Author: Jae, PANews

A research report from a traditional bank has ignited the somewhat quiet DeFi sector.

On June 15, Geoff Kendrick, Global Head of Digital Assets Research at Standard Chartered Bank, released a first-time coverage report on the DEX (decentralized exchange) Uniswap, making a radical prediction that turned heads in the crypto market: the price of Uniswap's governance token UNI is expected to surge approximately 40-fold before the end of 2030, reaching the $100 milestone.

At the time, UNI was trading at only around $2.6.

Once derided as a "governance token with no substance," UNI is being repriced by Wall Street as a productive asset with network effects. Although the distant narrative of a 40x gain is tempting enough, the journey to that endpoint may not be entirely smooth.

Wall Street's 40x Growth Script for UNI: Four Numbers, One Main Theme

In Standard Chartered's deconstruction logic, Uniswap is being embedded within a valuation framework for the deep integration of traditional finance and the on-chain world.

Exponential Expansion of RWA Tokenization ($340B → $4T)

The starting point for growth is the wave of RWA (Real World Asset) tokenization. Standard Chartered predicts that the global scale of on-chain tokenized assets will experience exponential growth, soaring from the current approximately $340 billion to $4 trillion by the end of 2028. Asset management giants like Fidelity and BlackRock are batch-uploading traditional assets like stocks, government bonds, and money market funds onto blockchains, meaning the liquidity of on-chain tokenized assets will expand at a pace far exceeding industry expectations.

This is equivalent to building a much larger reservoir for the DeFi track: the asset scale must be established first, and only then can subsequent financial activities like trading, lending, and staking have sufficient underlying assets to carry them.

DeFi Penetration Rate Leap (3.5% → 30%) Drives TVL Higher (37x)

Getting assets on-chain is only the first step; stagnant water needs to become flowing water. Simply put, only when assets flow into DeFi protocols can they be converted into protocol revenue and value. Standard Chartered expects that currently only about 3.5% of tokenized assets are deployed in the DeFi ecosystem. This proportion is projected to increase to 30% by 2030.

Driven by the dual engines of native crypto asset growth and RWA migration to chains, the overall DeFi TVL (Total Value Locked) is projected to skyrocket 37-fold from current levels by 2030, reaching approximately $2.7 trillion.

Fee Switch Provides Price Support (40x)

Uniswap, as the primary hub for on-chain liquidity, will become the biggest beneficiary of this tidal wave of capital. Its token, UNI, is also expected to rise from $2.6 to $100, capturing a near 40-fold increase.

The long-term price path for UNI provided by Standard Chartered is: $6.5 by end of 2026 → $20 by end of 2027 → $40 by end of 2028 → $65 by end of 2029 → $100 by end of 2030.

In the past, UNI was once mocked by the market as an "air token" because it only conferred governance rights and had no cash flow capture capability. At the end of last year, Uniswap activated the fee switch, officially ushering UNI into a deflationary era.

The report points out that on December 28th of last year, Uniswap destroyed 100 million UNI in a single move, and additionally burned 5 million UNI, reducing the total supply from 1 billion to 895 million. The circulating supply has also dropped to 622 million. This contraction in supply will provide support for the UNI price.

Furthermore, Uniswap has also generated approximately $21 million in protocol fees. The linear relationship between fees and trading volume means that as tokenized assets flood into the protocol, the fee switch will automatically trigger more burn. This signifies that UNI is transitioning from a "pure governance tool" to a "productive asset with deflationary properties," directly narrowing the valuation multiple gap between Uniswap and listed exchanges like Coinbase.

It is worth mentioning that Geoffrey Kendrick also proposed a vivid business analogy in the report: likening Uniswap to YouTube, and Coinbase to Netflix.

-

Coinbase (Netflix model): Centralized operation, heavy asset investment, requiring high capital support. Listing assets and compliance involve multi-layered screening, with high marginal costs for expansion, making it easier to limit the variety of asset classes covered.

-

Uniswap (YouTube model): An open liquidity pool architecture where any user can be a "content creator" (liquidity provider). The platform does not incur high costs for listing assets. In scenarios like stablecoin trading, liquid staking derivatives, and niche tokens, the network effects and long-tail advantages of this open model are hard for centralized exchanges (CEXs) to match.

This two-sided effect, which grows more prosperous with use, is precisely the moat that allows Uniswap to maintain its leading position in the long run.

More importantly, Standard Chartered believes Uniswap is far from a simple "retail DEX application." Its essence is a set of integrable market infrastructure. Once RWA scales up, traditional financial institutions can directly "plug" assets into Uniswap's liquidity pools for trading. This is a functionality that traditional financial markets themselves cannot achieve.

Uniswap Becomes Preferred On-ramp for Traditional Funds, Yet Faces Pincer Attack from Emerging DEXs and Aggregators

Wall Street's distant lens is captivating enough, but returning to the reality of the crypto market, Uniswap's actual situation is not as straightforwardly linear as portrayed in the research report.

