Original | Odaily Planet Daily (@OdailyChina)

Author|Golem(@web 3_golem)

On June 12th, US local time, Musk did not go to New York. Before SpaceX stock (Nasdaq: SPCX) officially listed on Nasdaq, he chose to stay at the company's Texas headquarters, standing among a group of employees to conduct a remote bell-ringing ceremony.

During this ceremony, Musk once again told SpaceX's story to a wider audience. He stated that the company's goal is to send humans to the Moon, Mars, and even more distant stars. After the bell ringing, Nasdaq's live channel played Elton John's "Rocketman," adding a romantic footnote to the most anticipated IPO in the history of space commercialization.

But the sentimental moments ended there, as the game of the capital market immediately began. The SpaceX IPO was priced at $135. On its first trading day, it opened at $150, surged to over $176 during the session, and finally closed at $160.95, with its market capitalization temporarily fixed at $2.1 trillion.

Opening at $150, First-Day Market Cap Settles at $2.1 Trillion

SpaceX's IPO has attracted global attention since it submitted its IPO registration information to the US SEC. The company ultimately decided to issue approximately 555.6 million Class A ordinary shares at a fixed price of $135, corresponding to a valuation of $1.77 trillion.

Regarding equity allocation, Musk personally holds about 42% of the shares, Valor Equity holds about 7.3%, Google holds about 5%, other early-stage venture capital firms collectively hold about 10-12%, and current and former employees hold about 10-15%. The shares offered in this IPO account for only 4.2% of the total. Although Musk and his surrounding interest groups hold the majority of SpaceX shares, their holdings cannot be sold immediately after the listing day. The lock-up period for core investors like Musk and Valor Equity is 366 days, while ordinary IPO shareholders (institutions and employees) also face a basic 180-day lock-up, meaning they cannot sell until at least the end of 2026.

Therefore, on June 12th, the initial trading day, the freely tradable shares consisted only of the approximately 555.6 million Class A ordinary shares offered in the IPO. SpaceX is a typical "low float, high FDV" project. According to its valuation model, the first-day free-float market cap was about $75 billion, roughly matching SpaceX's initially planned fundraising amount.

Investors familiar with crypto projects may not be strangers to high-control models. During the subscription phase, market sentiment quickly turned FOMO. Reports indicate SpaceX received over four times oversubscription, with combined institutional and retail subscription demand exceeding $250 billion. Retail investor subscription amounts alone surpassed $100 billion, far exceeding the $75 billion issue size. Crypto players certainly participated in this feast, but unfortunately, most ended up empty-handed.(Related reading:SpaceX On-Chain Subscription Dreams Shattered: Only 4 Shares in a Trillion-Dollar IPO Feast)

Notably, SpaceX unusually planned to allocate up to 30% of the IPO shares to retail investors, significantly lowering the participation barrier for this tech feast. Typically, such large IPOs allocate only 5% to 10% to retail investors. Although SpaceX ultimately allocated about 20%, it was still double the norm for regular IPOs.

The reason for this is that SpaceX management believes retail investors will hold their stock long-term, much like Tesla's core investor base now consists largely of retail investors. Essentially, they believe retail investors will buy into the dream Musk describes. However, this time, retail investors proved more rational than expected. (Detailed explanation below)

Before SPCX officially started trading on Nasdaq, its pre-market price on Hyperliquid fluctuated between $170-$175, corresponding to a company valuation exceeding $2.2 trillion. Before the official opening, during Nasdaq's pre-open auction, SPCX's opening indicative price was initially set at $172, representing an increase of about 29% over the IPO price, roughly matching pre-market expectations. However, an hour later, SPCX's opening indicative price quickly dropped, finally opening at $150, only about 11% above the IPO price.

According to Gate's US stock market data, SPCX rose to around $176 during the session and finally closed at $160.95, about 19% above the IPO price but only about 7.3% above the opening price. Its first-day market cap settled at $2.1 trillion. Judging by the results, SpaceX's first-day performance was undoubtedly successful. Musk became the world's first trillionaire. However, this outcome wasn't spectacular and even fell short of full market expectations.

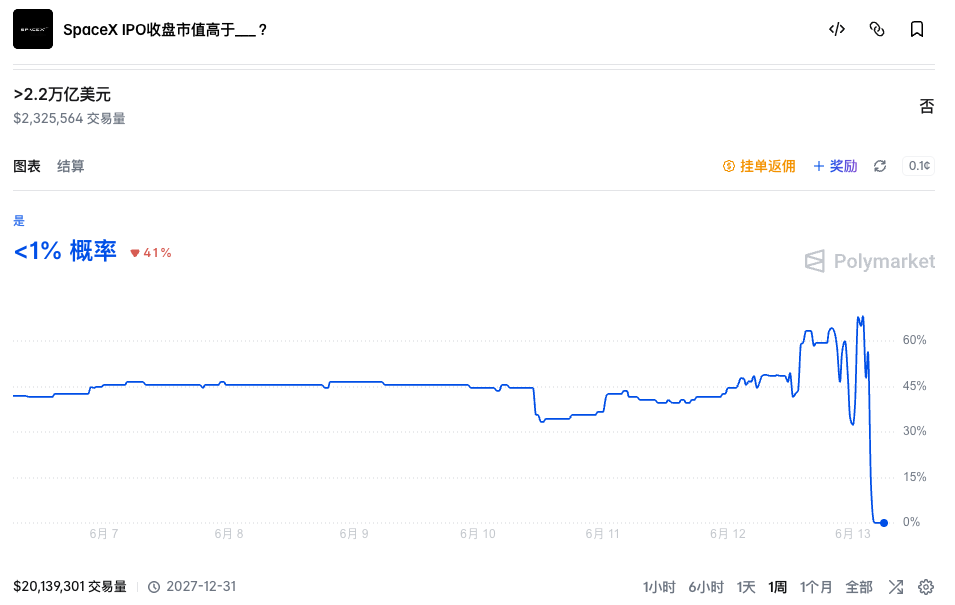

In pre-IPO pricing for SpaceX, not only did Pre-IPO platforms somewhat stumble, but prediction markets also weren't accurate. Hours before the SpaceX IPO, the market was generally optimistic that its market cap could exceed $2.2 trillion. On Polymarket, the probability of "SpaceX IPO closing market cap above $2.2 trillion" was still above 65%, once surging to 70%.

But as SPCX opened "relatively low," the probability for this event also began to fluctuate violently. Finally, the SpaceX IPO closing market cap settled around $2.1 trillion, and the event was settled as "No."

Retail Investors Affect Volatility, Not Gains

The reason for this phenomenon is simple: although the market is still willing to believe in SpaceX's narrative and the "Musk premium," SpaceX is just too expensive. At the right price, even the firmest convictions can be sold.

SpaceX is the first super behemoth in human history to directly descend upon the capital markets with a "trillion-dollar valuation," becoming the world's ninth-largest company by market cap on its first trading day, surpassing giants like Meta and Samsung. But even the craziest retail investors know that SpaceX's current revenue simply cannot support its massive valuation. SpaceX is still not profitable, with a net loss of $4.9 billion for full-year 2025 and a net loss of about $4.28 billion in Q1 2026.

Starlink is currently SpaceX's only profitable business. Prospectus data shows that Starlink generated $11.387 billion in revenue in 2025, accounting for 61% of SpaceX's total revenue, with operating profit of $4.423 billion. Its global user base exceeds 10.3 million, with over 9,600 satellites in orbit. In Q1 2026, it generated $3.257 billion in revenue and $1.188 billion in operating profit. However, this "cash cow" business is just a side venture for SpaceX.

Space launch is SpaceX's flagship. As of the prospectus disclosure, the Falcon rocket series has conducted over 650 launches with a success rate of 99%. Its reusable booster technology provides significant cost advantages and technological leadership within the industry. However, SpaceX's largest external customer for launch services is the US government, and this segment is still operating at a loss. In 2025, SpaceX's launch business recorded an operating loss of $657 million, with a loss margin of 16.1%. In Q1 2026, the operating loss surged to $662 million, with a loss margin of 107%.

The massive losses are due to increased investment related to Starship. However, based on current technological and application bottlenecks, Starship is still some distance away from true commercial-scale production.

Beyond these two businesses, SpaceX's still speculative space computing business is also part of its valuation framework. Compared to the more mature Starlink and launch businesses, Musk's claims about the space computing business seem a bit exaggerated.

SpaceX's plan can be simply understood as sending GPUs into low Earth orbit, using solar power to provide cloud computing capabilities for global AI computing clusters. Musk stated in the SpaceX prospectus that the company aims to deploy 100GW of AI computing capacity into orbit annually. Currently, the global AI industry's annual power demand is roughly in the 15-25GW range. This means SpaceX's planned orbital computing system could theoretically support today's global AI industry expanding about fivefold.

In case readers don't understand what 100GW means: The installed capacity of the Three Gorges Dam is about 22.5GW. That means the scale of one space computing center in Musk's plan is equivalent to 4.4 Three Gorges Dams operating at full capacity.

Moreover, SpaceX explicitly stated in the prospectus that its future (mainly AI-related) business could potentially unlock a $28.5 trillion market. For perspective, China, currently the world's second-largest economy, had a nominal GDP of approximately $19.4 trillion in 2025. The figure proposed by SpaceX is already equivalent to 1.47 times China's 2025 nominal GDP.

Reading this content makes one wonder if this is an IPO prospectus or a sci-fi essay. Even the most FOMO-driven investors need to cool down when seeing these numbers. Research firm CFRA gave SpaceX a "Sell" rating after its listing, with a target price of $115.

Besides the mismatch between actual business and valuation, the large proportion of IPO shares allocated to retail investors might also be a reason suppressing SPCX's stock price. Musk allocated 20-30% of the IPO shares to retail investors. A higher proportion of retail ownership inherently implies greater volatility. Retail investors can buy recklessly due to FOMO but can also sell emotionally at the slightest fluctuation. Therefore, retail investors truly affect volatility, not the final gains.

Important Upcoming Pivotal Moments

Whether you're watching from the sidelines or have already cashed out, the following three time points are particularly important for investors following SpaceX.

Approximately 15 Trading Days After IPO (Estimated around July 6th - July 7th)

This is the most important time point because SpaceX is expected to be directly included in the Nasdaq-100 index after about 15 trading days. In March, Nasdaq specifically revised its rules. Originally, newly listed companies had to wait three months to be eligible for index inclusion, but now they can be fast-tracked into the index after just 15 trading days if they meet the criteria. The requirement for at least about 10% free float was also removed. These new rules seem tailor-made for SpaceX and a subsequent wave of AI tech giants.

If successfully included in the index, it would mean over tens of billions of dollars in global passive funds would be forced to buy SpaceX stock, becoming a significant support for its price.So, if it's known that SpaceX has an extremely high probability of being included in the Nasdaq index in July, and top-tier funds will be buying the stock then, would you, as an investor, choose to buy now in advance and sell to them at a higher price later?

However, on the other hand, some US pension funds and long-term insurance funds have already expressed protest. In May 2026, three of the largest US public pension fund managers (managing over $1 trillion in assets) jointly wrote to Musk, expressing concerns about the risks passive funds might face due to rapid post-IPO index inclusion. In the same month, American Federation of Teachers President Randi Weingarten (representing about 1.8 million teachers, healthcare workers, and public sector employees) directly wrote to the SEC, requesting special scrutiny of the SpaceX IPO.

SpaceX Q2 Earnings Report (Mid-to-late August)

The second crucial time point is the release of SpaceX's Q2 2026 earnings report in August. This will be the first financial report SpaceX submits after going public. If the business shows no significant progress compared to the current state (realistically, major progress is unlikely so soon), its stock price may face further pressure.Furthermore, SpaceX's prospectus also stipulates that two days after the company announces its Q2 2026 earnings report, eligible insider shareholders (employees, former employees, some early investors) may sell a portion of their locked-up shares, up to 20% of their locked holdings. If the stock price has risen 30% above the IPO price at that time and meets this standard for 5 out of 10 trading days, an additional 10% may be unlocked.

This means that in August, the market will not only face volatility from SpaceX's earnings report but also the first major post-IPO share unlock, presenting a significant challenge.

Whether we will be "suffocated" by Musk's dream remains to be seen. At least judging from the first-day performance, the market chose to believe the story but didn't completely lose its rationality. What determines SpaceX's fate next is its own real performance.

Recommended Reading:

SpaceX On-Chain Subscription Dreams Shattered: Only 4 Shares in a Trillion-Dollar IPO Feast