Source: Tiger Research

Author: Ryan Yoon

Compiled and Edited by: BitpushNews

In February 2026, as the Iran attack incident escalated, the price of gold soared, while Bitcoin suffered a sharp decline. Can we still believe that Bitcoin is "digital gold"? This article explores the conditions Bitcoin must meet to become the "next generation gold".

Key Points

-

In every geopolitical crisis, gold rises while Bitcoin falls. After six tests, the data has never confirmed the "digital gold" narrative.

-

While governments are hoarding gold, they still exclude Bitcoin from their holdings. For investors, Bitcoin exhibits asymmetry: it falls with the stock market but fails to rebound in sync with it.

-

Three structural asymmetries hinder Bitcoin from gaining safe-haven asset status: excessive derivatives (market structure), dominance by leveraged traders (participant structure), and lack of a repeated behavioral record (behavioral accumulation).

-

Although Bitcoin is not a safe-haven asset, it is a "crisis utility asset" that proves useful in extreme environments where borders are closed and banks are shut down.

-

If these three asymmetries narrow, Bitcoin may no longer be a replica of gold but evolve into a new category—the "next generation gold". Generational shift and algorithmic adoption are variables that could accelerate this process.

1. Is Bitcoin Really "Digital Gold"?

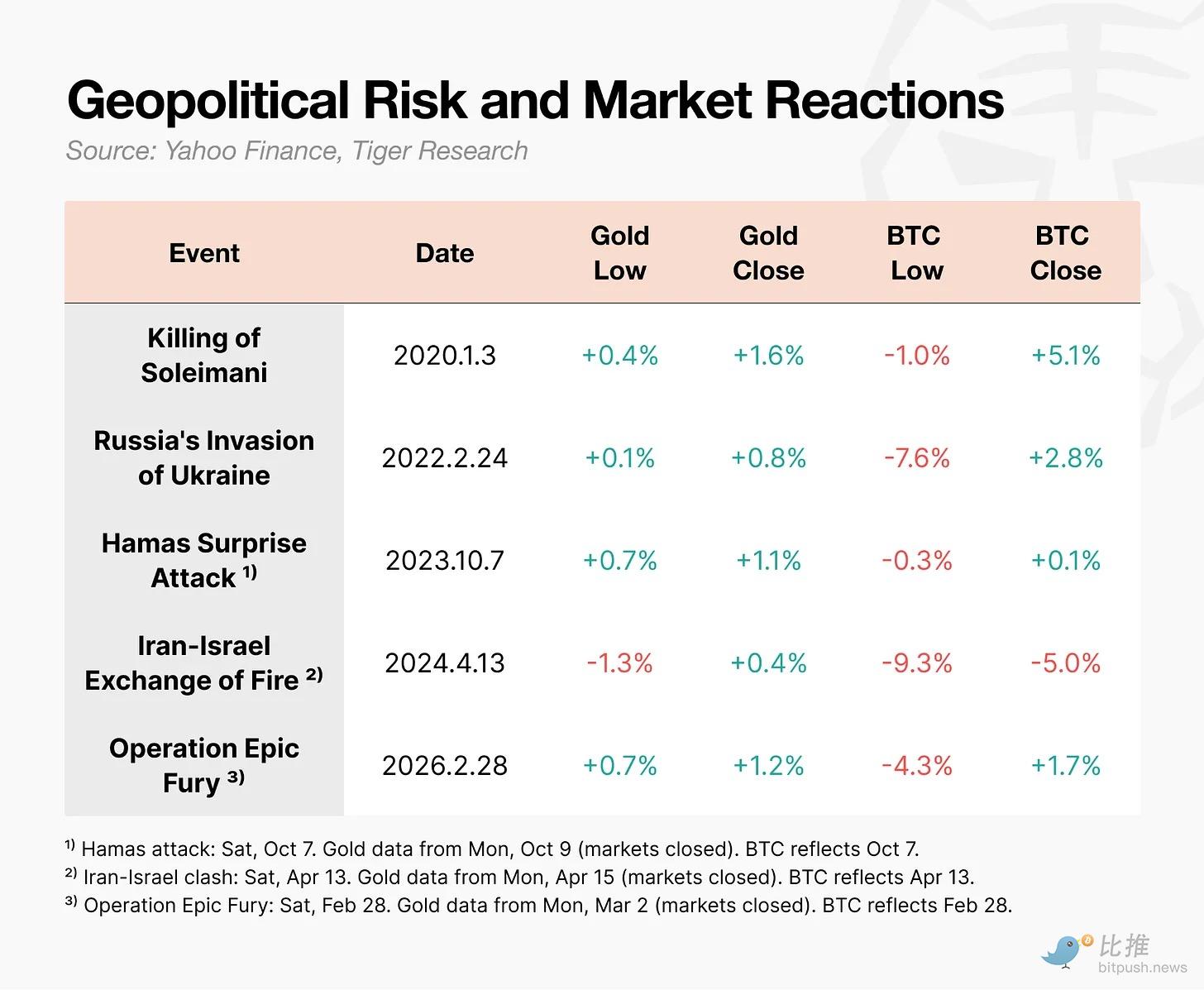

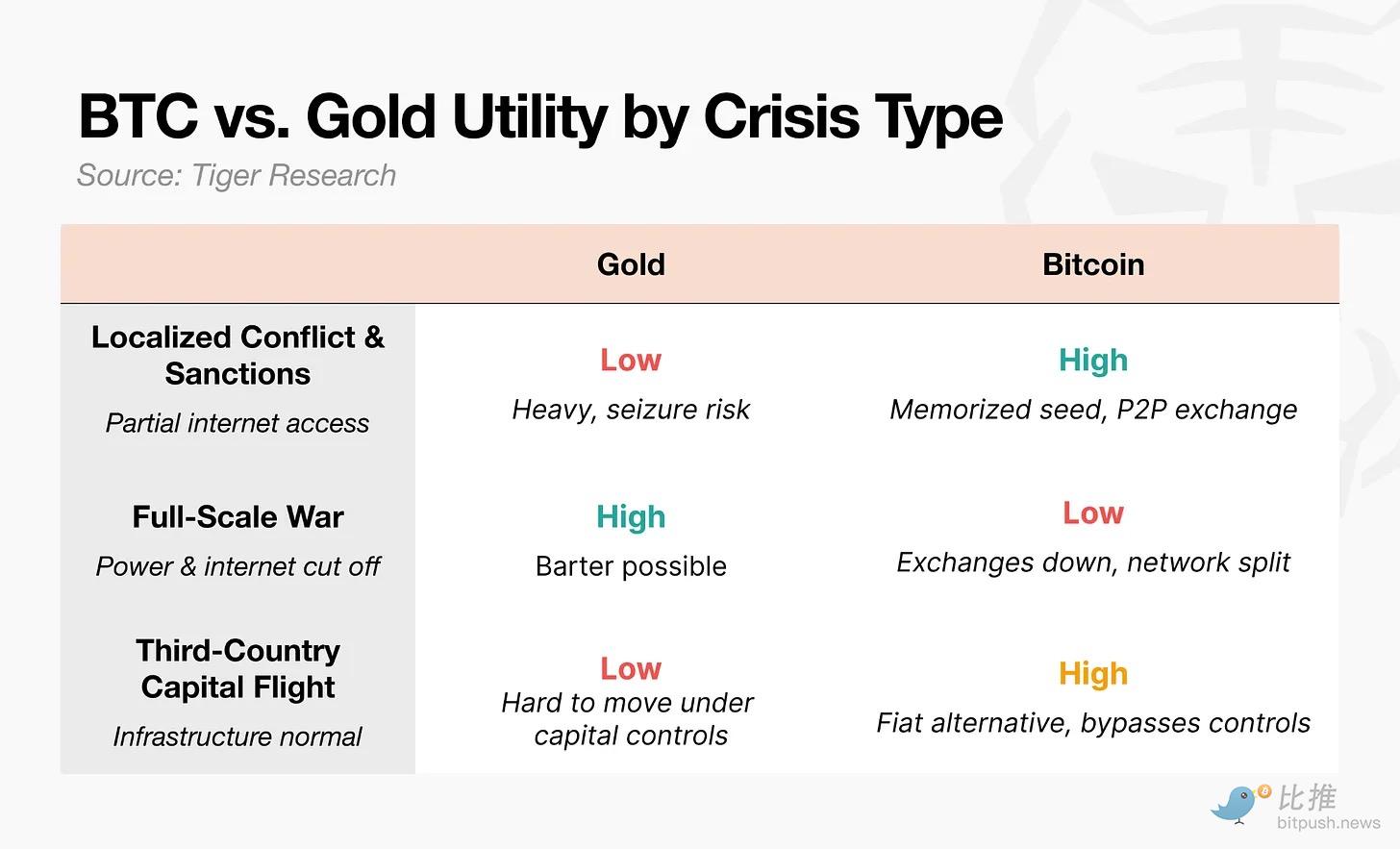

On February 28, 2026, the U.S. and Israel launched an attack on Iran. When "Operation Epic Fury" was announced, the price of gold immediately rose. In contrast, Bitcoin fell intraday to $63,000. Although it recovered within a day, its reaction was starkly different.

During geopolitical shocks like war, Bitcoin's performance completely diverges from gold. Although Bitcoin recovers quickly after the initial drop, chain liquidations by leveraged traders cause its decline to far exceed that of other assets. During the Iran-Israel conflict, its intraday drop reached -9.3%, while during the Ukraine war it was -7.6%. Meanwhile, gold was rising.

