Written by: Gino Matos

Compiled by: Chopper, Foresight News

On July 1st, Ethereum Institutional was announced, consolidating the Ethereum Foundation's marketing efforts into one team responsible for pitching Ethereum's tokenization and stablecoins to banks and asset managers.

Just days earlier, Ethlabs debuted, formed by five former senior Ethereum Foundation researchers, focusing on two main areas: enhancing on-chain settlement efficiency and refining the ETH monetary narrative.

Bitmine, Sharplink, and Ethereum co-founder Joe Lubin jointly provide funding for the two new organizations.

The launch of these two major new institutions coincides with a continued outflow of senior personnel from within the Ethereum Foundation. On June 18th, co-executive director Hsiao-Wei Wang announced her departure, following the resignation of Tomasz Stańczak. Over the past five months, at least eight executives have left the Ethereum Foundation.

As early as March 2026, the Ethereum Foundation released a new mandate, redefining its position: solely as a guardian of the principles of self-sovereignty, censorship resistance, open-source code, privacy, and security, not claiming to be Ethereum's parent company nor holding ultimate decision-making power over the protocol. This positioning deliberately leaves a business vacuum, with commercial deployment work outsourced to external organizations.

Ethlabs takes on the technology R&D and asset value narrative segments, responsible for improving the underlying infrastructure and crafting a complete logic for ETH as a monetary asset to address institutional concerns about entering Ethereum. Ethereum Institutional is fully responsible for business development, converting industry interest into real deployed capital by building industry forums, maintaining institutional networks, and customizing pitch plans.

The core reason for the two teams operating independently from the Foundation lies in the Foundation's neutral stance being incompatible with commercial work. A neutral standard-setting body simultaneously acting as an ETH promotional team and corporate sales department would directly harm its own credibility.

Thus, Ethereum's three-power structure is formed. The Foundation is responsible for legitimacy and long-term protocol value, Ethlabs for ETH value capture and technical R&D, and Ethereum Institutional for corporate business promotion.

Ethereum Institutional revealed that the team has already engaged with over 500 tier-1 banks, global asset managers, sovereign wealth funds, custodians, and market infrastructure service providers. Its hosted Ethereum Institutional Summit gathers over 150 financial executives from institutions managing a total of $250 trillion in assets. This massive scale of industry resources is also a key reason for the official split of operations and the establishment of independent entities rather than housing them as auxiliary Foundation businesses.

Delegating corporate business and ETH value promotion to external organizations solves the execution disconnect at the Foundation level, but it also means that giants holding vast amounts of ETH and sitting on massive balance sheets control the communication channels pitching to Wall Street. Convenience and independence are opposite directions, and Ethereum has chosen convenience.

Supporting Ethereum's Wall Street Push are Companies Holding Massive Amounts of ETH

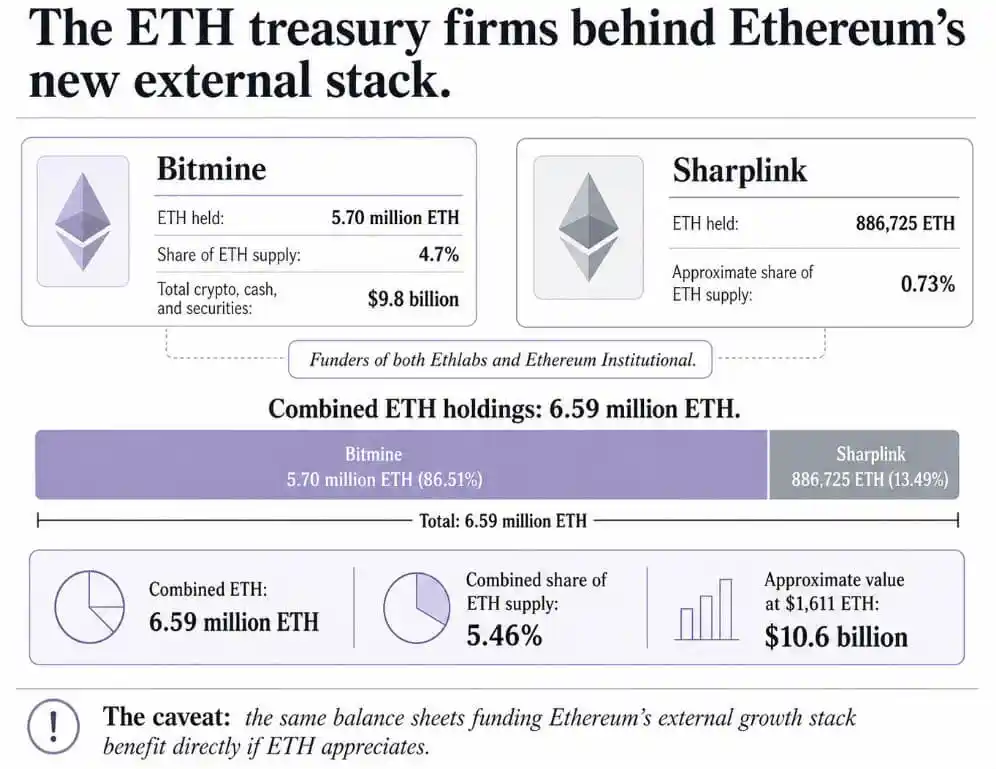

Bitmine currently holds 5.7 million ETH, accounting for 4.7% of ETH's total circulating supply. Combined with cash and marketable securities, its total asset size reaches $9.8 billion. Sharplink holds 886,725 ETH and added 10,000 ETH on June 28th at an average price of $1,611.

The two institutions collectively hold 6.59 million ETH, representing 5.46% of the 120.7 million circulating supply, with a total holding value of nearly $10.6 billion at current prices. Bitmine itself has a market cap of $6.55 billion, while Sharplink's market cap exceeds $1 billion.

If this operational split model proves successful, the two funding companies will directly benefit: improved underlying infrastructure and more mature institutional business will increase demand for ETH. Given their massive holdings, even minor ETH price fluctuations can translate into hundreds of millions of dollars in asset value changes. Ethereum co-founder Joe Lubin, supporting both non-profits, sits at the core of this interest system, with Bitmine and Sharplink's financial gains deeply tied to Ethereum's ecosystem development.

PeerDAS has already launched, potentially increasing Layer 2 data availability capacity about tenfold, while Glamsterdam, planned for the second half of 2026, aims to achieve base-layer scaling, parallel transaction processing, and larger block payloads.

An academic report from June 2026 shows that transaction throughput on the mainnet and Layer 2 networks has doubled; median mainnet fees have dropped from over $2 to below $0.02, while Layer 2 fees have fallen by over 95%, as low as $0.0015.

The report also provides long-term performance predictions: before 2034, Ethereum mainnet transaction processing capacity will remain under 100 transactions per second; not until March 2029 will Layer 2 throughput surpass Solana's, but by then Layer 2 fees will be far lower than competitors. Ethereum's ability to attract institutions relies almost entirely on Layer 2 scaling and industry standard adoption, which is precisely the core domain of Ethlabs.

Two Potential ETH Price Trajectories Will Determine the Ultimate Direction of This Structure

The bullish case is that Ethereum already possesses considerable scale. Ethereum currently hosts $157 billion in stablecoin market cap, representing over half of the global stablecoin total; DeFi locked value stands at $37.2 billion, accounting for 62% of the industry. RWA.xyz data shows Ethereum's tokenized real-world asset (RWA) size at $15.8 billion, with the entire sector totaling $31.52 billion, firmly holding the top position among public blockchains.

Citibank predicts the global tokenized real-world asset market will expand from the current $17 billion to $5.5 trillion by 2030, with a lower bound of $2.7 trillion and an upper bound of $8.2 trillion. If Ethlabs continues to iterate on infrastructure and Ethereum Institutional can convert network relationships into actual deployed capital, holding giants like Bitmine and Sharplink will become early beneficiaries, Ethereum could become the default settlement layer for compliant digital assets, and ETH asset value would rise accordingly.

The bearish case starts with price. Citibank lowered its 12-month ETH price target from $3,175 to $2,240, citing weak ETF demand and negative fund flows, and set a bear market scenario for ETH at $1,094.

Standard Chartered holds the completely opposite view, maintaining that ETH could reach $4,000 by the end of 2026. The huge divergence in expectations between the two major institutions reflects the high uncertainty in the short-term market outlook.

If ETH remains weak long-term, with Bitmine and Sharplink stock prices persistently trading at a discount relative to their held assets, the two companies' ability to fund the two non-profits will continue to shrink. Even if Ethlabs and Ethereum Institutional can maintain operations, funding stability will significantly decline. The market will continually question whether the core purpose of establishing these two institutions was to pump the ETH price rather than build genuinely usable institutional-grade infrastructure.

Regulatory tailwinds support the bull case but do not guarantee a price rise. The U.S. GENIUS Stablecoin Act of 2025 established a federal regulatory framework for stablecoins; the Visa, Mastercard, Coinbase consortium subsequently launched the Open USD stablecoin. Regulatory improvements will bring institutional settlement volume to all public chains, not a unique benefit for Ethereum. McKinsey offers a more conservative prediction, estimating the tokenized market size at around $2 trillion by 2030, forming a stark contrast with Citi's high expectations, indicating enormous disagreement on the industry's growth potential itself.

Summary

By splitting operations and establishing two independent organizations, Ethereum has resolved the inherent contradiction between the Foundation's neutrality and commercialization. However, with both institutions funded entirely by companies holding massive amounts of ETH, this structure presents both advantages and risks.

On the positive side, specialized organizations focusing on infrastructure and engaging Wall Street could position Ethereum as a universal settlement layer for tokenized finance. On the risk side, the ecosystem's expansion system is completely tied to the balance sheets of the holding giants, with ETH market performance directly determining funding supply. Both scenarios will coexist, and the ETH price a year from now will determine which trend dominates.