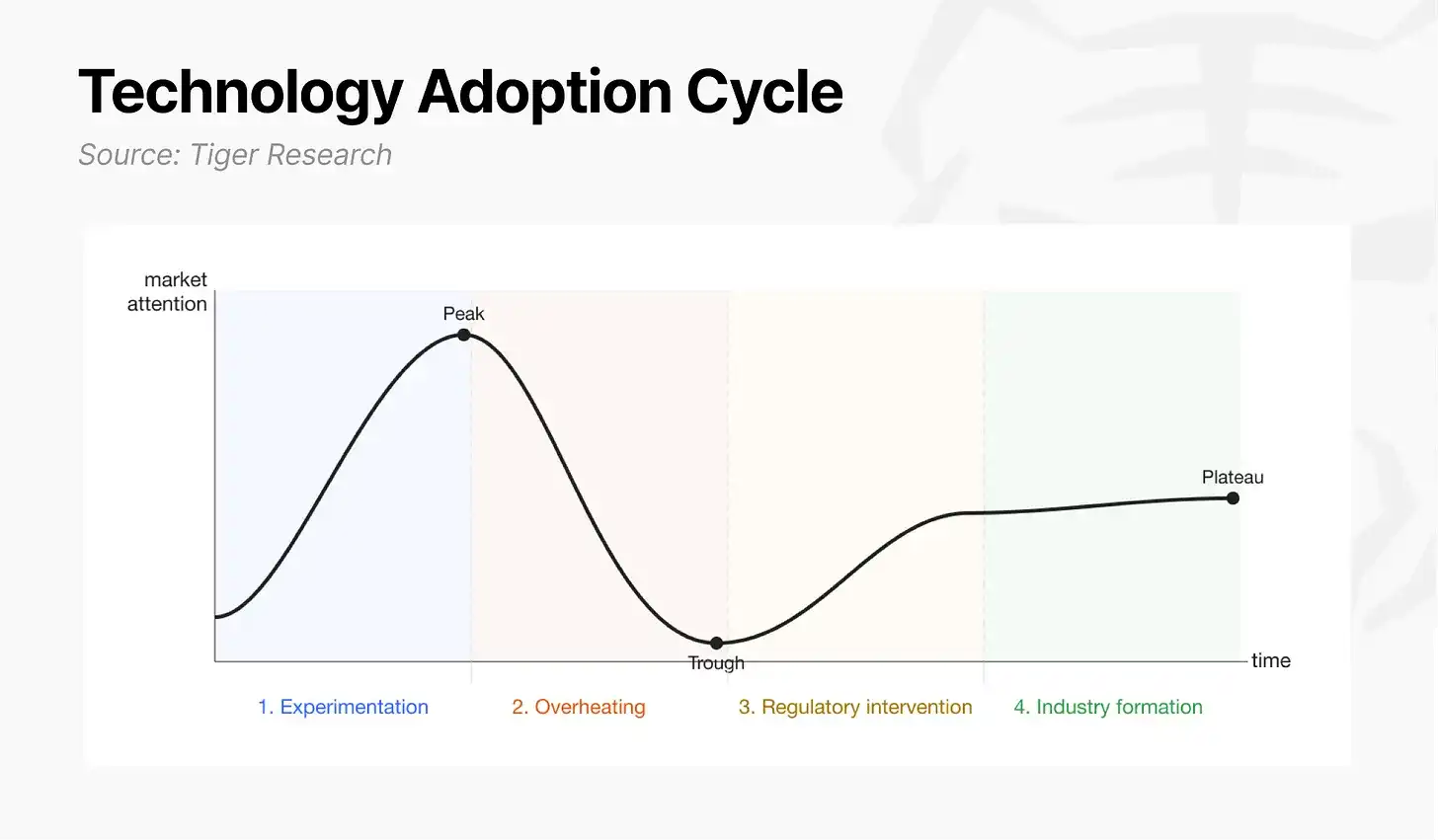

This article is from Tiger Research. New technologies typically go through four stages on the path from experiment to industry: experimentation, hype, regulatory intervention, and industry formation. The internet completed its experimentation in the 1990s, experienced the hype of the dot-com bubble, and eventually developed into a mature industry after the bubble burst and regulations and standards were established. Fintech and artificial intelligence follow the same path, albeit with different rhythms and forms.

The crypto industry is currently in the transitional zone between the third and fourth stages. After Bitcoin's birth, a small group of developers validated its potential in payments and settlement (experimentation). During the 2017 ICO boom and the 2021 DeFi wave, investors repeatedly rushed in and out (hype). The 2022 collapse of FTX was both a peak and a turning point. After multiple shakeouts, speculative demand has been filtered out, real use cases have been validated, and US regulators have begun moving towards formalization rather than laissez-faire or suppression (regulatory intervention).

Because the crypto industry attempts to directly replace core financial functions such as settlement, payment, and issuance, it has created greater friction with traditional financial institutions, leading to a longer absorption period. Today, the crypto industry has finally reached the intersection of regulatory intervention and industry formation.

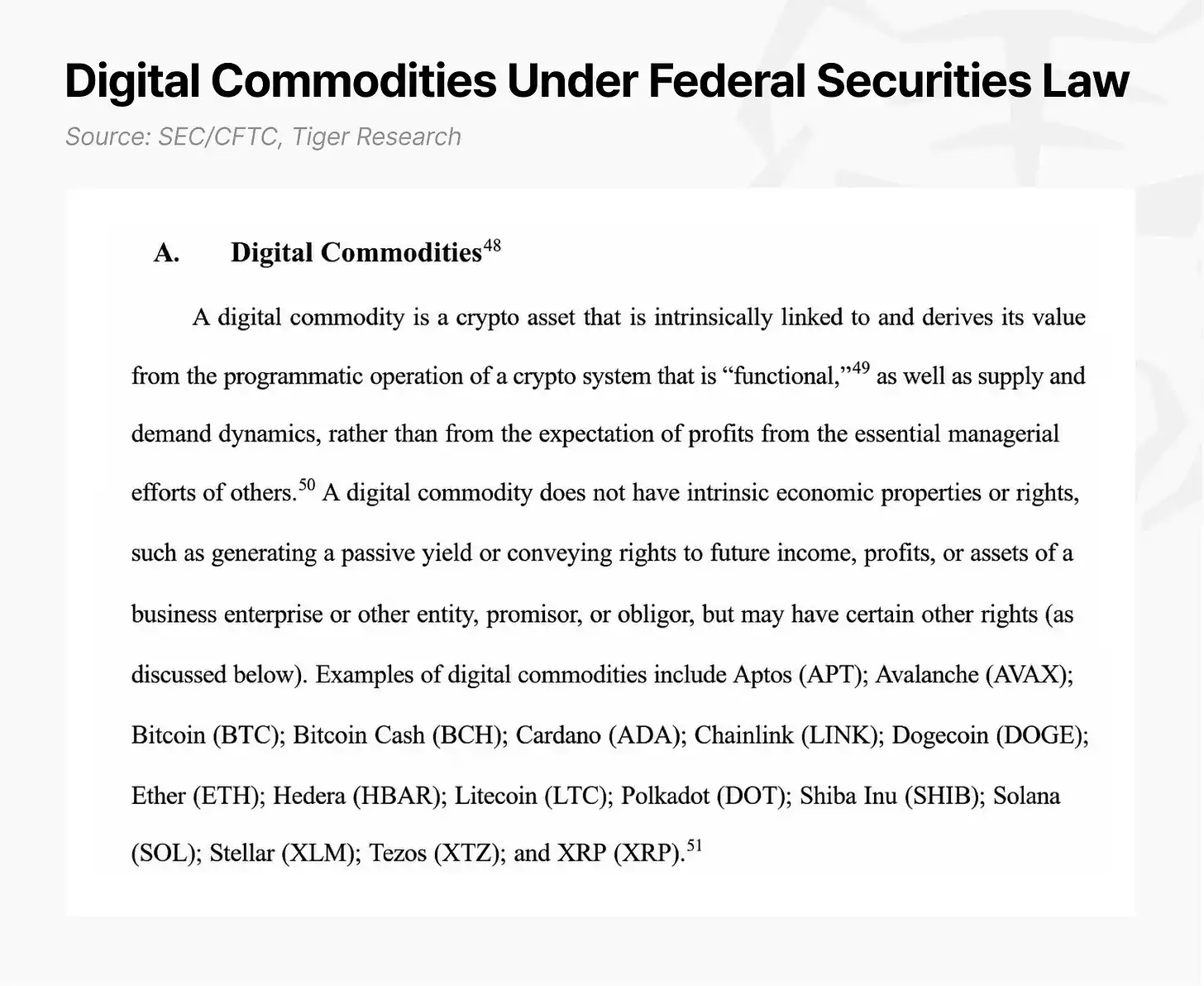

Progress on the regulatory front is significant. The US Congress passed the *GENIUS Act*, clarifying the legal status of stablecoins. In March 2026, the SEC and CFTC issued a joint interpretive guidance, confirming 16 assets including Solana (SOL) as digital commodities. It categorized assets into five classes, moving away from the old "security/non-security" binary classification, and formally excluded protocol staking from securities law oversight.