When an asset crashes first at the moment a crisis breaks out, can we really call it "digital gold"?

2. Bitcoin is Not "Digital Gold" for Nations or Investors

Bitcoin was not originally designed to be "digital gold". The title of Satoshi Nakamoto's 2008 whitepaper was "Bitcoin: A Peer-to-Peer Electronic Cash System". Its starting point was a transmission mechanism, not a store of value.

The "digital gold" narrative became popular during the 2020 zero-interest-rate and quantitative easing era. As concerns about currency devaluation peaked, Bitcoin gained attention as a store of value. But in practice, neither nations nor investors treat it as "digital gold".

2.1 National Level: Hoarding Gold, Only "Considering" Bitcoin

Data from the World Gold Council shows that central banks are increasing their gold holdings year by year. However, no major central bank includes Bitcoin in its official reserve assets.

Some counter that the U.S. formally established a "Strategic Bitcoin Reserve" via an executive order in March 2025. The order text even mentioned that "Bitcoin is often called 'digital gold'". But the details are crucial: its scope is limited to assets obtained through criminal and civil forfeiture. The government is not buying new Bitcoin; it is choosing to hold rather than sell seized assets.

Notably, as the appeal of U.S. debt declines, Europe and China are actively buying gold, but Bitcoin does not appear on their list of alternatives.

2.2 Investor Level: Falls with Declines, Doesn't Rise with Gains

The second half of 2025 was decisive. When the Nasdaq hit a record high, Bitcoin had plummeted more than 30% from its October peak of $125,000. The two began to decouple.

The real trouble isn't the decoupling itself, but the direction. Bitcoin fell in sync with the stock market decline but failed to rise when the market rebounded. For investors, this is the worst combination. There is no reason to hold an asset in a portfolio that only shares downside risk but misses out on upside gains.

