从6月份开始,加密资产的行情都受到美联储加息政策的影响,而且这个影响还特别大,接下来两天又是一个关键的时间窗口,本周三,美国最新一起CPI数据将公布,这是美联储最重要的一个加息参考指标,我今天看到的消息是9月再加息75个基点的概率是67%。其实,加多少不是关键,关键是有没有迹象现实CPI已经见顶,如果CIP见底,美联储政策就会调整,甚至结束紧缩政策,这相当于给全球的资本市场松绑。

关于这一点,马斯克是认为,通胀已经见顶,机构也普遍认为,美国本月通胀率将从9.1%的水平放缓。

当然,关键还是要看数据,只要CPI出现降低,低于9.1%,我估计市场多头就会猛炒一波,毕竟大家都要吃饭,市场也太平缓了,零星的利好就会被放大。

因此,短期行情走势,我认为本周大概率会继续反弹,周三以前维持震荡,数据公布,如果利多,就会快速突破,吃饭行情还继续,大家多些耐心。

长期的趋势,相对而言,估计就会很复杂。前两天,美国非农就业人口增加了52.8万人,是今年2月以来的新高,而这个指标是美联储和白宫判断经济是否衰退的重要指标,强劲的就业预示着衰退的可能性大大降低了,但马斯克却认为“接下来,我们还将经历 18 个月的衰退”,虽然马斯克这个家伙,在币圈的声誉不太行,但是他的观点,参考性还是很强,去年11月,他就一直在谈今年3月后估计会出现金融危机,比特币也正好是哪个时候见顶的。

对此,很多市场分析人士也认为,事实上美国的经济已经处于技术性衰退了。这也反映出宏观经济走势的复杂性,物价的下行也是一个复杂、漫长的过程,不可能一蹴而就,机构也普遍预测,鉴于第二季度生产率增长可能再次为负,加上强劲的非农就业报告显示,过去三个月工资增长再次加速,潜在通胀率可能在4%左右。即使明年整体通胀率下降,核心CPI可能会在未来几个月回升。

面对这种不确定性,从宏观层面就决定了金融市场也好,加密资产也好,很难有趋势性的大行情,这也是我为什么认为熊市还需要折腾很长一段时间的原因,整个加密圈,上半年,挤压了不少泡沫,流动性被洗出去不少,资金机构非常脆弱,大河无水小河干,在宏观经济形势没有出现明显好转迹象之前,我是认为大行情可能性非常低。

这个情况下,一堆由镰刀组成的分叉大军,能有啥好结果,我是看不到,最终大概率也是要归零。所以,分叉币我是建议大家不要碰,免费的糖果可以撸一撸,拉一波就要跑,投机性太强了,搞不好,偷鸡不成蚀把米。

不过这个分叉,对ETH确实有影响,对LDO这些锁币的平台也有影响,原因是,根据规则,STETH啥的,肯定是不能空投到糖果的,不仅是stETH不行,任何第三方的发行的xETH都不行,那大家就会赎回自己的ETH,等待分叉,这可能又会形成一轮挤兑,CRV、LDO等,都会面临这个问题,甚至一些交易所与ETH流动性挖矿相关的产品。对ETH短期是个利好,应该可以刺激一波需求,但我总觉的这个影响会很小,到时候,我们再跟踪一下。

就市场本身而言,除了不温不火的利好,利空也不少。

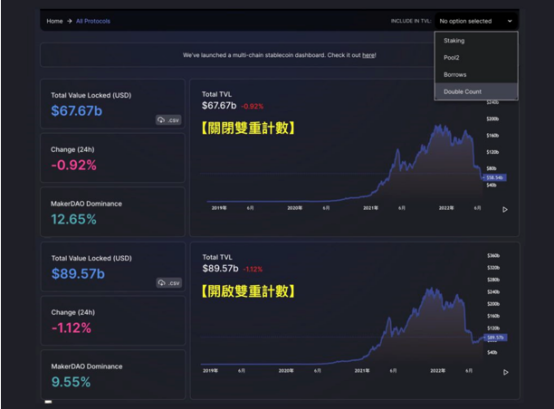

据悉,DeFi 数据分析平台 DeFiLlama ,从8月5日起,强制关闭了重复计数,导致DeFi 总锁仓量骤降 220 亿美元,这等于是撕掉了很多DeFi的遮羞布。

排名第一的以太坊:默认显示的总锁仓量为 390.8 亿美元;开启“双重计数”后提高为 582.1 亿美元,大约灌水 191 亿美元。排名第五的 Solana ,默认显示的总锁仓量为 19.8 亿美元,开启“双重计数”后提高为 25.8 亿美元,约灌水 6 亿美元。

我估计solana的水分还远不止这点,去年 11 月,它的总锁仓量(TVL)一度突破百亿美元,前几天被爆一对兄弟档在该生态匿名创建了 11 个协议,由于高达数十亿美元在两个协议之间重复计算,Saber 及 Sunny 在 Solana TVL 达到高峰时 时占据了 75 亿美元,水分大约有7成……,成了当之无愧的币圈灌水大师,据说这哥俩现在现在正打算转战Aptos……

哎,这让后期公链们的故事都不太好讲了,从这个角度,solana的艰难时刻,估计还远没有到,正如我上一期所说,这个币种短期可能会反弹,但长期更艰难的时候估计还没有。

这也提醒我们,参与热点的操作可以,但是千万别太把数据和信息太当真,把短期的炒作当成是长期的价值,这也正是大多数韭菜被深套的原因。

我经常说,人造风景终难久,独木不知归大盘,假的就是假的,在熊市都会一一暴露出来,经过熊市洗礼的项目,反而在后期,会迎来长远的发展。

这就是所谓的,不可胜在己,可胜在敌。

在我们的交易中,也是如此,先要让自己立于不败之地,确保本金安全,然后明显的机会出现,或者主力犯错,我们才能果断介入,获得好的结果。