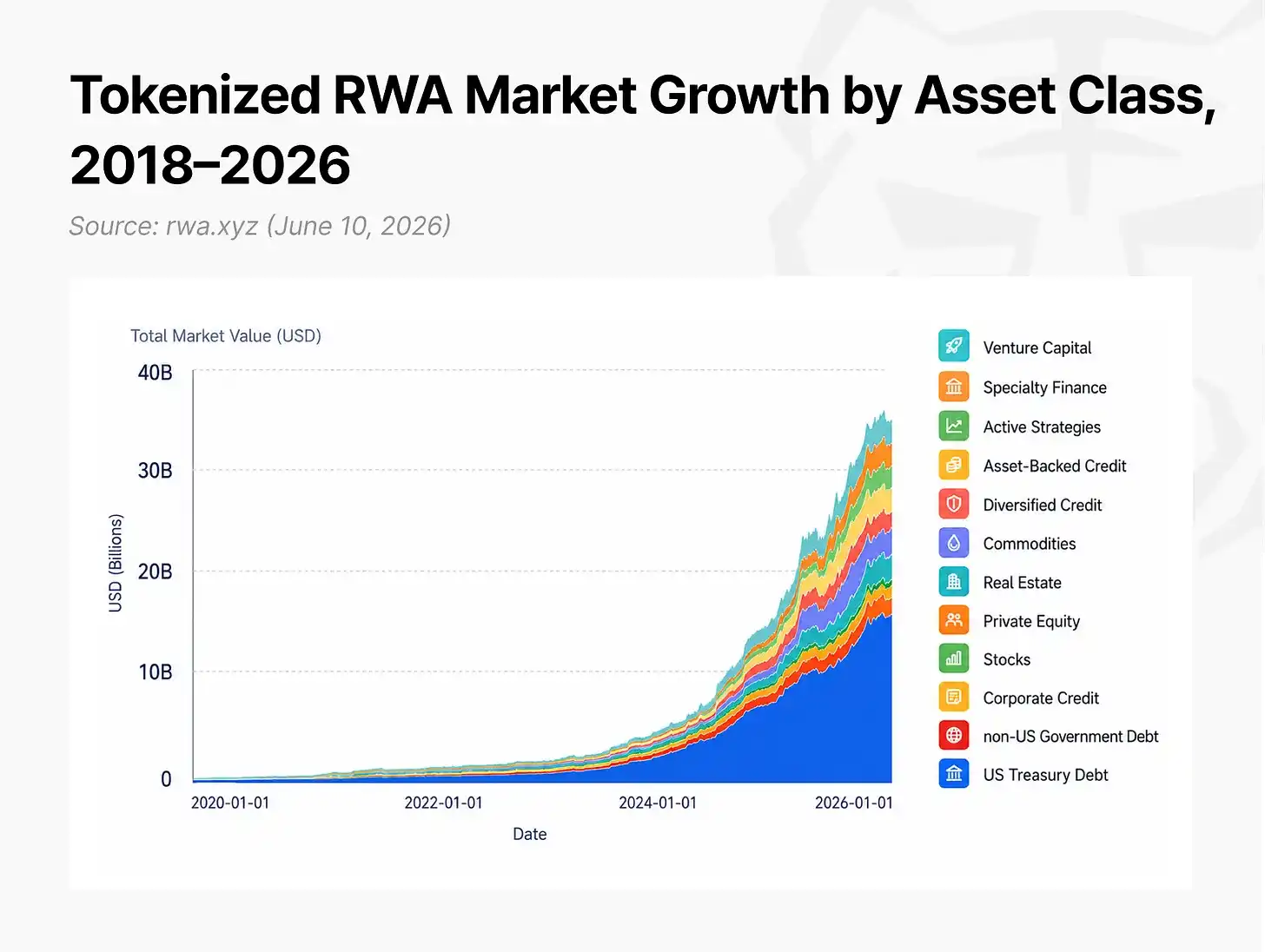

Institutional adoption continues to accelerate. The tokenized real-world asset (RWA) market grew approximately 257% in 15 months, from $5.4 billion in early 2025 to $19.3 billion by the end of March 2026. Including stablecoins, the total scale of on-chain assets is approaching $300 billion.

This is not yet enough to be called a mature industry, but industry formation has commenced in parallel with regulatory construction.

2. Internet Capital Markets: The Endgame Form of the Crypto Industry

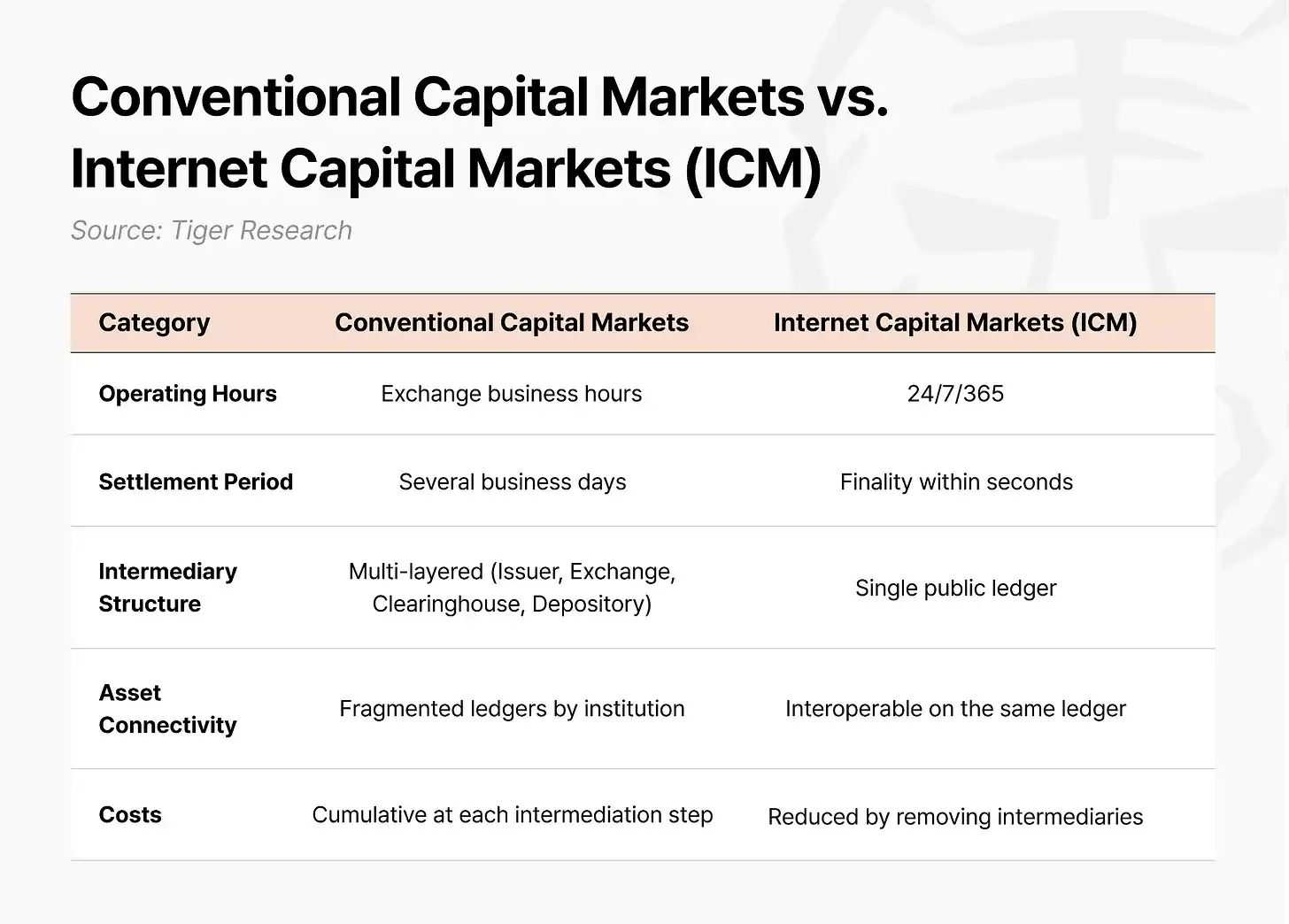

The future the crypto industry points to upon entering its industrial phase is the restructuring of capital markets themselves. This future can be defined as "Internet Capital Markets" (ICM): a capital market where the issuance, trading, and settlement of assets are all completed on a single public blockchain.

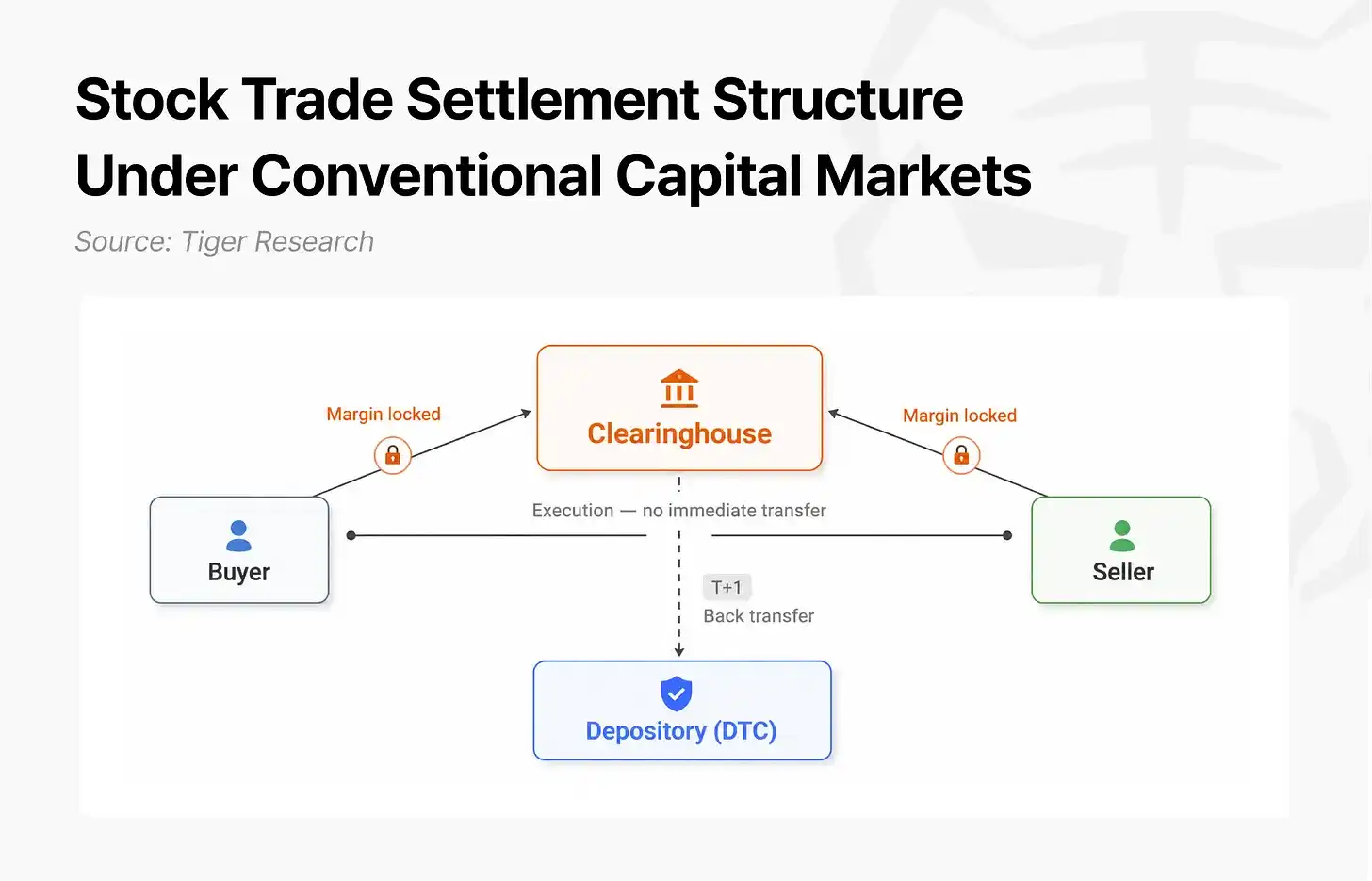

Today's capital markets operate on an architecture designed before the internet. When buying a stock, the asset and funds do not complete settlement at the moment of execution. A clearinghouse sits between buyer and seller to assume performance risk, requiring both parties to post margin, funds which are locked until settlement is complete. In the US market, the transfer of ownership at the depository doesn't happen until the business day after execution. Because brokers, exchanges, clearinghouses, and depositories each maintain separate ledgers, they must reconcile with each other daily, and any discrepancies delay settlement. Cross-border transactions further add currency exchange and national depositories, stretching settlement times to T+3 or longer. This architecture, designed for an era where counterparties distrusted each other, has itself become the cost.

In Internet Capital Markets, code takes over the role of the clearinghouse. The buyer's payment and the seller's asset are placed simultaneously into a smart contract, and the two transfers are executed as a single transaction. If either party's conditions are not met, the entire transaction is automatically canceled, eliminating scenarios where only one party's funds are transferred. Because performance risk is eliminated at the code level, there is no longer a need for a clearinghouse to require margin; because all participants share the same ledger in real-time, inter-institutional reconciliation is unnecessary. Execution and settlement are synchronized within seconds.

The driving force behind this transformation is expanding from crypto startups to traditional financial institutions. Those institutions that profit from multi-layered intermediary structures are now themselves participating in this shift. History repeatedly shows that at the inflection point of each infrastructure overhaul, institutions that follow late either pay a higher cost or lose leadership. The transition to electronic trading in the 1990s is a classic case: large institutions reliant on floor trading initially resisted electronic platforms like Island ECN and Instinet, only passively following through acquisitions and adoption after these platforms became the standard. The fintech transformation followed a similar pattern.

This transformation is advancing fastest in the US. Since the dollar became the reserve currency under the Bretton Woods system in 1944, global trade and financial transactions have been denominated and settled in dollars. CHIPS processes over $2.2 trillion in payments each business day. SEC disclosure standards serve as a reference for capital market regulations in other countries. Over 99% of stablecoins are dollar-denominated. The US is replicating this same pattern in Internet Capital Markets.

3. Solana: The Concrete Realization of Internet Capital Markets

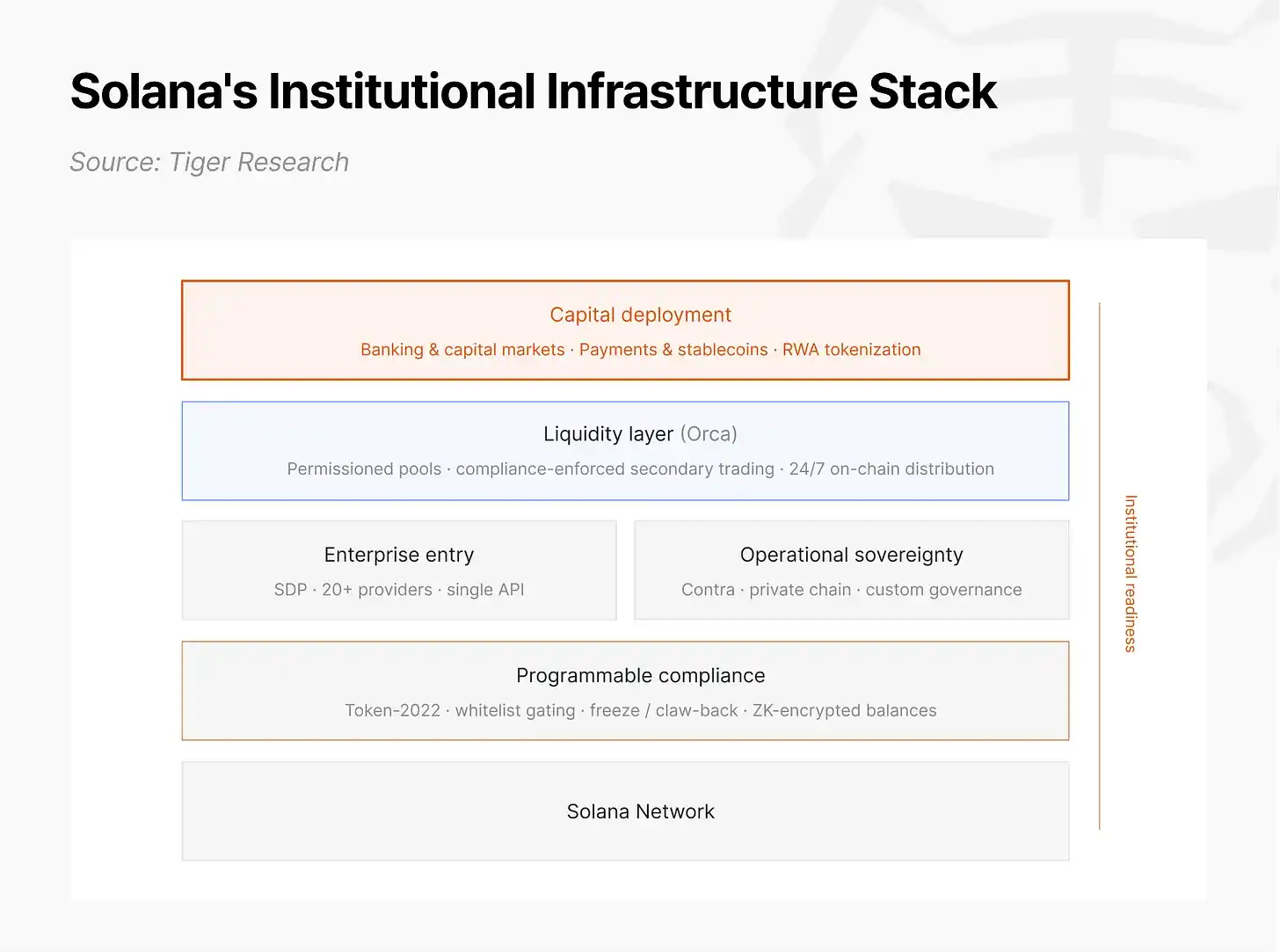

In the landscape of US Internet Capital Markets, Solana is a public blockchain network that integrates technological foundations, institutional practices, and regulatory design.

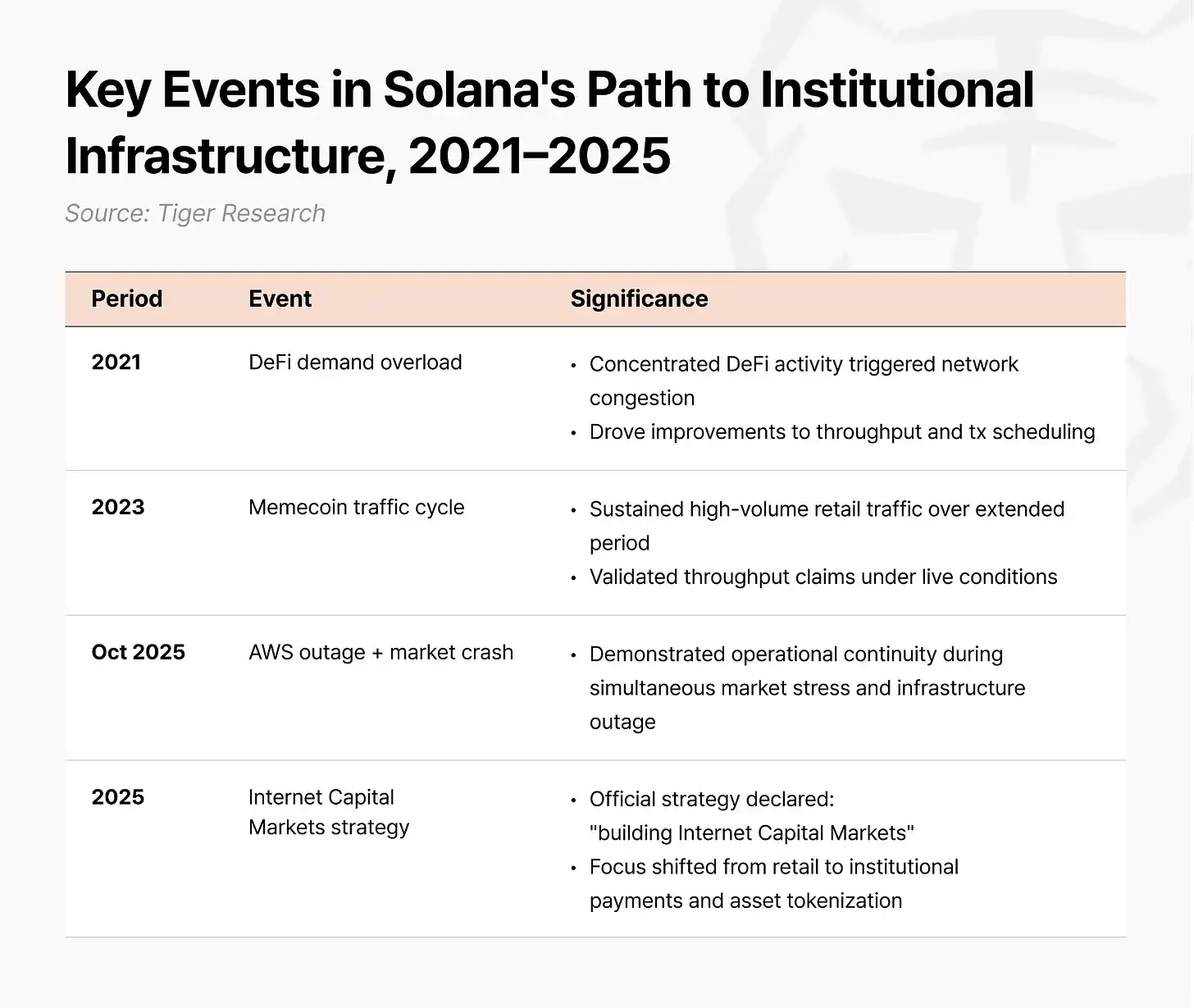

Solana's technical foundation was tempered in the retail market. Overload from DeFi demand in 2021 was seen as an opportunity to improve throughput and transaction scheduling. During the 2023 meme coin cycle, it validated its throughput claims by sustaining high-intensity retail traffic over an extended period. In October 2025, a market crash coincided with an AWS outage; transaction fees on other chains surged to $100 per transaction, while Solana continued operating at $0.0013 per transaction without interruption. The infrastructure stability required for institutional finance was first validated through stress testing in a retail environment.

In 2025, Solana established "building Internet Capital Markets" as its official strategy, shifting focus to institutional payments and asset tokenization. The Token-2022 standard introduced for this purpose embeds functions like freezing, confiscation, whitelist management, and confidential balances into the token's code itself. Issuers can implement compliance requirements within the token, addressing core financial needs for asset holding and transaction eligibility at the protocol layer without external systems.

On this infrastructure, seven large US financial institutions have initiated proof-of-concepts or completed real transactions on Solana: J.P. Morgan, State Street, Citi, Franklin Templeton, Visa, PayPal, and Western Union. Three of these are among the eight US Global Systemically Important Banks (G-SIBs).

Simultaneously, the Solana Policy Institute (SPI) was established in Washington D.C. in spring 2025, recruiting the former CEO of the DeFi Education Fund and the former CEO of the Blockchain Association. Instead of waiting for legislation to pass before reacting, it proactively submitted a pilot framework called "Project Open" to the SEC Crypto Working Group, attempting to set regulatory precedent while advancing business diversification and regulatory design.

4. Institutional Practice: Case Analysis Across Four Domains

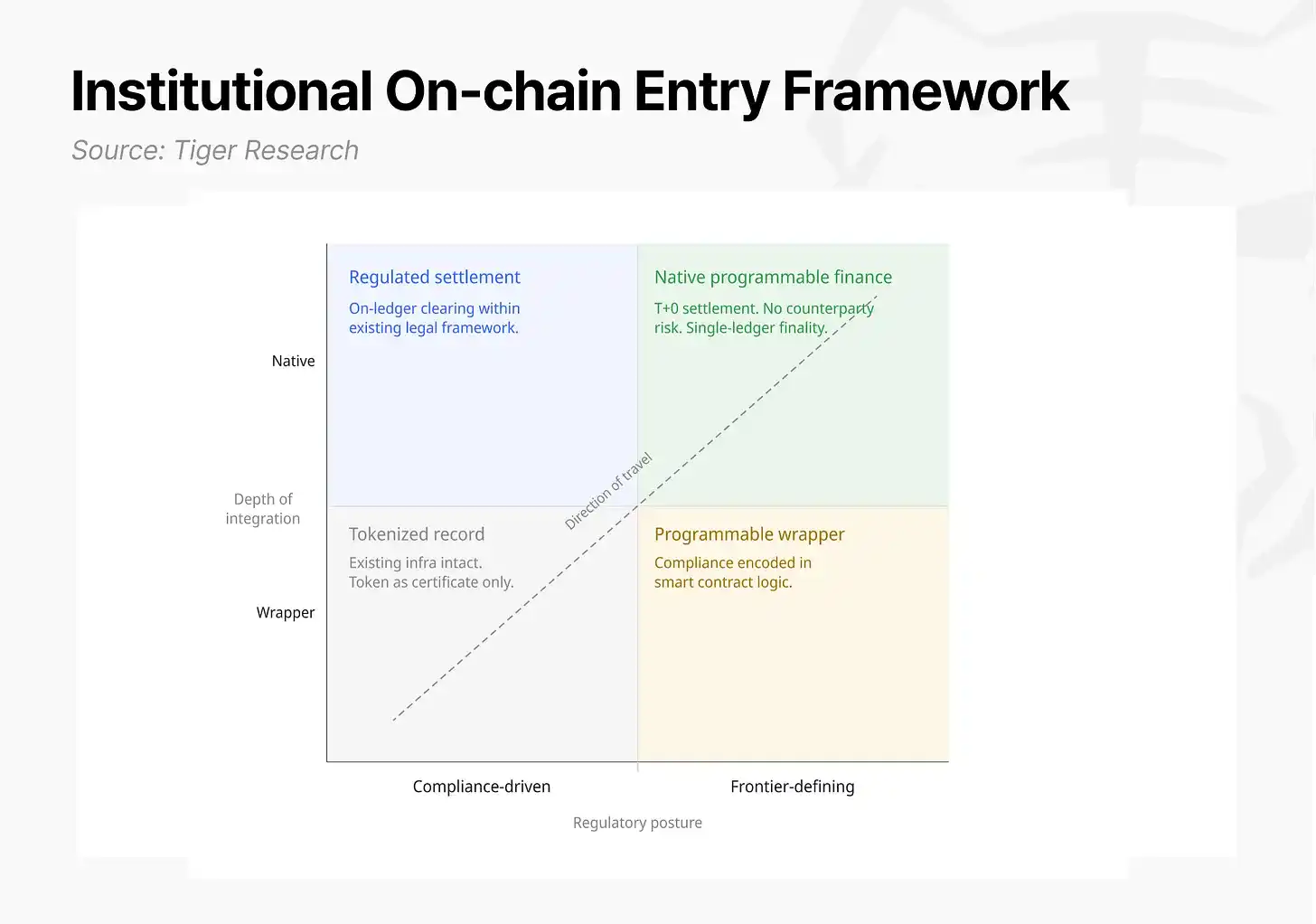

Institutional participation in Solana's Internet Capital Markets is unfolding across multiple fronts, but not all participants share the same goals. Understanding this layered activity requires an analytical framework built around two core axes: regulatory posture (compliance-driven vs. frontier-defining) and depth of value chain integration (wrapper layer vs. native layer).

4.1 Banks & Capital Markets: The Hidden Cost of Settlement Delays

The banking and capital markets domain encompasses bond issuance, trade finance, and treasury management. It is the core revenue source for traditional financial institutions and where the cost advantages of Internet Capital Markets are most directly evident. Three sub-domains share a key issue: a time gap exists between trade execution and the actual movement of funds.

According to Tiger Research estimates, in the US Treasury market alone, the opportunity cost of funds lying idle due to settlement delays is approximately $32 billion annually. Expanding to the entire US fixed-income market, the annual opportunity cost exceeds $45 billion. The speed limitations of the existing financial system are imposing huge hidden costs on market participants.

On Internet Capital Markets infrastructure, this chronic time gap disappears. Atomic settlement (DvP) bundles asset transfer and payment into a single transaction processed in real-time. Clearinghouses are no longer needed, and the reconciliation processes run separately by institutions vanish. Execution and clearing are completed within seconds (T+0).

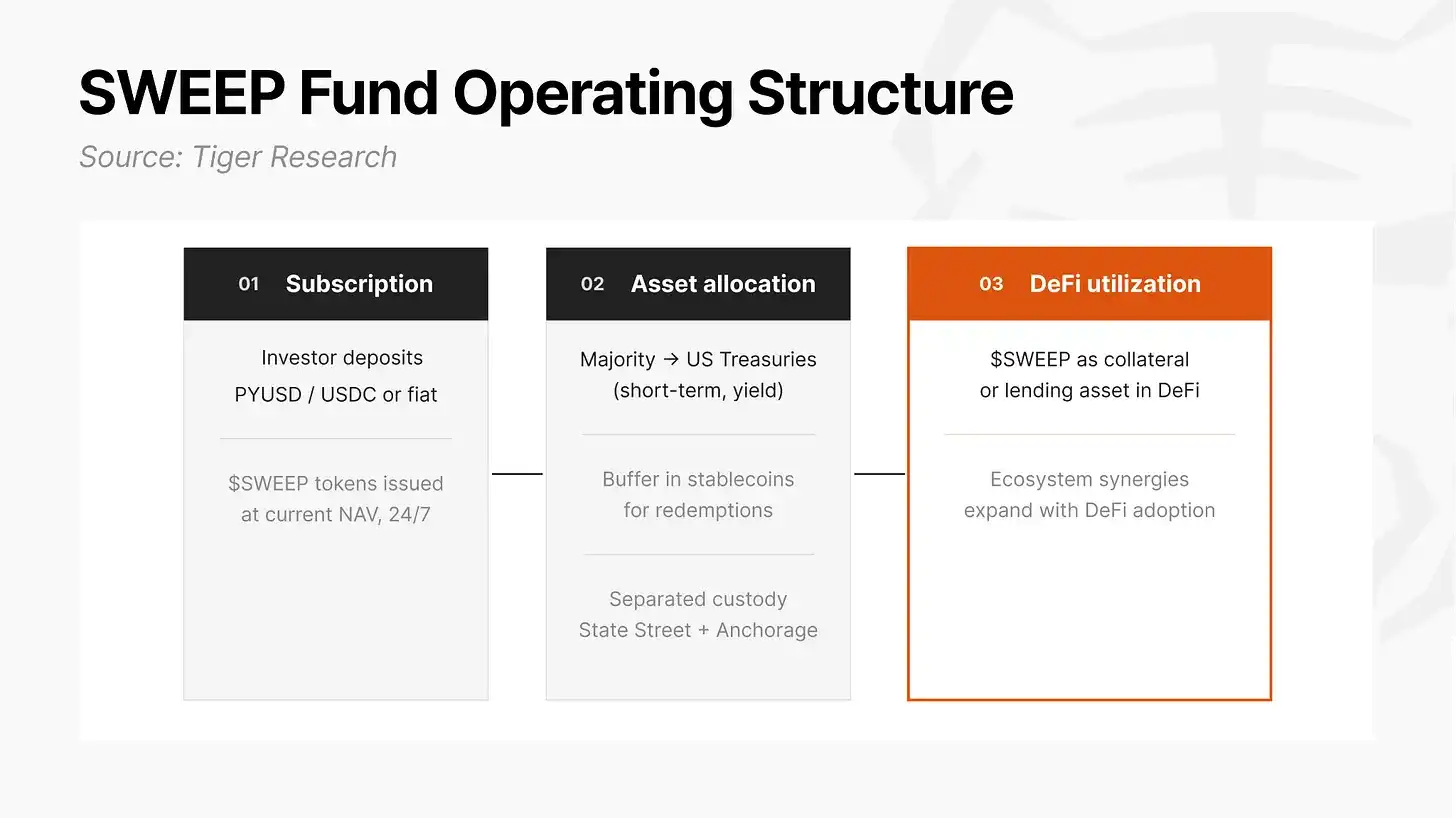

State Street × Galaxy: On-Chain Treasury Management (SWEEP). Launched on Solana in May 2026, SWEEP is an on-chain fund for institutional investors that accepts stablecoin (PYUSD, USDC) or fiat deposits to invest in short-term US Treasuries for yield. It implements the traditional finance concept of a "sweep account" as an on-chain fund. For Web3 foundations holding large amounts of stablecoins, using traditional financial services under existing infrastructure requires converting stablecoins to dollars first, incurring conversion fees and time delays. SWEEP allows institutions to deposit and redeem treasury yield assets directly from their wallets. Ondo Finance's flagship fund, OUSG, made an anchor investment of approximately $200 million at SWEEP's launch, representing about 26% of its TVL at the time.

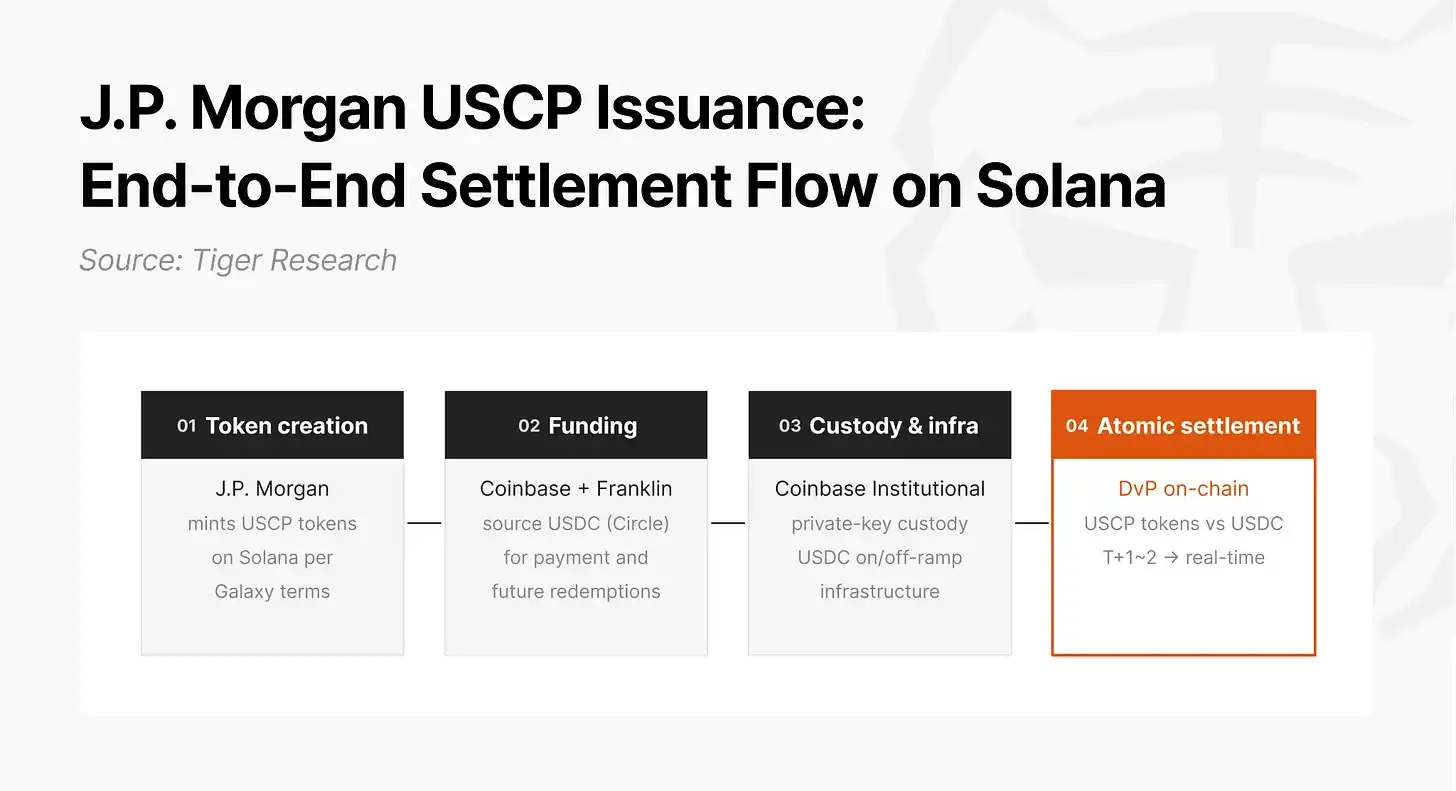

J.P. Morgan × Galaxy: Commercial Paper Issuance (USCP). In December 2025, J.P. Morgan arranged a $50 million US commercial paper issuance on the Solana public blockchain. This was not a simulation test but one of the earliest real debt security transactions on a public chain. J.P. Morgan, as arranger, directly created the USCP token on the Solana blockchain, with Coinbase and Franklin Templeton as principal investors and buyers paying in USDC (issued by Circle), and Coinbase providing private key custody and USDC on/off-ramp infrastructure. By combining stablecoin payment networks with on-chain atomic settlement (DvP), the corporate funding cycle, which traditionally takes T+1 to T+2 days and passes through multiple intermediaries, was compressed to real-time completion.

Citi × PwC: Trade Finance Tokenization (Bills of Exchange). Citi and PwC completed an internal proof-of-concept on Solana converting traditional bills of exchange into tokenized digital assets. In the simulated environment, the entire lifecycle of a bill (issuance, financing, circulation, settlement) was automated through smart contracts, reducing settlement time from days to minutes and manual reconciliation costs to zero. This case is strongly relevant for Asian financial markets, as global trade hubs are highly concentrated in the Asian region.

4.2 Payments & Stablecoins: Redesigning the Settlement Paradigm

Western Union: Global Remittances (USDPT). In May 2026, this 175-year-old company, handling about $150 billion in cross-border remittances annually across over 200 countries, issued the US Dollar Payment Token (USDPT) on Solana. In the traditional correspondent banking system, each intermediary bank processes only within its own systems and operating hours; settlement typically takes one to two business days, stopping completely on weekends and holidays. To be able to respond immediately to real-time payment requests from agent countries, Western Union must pre-lock large amounts of US dollars in local bank accounts in each country. These pre-funded correspondent account balances remain locked and non-yield-bearing until the transfer occurs.

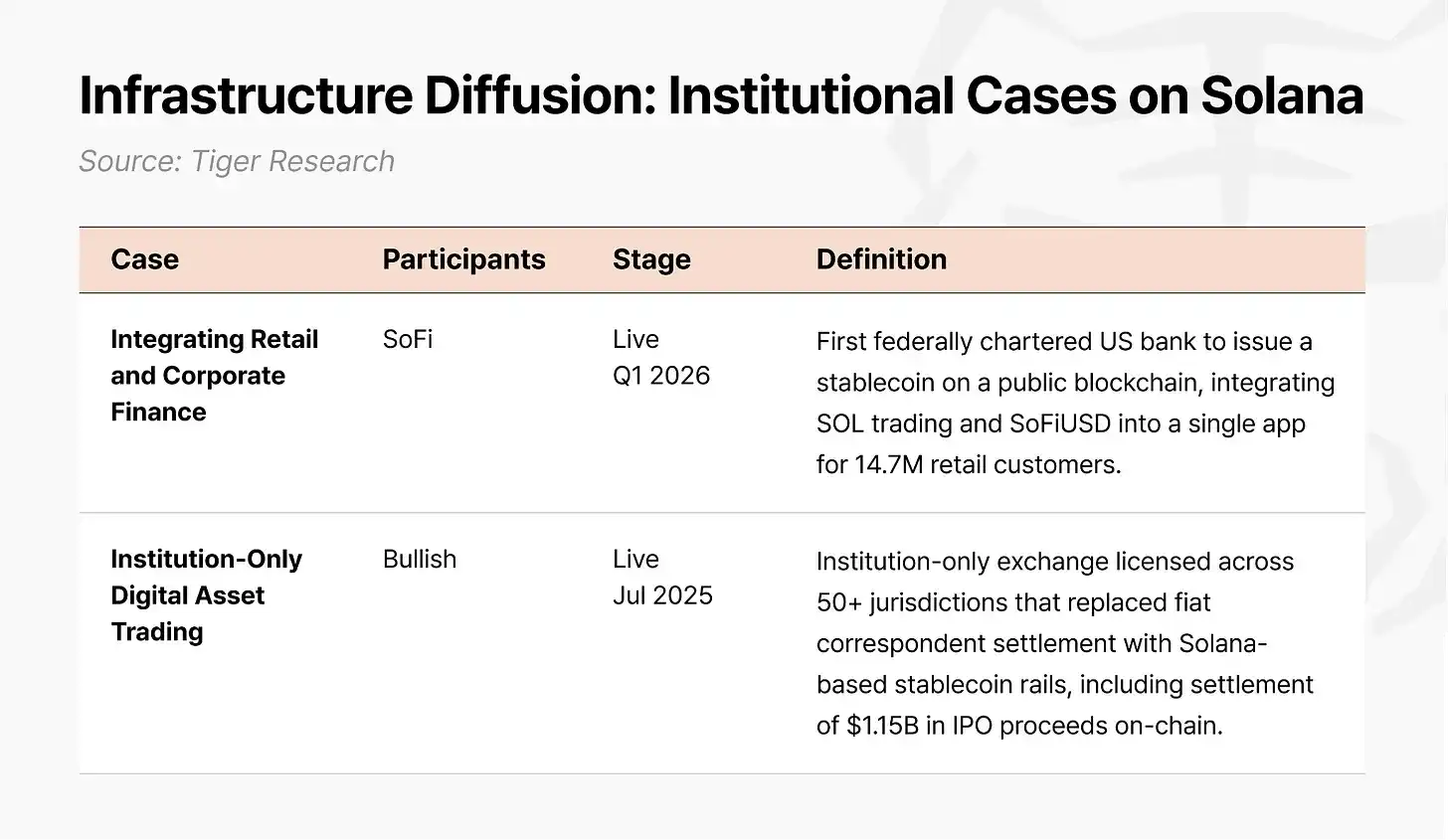

USDPT fundamentally redesigns this settlement flow, shifting the paradigm from "pre-funding" to "real-time, on-demand supply." When a country agent's cash inventory falls below a threshold, the US headquarters finance team immediately sends funds via USDPT (issued by Anchorage Digital) to that agent's institutional on-chain wallet. Whether it's a weekend, night, or holiday, final settlement is rapidly completed based on Solana's network block time of 0.4 seconds. Western Union is also building a Digital Asset Network (DAN), planning to roll out its consumer-facing stablecoin payment service, "Stable by Western Union," to over 40 countries within 2026.

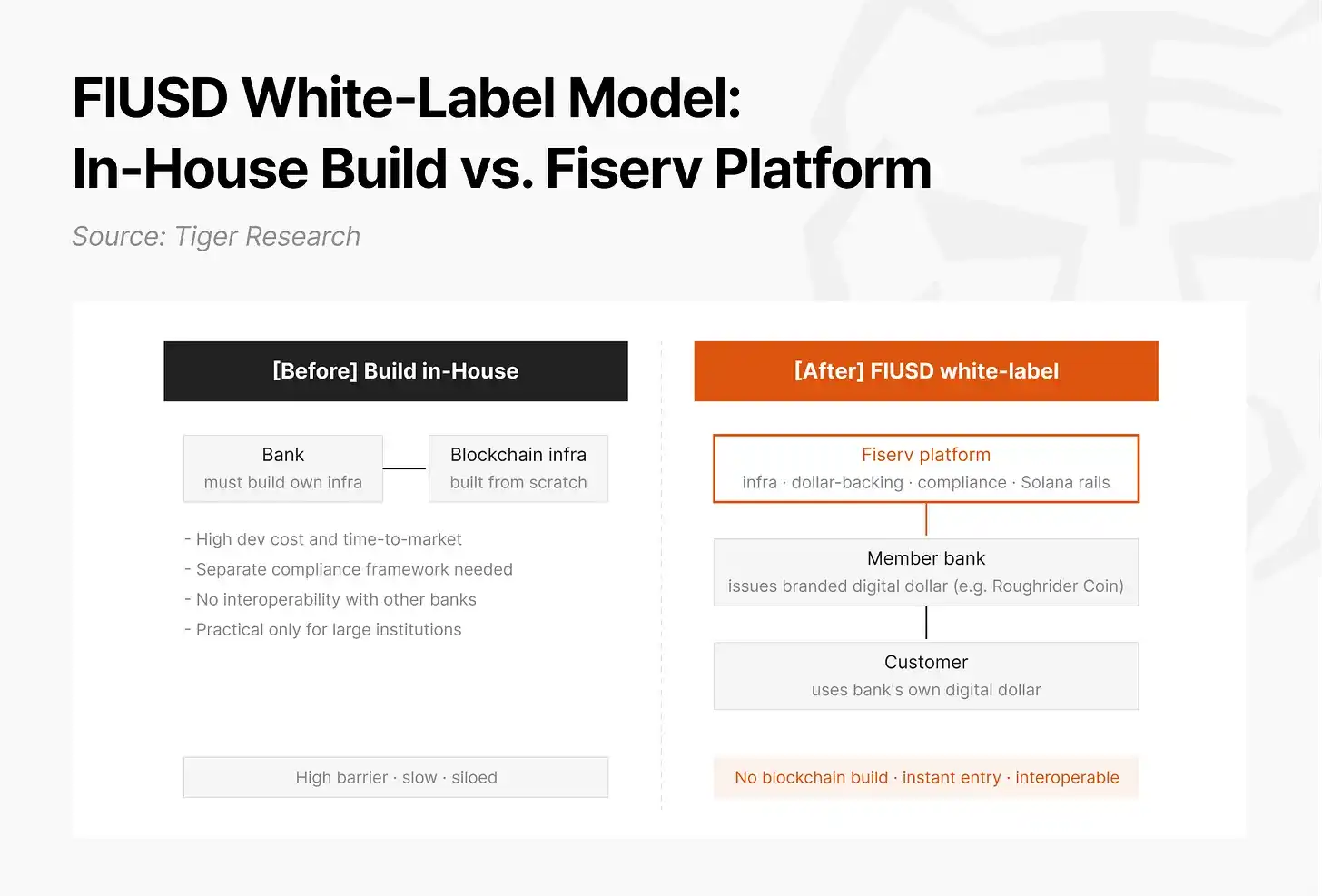

Fiserv: White-Label Stablecoin for Financial Institutions (FIUSD). Fiserv announced it will launch the FIUSD white-label stablecoin platform, scheduled to go live on Solana in July 2026. Under the white-label structure, Fiserv provides the technology infrastructure and dollar backing system, while individual financial institutions issue and provide stablecoins under their own brands. Banks can offer their own digital dollars without building blockchain infrastructure from scratch. Bank of North Dakota (the only state-owned bank in the US) has announced it will launch "Roughrider Coin" on this platform. Fiserv's multilateral network covers approximately 10,000 financial institution clients and 6 million merchants, processing 90 billion transactions annually. It plans to offer FIUSD for free to its member financial institution clients using existing technology.

This structure can be directly referenced by Asian financial institutions. For Korea, the white-label model maps precisely onto the current discussion of whether banks or non-bank institutions can issue stablecoins. Once the Financial Services Commission (FSC) delineates boundaries and establishes rules for won-denominated stablecoins, this model can be transplanted.

4.3 Real-World Asset Tokenization: Closing the Loop from Issuance to Circulation

Orca × Streamex: Compliant RWA Distribution (GLDY). The tokenized listed equities market has long suffered from a disconnect between issuance and distribution. Tokenized assets representing listed stocks have multiple exchanges offering secondary trading paths, but non-equity tokenized securities like bonds, commodities, and private loans lack issuer-controlled, eligibility-gated liquidity infrastructure post-issuance. Issuance technology advances, but distribution infrastructure hasn't kept up.

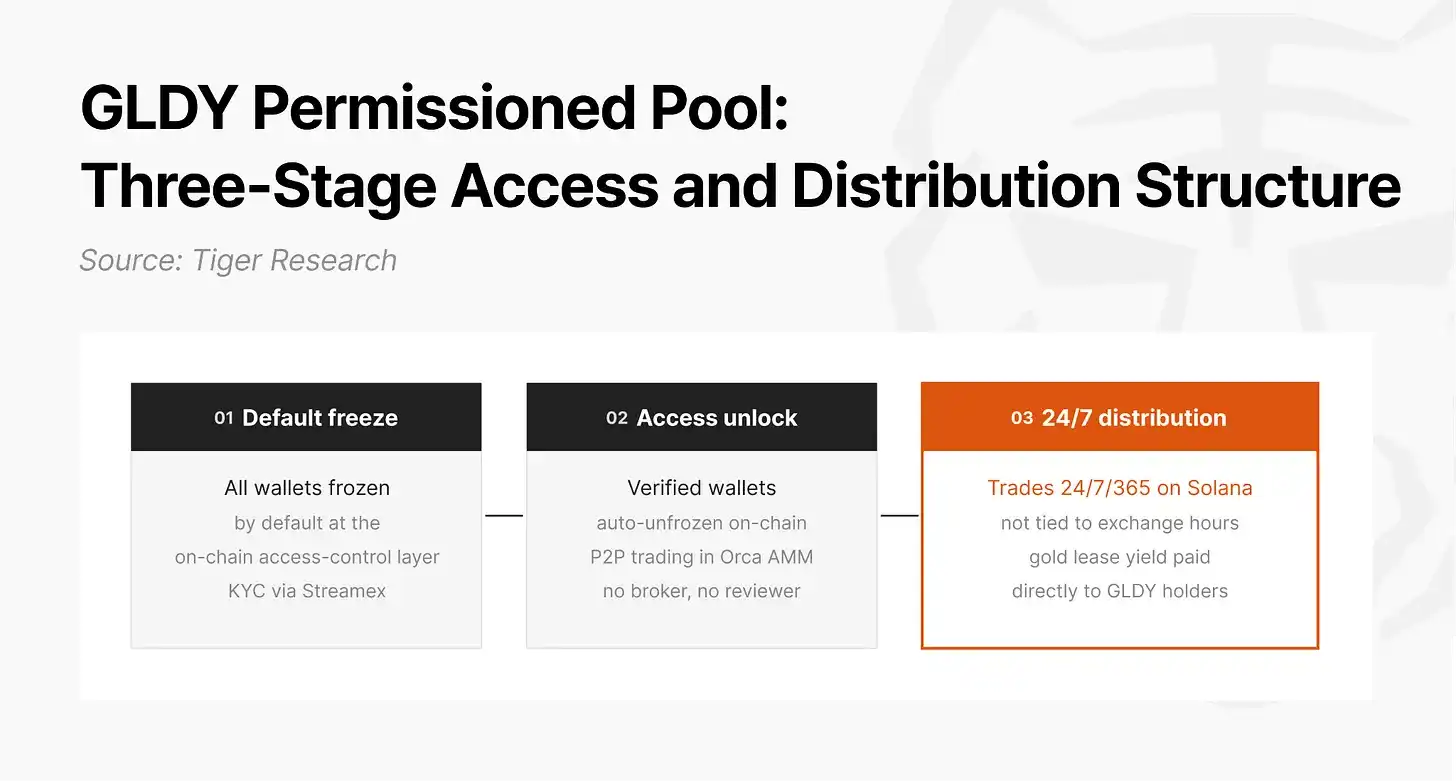

In May 2026, Orca launched permissionless AMM infrastructure allowing issuers to create customizable permissioned pools based on their regulated asset requirements. Nasdaq-listed Streamex, as the first issuer, used this solution to provide secondary liquidity for its gold yield token, GLDY. The GLDY permissioned pool operates in three phases: All investor wallets are frozen by default; only wallets passing Streamex's KYC verification are automatically unfrozen at the chain's access control layer. Unfrozen wallets engage in peer-to-peer real-time trading on the Orca AMM pool, without broker or compliance officer intervention. Unlike traditional gold investment products restricted by exchange hours, GLDY trades 24/7 on Solana, with gold lease contract yield payments from Monetary Metals distributed directly to GLDY holders.

This token-level freeze/unfreeze control mechanism is not limited to gold; it can be directly applied to any regulated asset like government bonds, corporate bonds, and private credit. This is precisely why Orca proposed this structure as the trading infrastructure for its Project Open pilot framework.

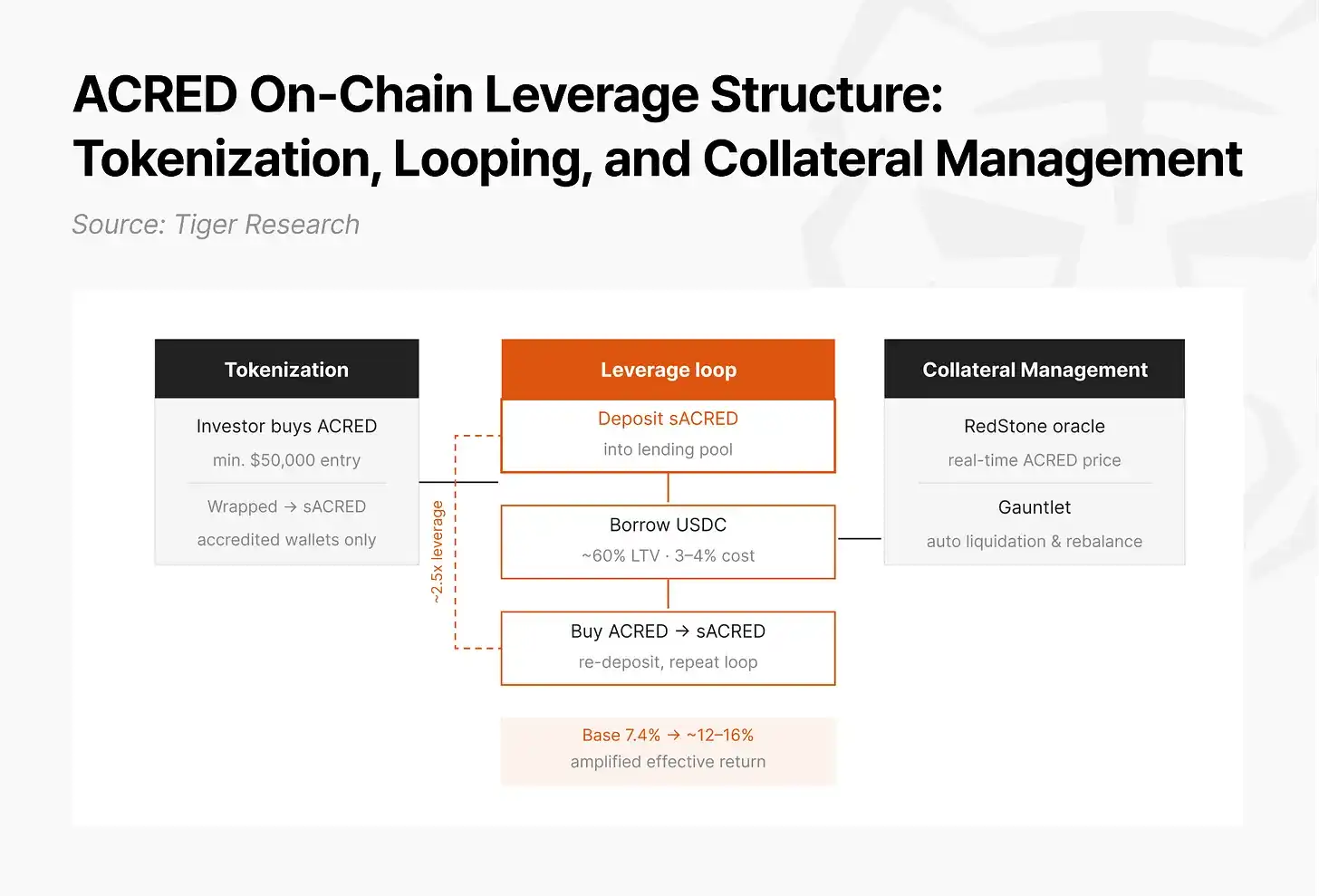

Apollo: Private Credit Tokenization (ACRED). The traditional private loan market, despite its high yield, has two major structural barriers: high minimum investment thresholds restricting access to institutions and ultra-high-net-worth individuals, and illiquidity once invested until maturity. In January 2025, Apollo issued the tokenized tranche fund ARED based on its Diversified Credit Fund (ADCF) through Securitize, with a $50,000 minimum. Within the Solana ecosystem, investors wrap ACRED into an sACRED token, deposit it as collateral in institution-specific lending pools at ~60% LTV to borrow stablecoins (borrowing cost ~3-4%), use the borrowed stablecoins to buy back more ACRED and repeat the cycle, achieving effective leverage of ~2.5x, amplifying the ~7.4% base yield to ~12-16%. RedStone oracles provide real-time ACRED price data, and Gauntlet automatically manages liquidation conditions and rebalancing timing.

This leveraged structure is viable only because of Solana's transaction fees of less than $0.001 and the second-speed collateral posting/release. On infrastructure requiring days to settle or incurring high costs per operation, the same structure is nearly impossible to operate.

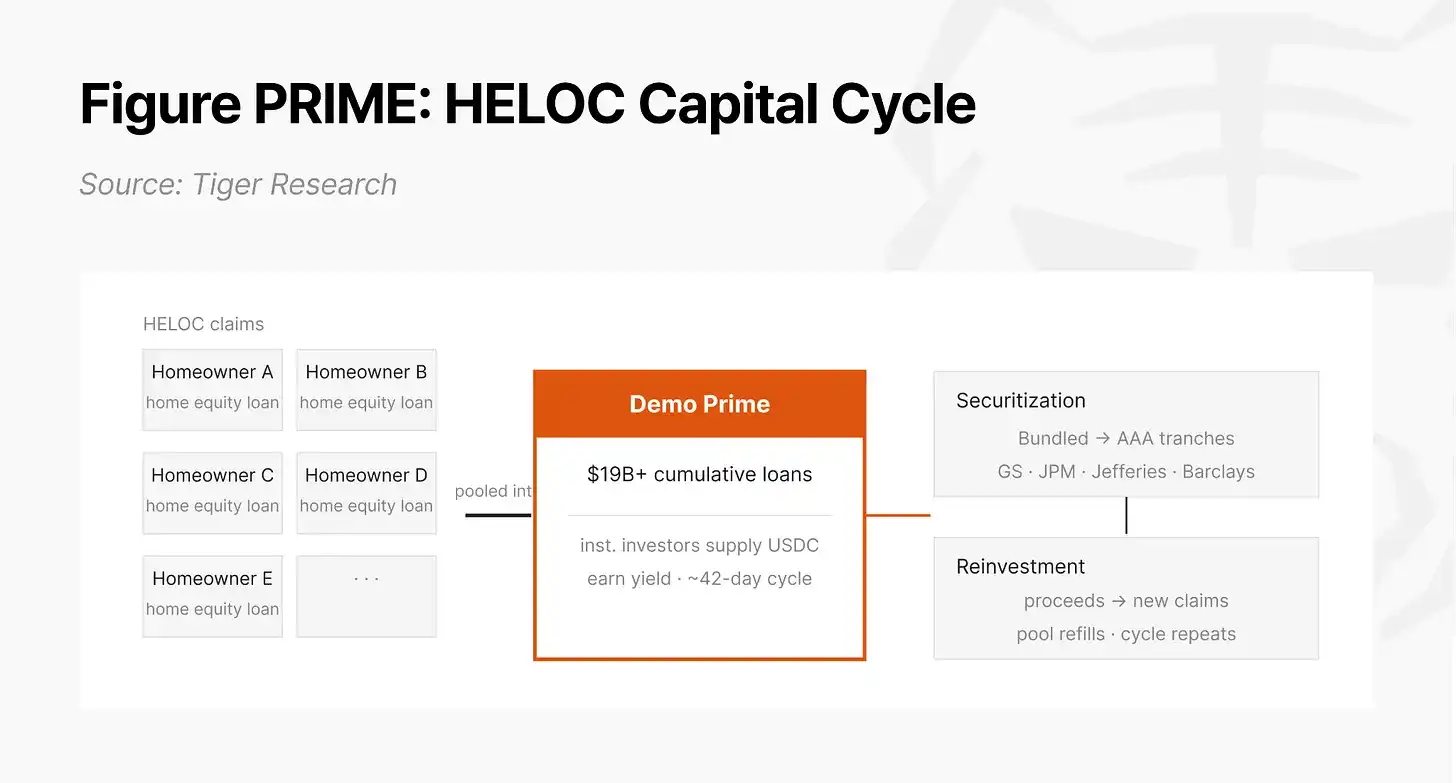

Figure Technology: Liquidity Expansion for Home Equity Lines of Credit (HELOC). Figure is the largest non-bank HELOC issuer in the US, with over $19 billion in cumulative on-chain loans by December 2025, having issued multiple AAA-rated securitizations underwritten by Goldman Sachs, J.P. Morgan, Jefferies, and Barclays. It originally tokenized HELOCs and operated its Demo Prime liquidity pool on its proprietary chain, Provenance, but the closed ecosystem lacked the DeFi liquidity infrastructure to build leverage, limiting capital turnover efficiency gains. In December 2025, Figure launched the PRIME token, bridging loan yield rights from Provenance to Solana via Chainlink CCIP, utilizing the Kamino lending protocol to support up to 9x leverage, with Orca providing AMM depth for the PRIME/PYUSD pool.

Figure's choice of Solana was not a technical preference but a matter of capital efficiency. The net spread between Demo Prime's 9% yield and Kamino's 6% borrowing cost is amplified by the leverage multiple. Unless collateral posting and release can be completed within seconds for under $0.001 on Solana, the economics of this strategy don't hold. Even with its own chain, connecting to public chain liquidity is crucial.

4.4 Infrastructure Proliferation: Formation of Network Effects

The first three domains deal with transformation within their respective fields, while infrastructure proliferation deals with the convergence point of these transformations. Banks issuing bonds on-chain, remittance companies settling with stablecoins, asset managers tokenizing funds—these are not advancing independently but are happening simultaneously on the same infrastructure.

Proliferation occurs at three layers. At the issuance layer, PayPal, Fiserv, Circle, and Tether issue stablecoins or operate issuance infrastructure on Solana, with multiple competing issuers coexisting on the same network. At the settlement layer, Visa expanded stablecoin settlement to Solana, Worldpay migrated merchant transaction settlement to the Solana network, and YouTube adopted PYUSD on Solana to pay US creators. At the access point layer, SoFi enabled its 14.7 million customers to buy SOL directly from their bank accounts and operates its bank-issued stablecoin SoFiUSD, becoming the first federally chartered bank under OCC oversight to place its own liabilities as stablecoins on the Solana public chain; Bullish adopted Solana stablecoins as the primary settlement rail in over 50 jurisdictions and processed $1.15 billion in IPO financing on the Solana network.

When issuance, settlement, and access points operate on the same network, network effects emerge. Tokens issued by a bank are settled by a payment company, and consumers hold the asset in their banking app, forming a closed loop. The more participants, the greater the utility for each. The formation of Internet Capital Markets will accelerate the moment this closed loop passes a critical threshold.

5. Regulatory Landscape: The Established and The Unresolved

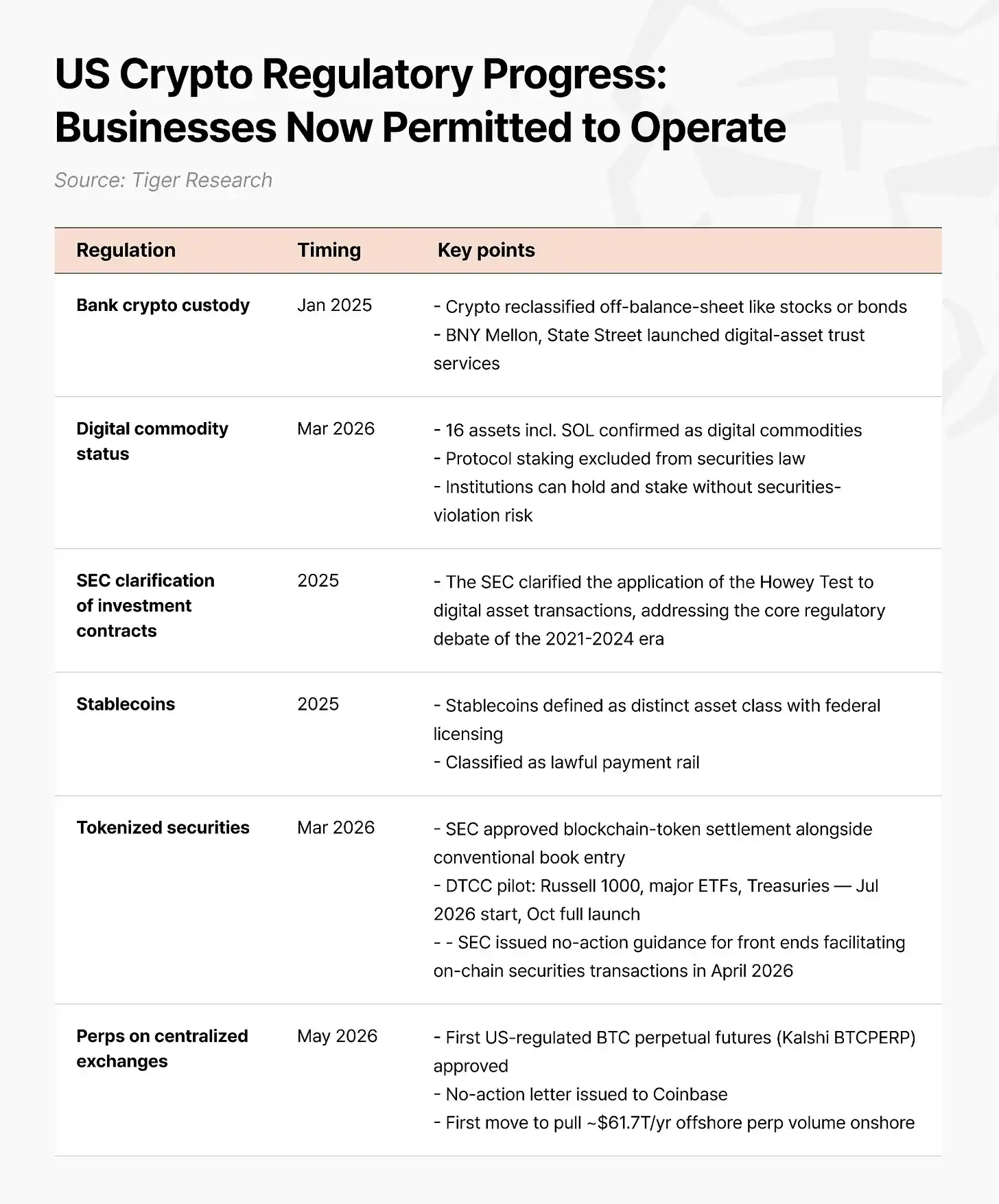

Areas Already Within Regulatory Frameworks cover a broad scope. Regarding bank custody of crypto assets: After the repeal of SAB 121, crypto assets are classified as off-balance-sheet assets, and major custodial banks like BNY Mellon and State Street launched digital asset trust services. Regarding digital commodity status: 16 assets including SOL were confirmed as digital commodities, protocol staking was excluded from securities law, providing legal security for institutional investors to buy, hold, and stake legitimately. Regarding stablecoins: The *GENIUS Act* defines stablecoins as a distinct asset class, not securities or deposits, imposing federal licensing standards on issuers. Regarding tokenized securities: In March 2026, the SEC approved Nasdaq to trade specific securities in tokenized form; DTCC confirmed a limited pilot launch in July and full launch in October, covering Russell 1000 component stocks, major index ETFs, and US Treasuries. Regarding perpetual futures: The CFTC approved Kalshi's Bitcoin perpetual futures contract for the first time, taking the first step to bring offshore perpetual futures liquidity (~$61.7 trillion in 2025) into the US regulated system.

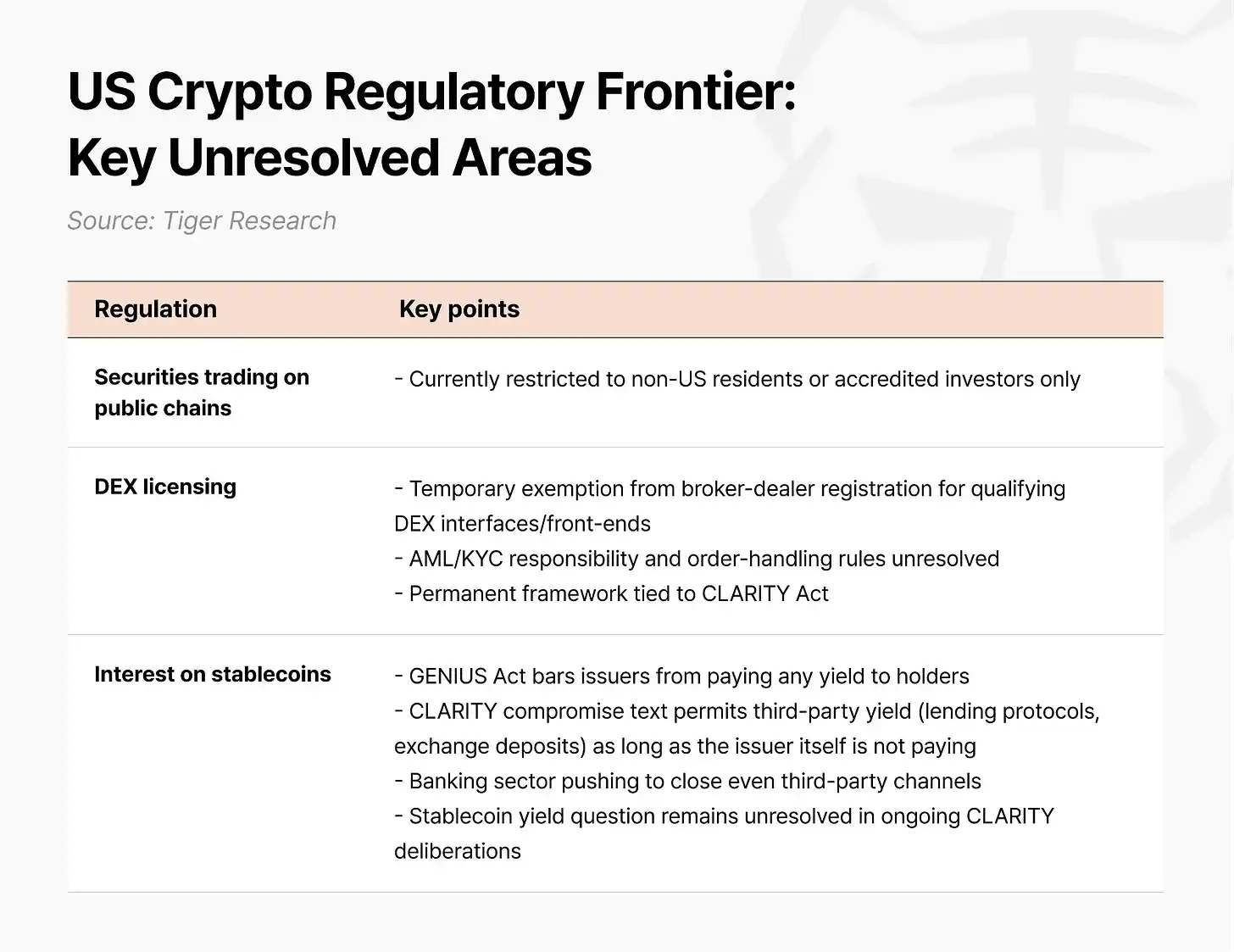

Unresolved Frontier Areas are equally critical. Free stock trading on public chains is currently limited to non-US residents (Reg S) or accredited investors (Reg D). While the SEC has discussed an innovative exemption for "third-party stock tokenization" without listed company consent, strong opposition from traditional finance (Nasdaq, SIFMA, etc.) over liquidity fragmentation leaves final approval uncertain. Regarding DEXs: The SEC issued a five-year sunset provision temporary guidance in April 2026, but key regulatory gaps remain, such as the assignment of AML obligations and order handling responsibilities. Regarding stablecoin interest payments: The *GENIUS Act* strictly prohibits issuers from paying any form of yield to holders, with banks even lobbying to close third-party channels.

The *CLARITY Act* is the key legislation to comprehensively address these issues. It would define the overall market structure for digital assets, create a spot market regulatory framework for digital commodities, and direct the SEC and CFTC to conduct rulemaking to allow businesses to operate on public chains. However, the probability of this bill passing in 2026 is around 50% or lower. Bipartisan disagreement exists on ethics clauses restricting the President and senior officials from profiting from crypto businesses. The roughly four-week legislative window in the Senate from mid-July to early August is effectively the final deadline for passage this year. Missing this window pushes the timeline into the 2026 midterm election period, where consensus will be more difficult to achieve in the pre-election landscape.

6. The Technical Reasons Behind Institutional Choice

Global financial institutions are not choosing Solana out of preference, but because it meets the technical requirements of institutional finance.

Settlement Economics. Solana's time to finality is ~0.5 seconds, with an average transaction fee of $0.0013. If each collateral posting and release added several dollars in cost or took a day to settle, leveraged strategies would be consumed by costs before generating any return.

Programmable Compliance. The Token-2022 standard embeds features like freezing, confiscation, whitelist access, and zero-knowledge proof encrypted balances at the token level, shifting compliance from a post-hoc measure relying on external systems to a pre-designed element built into the protocol layer. Transaction amounts are encrypted via ZK proofs, preserving origin and destination on the public ledger, but only the sender, receiver, and designated auditors can see the amount. This is a design ensuring both auditability and confidentiality.

Institutional-Grade Stability and Evolving Infrastructure. Addressing the vulnerability of a single validator client, Solana is evolving towards a multi-architecture running multiple independent validator clients. The technology roadmap aims to shorten time to finality from the current ~0.5 seconds to ~150 milliseconds and introduce identity verification structures before transaction execution at the protocol layer.

Full Operational Sovereignty: Contra. For institutions where all transactions and balances cannot be exposed on a public ledger, or which need internal control over validation and governance, Solana offers the Contra option—independent of the public mainnet, using the performance foundation validated on the public network but resetting operational conditions to meet institutional needs.

7. The Strategic Execution Framework for Asian Institutions

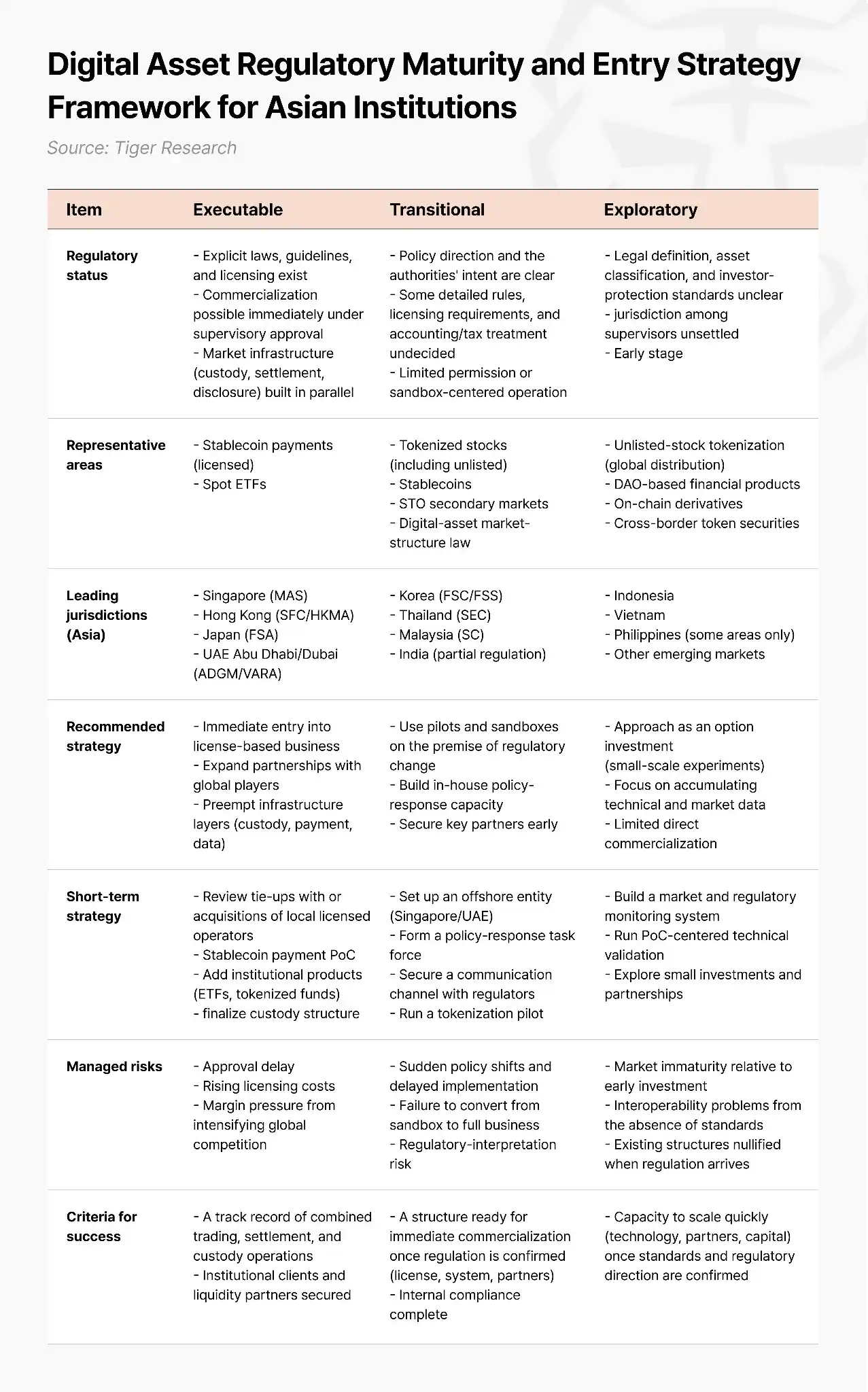

The phase for Asian financial institutions to design infrastructure from scratch as first movers has passed. The pragmatic path is to be fast followers, adopting the infrastructure and regulatory references validated in the US market to reduce trial-and-error costs. The criterion for deciding to enter is not whether a policy exists, but whether it can be truly executed: the presence of clear laws, guidelines, and licensing systems, and whether market infrastructure (custody, settlement, disclosure) has been built in parallel—these are the keys distinguishing what is commercially viable now from what is not.

Executable Stage (Singapore MAS, Hong Kong SFC/HKMA, Japan FSA, UAE ADGM/VARA): Clear licensing systems and market infrastructure are in place; commercialization can commence immediately. Representative areas include licensed stablecoin payments and spot ETFs. The risk here is delay, not entry. Institutions entering first can lock in operational track records and liquidity partners early; latecomers will pay a gap as the price.

Transition Stage (South Korea FSC/FSS, Thailand SEC, Malaysia SC, parts of India): Policy direction is clear, but detailed rules and licensing requirements are not yet determined. Representative areas include tokenized stocks, stablecoins, STO secondary markets, and digital asset market structure laws. What is needed now is not full-scale commercialization, but building a structure that can be immediately converted into commercial operations upon regulatory confirmation. Korean institutions are at this stage. Starting preparation only after regulatory confirmation is too late, as institutions that have already arranged licenses, systems, partners, and internal compliance will not be on the same starting line as those that haven't. For institutions where domestic regulation progresses slowly, an offshore path is an effective alternative: establishing an entity in a jurisdiction with a complete framework like Singapore or the UAE for pilot projects, accumulating compliance systems and counterparty networks, and transferring capabilities back home once domestic regulations are ready.

Exploration Stage (Indonesia, Vietnam, the Philippines in certain areas, and other emerging markets): Legal definitions, asset classifications, and investor protection standards are not yet clear; jurisdictional boundaries between regulators are not yet delineated. The approach should be to accumulate technology and market data through small-scale experiments, maintaining the capacity to scale rapidly once standards and regulatory directions are confirmed. At a stage where asset classifications are not yet determined, committing resources to one side is itself the biggest risk.

8. Conclusion: The Window is Open, But Its Duration is Uncertain

Internet Capital Markets are no longer a concept but an operating reality. The simultaneous choice of Solana by global institutions with varied goals—J.P. Morgan, State Street, Franklin Templeton—is not a matter of preference but because it meets their respective technical and structural needs: institution-grade compliance capabilities embedded within the asset itself (Token-2022), a throughput record tested by extreme traffic and sudden market volatility, and a complete ecosystem accumulating everything from Washington policy engagement to real-time settlement and clearing infrastructure.

These three points are not a verdict on one infrastructure being superior to another, but an observation of where institutional capital is actually converging. Validation is not reflected in price, but in who has placed what and where.

The variable left for Asian institutions is no longer "whether to enter," but the order of entry and the point of entry. Reference cases have been validated; standards are not yet solidified. This interval of "validation complete but standards not yet solidified" is precisely the window available to fast followers. How long it will remain open is uncertain.

To read the full report, click the original link.