Original Authors: Xu Qian, Jin Weilin

Introduction

In recent years, more and more people have earned considerable income through crypto asset trading, but many are still wondering: Do I need to pay taxes on money earned in anonymous wallets or on decentralized exchanges?

To put it directly: If you are a Chinese tax resident, in principle, you should declare and pay taxes to the Chinese tax authorities according to the law on income from crypto assets obtained through any channel.

How is a "Chinese Tax Resident" Defined?

According to the "Personal Income Tax Law of the People's Republic of China", an individual who meets any of the following conditions is considered a Chinese tax resident:

1. Has a domicile in China

Domicile: Refers to an individual who habitually resides in China due to household registration, family, main economic interests, or other reasons.

If your household registration (hukou) or family's center of gravity is in China, or your main life, work, and economic ties are in China, you may still be recognized as a tax resident even if you are often overseas.

2. Has resided in China for an aggregate of 183 days or more within a tax year

This is a clear time-based criterion. Even if you are a foreign national, as long as you reside in China for an aggregate of 183 days or more within one year, you are considered a Chinese tax resident.

Mankun Reminder:

Whether you are recognized as a tax resident due to "domicile" or "length of residence", once you meet the criteria, you need to declare and pay taxes to China on your worldwide income (including domestic and foreign income) according to the law.

Why Do Crypto Asset Profits Also Require Tax Payment?

Many people believe that since crypto assets are restricted domestically, the related profits are also "tax-free". This is a common misconception. Taxation focuses on whether you have income, not whether that income comes from an encouraged industry.

