Gold continues to surge to new highs while Bitcoin struggles to reclaim higher price levels, reinforcing a growing divergence across global markets. According to a recent CryptoQuant report, the current investment landscape has become a tale of two worlds.

On one side, precious metals and US equities are attracting consistent inflows as investors seek assets with clearer momentum and perceived stability. On the other hand, Bitcoin is showing signs of fatigue, with on-chain data signaling that the market is losing strength rather than preparing for an immediate recovery.

CryptoQuant highlights a concerning confluence of indicators that suggests the crypto market is entering a more fragile phase. While price remains relatively elevated compared to historical bear market levels, underlying metrics point to weakening demand and diminishing participation from key market segments. This disconnect implies that Bitcoin’s struggle is not purely technical, but structural, rooted in shifting capital preferences and risk appetite.

The contrast is striking. As gold benefits from macro uncertainty and equity markets push higher on liquidity expectations, Bitcoin appears caught in consolidation, unable to attract the same conviction-driven flows. This growing divergence raises important questions about Bitcoin’s role in the current cycle and whether it can reassert itself as a competitive asset amid tightening conditions and changing investor behavior.

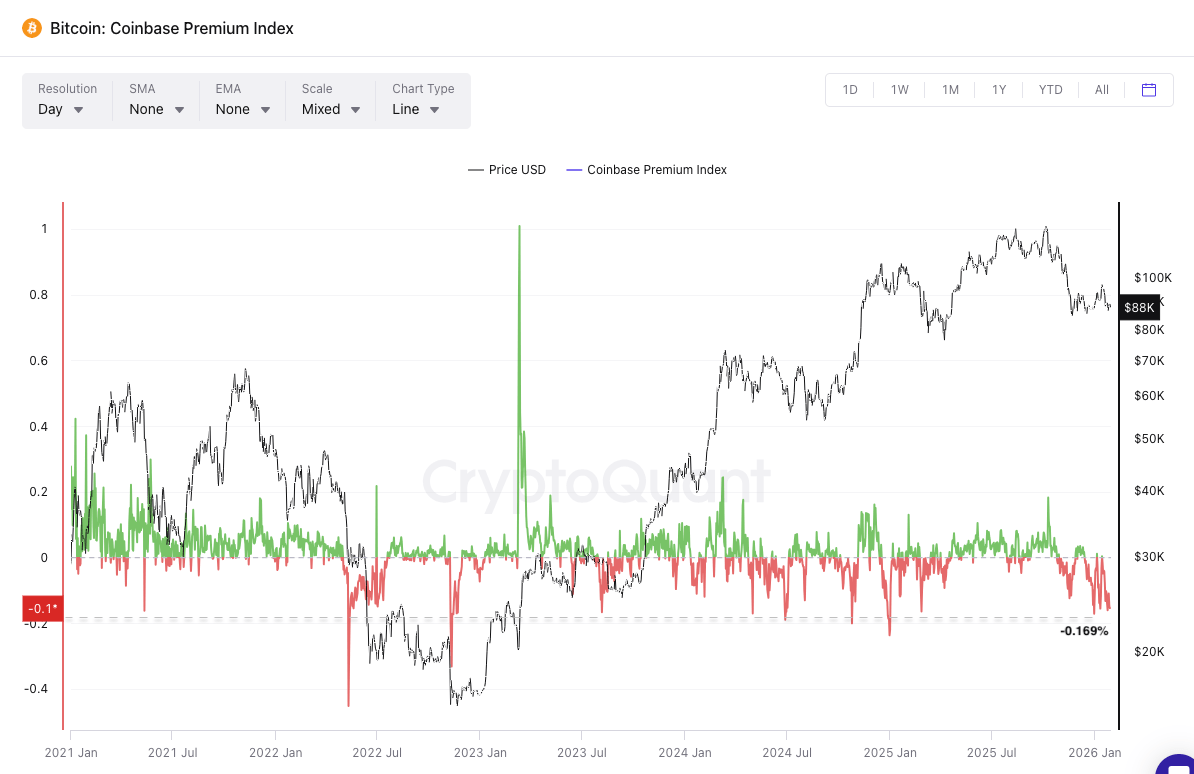

The report points to a clear institutional retreat that is weighing heavily on Bitcoin’s market structure. The Coinbase Premium Index, a key proxy for US institutional demand, remains deeply negative and recently reached a periodic low of -0.169%. This signals that selling pressure during US trading hours is materially stronger than the global average.

Notably, the index has turned positive only twice throughout January, reinforcing the view that institutions and high-net-worth participants are actively deleveraging rather than accumulating exposure. Historically, sustained negative premiums of this magnitude tend to coincide with phases of distribution, not early-stage recoveries.

Compounding this weakness is the evaporation of market “dry powder.” The combined market capitalization of the top 12 stablecoins has contracted by $2.24 billion recently, extending a peak-to-trough decline of roughly $5.6 billion.

This behavior differs from the typical rotation into stablecoins seen ahead of dip-buying phases. Instead, it reflects a more concerning dynamic: capital exiting the crypto ecosystem entirely and moving back into fiat. Without sidelined liquidity ready to re-enter, upside reactions become structurally weaker and short-lived.

Caught between institutional selling and shrinking liquidity, Bitcoin’s near-term bias remains skewed to the downside. In a bearish scenario, key levels to monitor include the True Mean Price near $81,000, the 2024 high around $70,000, and ultimately the 200-week moving average near $58,000.

Conversely, a bullish outcome would likely require an extended period of sideways consolidation, allowing overhead supply to be absorbed while stablecoin inflows recover and fresh capital gradually returns.