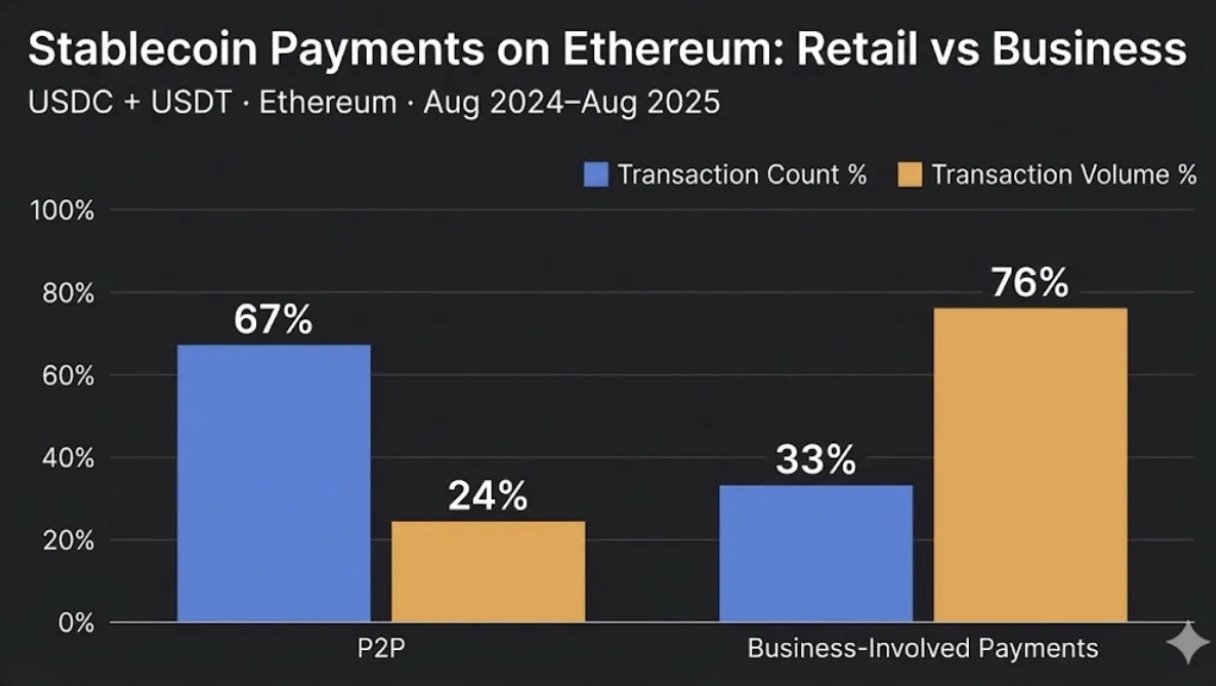

Data shows 67% of Ethereum transactions involving the stablecoins USDT and USDC are P2P in nature, but the majority of volume lies elsewhere.

Business-Related Ethereum Stablecoin Transactions Dominate Volume

In a new post on X, Ethereum Foundation head of ecosystem James has shared some numbers related to stablecoin transactions on the ETH blockchain. Stablecoins refer to cryptocurrencies that have their value pegged to a fiat currency.

As these assets are relatively “stable” by nature, they have quickly established themselves as the preferred mode of payments, with their volume surpassing combined that of the top five non-stablecoin cryptocurrencies.

But what does the nature of these transactions look like? Below is the data posted by James, showcasing how the transfers related to the Ethereum versions of USDT and USDC break down between retail and business payments.

Businesses seem to be dominating in terms of the volume | Source: @Snapcrackle on X

As is visible in the chart, 67% of USDT and USDC transactions on the Ethereum network that occurred between August 2024 and 2025 were of the peer-to-peer (P2P) type. Such transactions are usually a sign of activity from retail users.

The small size of the users being involved could be why the transaction volume share of P2P transfers was just 24%. In contrast, business-involved payments made up for 76% of the volume, despite occupying a transactions share of just 33%.