3. Why Has Bitcoin Failed to Become "Digital Gold"?

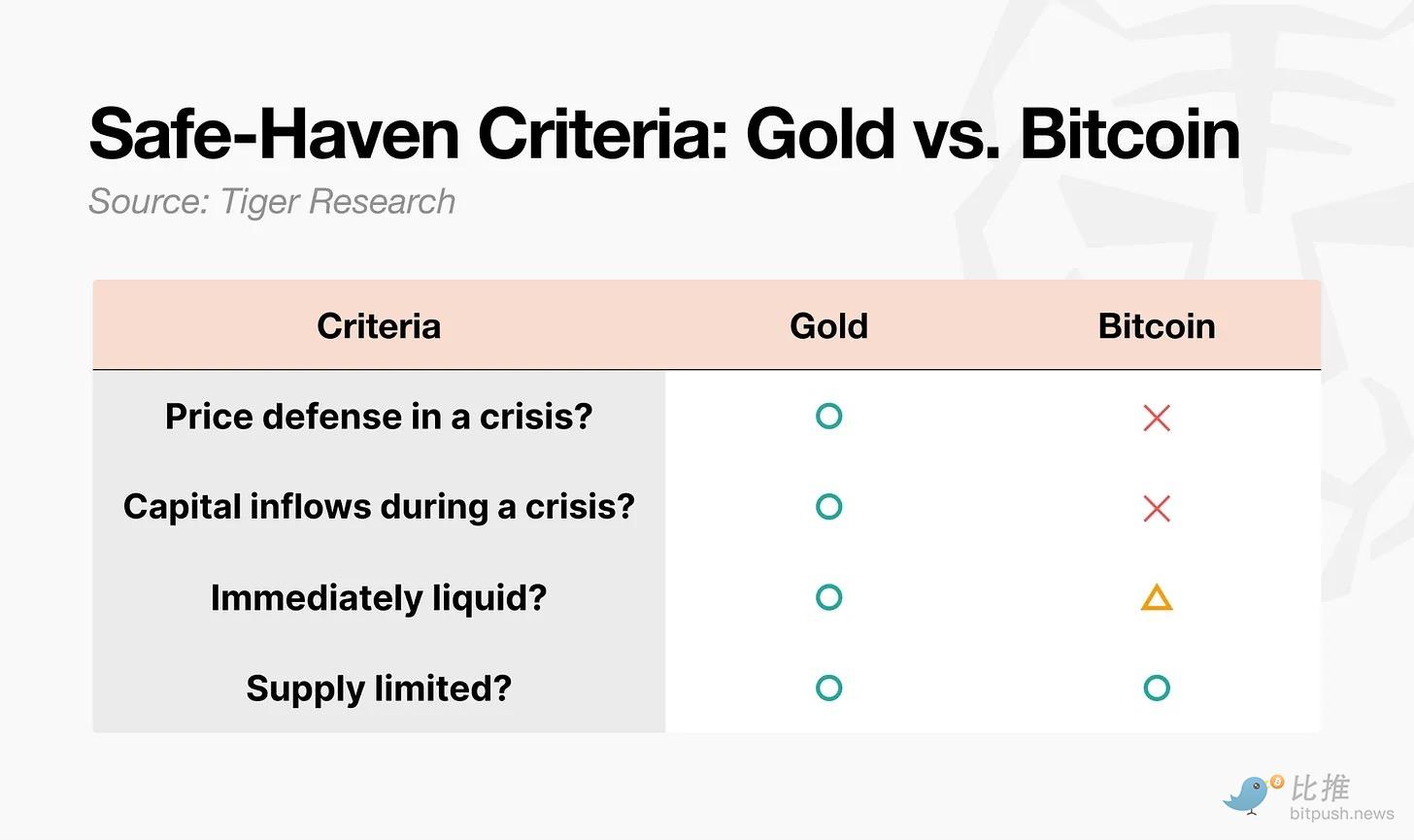

A safe-haven asset is not just one whose price rises. In academic definition, a safe-haven asset is one whose correlation with other assets drops to zero or turns negative during extreme market downturns. The key is whether its reaction in a crisis is predictable. Measured by this standard, the gap between gold and Bitcoin is evident.

Three structural asymmetries explain this gap:

-

Market Structure Asymmetry: Gold has physical demand supporting its price floor, and futures leverage is relatively low. Bitcoin's derivatives trading volume is about 6.5 times that of spot, and it trades 24/7, making it the first asset sold off when a crisis hits.

-

Participant Asymmetry: Gold's crisis buyers are patient capital (central banks, pension funds). The Bitcoin market is dominated by leveraged traders and hedge funds, which are the fastest to withdraw in a crisis.

-

Behavioral Accumulation Asymmetry: "Buy gold in times of crisis" is a behavioral pattern repeated for decades, becoming a formula. Bitcoin needs time to earn the same trust.

4. Not "Safe", But Proven "Useful"

In terms of safety, it's hard to call Bitcoin digital gold. But its utility in a crisis is real.

Ukraine (2022): After the war broke out, the Ukrainian central bank restricted electronic transfers and set withdrawal limits. Citizens couldn't access their deposits. Some refugees crossed borders with Bitcoin seed phrases stored on USB drives and exchanged them for local currency via Bitcoin ATMs or P2P transactions in Poland to sustain their lives.

UNHCR: Distributed the stablecoin USDC to displaced persons, allowing them to exchange it for cash at MoneyGram outlets.

Iran (2026): After "Operation Epic Fury", fund outflows from Iran's largest crypto exchange, Nobitex, surged by 700%.

These cases show people turn to Bitcoin not because it is safe, but because it works when the financial system fails.

In finance, a "safe-haven asset" means price resilience, which is a different concept from an "asset usable in a crisis". Bitcoin provides functional value for movement and transfer in wartime but cannot defend its price.

5. Bitcoin's "Next Generation Gold" Script

Although Bitcoin currently moves opposite to gold in every crisis, the path to "next generation gold" opens if the following three asymmetries narrow:

5.1 Market Structure Transformation

Derivatives trading volume being 6.5 times spot is a trigger for chain liquidations. Recently, futures open interest has declined, and price discovery is shifting towards spot and ETFs. The real test is whether leverage will spiral out of control again in the next bull market.

5.2 Participant Shift (Generational Change)

After the spot ETF approval, institutional inflows made Bitcoin a mainstream asset. But this creates a paradox: the more institutional holdings, the more likely Bitcoin is to be sold off with the stock market in risk-aversion events.

There is an overlooked variable here: generational change. When Gen Z starts managing wealth, gold might seem like "their parents' safe haven". This generation's first investment account is often a crypto exchange. This instinctive behavioral shift could be more influential than institutional decisions.

5.3 Behavioral Accumulation Shift

Gold took about 50 years after the Nixon Shock to establish its status. Bitcoin might not need that long. Although the sixth test (Iran attack) result was again a drop followed by a rebound, the repetition of this pattern is building a belief that "it always comes back after a fall".

A more important variable is algorithms. Currently, a large amount of trading is executed by AI agents and algorithms. If a "buy Bitcoin in a crisis" strategy is embedded into algorithms, this pattern can form without the need for human psychological accumulation. Trust might be established in code before it is in humans.

Conclusion: Today's Bitcoin is not yet "digital gold". But if it can achieve transformation in market structure, participant composition, and behavioral accumulation on top of its utility, it will become the "next generation gold"—not a replica of gold, but the birth of a new category.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush