Author: Max.s

Original Title: Foreseeing 2026: Prospects of Quantitative Trading and How to Allocate Alternative Assets

After experiencing the extreme volatility of 2024 and the profound reshuffle of 2025, the quantitative finance industry stands at a new crossroads. At last week's 2025/2026 China Quantitative Investment New Year Summit, Dr. He Kang, Chief Strategist and Head of Financial Engineering at Huatai Securities Research Institute, delivered an in-depth speech titled "2025 Trends and 2026 Outlook for the Quantitative Industry." This is not just a strategic report on the A-share market; it is a field manual on how Alpha finds new survival space in an increasingly crowded market.

For practitioners at the intersection of Web3 and traditional finance, this report sends a clear signal: traditional Alpha is decaying, and new paradigms—whether the "Order as Token" based on large models or alternative assets represented by cryptocurrencies—are becoming must-haves for institutional investors.

Below is an in-depth review and industry outlook based on the content of Dr. He Kang's speech.

For the quantitative industry, 2025 was a year of both "high prosperity" and "high volatility." One notable data change is that while the scale of securities private equity remains high, the growth of public fund quant is even more rapid. By the third quarter of 2025, the scale of public fund index enhancement products had exceeded 200 billion yuan, with active quant strategies reaching 120 billion yuan.

Behind this lies an interesting structural change: the top player has changed.

The landscape of former leading players has been broken, with institutions like Bodo and Guojin rising rapidly through extremely flexible strategies. In Dr. He's research, these top-performing public quant funds are essentially "private funds in public fund clothing." They boast extremely high turnover rates, astonishingly fast strategy iteration speeds, and even rival top private funds in the use of intraday reversal (T+0) trading.

This phenomenon reveals the survival rule of 2025: as the difficulty of obtaining excess returns increases exponentially, only extreme flexibility can break through in a red ocean. For investors, the past logic of "choosing a big name and lying flat" is no longer applicable; they must use more refined attribution analysis to identify managers who truly possess "agile development" capabilities.