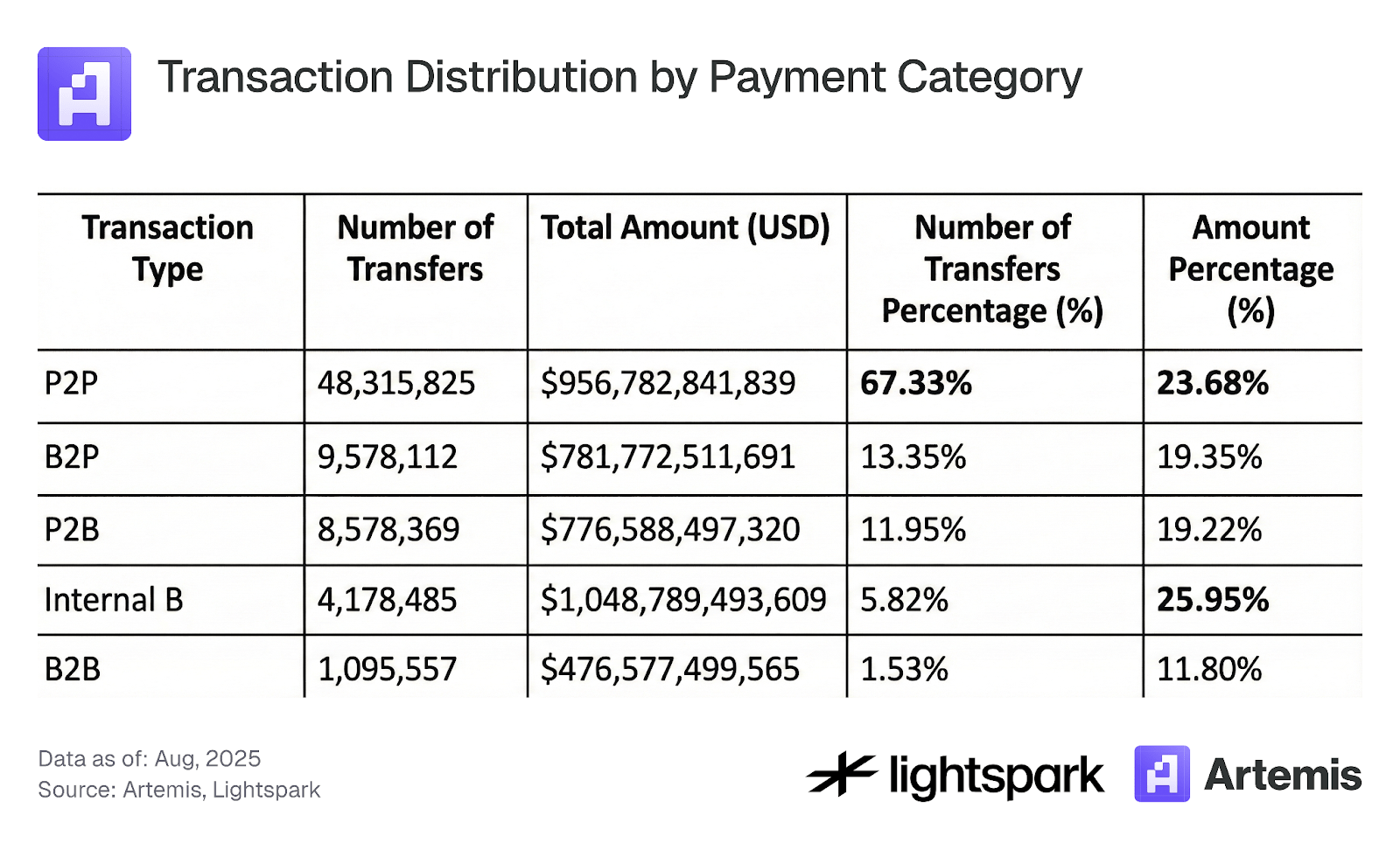

The Ethereum Foundation member sourced the data from Artemis’ report on Ethereum stablecoin payment usage. While stablecoins pegged to various currencies exist, Artemis focused on the USD-tied USDC and USDT as they are by far the most popular options, occupying 88% of the sector’s market cap.

These coins circulate on several blockchains, but Ethereum is currently the most dominant network, hosting more than 50% of the global stablecoin supply. “We also only focus on transfer transactions and exclude any mint, burn, or bridge transactions from our analysis,” noted the report.

Artemis has broken down how it classifies transactions. Transfers are considered P2P if they occur between the externally owned accounts (EOAs) of two separate users.

Determining whether a transaction is P2P can be tricky, however, given that it’s not always possible to determine whether two accounts are owned by different entities. Problems also arise for wallets owned by exchanges and other centralized entities. “In our dataset we are able to label many institutional and firm EOA wallets; however, the labeling is not perfect and some EOA wallets that are owned by firms and are not documented in our dataset can be mislabeled as individual wallets,” explained the report.

The second category is business-to-business (B2B), naturally consisting of the moves taking place between two institutional EOAs. Transactions between the same institutional entity fall inside the “Internal B” label.

Finally, there is the person-to-business (P2B) category, accounting for the transfers happening between individuals and businesses. James’ chart clubs all the business categories into one.

The numbers related to the stablecoin transactions on the Ethereum network | Source: Artemis

ETH Price

Ethereum made recovery above $3,000 earlier, but it seems the coin has once again faced a pullback as its price is now back at $2,950.

The trend in the ETH price over the last five days | Source: ETHUSDT on TradingView