Written by: Rita

Tidal Guide Introduction

Goldman Sachs released the management meeting notes for Circle Internet Group (CRCL.US) on July 5th. Circle is the issuer of USDC. The core message of this meeting is: Stablecoins are transitioning from being peripheral tools in the crypto world to becoming infrastructure for traditional finance and the AI economy. USDC's use cases are rapidly expanding, extending from crypto trading to cross-border payments, consumer e-commerce, capital market settlements, and even AI agent payments. Goldman Sachs rates Circle as Neutral with a target price of $96. The current stock price is $64.62, implying an upside potential of approximately 48.6%.

Stablecoin Growth Has Decoupled from the Crypto Market Cycle

Circle management repeatedly emphasized a key judgment during the meeting: stablecoin growth has decoupled from the fluctuations of the crypto market. Over the past few quarters, while crypto market trading volume and prices have trended downwards, the market capitalization and transaction volume of stablecoins have continued to rise.

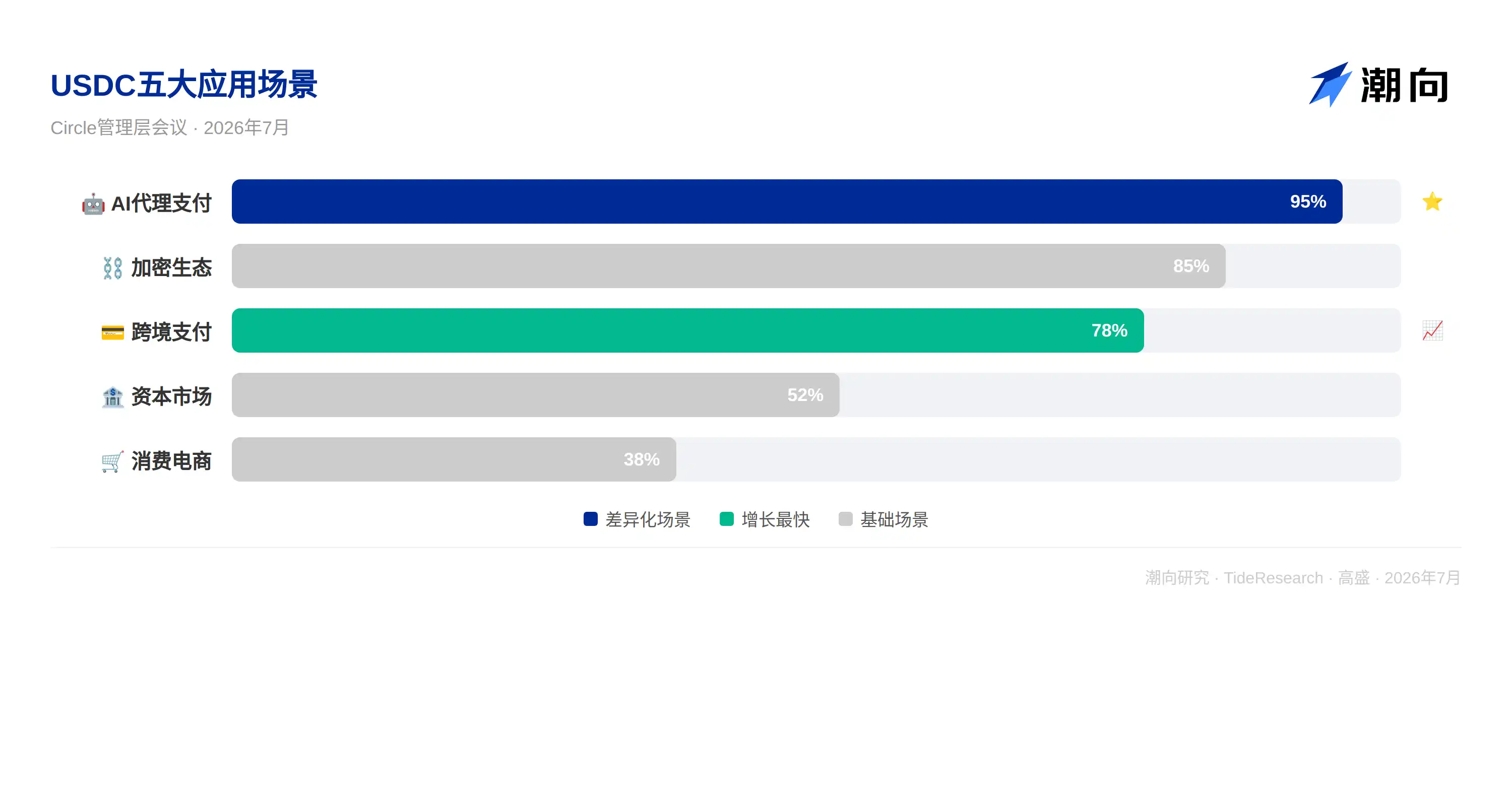

The reason lies in the diversification of use cases. Circle categorizes USDC's application scenarios into five tiers, covering the full spectrum from the crypto ecosystem to AI agent payments.

The crypto ecosystem is USDC's foundation, with continuous expansion of liquidity through partnerships with rapidly growing platforms like Hyperliquid.

Cross-border payments and treasury management are currently the fastest-growing segments. USDC's instant settlement and extremely low transaction costs are transforming traditional bilateral cross-border payment processes. Circle noted that demand for USD stablecoins is particularly strong in emerging markets, representing a trend of "digital dollarization," where people use USDC as a substitute for local currency or unreliable banking systems.

