive user base, focusing on 'data dividends', allowing users not only to earn money by completing tasks but also to profit from selling their own data. Binance Labs-incubated Coral Phone also joined the fray, aiming to build a dedicated hardware entry point for the BNB Chain ecosystem, focusing on multi-chain aggregation and AI functions.

In the low-end market, the JamboPhone entered the arena with an ultra-low price of $99, serving as an entry point for 'super apps' and attracting users in Africa and Southeast Asia through a 'Learn to Earn' model. New players like Up Mobile also began to get a piece of the pie by combining AI and Move language technology. Jambo has already launched its second-generation product. While maintaining the $99 price, it upgraded the RAM to 12GB (although the processor remains entry-level), which is already capable of handling more Web3 tasks and 'super app' demands in emerging markets.

The BSIM card launched by China Telecom and Conflux showcased another path: a SIM card with a built-in high-performance security chip. Users simply need to replace their SIM card to transform any ordinary Android phone into a higher-security Web3 device. This 'Trojan Horse' strategy provides a new approach for large-scale adoption in compliant markets.

Trends: Shifts in Five Directions

Looking at the development over these eight years, we can clearly see five key shifts happening with Web3 phones.

Hardware capabilities and security architectures are upgrading. Early security relied mainly on software or simple TEE isolation, whereas now, technology is evolving towards more complex directions. Solana Seeker introduced the TEEPIN (Trusted Execution Environment Platform Infrastructure Network) architecture, enabling the phone to act as a trusted node participating in DePIN network construction. The BSIM card launched by China Telecom and Conflux integrates private key generation and storage directly into the SIM card, achieving telecom-grade hardware security. The collaboration between Xiaomi and Sei employs MPC technology, allowing users to log in with one click via their Google account, enabling secure management without seed phrases.

Ecosystem binding has become standard. Today's Web3 phones are not just generic crypto devices but entry points to specific public chain ecosystems. Saga is bound to Solana, Up Mobile is bound to Movement Labs, while JamboPhone, based on Aptos, further aggregates the Solana and Tether payment ecosystems, becoming a super app entry point for emerging markets. The phone has become a channel for public chains to distribute applications and retain users.

Airdrops or incentives dominate user growth. The motivation for users to buy Web3 phones has shifted from 'secure storage' to 'obtaining收益 (returns/profits)'. Saga's success proved that hardware can be used as a 'loss-leading' tool, compensating users with subsequent token airdrops or other incentives. This economic model of 'phone-as-a-miner' or 'phone-as-a-golden-shovel' has become the strongest driving force in the current market.

Application scenarios take precedence over technical concepts. Early products were obsessed with geeky functions like 'running a full node', while the current focus has shifted to practical applications. The core of the Xiaomi-Sei collaboration is stablecoin payments, and JamboPhone focuses on流量变现 (monetizing traffic) through built-in apps. Solving real payment and application distribution problems is more attractive than pure technological stacking.

Channel and scale effects are beginning to show. Selling 20,000 Solana Saga units was considered a huge success, but it's a drop in the bucket compared to Xiaomi's annual shipment volume of 168 million units. When a major manufacturer like Xiaomi starts pre-installing wallets via system updates, the growth scale of Web3 users will leap from 'ten-thousands' to 'hundreds of millions'. This scale effect is unmatched by any vertical crypto phone manufacturer.

Conclusion: Tearing Down the Walls, Integrating into the Mainstream

Throughout this eight-year evolution, we attempted to build expensive, closed Web3 phones as secure fortresses. But reality has proven that the real 'wall' hindering Web3 adoption is not security, but the complexity of seed phrases and the fragmented user experience.

Truly valuable Web3 phones will eventually no longer need to label themselves as 'Web3 phones'. They should be like today's 5G phones; you don't need to understand the underlying communication protocols, you just enjoy the high-speed experience they bring.

Solana Mobile proved that breaking through driven by利益 (interest/profit) is feasible, while SEI's partnership with Xiaomi is attempting to prove that integration driven by experience is the long-term solution. In this evolution from 'hardcore toy' to 'mass tool', whoever lowers the technical barrier of Web3 the most, whoever彻底推倒 (completely tears down) this cognitive wall, will hold the ticket to the next hundred-million user base.