1. What is the nature of crypto assets?

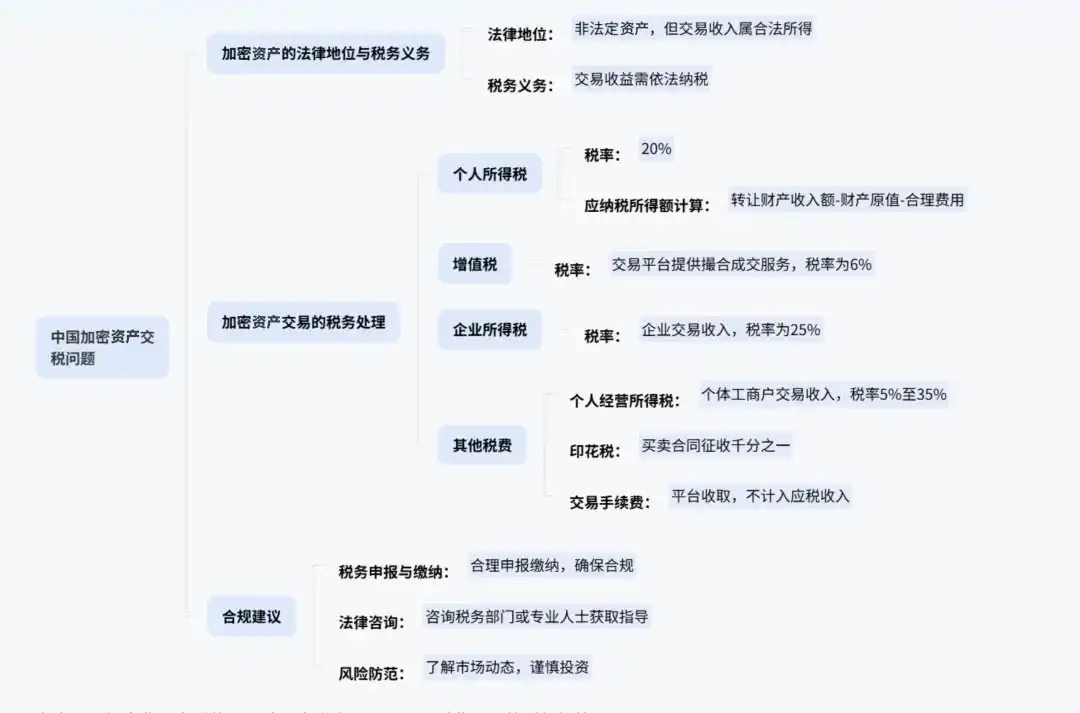

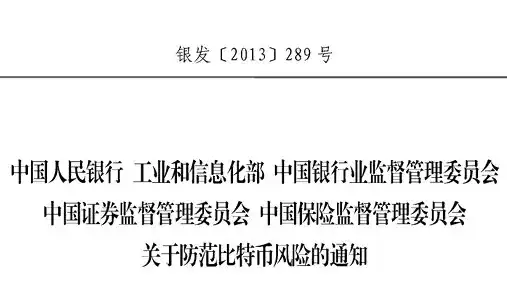

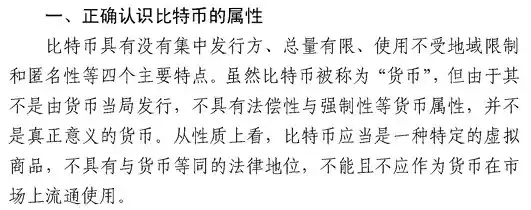

According to the "Notice on Preventing Bitcoin Risks" (Yin Fa [2013] No. 289) issued by the People's Bank of China and four other ministries, the "Announcement on Preventing Risks from Token Offering Financing" issued by the PBOC and six other ministries on September 4, 2017, and the "Notice on Further Preventing and Dealing with Virtual Currency Trading Speculation Risks" issued by the PBOC and nine other ministries on September 24, 2021, virtual currencies cannot be circulated as currency, but their property attributes as a "virtual commodity" are not denied. That is, the law recognizes them as tradable property.

2. What are the corresponding tax regulations?

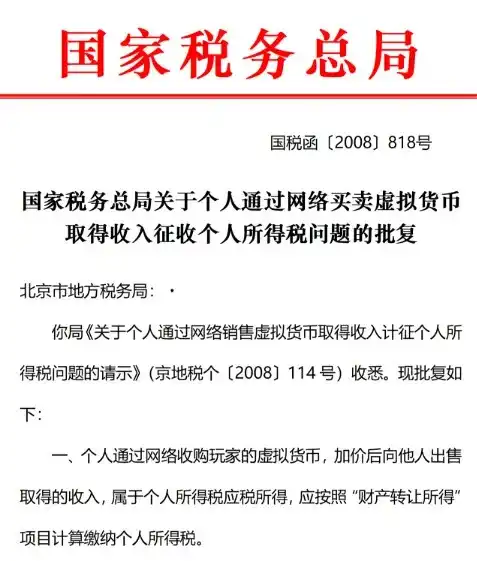

The "Reply of the State Administration of Taxation on the Levy of Personal Income Tax on Income Obtained by Individuals Buying and Selling Virtual Currency Online" (Guo Shui Han [2008] No. 818) clearly states: Income obtained by individuals from buying and selling virtual currency online belongs to "income from the transfer of property" and shall be subject to personal income tax according to the law.

3. Conclusion and Tax Rate

Therefore, regardless of which crypto asset you trade, as long as the transaction generates profit, this portion of the income is considered "income from the transfer of property" and should be subject to personal income tax at a rate of 20% according to the law.

In short: Taxation does not distinguish by industry; it only looks at income. Profits from crypto asset trading are considered income from property transfer and require declaration and payment of 20% personal income tax.

Do I Need to Declare Profits from Anonymous Wallets and DEX Trades?

Some investors believe that using decentralized wallets (like MetaMask) or trading on decentralized exchanges (like Uniswap) is anonymous and therefore untraceable by tax authorities. However, in the current regulatory and technological environment, this thinking carries significant risks.

1. The fund repatriation stage can still be traced

The vast majority of investors ultimately convert their crypto assets into fiat currency through OTC or compliant platforms and transfer it into domestic bank accounts.

Once funds enter the banking system, they fall under the purview of tax authorities. Transactions that are large in amount or high in frequency can easily trigger bank risk control systems, subsequently drawing attention from tax departments.

2. International tax information exchange mechanisms are now routine

China has joined the CRS (Common Reporting Standard) for the Automatic Exchange of Financial Account Information in Tax Matters, achieving automatic tax information exchange with over a hundred countries worldwide. If you have an account with an overseas exchange or bank, the relevant account information has likely already been exchanged back with the Chinese tax authorities.