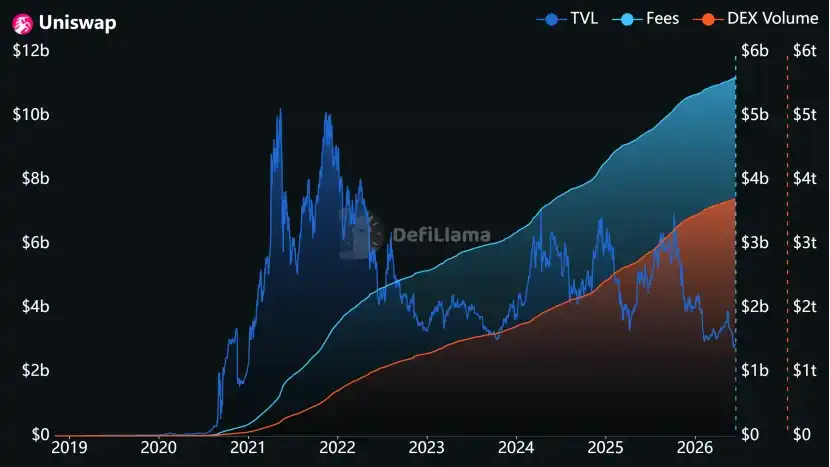

Since its founding in 2018, Uniswap's cumulative trading volume has exceeded $3.7 trillion, with cumulative fees as high as $5.6 billion. Its TVL is approximately $2.88 billion.

In terms of market share, Uniswap's DEX throne remains solid. Whether on the Ethereum mainnet or across major L2 ecosystems, Uniswap's trading volume and liquidity depth hold a dominant position, with no competitor posing a substantive threat.

More significant signals come from the institutional side. In February this year, BlackRock's tokenized money market fund BUIDL announced it would be available for trading on UniswapX and strategically purchased UNI tokens. With the adoption of UniswapX, which introduces features like off-chain routing, gasless transactions, and MEV (Miner Extractable Value) resistance, the experience gap between DEXs and CEXs is significantly narrowed, making it the preferred on-ramp for traditional capital.

Similarly, last Friday (June 12th), Fidelity also deployed liquidity for its stablecoin, FIDD, on Uniswap. The protocol's concentrated liquidity model is currently the most efficient pricing mechanism on-chain. Once compliant RWA assets are tokenized on a large scale, Uniswap is poised to become the "New York Stock Exchange" on-chain, holding the power of asset pricing.

Wall Street's water is flowing on-chain. And Uniswap is that faucet. Wall Street institutions are treating Uniswap as the on-chain interface for compliant assets, and UNI is also moving towards a pricing logic akin to "on-chain routing infrastructure."

Although the vision of a $100 endpoint is quite enticing, two major obstacles still lie in Uniswap's path to the summit, which could significantly delay or even nullify this distant promise.

-

Traffic Hijacking by Emerging DEXs and Aggregators (Competitive Risk): Solana-based DEXs like Jupiter and Raydium, riding on Meme mania and extremely low transaction costs, have captured a massive amount of retail traffic. Meanwhile, aggregators like 1inch and CowSwap intercept users at the front-end, reducing Uniswap to a mere "backend liquidity pool" in certain ecosystems, continuously eroding its brand premium and user mindshare.

-

Delays in Tokenization Adoption (Macro Risk): Standard Chartered's valuation heavily relies on the assumption that "DeFi TVL will reach $2.7 trillion by 2030." If global legislative progress on tokenization falls short of expectations, or if large-scale security incidents or systemic risks occur, the penetration rate of RWA could slow down significantly, potentially severely postponing the realization cycle of this grand narrative.

Returning to the most intuitive price perspective, UNI is currently trading below $3, down more than 92% from its all-time high in May 2021.

The fee switch brought deflation but not a price reversal. Market apathy towards the DeFi narrative, depleted liquidity, and high macro interest rates have all put significant pressure on UNI's valuation.

However, this might be precisely the source of the "40x potential" in Standard Chartered's eyes: starting from a low base.

Standard Chartered's first-time coverage of UNI with a $100 target price carries more symbolic significance than the price itself. In reality, the accuracy of the prediction is not the most important thing; what matters is that Wall Street's perception of DeFi is evolving: shifting from the early days of "unbridled growth and speculative bubbles" towards a rational business judgment based on "capital efficiency, network effects, and cash flow value."

It should be noted that Wall Street research reports are often strong on macro logic but short on micro risks. For investors immersed in this space, the 40x endpoint is undoubtedly attractive, but the road to 2030 is also destined to be strewn with thorns.

Whether UNI can truly capture the $4 trillion tokenization红利 depends on how skillfully it performs the high-difficulty dance between the principles of decentralization and global regulatory compliance in the real world.

More challenging than a 40x gain might be the four-year wait, which tests faith even more.