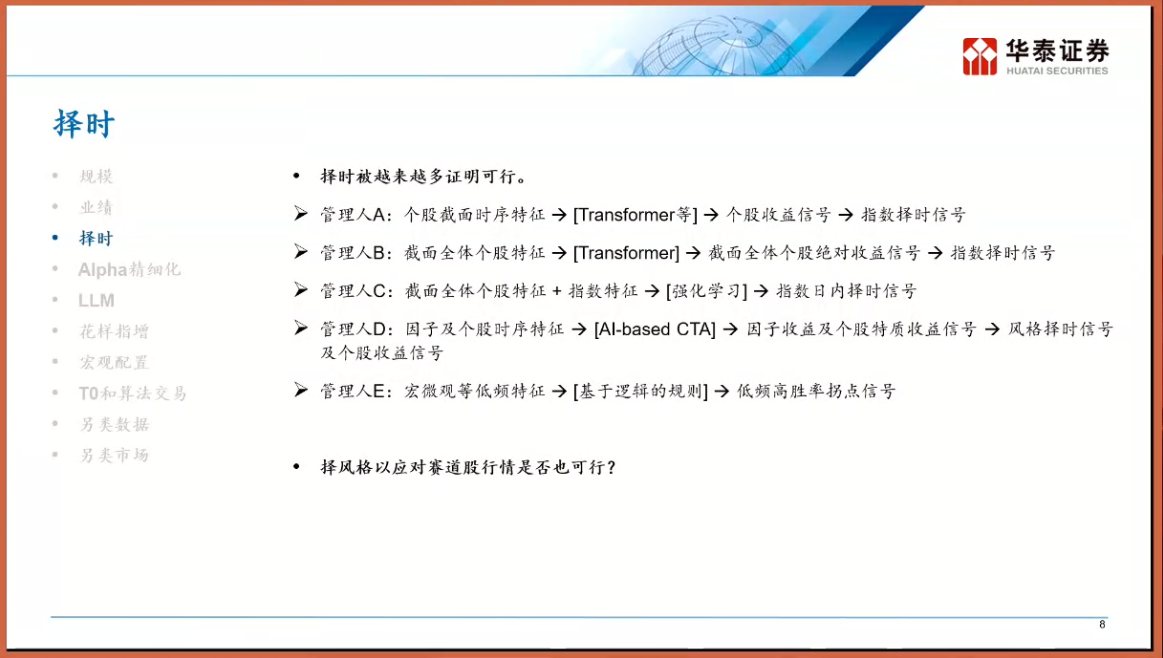

Over the past five years, the mainstream narrative of the quantitative industry has been "full position stock selection," using Alpha from the stock selection side to cover market fluctuations. However, after the market education of 2025, "timing" has returned to the center of the table. Dr. He Kang categorized managers in the market into five types, A through E, with the most noteworthy being Type E managers—those who time the market based on logical rules (Logic-based). Unlike black-box predictions, these strategies build explicit logical chains of "If A then B."

The rise of Sub-domain Modeling.

As market efficiency improves, factors applicable across the entire market are becoming increasingly difficult to unearth. Top managers have begun adopting a "divide and conquer" strategy: slicing the entire market stock universe into different "domains" such as growth, cyclical, small-cap, and micro-cap, and training models separately within each domain. This is akin to how in Web3, you cannot use the same logic to trade Bitcoin and on-chain Meme coins—their pricing logic, liquidity characteristics, and participant structures are completely different. Through sub-domain modeling, quantitative strategies can extract higher excess returns in local markets.

If sub-domain modeling is a tactical optimization, then the introduction of large language models (LLMs) is a strategic dimensional reduction strike. Dr. He Kang mentioned three application tiers for large models in quant, the most memorable being the third tier: treating financial trading as a language, i.e., "Order as Token."

In traditional NLP (Natural Language Processing), GPT predicts the next word (Token); in a financial large model, the input is the price series, trading volume, and order flow over a past period, and the model predicts the next "price Token." This is not just a technological migration but a revolution in thinking.

Traditional quantitative models are often based on linear or nonlinear regression in statistics, while the Transformer architecture allows models to capture extremely long-term dependencies and complex nonlinear patterns. Imagine future trading not being based on a linear weighting of a few factors, but a pre-trained financial large model "generating" future price paths, much like generating text. This shares similarities with the AI Agent trading logic based on Intent-centric approaches in the Crypto field—AI is no longer an auxiliary tool but the direct execution agent.

The Blue Ocean of Alternative Data: The Institutionalization of the Cryptocurrency Market

When excess returns in the A-share market are "competed" to the extreme, smart money begins to look towards alternative markets with lower correlation through total return swaps (TRS) or offshore entities.

Compared to the T+1 system and price limits of A-shares, the crypto market features 7*24 hour trading, T+0 settlement, high volatility, and fragmented liquidity. For quantitative institutions with high-frequency trading capabilities and risk control models, this is like the A-share market before 2015—Alpha is everywhere, and the competitive landscape is not yet solidified.

