Written by: Oluwapelumi Adejumo

Compiled by: Saoirse, Foresight News

For a long time, the profits in the stablecoin sector have been largely monopolized by stablecoin-issuing companies: these firms take in user cash, invest the reserves in short-term government bonds, and pocket the interest income. However, today, distribution channels responsible for stablecoin dissemination, which control user traffic, want a larger share of the profits. The birth of the Open USD (OUSD) project stems precisely from this conflict of interest. This stablecoin is being jointly established by over 140 financial, technology, and crypto companies, with Coinbase, Visa, Mastercard, Stripe, BlackRock, and Google listed among the alliance members.

The project offers free minting and redemption services to enterprises while designing a new reserve yield distribution mechanism that allocates the majority of the earnings directly to the channel platforms responsible for user acquisition and circulation expansion.

For Circle, the issuer of USDC, the most threatening name on this cooperation list is undoubtedly Coinbase. It was this exchange that allowed USDC to grow into one of the most widely circulated dollar stablecoins in the crypto market. Coinbase's Q1 financial report data shows that the platform holds over 25% of the circulating USDC, averaging around $19 billion; its Layer 2 network, Base, accounted for 62% of the global on-chain stablecoin transaction volume in a single quarter.

This means Coinbase's support for OUSD is far more than a superficial endorsement. Amid the escalating controversy over stablecoin yield distribution rules, Circle's most important distribution partner has turned around to invest in a competing stablecoin system.

The Cost Game of Channel Distribution

The official launch of the OUSD alliance directly shakes the existing market structure of the stablecoin market, which currently boasts a total market capitalization exceeding $320 billion. For a long time, companies like Circle and Tether, focused on issuing stablecoins, have maintained a high-profit model: all interest generated by the hundreds of billions in reserves backing the tokens is kept by the issuer.

However, as stablecoins evolve from mere speculative trading tools to the underlying infrastructure for global settlement and cross-border payments, channel enterprises with access to end-users are demanding a complete overhaul of the profit distribution system. OUSD directly addresses this pain point: it eliminates conventional minting and redemption fees and, at the mechanism level, returns the vast majority of reserve interest directly to distribution partners.

The market responded immediately: on the day of the alliance's announcement, Circle's stock price plummeted by 16%. This drop fully reflects investors' concern—the core business cooperation bond between Circle and Coinbase could break at any moment.

Their previous cooperation was mutually beneficial, but the divergence of interests has been deepening. In 2024, Circle paid Coinbase $908 million under a revenue-sharing agreement, sufficient proof that Coinbase is a crucial circulation and liquidity channel for USDC.

Public financial reports show that Coinbase's share of earnings from USDC far exceeds most market investors' expectations, confirming a fact: in the stablecoin industry chain, the voice of channel distribution has already surpassed that of pure issuance business. For the full year 2025, Coinbase's total revenue related to stablecoins was approximately $1.35 billion, accounting for 19% of the company's annual total revenue.

Coinbase becoming a founding member of OUSD is equivalent to holding a powerful alternative bargaining chip, as its current distribution agreement with Circle is approaching a critical juncture: their three-year contract is set to expire in August 2026. Tiger Research commented: participating in negotiations as a core builder of a competing stablecoin gives Coinbase extremely strong commercial leverage.

Coinbase CEO Brian Armstrong's public statement was brief, merely stating that the company "looks forward to promoting stablecoin adoption and innovating the global financial system." However, behind this business model lies an industry-wide consensus: platforms controlling distribution networks are no longer willing to watch the vast majority of interest income from reserves flow into issuers' pockets.

Circle Defends Its Mature Model

Circle does not agree with the argument that "channels can easily replicate existing mature networks" and has stepped forward to defend the USDC system. Circle CEO Jeremy Allaire posted a lengthy thread on platform X, elaborating on the advantages of the USDC ecosystem. He stated that stablecoins possess platform attributes and network effects, leading to a "winner-takes-most" dynamic in long-term development.

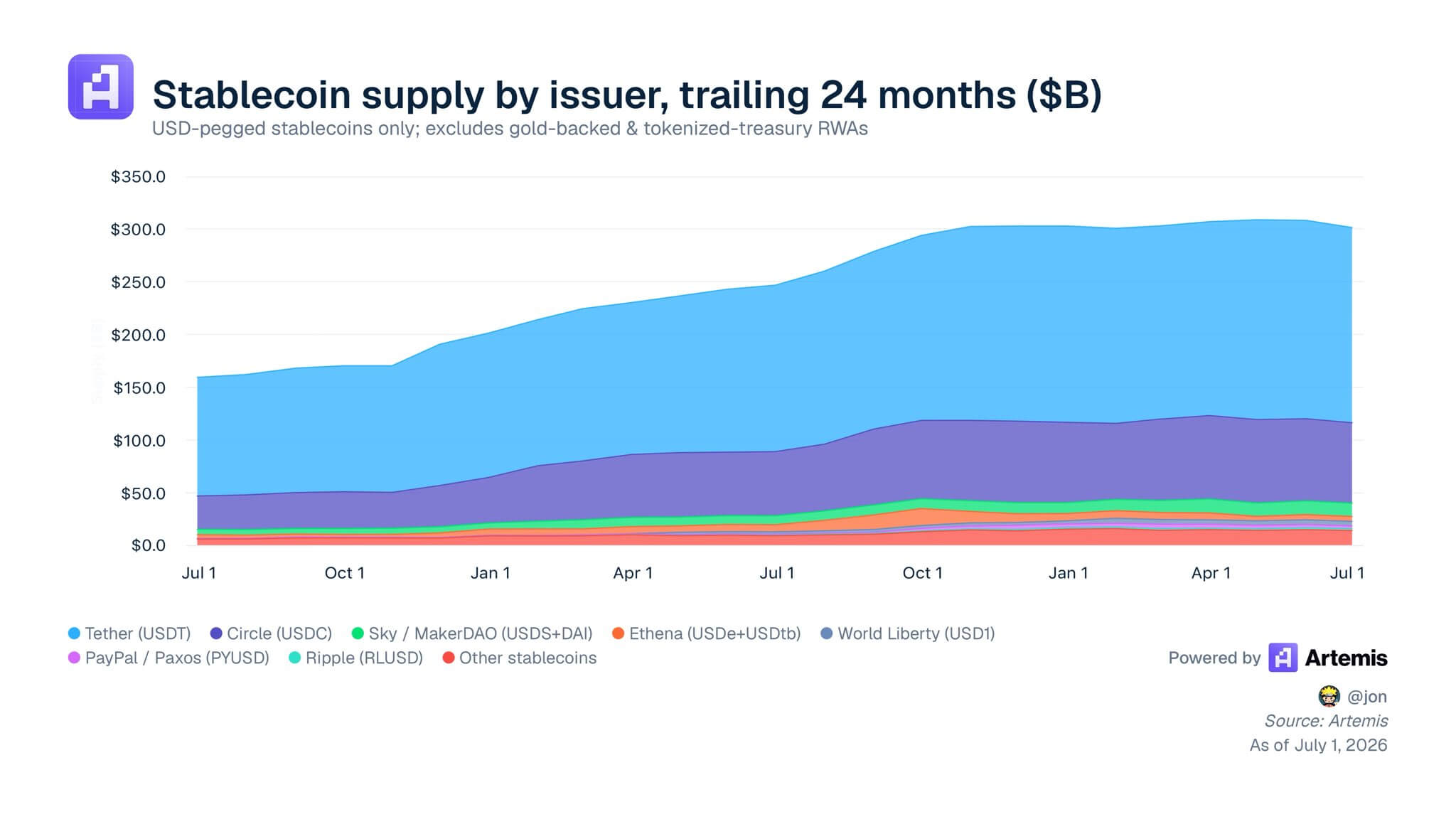

Citing Artemis data, Allaire noted that in Q1 2026, the total on-chain transaction volume of USDC was close to $30 trillion, capturing 80% of all dollar stablecoin transaction volume on major public blockchains. He said: "Today, USDC is firmly among the top three digital assets globally by liquidity, with a significant liquidity gap to the assets following it. BTC, USDT, and USDC possess top-tier liquidity; the liquidity scale of other dollar stablecoins is only about one-tenth of theirs. Moreover, competitor liquidity is mostly concentrated in market-making orders on single exchanges, whereas USDC's liquidity is widely dispersed across dozens of application scenarios. Building this liquidity system has been our deep focus for nearly a decade."