Consumer and e-commerce use cases are also taking shape. Major e-commerce platforms like Stripe and Shopify have begun supporting USDC payments, allowing users to directly choose USDC at checkout. Stablecoin-linked credit cards are also emerging, enabling users to hold and spend stablecoins.

Breakthroughs in capital markets are even more critical. Circle sees the potential for USDC as collateral for derivatives and a settlement currency. The recent CFTC approval allowing Futures Commission Merchants to treat specific stablecoins as readily marketable collateral is a significant institutional catalyst. The tokenization of real-world assets is also expanding USDC's application scenarios, as stablecoins are the natural cash settlement tool for on-chain transactions.

The most emphasized differentiated scenario by Circle is AI agent payments. AI agents are autonomously executing economic activities. x402 is currently a leading agent payment protocol, with USDC accounting for approximately 99% of all transactions on that protocol. AI agents require atomic settlement and extremely low transaction costs, making stablecoins the most suitable payment tool.

USDC's Competitive Moat is Network Effects

Management believes that stablecoins are a classic network effects business. The USDC network is a public, internet-native financial infrastructure that anyone can access—individuals, businesses, and developers alike.

Circle outlined three major competitive advantages for USDC.

First, the breadth of distribution and platform ecosystems. USDC strengthens liquidity by continuously adding partners, creating a "liquidity supernova" effect. New stablecoin entrants find it difficult to replicate this network effect due to the cold start problem: no liquidity without users, and no users without liquidity.

Second, global liquidity depth. USDC has deep liquidity across exchanges, over-the-counter markets, payment networks, and collateral markets. This depth itself is a moat.

Third, compliance infrastructure. USDC has regulatory arrangements across multiple jurisdictions. Management views this as a key driver for institutional adoption, not a constraint.

Regarding competition, Circle distinguishes between two types of opponents. One is tokenized deposits, which are digital deposit certificates issued by banks. Circle argues that stablecoins have advantages over tokenized deposits because they are open, interoperable, carry no bank credit risk, and are fully reserved. The other is new stablecoin competitors. Circle expects more new stablecoins to emerge, but they lack the network effects Circle has accumulated over more than a decade.

The Difference Between Tokenized Deposits and Stablecoins is Structural

Circle believes the difference between stablecoins and tokenized deposits is structural, not merely a matter of who arrived first.

Stablecoins constitute an open, public, internet-native financial system accessible to anyone, with liquidity flowing freely across platforms. Tokenized deposits are more like an extension of the banking system, likely confined within a single bank or consortium ecosystem. These are two completely different architectures: stablecoins are internet-native, while tokenized deposits represent a digital upgrade of the banking system.

Another key difference is credit risk. Stablecoins are fully reserved, digital cash with no credit risk. Tokenized deposits are essentially liabilities of a bank, carrying bank credit risk. In Circle's view, this difference is fundamental.

Circle's Three Strategic Products Aim to Turn Stablecoins into an Operating System

Circle is not just a stablecoin issuer; it is positioning itself as an internet-native financial platform. Management emphasized three strategic products during the meeting.

Arc is Circle's in-house developed Layer 1 public blockchain, positioned as a comprehensive financial operating system aimed at enhancing liquidity and interoperability, particularly for attracting traditional financial institutions.

Circle Payments Network (CPN) is the cross-border payment product, enabling faster and more efficient cross-border payments through blockchain settlement. Institutional adoption is growing.

Agentic Stack is the product line for AI agents, with the goal of maintaining USDC's dominant share in AI-related economic activities. Given that USDC already accounts for roughly 99% of transaction volume on the x402 protocol, the first-mover advantage in this space is evident.

Regulation is a Catalyst, Not a Constraint

The market has long been concerned that stablecoin regulation might constrain Circle's business model, but Circle management offered a completely opposite interpretation. They believe that if market structure legislation like the CLARITY Act passes, it will serve as a catalyst for USDC growth, not a business constraint. The reasons are threefold: The bill allows issuers to continue incentivizing distribution through revenue sharing, enabling Circle to keep expanding its partner network; The bill could unlock institution-grade crypto adoption, leading to greater stablecoin usage; The bill encourages usage-based reward mechanisms over passive holding, which would promote active use of USDC and reduce idle accumulation.

Tidal Guide Perspective

Goldman Sachs rates Circle as Neutral, but the notes themselves reveal a lot. Circle is successfully expanding USDC from a crypto trading tool into internet-native financial infrastructure, which is the right direction.

It's worth questioning how deep Circle's moat really is. Network effects do exist, but USDC's biggest competitor, USDT, still leads in stablecoin market capitalization. The compliance advantage Circle relies on is seen as a weakness by crypto purists: transparency means being subject to regulation, and regulation means the potential for freezing assets. Circle's institutional positioning is a double-edged sword.

Another point worth noting is Goldman Sachs' valuation framework. The $96 target price corresponds to a 35x P/E ratio, but Circle's current profitability heavily depends on interest income from reserve assets. If interest rates decline, Circle's profits would be directly pressured. This risk is only briefly mentioned in the notes, but its actual impact on valuation could be greater than that of regulation.

Disclaimer

This article is Tidal Guide Research's compilation and interpretation of a third-party securities firm research report. The ratings, target prices, profit forecasts, and related judgments cited herein are the views of that firm's analysts, representing only the stance of their affiliated institution. They do not represent the views of Tidal Guide Research and do not constitute any investment advice.

The market carries risks, and decisions should be made independently. This article should not serve as the basis for buying or selling any securities.