US inflation data did not change market expectations for the timing of the Federal Reserve's rate cuts. The three major US stock indices closed lower, US Treasuries fluctuated and ended little changed, the dollar strengthened to recoup yesterday's losses, while commodities and cryptocurrencies performed strongly.

According to Wall Street News, the US core CPI in December was only 2.6% year-on-year, matching a four-year low. Although core inflation cooled, it did not alter the key pricing for the Fed, with the interest rate market still betting on the next rate cut occurring in June this year. This means that the "good news" on inflation is not enough to secure more accommodative financial conditions.

Wall Street News mentioned that Nick Timiraos, the chief economic correspondent for the Wall Street Journal, known as the "new Fed whisperer," commented:

To resume rate cuts, Fed officials may need to see new evidence that labor market conditions are weakening or that price pressures are subsiding. The latter may require at least a few more months of inflation reports to be confirmed.

Consequently, the algorithmic buying triggered after the CPI data release quickly faded, and the benchmark US stock indices retreated and turned lower during European trading hours. The S&P index pulled back from its historical high. JPMorgan confirmed in its earnings report that investment banking revenue was below guidance, falling over 4% and dragging down the financial sector.

US Treasuries briefly strengthened after the CPI release but similarly failed to sustain the move. The 10-year Treasury yield ultimately ended largely flat around 4.17%, while the 2-year yield edged lower. Notably, as the yield curve steepened, bond market volatility decreased significantly.

The strengthening dollar recouped yesterday's losses, driving the USD/JPY pair significantly higher, with the exchange rate breaking through 159. Notably, the 10-year Japanese government bond yield rose 6 basis points. Analysis suggests the market is increasingly focusing on Japan's potential debt crisis. In particular, the potential for Sanae Takaichi to call an early election, and the risks associated with potential fiscal expansion, continue to weigh on the yen's exchange rate.

Despite the stronger dollar, spot gold once again hit a new historical high during the session, briefly surpassing $4600, before retreating slightly to close lower, though the overall structure remained intact. Silver maintained its strength, touching the $89 mark for the first time.Gold and Silver ratio fell to 52 times, hitting a new low since December 2012.

Analysis believes that, unlike previous precious metal rallies dominated by "inflation-interest rates," this round of gains resembles a repricing of macroeconomic uncertainties: ambiguous monetary policy prospects, deepening fiscal dominance, and ongoing geopolitical tensions are causing gold and silver to continue playing the role of a "hedge against systemic risks."

Commodity and cryptocurrency markets performed notably well. International crude oil prices continued to climb after the US President made hawkish remarks regarding Iran, with WTI crude prices breaking through $61. Cryptocurrencies also saw significant gains, with Bitcoin returning near its year-to-date high.