Stablecoin supply from various issuers over the past two years (Data source: Artemis)

Allaire believes that the data above is the result of nearly a decade of deep ecosystem integration, something an enterprise alliance cannot replace overnight. USDC's comprehensive coverage of major global financial trading centers, various DeFi protocols, and global payment service providers has built an insurmountable operational moat.

Addressing OUSD's promoted zero-fee model, Allaire raised doubts: while the zero-fee narrative sounds appealing, implementing it in the real market often requires more mature and structured commercial solutions. He revealed that Circle has long been reducing transaction flow costs by signing customized exclusive contracts with enterprise payment partners, rather than simply eliminating all fees across the board.

Furthermore, Allaire questioned whether large corporate alliances could operate efficiently in the rapidly changing digital asset industry, commenting that past large alliances in the financial sector were generally "slow-moving, with predictable outcomes." He said: "Large alliances composed of many big corporations find it difficult to coordinate. Diverse interest demands are hard to unify, slowing overall progress, making it almost impossible to nurture innovative outcomes with long-term competitiveness."

He also revealed that in the early days of USDC's development, Circle tried a small-scale alliance structure, ultimately finding that a streamlined, autonomous strategic partnership model was far more efficient than a committee-led alliance network.

From an operational cost perspective, Allaire warned: if all reserve earnings are allocated to channels, the stablecoin operator would have no retained funds for infrastructure investments such as global compliance licensing, risk control implementation, and 24/7 treasury fund management.

Multiple Hurdles for OUSD's Large-Scale Adoption

Market analysts remain cautious as well: even with the backing of numerous well-known enterprises, the OUSD alliance will find it difficult to quickly translate that into real on-chain liquidity.

Lorenzo Valente, Head of Digital Assets Research at ARK Invest, pointed out that any new stablecoin faces severe cold-start challenges. Capital markets and crypto exchange trading systems have long been optimized around the mature trading pair depth of USDT and USDC. He wrote: "There is no successful precedent for an alliance composed of hundreds of competing enterprises. Circle and Tether can independently plan product iterations and execute business without compromise to any partners; whereas alliances spanning multiple competing corporations will have extremely slow decision-making and progress."

Valente also raised concerns regarding regulation and antitrust issues: Circle and Tether have spent years obtaining multiple compliance licenses worldwide and building regulatory communication channels, enough to handle regulatory pressures from various countries. However, OUSD simultaneously aggregates global leading card networks, asset management companies, and major banks, making it too conspicuous a target, easily becoming a key subject for antitrust regulatory scrutiny.

At the same time, whether the OUSD founding members can maintain a long-term united front remains unknown. Stripe recently acquired the stablecoin infrastructure firm Bridge, continuously building its own financial service system; major banks are testing self-developed tokenized deposit products; Ripple is also launching its own stablecoin. These enterprises, holding vast distribution channels, are simultaneously deploying multiple digital asset product lines. They will not exclusively divert traffic to OUSD, and this traffic dispersion will significantly weaken OUSD's network expansion speed.

Kayla Phillips from blockchain venture capital firm Hivemind commented on this: "How will so many institutions coordinate governance? For efficient operation, it's impossible to give 140 enterprises equal decision-making power; if some companies cannot enter the core governance layer, how can they be continuously incentivized to stay in the alliance and participate in operations?"

The On-Chain Settlement Sector Moving Towards Fragmentation

The birth of OUSD reflects a larger trend in the stablecoin industry: the sector is gradually splitting, and the underlying stablecoin settlement layer may become more diverse. Large enterprises no longer view stablecoins solely as independent products for ordinary consumers but increasingly as standardized, reusable backend settlement tools.

For Circle, to maintain market share, it must accelerate the promotion of value-added development tools like the Cross-Chain Transfer Protocol (CCTP) and institutional embedded wallets, ensuring its software ecosystem provides added value beyond interest sharing.

Ultimately, the core competition in the stablecoin sector has shifted from a battle of underlying technologies to a direct contest over network profit distribution rights. Currently, channel platforms are banding together, seeking to reclaim the interest income generated by their own user traffic. The issuer-dominated stablecoin model is facing the strongest challenge from the channel side in its history.