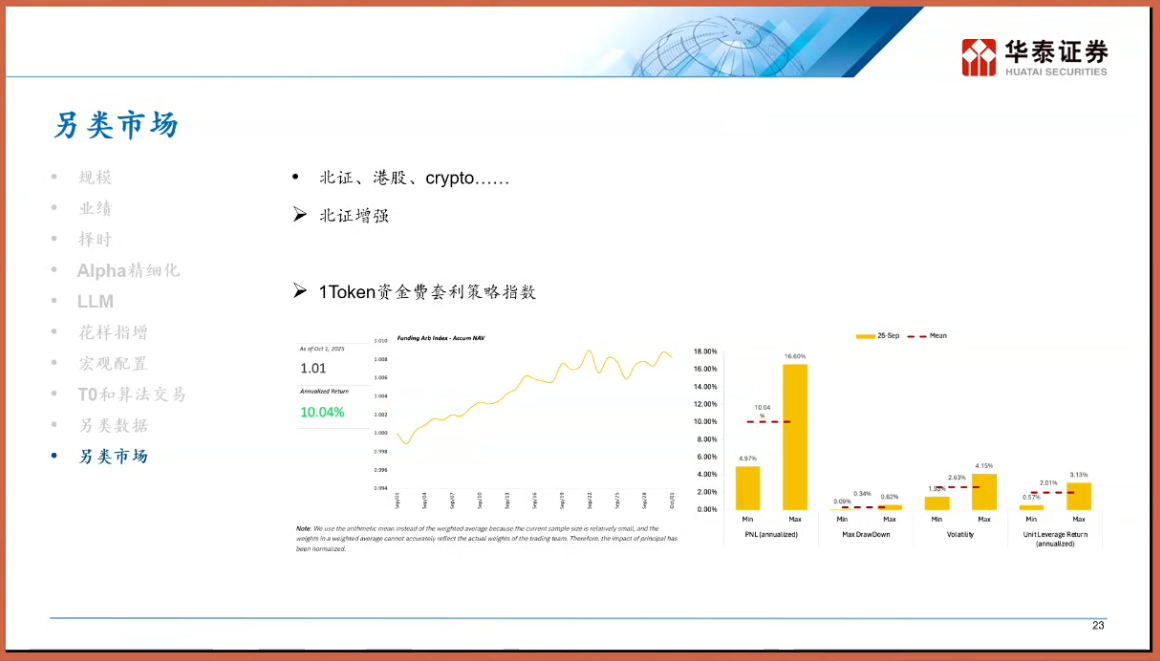

Here is a special introduction to the Funding Rate Arbitrage strategy. In the perpetual contract mechanism of the crypto market, long and short positions need to pay funding fees to maintain price anchoring. In a bull market cycle, longs often need to pay high fees to shorts. This creates a market-neutral strategy akin to fixed income: buy spot, short an equivalent value of perpetual contracts, hedging price volatility risk while steadily earning the funding rate. In this field, the 1Token Funding Rate Arbitrage Strategy Index has become an important industry bellwether.

According to industry data, such strategies' annualized returns in specific market cycles far exceed those of traditional fixed-income products, and their correlation with traditional assets (stocks, bonds) is extremely low. 1Token, as a professional digital asset institutional service provider, constructs indices that not only reflect the overall market arbitrage space but also embody the evolution of Crypto quant from "artisanal workshops" to "institutionalization and indexation."

For traditional finance practitioners, the significance of paying attention to indices like those from 1Token is that it provides a window to observe the Web3 liquidity premium. When funding rates remain high for a long time, it signifies extremely exuberant market sentiment and is a warning of spot selling pressure; conversely, it may be a good opportunity to buy the dip.

Looking ahead to 2026, the keywords given by Dr. He Kang are "Dynamic" and "Anti-fragile."

From Static Allocation to Dynamic Game Theory. In the past, doing FOF (Fund of Funds) or major asset allocation often involved setting a static weight (e.g., a 60/40 portfolio). But in the future, a dynamic adjustment mechanism must be introduced. For example, when the crowding degree of a certain strategy (e.g., micro-cap index enhancement) becomes too high, due to the "stampede risk" brought by homogenized trading, its weight must be actively reduced, even if its historical performance is excellent.

The "Airbag-ization" of Products. Having experienced the pain of drawdowns, investor aversion to downside risk has peaked. Derivative products with "airbag" or "snowball" structures, as well as index enhancement products protected by options, will become mainstream in 2026. This logic is identical to that of DeFi structured products—sacrificing a portion of potential upside gains in exchange for higher certainty and principal protection.

Finding Low-Correlation Assets. Whether seeking independent Alpha within A-shares or allocating to Hong Kong stocks, US stocks, or even Crypto assets, the core goal is to reduce the overall correlation of the portfolio. Dr. He Kang specifically mentioned that while making pure Alpha in Hong Kong stocks is difficult (poor liquidity, expensive shorting tools), its value as part of a diversified allocation still exists. And the Crypto market, with its unique driving logic, will become an important piece for hedging traditional financial risks.

Dr. He Kang's speech, in fact, reveals the essence of financial engineering: the process of finding certainty within uncertainty.

In the 2025 quantitative industry, the traditional low-hanging fruit has been picked. Practitioners face only two paths: either persevere technologically, using large models to mine deeper nonlinear patterns; or go overseas on the asset side, conducting dimensional reduction strikes in blue oceans like Crypto.

For Web3 natives, this is also a warning: as top institutions like Huatai Securities begin to deeply research and focus on this field, the entry of正规军 (regular army/institutional players) is only a matter of time. When traditional quantitative dragon-slaying skills are applied to decentralized trading markets, new红利 (dividends/opportunities) and new brutal competition will arrive simultaneously.

In 2026, whether in TradFi or Crypto, only the evolvers will survive.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush