1. BTC discharge shock

The daily K line chart shows that after BTC retreated for four consecutive trading days, the trading volume has reached its peak in the past month. With the adjustment, the selling pressure also reached its peak on November 2. On the news side, the Federal Reserve raised interest rates again by 0.75 basis points to 3.75% - 4.00%, which is the fourth consecutive meeting of the Federal Reserve to announce a 75 basis point increase in interest rates. Affected by this, the BTC price also experienced a short-term strong earthquake of 3.68%. The performance of volume and price suggests that BTC, an investor, has once again withstood the impact of interest rate hikes. At present, the price is still above the middle track of Bollinger Line.

2. BTC contract position decline

The position of BTC contract showed signs of continuous decline. On November 3, the position of BTC contract fell to 8.89 billion US dollars, a decrease of 1.76 billion US dollars, or 17%, compared with the peak of 10.65 billion US dollars on October 26. The position of BTC contract ushered in the most important decline since October, which means that the price amplitude that contract investors can bear in the near future has increased. At the same time, it means that BTC is easier to choose a breakthrough direction in the near future.

3. ETH ready for lifting

The daily K line chart shows that there is limited room for ETH price to retreat in the short term. As the rebound continues, ETH still maintains a large-scale operation. This shows that the recent ETH price rebound trend is expected to continue. Until the trading heat cools down, investors can absorb the market at a low price. In terms of contracts, the long short ratio of ETH rebounded, further indicating that spot prices will strengthen.

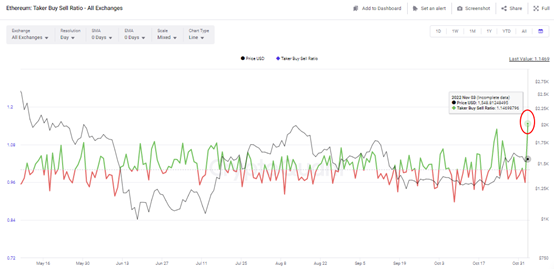

4. ETH long short ratio continues to rise

With the rebound of the long short ratio of ETH contracts, the value has reached the peak level of the recent high of 1.146. That is to say, compared with 1.129 on October 23, many parties are more optimistic about the short-term breakthrough performance of ETH price. In terms of trading, attention can be paid to ETH bargain buying opportunities. Considering that the long short ratio has fluctuated less in the past three years and is currently the highest in three years, it has a better effect on the market, further verifying that ETH's market entry trading opportunities are relatively reliable.

5. AR short line volume soars

In the short-term surge phase of AR, the trading volume was significantly enlarged, and the volume started on November 3 was the same as that on October 30. The short-term capacity has reached 20 times, and the AR has been continuously pulled up to the K line for 8 times and 30 minutes. In the phase of AR surge and fall, the trading volume shrinks significantly relative to the phase of price rise, indicating that bulls still have the opportunity to raise prices for a second time. The profit taking market did not completely escape, and focused on the rebound opportunity after the withdrawal of AR. From the point of view, pay attention to the low absorption opportunities of AR above $15.