3. "Golden Tax Project Phase IV" has strengthened data supervision capabilities

The "Golden Tax Phase IV" system utilizes big data, AI, and other technologies to achieve data linkage between tax, banking, customs, industry and commerce, and other departments. The system can automatically compare declared personal income with actual consumption and asset situations. Once a significant discrepancy is found, it triggers a tax warning.

Therefore, even if the trading activity occurs on-chain or overseas, as long as the final profits enter your name or are used for your living expenses in some form, there is a risk of being discovered by the tax authorities and being required to pay back taxes.

What Are the Consequences of Not Declaring Crypto Asset Income?

If the tax authorities discover that you have not declared income from overseas crypto assets, you may face the following legal consequences:

1. Back Taxes and Late Payment Surcharges

The tax authorities will order you to pay the taxes that should have been paid but were not, and, according to Article 32 of the "Law of the People's Republic of China on the Administration of Tax Collection", a late payment surcharge of 0.05% per day (approximately 18.25% annualized) will be added. The longer the time, the larger the accumulated amount.

2. Facing Tax Penalties

If deemed as "failure to file a tax return", a fine of up to RMB 2,000 may be imposed; if the circumstances are more severe, a fine between RMB 2,000 and RMB 10,000 may be imposed.

If deemed as "tax evasion" (refusing to declare or making false declarations after being notified), a fine of 50% to 5 times the amount of tax evaded or not paid will be imposed.

3. Possible Criminal Liability

If the amount of tax evaded is relatively large and accounts for more than 10% of the tax payable, and payment is still not made after the tax authorities have legally issued a recovery notice, it may constitute the crime of tax evasion, leading to criminal liability.

Mankun Reminder:

Not declaring crypto asset income may seem "hidden", but it actually carries multiple risks, from high late payment surcharges and substantial fines to potential criminal liability. We recommend proactive compliance and reporting to avoid subsequent legal and financial risks.

Mankun's Recommendations

If you have earned income from trading crypto assets, especially if funds have already been repatriated to domestic accounts, Mankun Law Firm recommends that you:

1. Proactively organize your transaction records

It is advisable to try to organize a clear transaction history, including the time, quantity, and price of purchases and sales, and focus on retaining proof that can demonstrate the "cost" of the assets, such as bank transfer records, exchange transaction details, on-chain transaction hashes, etc.

The more complete the cost documentation, the more accurate the calculation of taxable income, and the more reasonable the tax burden.

2. Consider proactive declaration or self-review

- If you have not yet received notice from the tax authorities, you can declare through the "Personal Income Tax" APP or on the Natural Person Electronic Tax Bureau website.

- According to regulations, the declaration should be submitted to the competent tax authority in the location of your employing unit; if you are not employed, you can file with the tax authority in your place of household registration, place of habitual residence, or place of main source of income.

- If you have already received reminders from the tax authorities via text message, phone call, etc., please cooperate actively, truthfully explain the source of funds, and prepare relevant supporting materials such as transaction records.

3. Retain all transaction vouchers

Develop the habit of long-term retention of transaction screenshots, wallet addresses, transfer records, exchange statements, and other materials. These are not only the basis for calculating taxes but also key evidence for explaining and proving the authenticity of transactions during tax inspections.

4. Plan reasonably within compliance boundaries

If your trading is frequent and involves large amounts, you might consider tax planning within the legal boundaries, such as managing assets through compliant structures or legally applying tax treaties. It is recommended to consult professional tax lawyers or accountants during this process to ensure the plan is sound and feasible.

Conclusion

In today's world intertwined with the digital economy and globalization, tax compliance has become a required course for every investor. Although the world of crypto assets has a "decentralized" flavor, tax obligations do not disappear because of it.

Proactively understanding regulations, truthfully declaring income, and properly retaining vouchers are not only a respect for the law but also long-term protection for your asset and credit security.

If you have questions or need assistance regarding crypto asset taxation, you can seek professional support early to ensure steady progress on a compliant track.