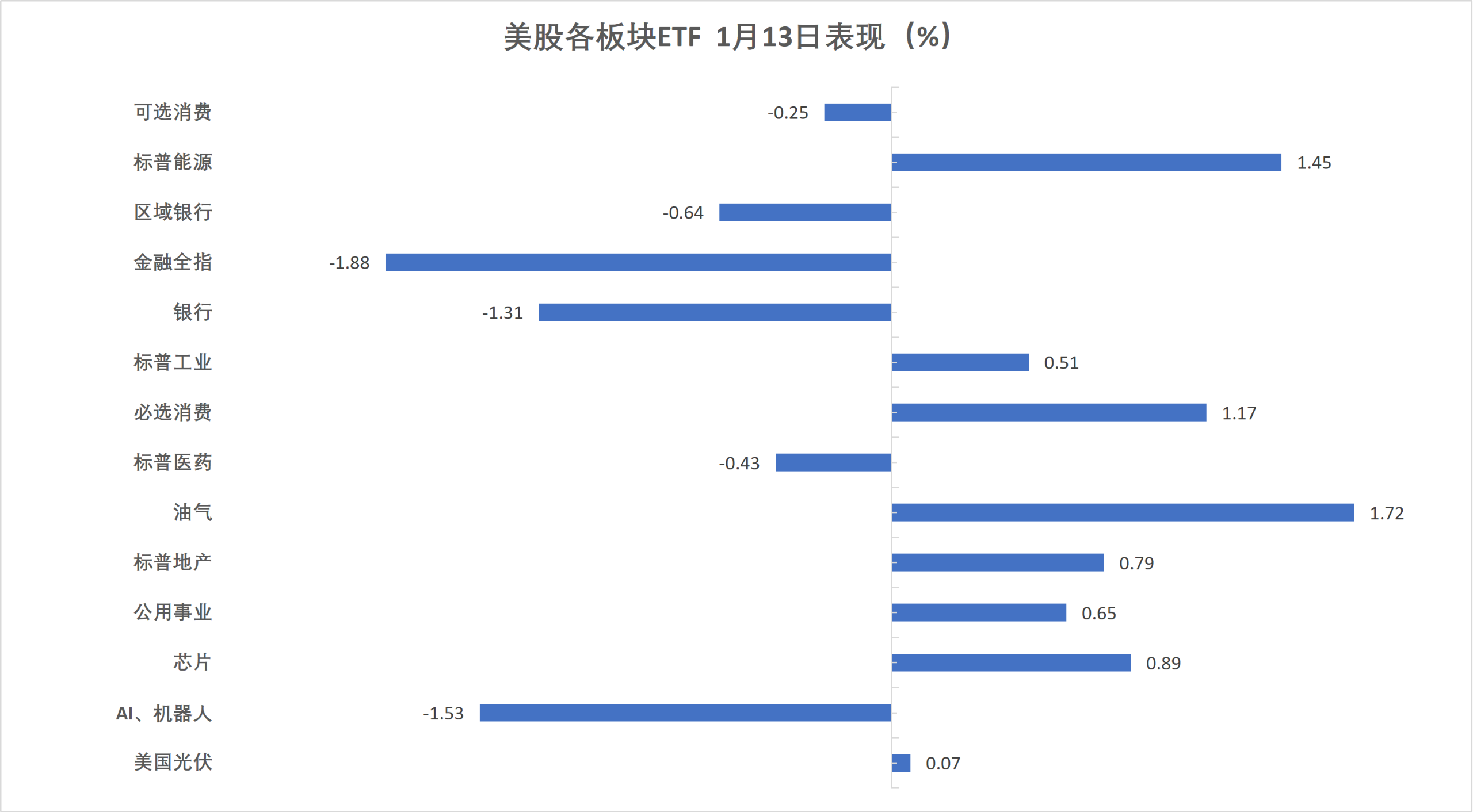

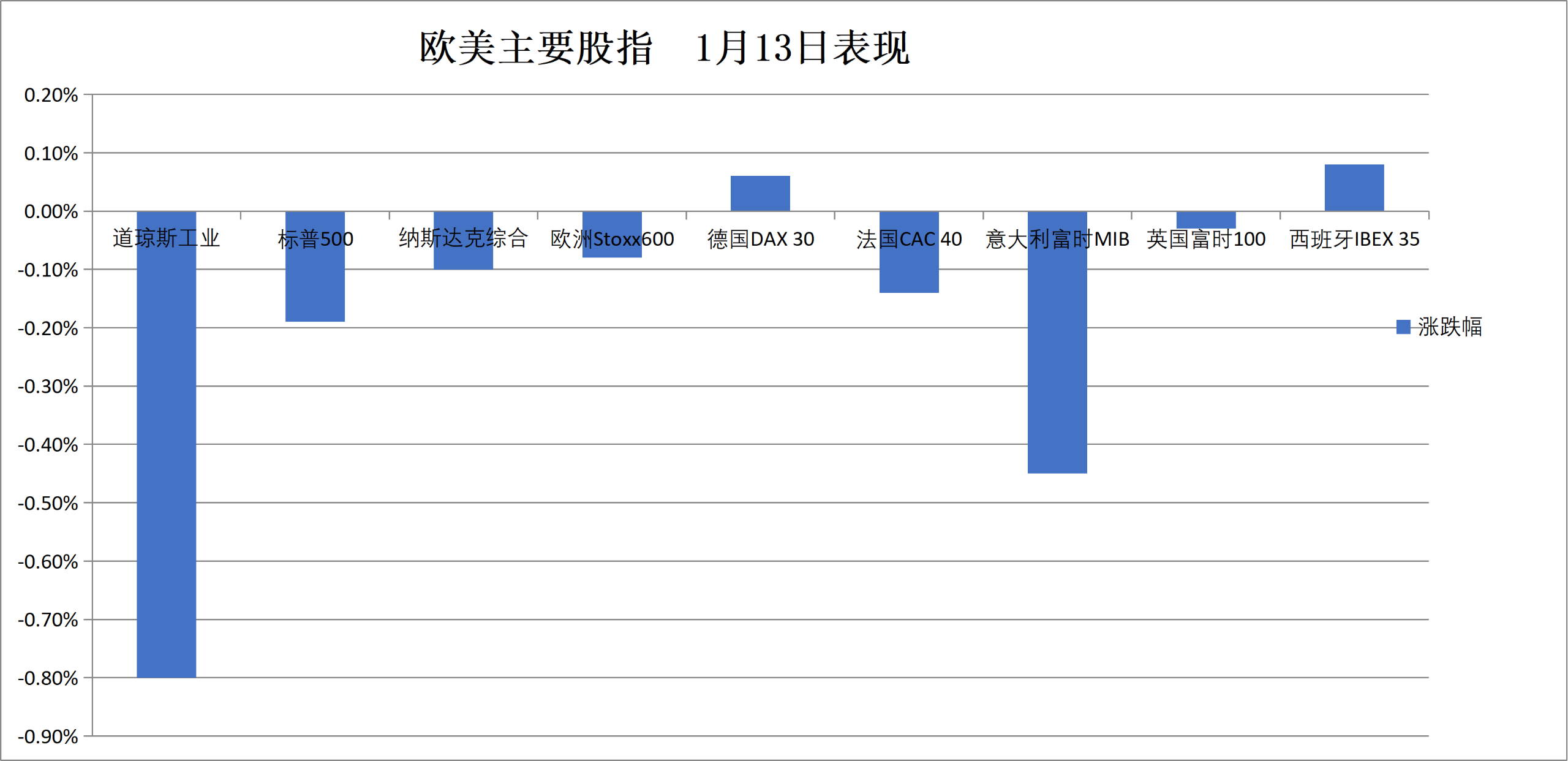

On Tuesday, the three major US stock indices closed lower, with the Dow down about 400 points and the Nasdaq down 0.1%. The Financial Select Sector ETF fell over 1.9%, leading the decline among US sector ETFs, while the S&P Energy sector rose over 1.5%.

US Benchmark Indices:

S&P 500 Index closed down 13.53 points, or 0.19%, at 6963.74 points.

Dow Jones Industrial Average closed down 398.21 points, or 0.80%, at 49191.99 points.

Nasdaq Composite closed down 24.032 points, or 0.10%, at 23709.873 points. Nasdaq 100 Index closed down 45.711 points, or 0.18%, at 25741.952 points.

Russell 2000 Index closed down 0.10%, at 2633.10 points.

CBOE Volatility Index (VIX) closed up 4.35%, at 15.12.

US Sector ETFs:

Financial Select Sector SPDR Fund (XLF) closed down 1.92%, U.S. Global Jets ETF (JETS) down 1.68%, SPDR S&P Bank ETF (KBE) down 0.94%, SPDR S&P Regional Banking ETF (KRE) down 0.66%.

(January 13th - US Sector ETFs Performance)Magnificent 7 Tech Stocks:

The Wind Magnificent 7 Index fell 0.22%.

Google (Alphabet) closed up 1.24%, Nvidia up 0.47%, Apple up 0.31%, Tesla down 0.39%, Microsoft down 1.36%, Amazon down 1.57%, Meta down 1.69%.

Chip Stocks:

PHLX Semiconductor Index (SOX) closed up 0.95%, at 7747.993 points.

TSMC ADR down 0.22%, AMD up 6.39%.

Chinese Stocks (US Listed):

Nasdaq Golden Dragon China Index closed down 1.86%, at 7874.82 points.

- Among popular Chinese stocks, Pony.ai fell 9.6%, Pinduoduo fell over 5%, Alibaba rose 0.4%.

Other Stocks:

Circle rose 0.72%.

Eurozone blue-chip index hit a closing record high for the third consecutive day. German stocks hit a closing record high for the seventh straight day, Danish stocks rose about 1%.

Pan-European Indices:

STOXX Europe 600 Index closed down 0.08%, at 610.44 points, retreating from its record closing high, showing a W-shaped pattern overall, after hitting a new intraday record high of 611.86 points early in the European session.

Euro STOXX 50 Index closed up 0.22%, at 6029.83 points, setting a record closing high for the third consecutive trading day.

National Indices:

German DAX 30 Index closed up 0.06%, at 25420.66 points, barely eking out its seventh consecutive record closing high.

French CAC 40 Index closed down 0.14%, at 8347.20 points.

UK FTSE 100 Index closed down 0.03%, at 10137.35 points.

(January 13th - Performance of Major European and US Indices)Sectors and Stocks:

Among Eurozone blue-chips, Argenx closed up 3.75%, TotalEnergies up 2.321%, Italian energy giant Eni up 2.15%, Safran up 2.13%, Infineon up 2.09%.

Among all components of the STOXX Europe 600 Index, Swiss Sika AG closed down 9.50%, Rockwool down 7.72% – Russia temporarily took over the company's assets in Russia; Vuzzi, which has operations in Russia, fell 7.16%, the third largest decliner.

Crude oil rose for the fourth consecutive day, with WTI crude prices briefly breaking through $61.

Crude Oil:

WTI February crude futures settled at $61.15/barrel.

(WTI Crude Oil Futures)

Brent March crude futures settled at $65.47/barrel.

Natural Gas:

NYMEX February natural gas futures settled at $3.4190/MMBtu.